WEX - WEX Inc: Q2 2023 Earnings Was Good But More Is Needed

2023-08-04 02:50:18 ET

Summary

- I recommend a hold in the near term until it can further prove stable growth and margins amid concerns over fuel price normalization.

- Despite higher fuel prices, WEX reported 2Q23 revenue growth of 4% and exceeded expectations, showing promise for future progress and potential for growth through diversification efforts.

- If WEX can continue growing as guided, I think the market will start to revalue the multiple upwards back to its historical average.

Overview

My recommendation for WEX Inc ( WEX ) is still a hold in the near term, as I don't see any reasons for the market to revalue the stock upwards. WEX would need to show that growth and margins have stabilized and will grow from here, thereby removing the concern that fuel price normalization will hurt the business earnings outlook. Once that is proven, I could envision a path for further upside. Note that I previously gave a hold rating for WEX until fuel prices normalized.

Business

WEX provides payment processing (fleet cards) and information management services to vehicle fleets. I think there are a lot of advantages to using fleet cards, including cost savings, reduced fraud, and improved visibility into fleet operations.

Recent results & updates

In spite of higher fuel prices and slower mobility transaction growth due to attrition from credit tightening, 2Q23 revenue grew by 4% to $621 million on stronger-than-expected travel volume. As a result of higher incremental margin brought on by revenue growth, WEX reported adjusted EPS of $3.63, which was higher than the consensus estimate of $3.52.

The quarter's high point was a better-than-anticipated travel recovery, which more than made up for a sharp drop in fuel prices (a key concern of mine, and I believe the market's). Notably, management increased the midpoint of its FY23 revenue and adj EPS outlook, despite a 26% y/y drop in fuel prices and the resulting drop in Mobility revenue. The increase may have been small, but I see it as a sign of stability and hope for the next quarter. In addition to the travel industry's recovery, WEX's Corporate Payments division saw strong results, with travel purchase volume increasing 44% to $22.9 billion. To put this in perspective, the segment's growth from 1.3x FY19 purchase volume in 1Q23 to 1.49x in 1Q23 demonstrates clear demand momentum.

I think WEX 2Q23 results clearly did better than I expected, while not enough, it was a good start. On another note, this quarter was a great example of how WEX's ongoing efforts to diversify its business model could help the company become less vulnerable to fluctuations in fuel prices. For instance, I'm heartened by WEX's new $100 million investment mandate for early-stage mobility companies specializing in fleet electrification, electric vehicle charging, and energy management. In my opinion, this is a strategic film that will pay off in the long run. By doing so, WEX can raise its profile in the booming EV industry and potentially identify promising targets for future acquisitions.

The company's strategy for diversification is not limited to the EV market. They recently announced their agreement to purchase Ascensus Health and Benefit . The deal is expected to close before the end of 2023. As a result of this purchase, I have higher hopes for WEX's existing Benefits offerings. Ascensus's Affordable Care Act compliance and verification capabilities provide a natural avenue for expanding the company's customer base through upselling. Ascensus has demonstrated a growth profile of 15-20%, so there are financial upsides to the deal as well.

Valuation

Author's valuation model

According to my model, WEX is valued at $198 by the end of FY23, representing a 54% increase. This target price is based on management's FY23 guidance and a similar growth for FY24 as travel volume gradually recovers. I expect margins to follow guidance in FY23 for FY24 and FY25 as the normalization in fuel prices (high decremental margins) will net off the increase in volume.

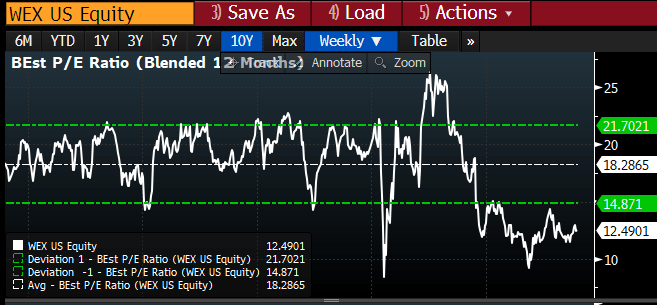

My model showed 2 scenarios, the near-term price target (end of FY23), where I expect multiple to stay at the current level due to the lack of positive catalysts. WEX needs to convince the market that it can continue to grow as guided in the face of fuel price normalization (refer to my previous write-up for more on fuel price normalization's impact). Suppose WEX grows as guided, I think investors will be more confident in the earnings outlook, hence crediting the company by revaluing the business at a high multiple, a step closer to its historical average. WEX used to trade at an average of 18x but is only trading at 12.5x today.

{kind=link}

Summary

In conclusion, my recommendation for WEX remains a hold in the near term, as the company still needs to demonstrate stable growth and margins amid concerns over fuel price normalization. Although 2Q23 results exceeded expectations and showed promise, further progress is required to justify a higher stock valuation. WEX's diversification efforts, such as the investment in early-stage mobility companies and the pending acquisition of Ascensus Health and Benefit, hold potential for future growth and customer expansion.

For further details see:

WEX Inc: Q2 2023 Earnings Was Good, But More Is Needed