WEX - WEX Inc.: Potential Is There But Tread Carefully For Now

2023-04-20 04:33:40 ET

Summary

- With very solid FY22 results and good guidance for the long term, I decided to look into the company further.

- A decent balance sheet and free cash flow generation show potential.

- In this article, I will focus on testing the company's long-term goals for revenue and EPS growth to see what it would be worth.

- A 10-year DCF model suggests the company is fairly valued with a slight upside.

- However, I would hold off for now because of the pessimism in the economy, which may present an even better entry point.

Investment Thesis

With the latest annual report beating estimates by decent numbers and what I believe to be a good guidance for 2023 and beyond, I wanted to see what the WEX Inc.'s ( WEX ) financials look like and check what would be a decent valuation for the company that will see high EPS growth over the next years and the company's desire to achieve 10%-15% CAGR revenue growth in the long run.

With a decent balance sheet and UFCF growth over the next decade, the company seems to be fairly valued right now and may reward shareholders in the long run if the company manages to achieve such results going forward. I would suggest holding off for now because of economic headwinds and volatility that we will see creeping up in the next 6 or so months.

Guidance and an Anchor for Valuation

The company saw record revenues in all their segments, some saw over 50% increases in revenue (Travel and Corporate Solutions). Total revenues were up 27% y-o-y, however, the guidance suggested only around a 3% increase in revenues in '23, which suggests that the economic headwinds are starting to take hold. The management is still confident that they will see a 10%-15% CAGR in revenue growth in the long run and low double-digit EPS growth also.

The company is focusing on a non-GAAP EPS outlook, so I will do the same when I am going to attempt to value the company later in the article. Right now, I will look at the company's financials to see how healthy the company is and how well it will weather a short-term downturn in the economy.

Financials

The company has $922m in cash and $1.4B in short-term investments as of FY22 while the debt figure has slightly decreased to $2.5B. It doesn't seem to be in a bad position in terms of leverage because the company's interest coverage ratio is 4.63, which is a very healthy ratio. 2 is acceptable and 3 is great, so the company has no issues covering its annual interest expenses on debt.

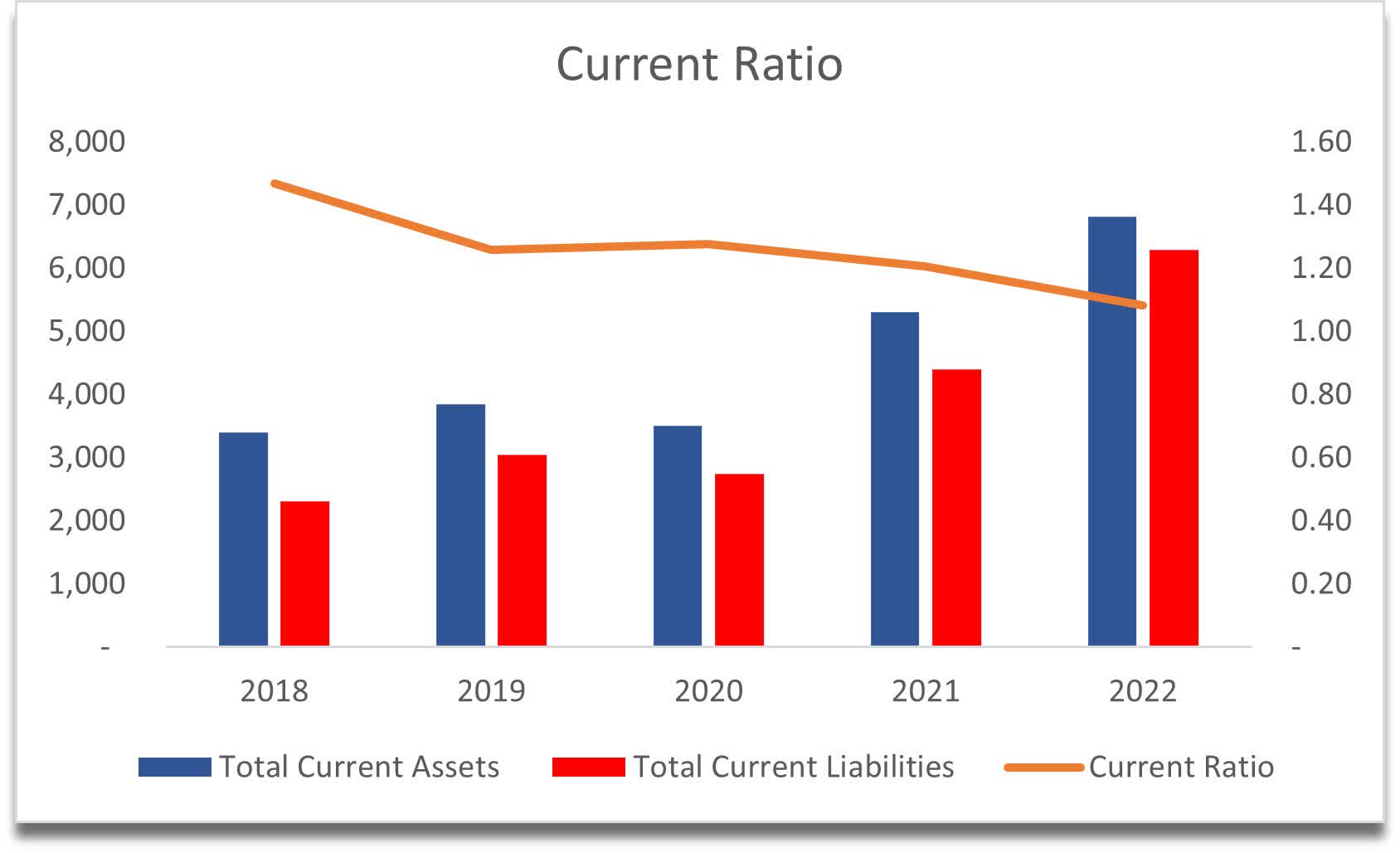

Furthermore, the company's current ratio also suggests it does not have any liquidity problems, although it was a little better in the past, it is still over 1.0, meaning the company can cover its short-term obligations.

{kind=link}

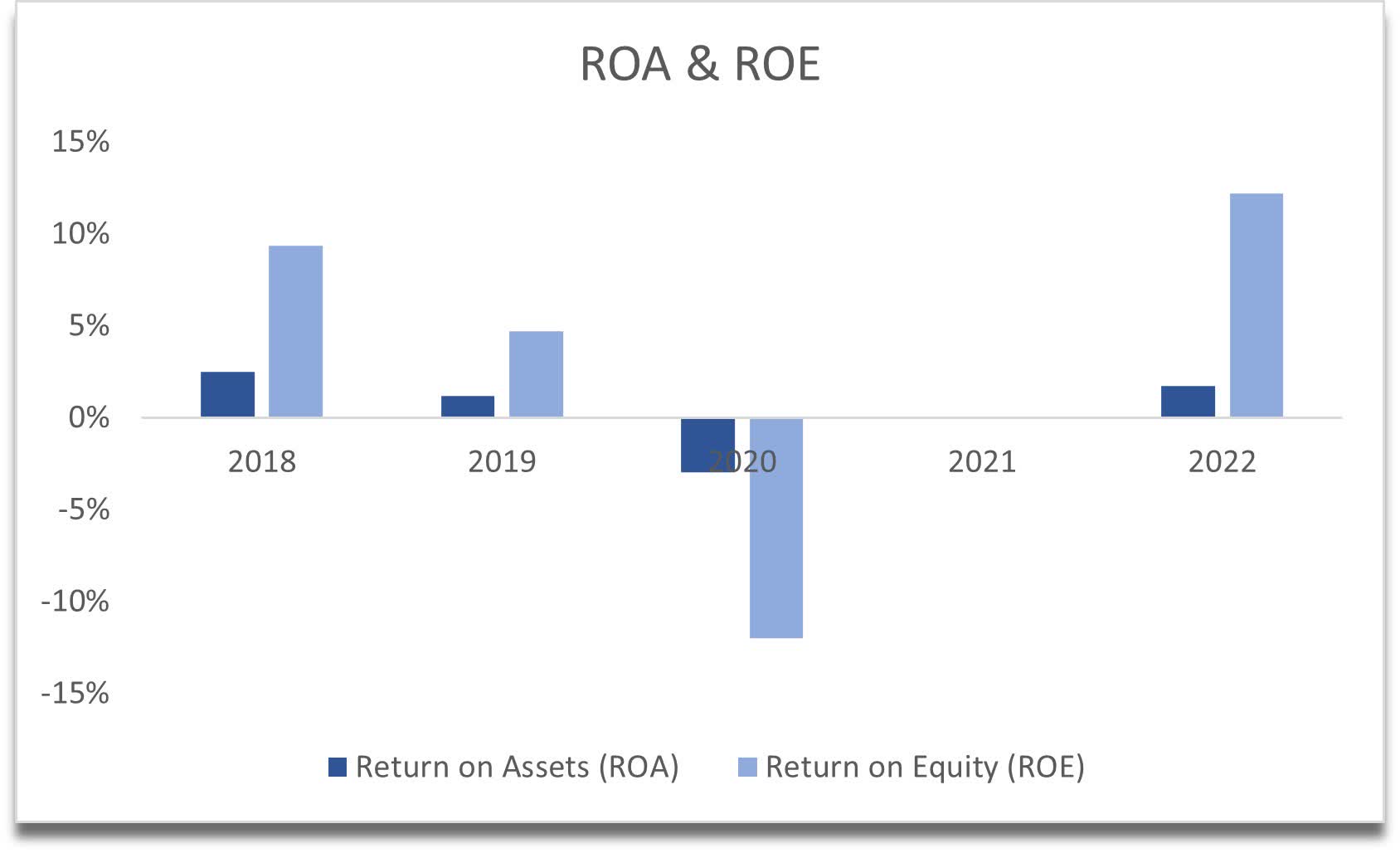

In terms of profitability and efficiency, ROA has been quite disappointing throughout the years, while ROE has been somewhat acceptable. I would like to see these improvements in the future.

{kind=link}

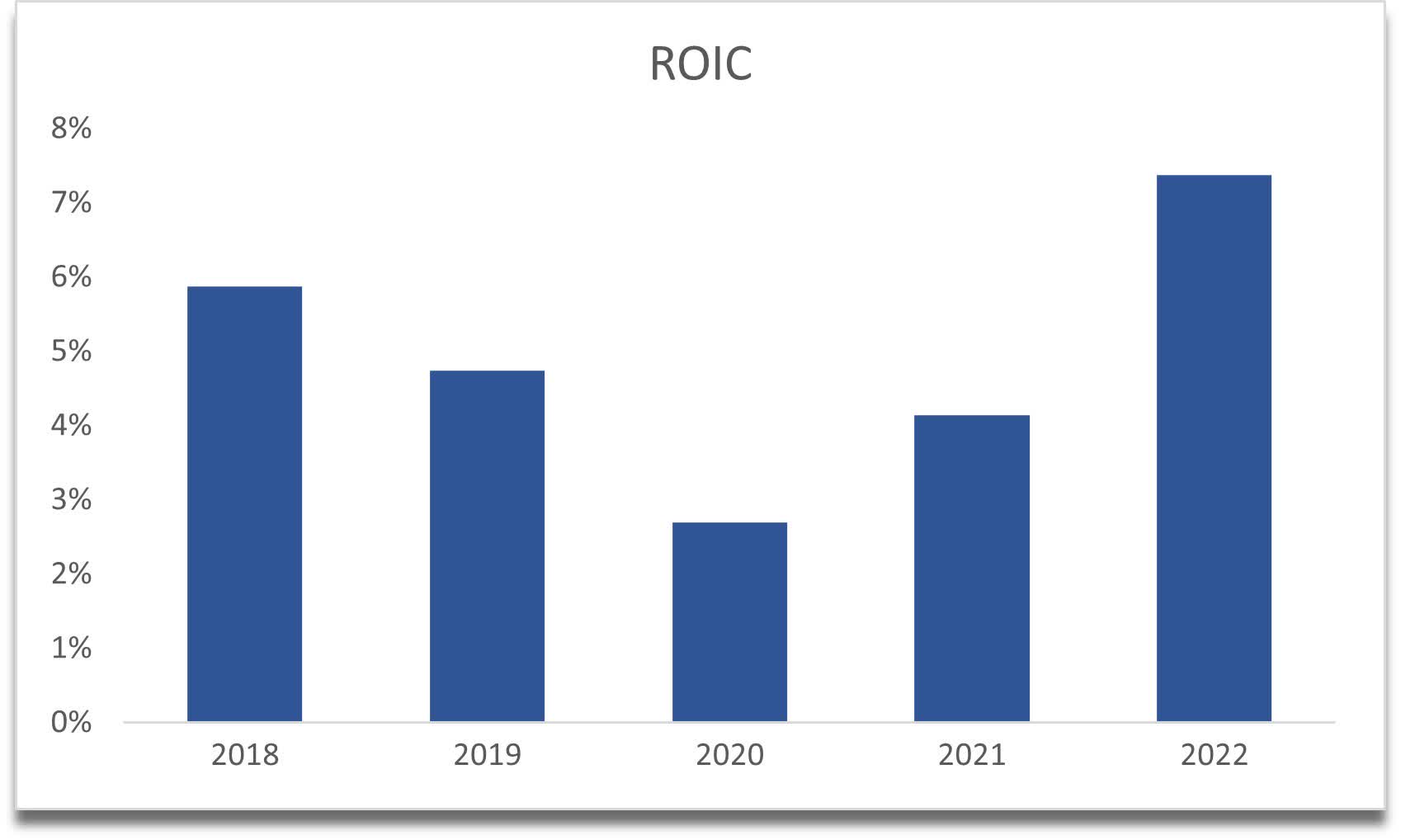

ROIC is also just about acceptable in my opinion. The only positive I can see is that the company's moat and competitive advantage is increasing. The management can deploy capital to fund positive NPV projects, let's hope they can continue this in the future.

{kind=link}

If we compare the same metric to its competitors, it is right up there at the top next to EEFT.

{kind=link}

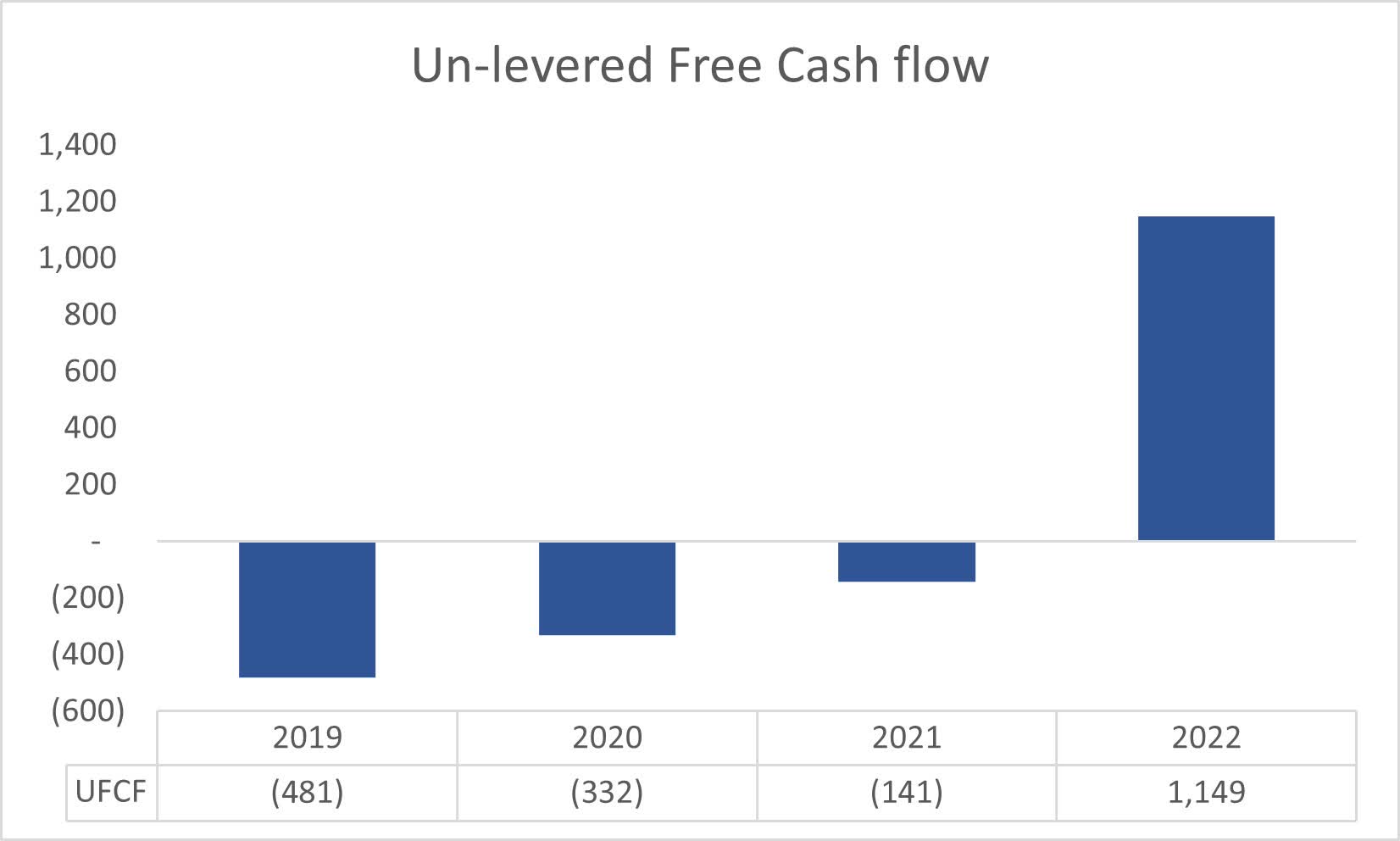

In terms of unlevered free cash flow (UFCF), the company only in the last year managed to achieve positive figures, however, that figure was quite a jump from the previous year. This will help me with the DCF valuation model.

{kind=link}

Overall, the company seems to be financially healthy, with very good free cash flow generation and no liquidity problems.

Valuation

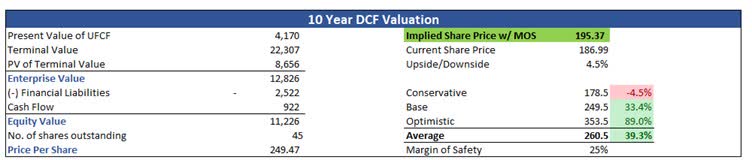

I decided to test the management's long-term revenue growth outlook and the EPS growth. As I mentioned the company is looking to grow revenues at 10%-15% CAGR and 15%-20% EPS growth in the long run. I ran with these numbers as an anchor to my valuation, however, I do like to approach it with a bit more conservatism, so my base case scenario will have revenue growth over the next decade at around 13% while EPS at around 17%. To get a range I also modeled an optimistic case that has revenue grow at 16% while EPS is at 19% and the conservative case revenues grow at around 11% while EPS is at 15%.

For the sake of simplicity, I kept margins the same as the company has reported in the FY22 report. Furthermore, I will add a 25% margin of safety to the intrinsic value calculation because I feel like the balance sheet is strong enough to withstand any upcoming headwinds. I usually don't go lower than 25% MoS as it is better to be conservative.

With that said, the company's intrinsic value right now according to the management's long-term guidance is $195.37, which means it is pretty much fairly valued right now with around 4.5% upside.

{kind=link}

Closing Remarks

The company has a lot of potential in this sector, coupled with more growth opportunities that generate positive free cash flow in the long run, it can reward shareholders handsomely in the future. The growth numbers seem to be very reasonable from what I saw in the last reported quarter, maybe even on the conservative side also. The company can be a buy at these levels, however, I would suggest waiting a little longer because of the economic headwinds that are predicted by so many economists which will bring volatility to the markets and may bring a better entry point for this and many other companies if you are patient enough. I know I am, mainly because I don't have any capital available at the minute for this company as it is already reserved for some other companies that I reported on.

The balance sheet is also strong enough to withstand the volatility of the economies. The recession is predicted to be one of the mildest in recent history, so I don't have any worries there.

I did not go into any detail about potential growth catalysts for the company as I merely wanted to test the management's assumptions for their own company, whilst also being slightly on the conservative side to not get burned by buying at the wrong price, reducing my potential returns dramatically. In the last 6 months, the company is up 38%, which to me signals that a correction is due, especially if we are going to see some hiccups in the economy. Many people will take the hiccup as an excuse to take profits in the short run and that can present a good entry point.

My price alert is at around $175 a share, and if I'll have the capital to play the stock by then, I will consider opening a small position to test the waters.

For further details see:

WEX Inc.: Potential Is There, But Tread Carefully For Now