WEX - WEX Inc.: Normalization Of Fuel Prices Might Be A Headwind

2023-05-08 12:52:03 ET

Summary

- WEX's 1Q23 revenue increased by 18% to $612 million, beating consensus expectations, due to increased travel activity.

- WEX's mid-term outlook is challenging due to weak Fleet gallon volumes and the expected normalization of fuel prices.

- I recommend to hold until fuel prices have normalized, at which point it may be a better time to buy, as expectations will have been lowered.

Investment thesis

WEX Inc. ( WEX ) provides payment processing (fleet cards) and information management services to vehicle fleets. I think there are a lot of advantages to using fleet cards, including cost savings, reduced fraud, and improved visibility into fleet operations. As more people become aware of fleet cards, either through organic funnels or through distribution by major oil companies, I anticipate that penetration will rise over time. While the results for the 1Q23 were better than expected, more focus needs to be placed on the mid-term outlook, where I anticipate weak Fleet gallon being processed, which will act as a drag on growth. This is just WEX business, frankly, which is highly cyclical due to its dependence on the fuel and travel. My recommendation is to hold until fuel prices have normalized, at which point I believe it will be a better time to buy. Expectations will have been lowered by then, and WEX would be facing an easier y/y growth comps.

1Q23 results

WEX's revenue increased by an impressive 18% (19% excluding fuel and foreign exchange effects) to $612 million, which I believe a key driver was the increased travel activity and new Benefits SaaS accounts. EPS of $3.31 surpassed market expectations on the back of interest income from custodial assets and a sizable increase in margins brought about by the sustained uptick in volume.

FY23 outlook

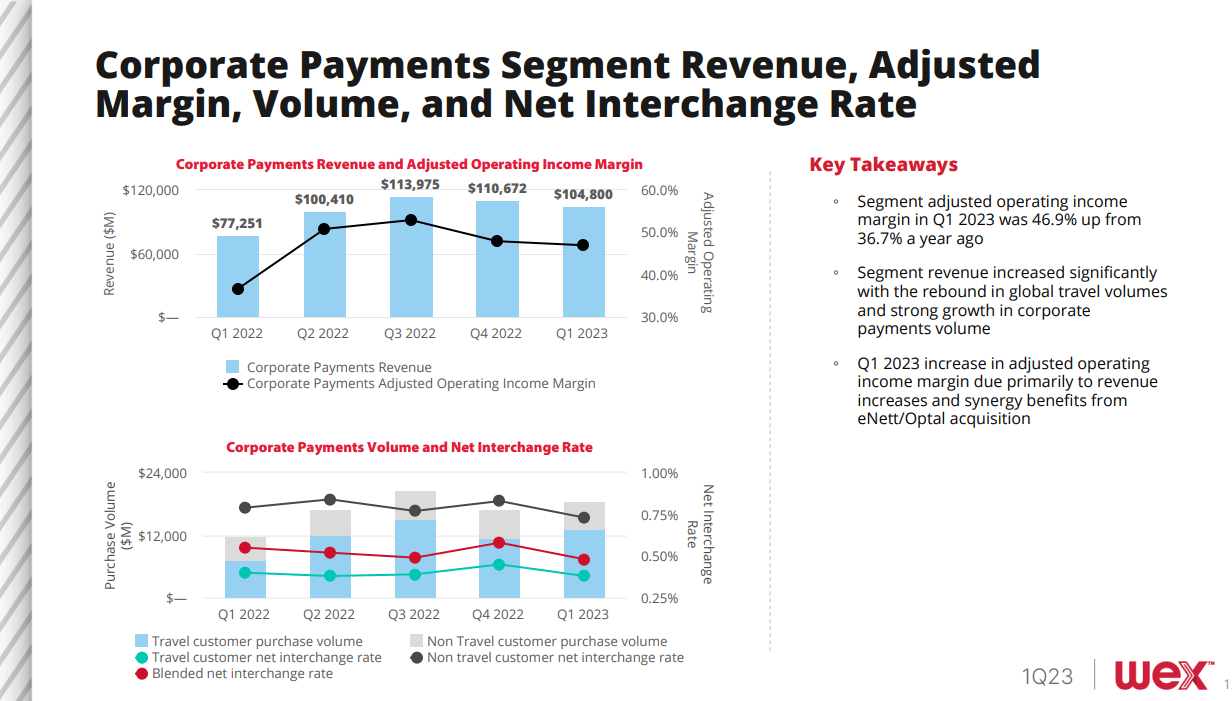

A revised FY23 outlook of 4–6% top-line growth and 2–5% Adj. EPS growth was released after the solid 1Q23 results. I believe the fundamental drivers were the higher-than-anticipated travel volume and the expansion of Benefits SaaS accounts. This guidance also considered the challenging comparison to last year's performance and assumed an incremental slowdown in the economy in 2H23. My take is that the short-term positive to note is volume should continue to grow strongly in 2/3Q23 as it follows historical seasonality, but the mid-term negative to note is that fuel prices are expected to normalize (based on US Energy Information Administration) which will hurt WEX – it will have a direct hit on the dollar amount of fuel purchased being processed by WEX (amount of fuel * fuel price = payment processed). Clearly, things are back on track as 1Q23 travel volumes increased by 84% to around $13 billion, or 1.3x 2019 levels.

{kind=link}

{kind=link}

Importantly, all regions, but especially Europe saw the largest gain. Consequently, these volumes should carry high incremental margin as the cost base is largely fixed, as such we should see healthy profit growth and margin expansion from these. In addition, partner channel was a major contributor to the revival of corporate payment volumes, which increased by 17% to $5.4 billion. While the uptick in volume is encouraging, I'm worried that normalizing fuel prices, which are expected to surpass their FY22 highs. In the 1Q23, Mobility revenue growth slowed to 7.3% from 19.7% in the previous quarter, indicating that the segment was beginning to show signs of cracks. For the rest of FY23, I expect WEX to continue to slow down or even experience negative growth (normalization in fuel prices has a direct impact on the revenue algorithm of the company = fuel prices X volume of fuel). If fuel prices spike, however, WEX will be fine for another year, but that will only push the bad news into FY24. Additionally, I expect that the recent banking turmoil will result in further credit restrictions and shortened payment terms, which will create challenges for growth, but improve credit status. This is in line with management expectations as well. Management has adjusted their guidance due to the anticipation of a significant decrease in credit losses. Fleet loss rates have shown improvement in a sequential manner, thanks to reduced fraud losses. This reduction in both fraud and credit losses has led to a 2bps sequential improvement in fleet loss rates, bringing it to 32bps of volume.

M&A

What could drive a positive momentum on growth and allow WEX to continue beating/surprising consensus is by conducting M&A. WEX has been pretty active in the market over the past few years with 7 acquisitions done since 2019, and the latest pending deal is to acquire Exxon commercial card portfolio. I would not be surprised if management continues this streak of M&A to improve the business portfolio and also drive growth. Importantly, if done right, M&A could be a way for WEX to expand its TAM and growth, and also reduce its exposure to fuel. WEX can explore the EV market, where management has already made some headway , by signing acceptance agreements with large public charging networks and planning to launch a home reimbursement pilot program in 2H23 (1Q23 earnings call). This strategy is in line with WEX's strategy of ensuring all EVs can be charged conveniently while simplifying payments and reimbursements.

Risks

As mentioned throughout the entire post, the key risk is a decline in fuel price, especially a significant decline (which has happened before back in 2020, which caused WEX stock to fall from $236 to $71 within a few weeks). This, if coupled with an extended decline in travel volumes due to a prolonged recession (could be companies going under and the overall pool of drivers decrease), would be a disaster for the business performance.

Conclusion

WEX has shown impressive revenue growth in 1Q23. However, the mid-term outlook remains challenging due to weak Fleet gallon payment processed. While WEX travel volume is strong, the normalization of fuel prices is a key concern. My recommendation is to hold until fuel prices have normalized, at which point it may be a better time to buy.

For further details see:

WEX Inc.: Normalization Of Fuel Prices Might Be A Headwind