JDWPF - Wetherspoon: World-Class Operator

2023-04-25 05:59:51 ET

Summary

- British pub chain Wetherspoon has passed pre-pandemic revenues and is profitable again.

- I think its business model is unsurpassed and it stands to gain not lose from a contracting pub sector.

- The shares are up over half in 2023 but still look cheap given the proven potential of the business model.

I continue to see Wetherspoon ( JDWPF ) as a world-class business in the U.K. stock market that is not fully understood and so offers substantial value. I maintain a buy rating.

My last piece on the name was the bullish October 2020 piece “ Revisiting The Long-Term Investment Case For J D Wetherspoon ”. Since then the shares have declined 27%.

Perception and Reality

It has been a very challenging few years for leisure operators in the U.K. as in other markets. Pubs were hard hit by lockdowns on multiple occasions, inflation making the value equation of drinking at home versus out of home better than before and also the demographic: pubs have a lot of older punters, some of whom have been permanently scared by government handling of the pandemic when it comes to congregating in crowded public spaces. Soaring energy prices and shortages both of product and staff have added to the sector’s woe. The net impact is that dozens of pubs are closing monthly in the U.K. In the first quarter of this year, 150 closed in England and Wales . Between 2000 and 2020, the number of pubs in the U.K. fell by around a third and I expect that long-term trend to continue.

Based on that, some investors remain bearish on Wetherspoon. I, on the other hand, am bullish in the long term for a couple of reasons.

From a pub perspective, I think the market is large even if declining. I see Wetherspoon as the best operator in the space with a unique proposition, which means that it could stand to benefit as competitors fold.

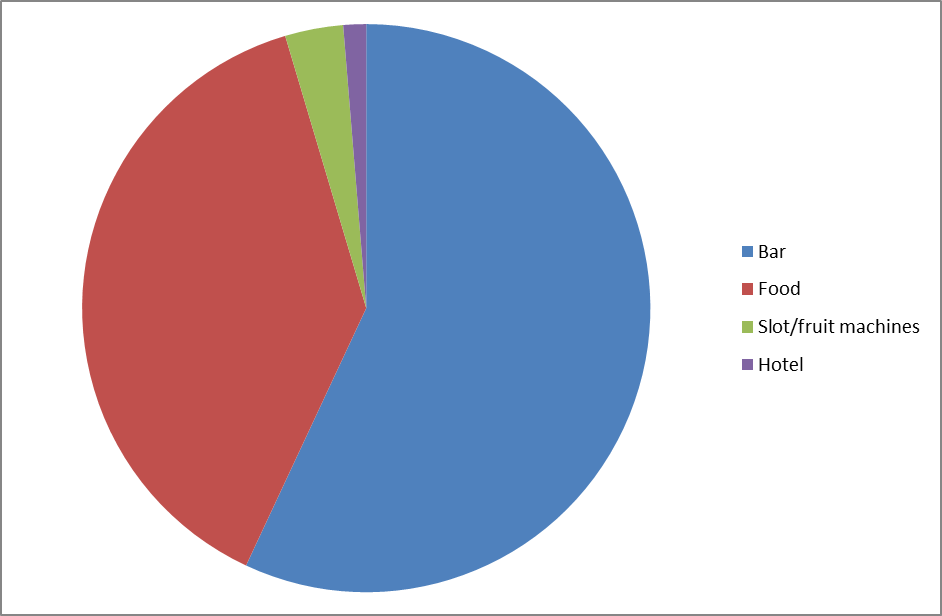

But there is also a question of how to conceptualise Wetherspoon. Yes it is a pub chain (albeit with a smallish hotel operation on the side). But its role is not purely that of the traditional English pub, in my view. Its all-day coffee offering at a very attractive price takes business from cafes not pubs. Its food offering is similarly a threat not only to pubs, but also other eateries. A breakdown of the chain’s revenue in its first half makes the point.

Chart: first half revenue by source (chart compiled by author based on data in company report)

{kind=link}

So although I do expect ongoing difficulties for the pub trade in the U.K., I do not think that necessarily means that Wetherspoon will share the pain equally with the trade in general.

Set against that is evidence of challenges to Wetherspoons’ own estate. It closed 11 pubs in the first half but opened only 2. Last year and this year the chain has announced plans to sell a few dozen pubs although in the current market that has proven difficult. Seen negatively this suggests that the company is feeling the pain of a shrinking pub market. I think a positive view is that it reflects the proactive management of the company in keeping its estate competitive.

The company says supply and delivery issues have passed and it has a full complement of staff. It says inflationary pressures have been “ferocious” but describes itself as cautiously optimistic about prospects for the remainder of this year and the longer term.

That may explain why Wetherspoon shares have improved 52% so far this year. Despite that, I see substantially more room for growth.

The Investment Case

Wetherspoons has large format pubs in central areas and follows a pile em high, sell em cheap formula. It eschews background music, although the throng of punters can mean that Wetherspoons’ pubs are busy. Each pub has its own identity but is identifiably a Wetherspoons, which are known for cheap drinks and fairly downmarket though not necessarily rowdy atmospheres.

That may not sound like a winning formula, but it is and has been proven over three decades (the company was consistently profitably until the pandemic). Walk into any Wetherspoons at almost any time of day (most open at eight in the morning) and immediately the investment case becomes clear. They are routinely busy and often packed to the gunnels.

Looking at the drinks prices explains things. I see Wetherspoons as being like the Walmart ( WMT ) of the U.K. pub trade in this way. Prices are not only cheaper than at competitors, they are dramatically cheaper (airport branches, sadly, being an exception, as seen at Edinburgh airport to my chagrin). At a time when a pint in a central city location can cost five, six, seven or even eight pounds, it is often possible to get a pint (not necessarily one’s pint of choice) in a Wetherspoons for under two pounds.

Take The Moon Under Water as an example. Situated in the heart of London’s West End, this is in some of the priciest pub territory in the land. But a bottomless coffee can be had for £1.45. A small fish and chips including a pint can be had for less than a tenner. And so on. For price, Wetherspoons is simply in a different league to the competition. That has helped it build a massive, loyal customer base.

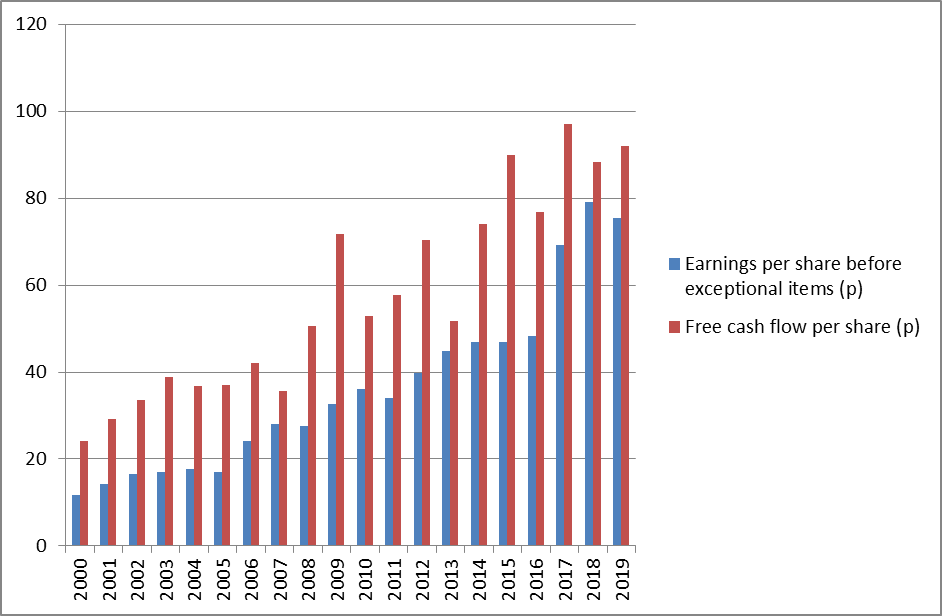

Wetherspoons has now surpassed pre-pandemic revenue levels, albeit inflation has helped on that front. It has also returned to profit, albeit narrowly. But I think the key point here is that the company has now put the pandemic firmly behind it. Looking at its historic performance, the firm had a long, somewhat uneven but steady history of growing earnings and cash flow.

{kind=link}

For 2020 and 2021, the company fell sharply into the red on both metrics for the first time in its history as a listed business. Last year, free cash flow was positive again and this year I expect both metrics to be positive for the full year, as they were in the first half.

With its proven strong and unique business model, I think the company is set to come roaring back in the next several years.

Valuing Wetherspoon's shares

Even after rising by more than half this year, however, I do not think the share price fully reflects that optimistic viewpoint of mine. The founder and chief executive spent £12m in February adding (at £4.57 per share) to his holding, which now totals around 24% of the company. That level of alignment between management and shareholder interests is unusual.

Based on 2019 earnings, Wetherspoon trades on a P/E ratio of less than 10.

Can it get back to 2019 earnings, making that price the bargain it seems? There are risks, including inflationary pressure on profit margins and a lacklustre U.K. economy leading people to drink at home more rather than at the pub (a risk about which the company has consistently been highly vocal). But the company’s formula has been proven over decades and I think it is as strong as ever. It has moved beyond the pandemic and is rebuilding profitability, having already regained revenues. I expect it not only to match but to surpass 2019 profit levels in the coming few years.

The balance sheet is now back to roughly where it was before the pandemic, too. The company ended its 2019 financial year with net debt of £737m. In its interim results last month, net debt was more or less the same, at £744m. Meanwhile, its estate has not been revalued since before the millennium, so I think the carrying value of property on the balance sheet may actually be understated in real terms.

Accordingly, I consider the shares to be a “buy”.

For further details see:

Wetherspoon: World-Class Operator