IAUM - What Affects The Price Of Gold: Conventional Wisdom Vs. History

2023-10-26 10:38:08 ET

Summary

- Gold and silver are purchased for various reasons, including as a hedge against inflation and to protect against geopolitical turmoil.

- The correlation between gold and inflation is not always consistent, with gold sometimes going down despite high inflation.

- Precious metals can potentially protect wealth in the long term, but other assets like stocks and real estate may provide better returns.

- Geopolitical events have not historically moved gold in a particular direction, and fearmongering should not be fronted as a buy thesis.

People buy gold and silver for a lot of reasons. For jewelry and adornment, for numismatic (coin collecting) purposes, to store wealth, limited industrial applications, to protect against inflation, and to guard against geopolitical turmoil and related threats to fiat (government-issued) currency. As it relates to investing, the list is narrowed: the purchase of precious metals serves as a hedge against inflation and to serve as a store of wealth to be used as a medium of exchange in instances where fiat currency can no longer be relied upon as a result of changing world orders and the rise and fall in prominence of governments. Current conditions in the United States and the world would suggest that, according to conventional wisdom, gold should be appreciating in value, what with multi-decade highs in inflation and unrest throughout the world, chiefly in Ukraine and Israel, and the threat of what China might do as it relates to Taiwan. Is there a historical precedent for this conventional wisdom? The purpose of this article is to look at what the price of precious metals has been in other periods of inflation and/or world turmoil and see if the conventional wisdom holds up under historic scrutiny. Bottom line up front: the inflation theory holds up but only under very long time periods, with interim divergence that can be costly if ill-timed. The world turmoil theory does not have a strict historical precedent, with precious metals sometimes going up and sometimes going down in the aftermath of considerable global events. For these reasons, do not count on gold to be the safe haven it is oft touted as, and don't sell all your other assets for precious metals due to the intense conditions we find ourselves in. However, it can potentially insulate a portfolio when used judiciously as part of a larger portfolio.

Gold vs. Inflation

First, it must be stated and underscored that there is nothing special about gold that makes it magically go up in value in response to inflation. Gold is a commodity, and like any other commodity, its price rises and falls according to supply and demand dynamics (with plenty of interference from gold futures speculation). In other words, the price of gold only goes up if people are willing to pay more for it. And, as inputs, commodities tend to be the first to feel inflation's power.

Because it has been repeated so often that gold protects purchasing power from the ravages of inflation, it could be a classic instance of the tail wagging the dog. When people hear that inflation is high or going to be high, they flock to gold to protect their purchasing power thus driving the price of gold up. That increase in price then makes it look like gold did indeed track with inflation, but it wasn't the inflation that caused it. It was people buying gold due to inflationary fears. It's correlation but not causation. There have been tons of instances where gold went down in spite of inflation:

.... the trading patterns of gold relative to the consumer price index have been volatile. According to Forbes Advisor, the ratio of the price of gold to the consumer price index has averaged 3.6 since 1972. But as of May 2023, that ratio was closer to 6.4. If there was a direct correlation between inflation and the price of gold, that ratio would be more stable.

Similarly, from 1980 to 1984, as noted by Forbes Advisor, inflation averaged 6.5% annually, but gold fell an average of 10% per year. A similar negative correlation occurred from 1988 to 1991.

However, for the years between 1974 and 2008 when inflation ran over 5% annually, gold rallied as well, averaging 14.9% on a year-over-year basis, according to an article in The Journal of Wealth Management.

In other words, trying to time the market and get in and get out of gold according to inflation reads and inflation expectations could result in considerable money loss.

However, using gold as a store of value over extremely long periods of time could indeed achieve the desired result. This chart explains it all:

chart of gold and inflation (kinesis.money)

With notable periods of divergence, gold and to a lesser extent silver have both kept pace with inflation. But the problem with this is that we have instruments that allow us to exactly pace inflation with zero periods of divergence, TIPS and I-bonds. So gold and silver become lesser vehicles if matching inflation is the stated goal. Another issue is that tracking with inflation via gold, silver, TIPS, or I-bonds means that the real return is still 0%. Purchasing power was maintained but wealth did not increase. If you can use an asset that BEATS inflation, why not use it?

Gold and silver are non-productive assets. More than perhaps any other asset class, the value of these is inherently tied to how much someone else is willing to pay for it. Beyond limited use in industry and electronics, gold is just a mineral. Unlike stocks which represent proportional ownership of an entity that produces (and can produce more of) things that humans use, need, want, and demand, or real estate that serves a critical function to giving people a place to live, work, eat, etc., gold just sits there. As Warren Buffett said, sure you can fondle gold, but don't expect it to respond.

In summation for this portion, yes precious metals can protect against inflation but only if they are held for the long term. But maintaining purchasing power is a far lesser goal than actually building wealth, so if you have to hold something for the long term anyway you might as well buy stocks or real estate, whose returns smash gold and silver.

Medium of Exchange vis-a-vis Global Unrest

I am of the opinion that investing in precious metals for the inflation aspect alone simply isn't worth it. If you want to match inflation, buy TIPS or I-bonds. Better yet, beat inflation by investing in stocks and real estate for the long term. However, when coupled with a second factor, allocating a modest portion of one's overall portfolio to precious metals makes sense.

Let me put it bluntly: if something like World War III starts up and the United States loses, our currency will almost certainly collapse. With the Russian invasion of Ukraine, the hot situation in Israel, and China's objective of someday re-taking Taiwan, plenty of folks are prognosticating about an outbreak of widespread war involving major powers. If the U.S. does not win that conflict alongside allies, don't count on being able to buy TIPS or I-bonds. If things get especially bad, don't count on your dollar bills being worth much more than the paper they are printed on. That is the doomsday scenario, a picture often painted by the "gold bugs".

In that scenario where a strong government doesn't exist to issue and back up a fiat currency, silver and gold will be the likely fallback for a medium of exchange.

An article from Forbes describes it well. The U.S. dollar is....

".... backed by the weight of the United States, reflecting everything within the economy.

So in order for a dollar to have value, society needs to believe that the United States has value. Given how many taxpayers, businesses and valuable assets are in the US, it's hard to argue that it doesn't have value. In fact, the reason why the U.S. was able to move off the gold standard was because it had so much economic value.

So, a currency collapse is when there is no longer any trust that the asset, country or organization has sufficient value to reflect the currency.

War could easily upset the value proposition of the United States.

Even without a war or any doomsday scenario, the U.S. dollar is facing unprecedented challenges to its status as the world's reserve currency. This is due to the world becoming increasingly concerned about the U.S. capacity to meet debt obligations, alongside a rising China and other nations that would rather not bow to the dollar for settling global trades.

At a BRICS summit earlier this year (BRICS = Brazil, Russia, India, China, South Africa), this theme was touched on by several world leaders. Russian President Vladimir Putin said, "The objective, irreversible process of de-dollarization of our economic ties is gaining momentum." President Xi Jinping of China was recorded as promoting "the reform of the international financial and monetary system". If any such "BRICS currency" comes into being even a decade from now, having gold and silver could very well act as a store of wealth insulated from any impact on the U.S. dollar. This is especially so if the rumors are true that any such BRICS currency would be backed by gold. It's worth noting that the past two years have seen unprecedented levels of gold hoarding by central banks of various nations the world over.

What happens to the price of silver and gold during periods of major conflict, threats, and social/economic unrest? A few examples.

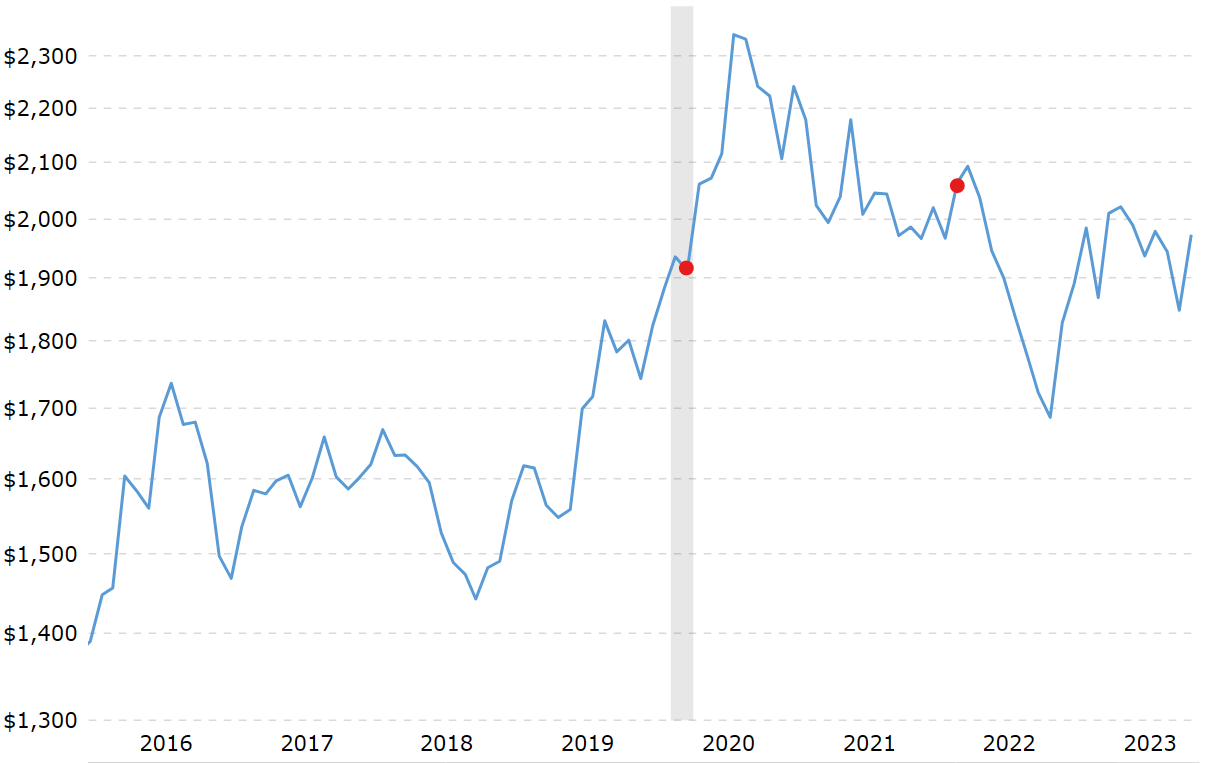

Let's start with the most recent first, looking at a period that encompasses the COVID-19 pandemic in 2020 and the Russian invasion of Ukraine in 2022, indicated by the first and second red dots, respectively:

{kind=link}

You could make the case that gold shot up in response to COVID commotion, but you could also argue that the surge was simply a continuation of a previous bull trend that started two years earlier. The Ukraine situation saw gold soon then-after plummet by 19%.

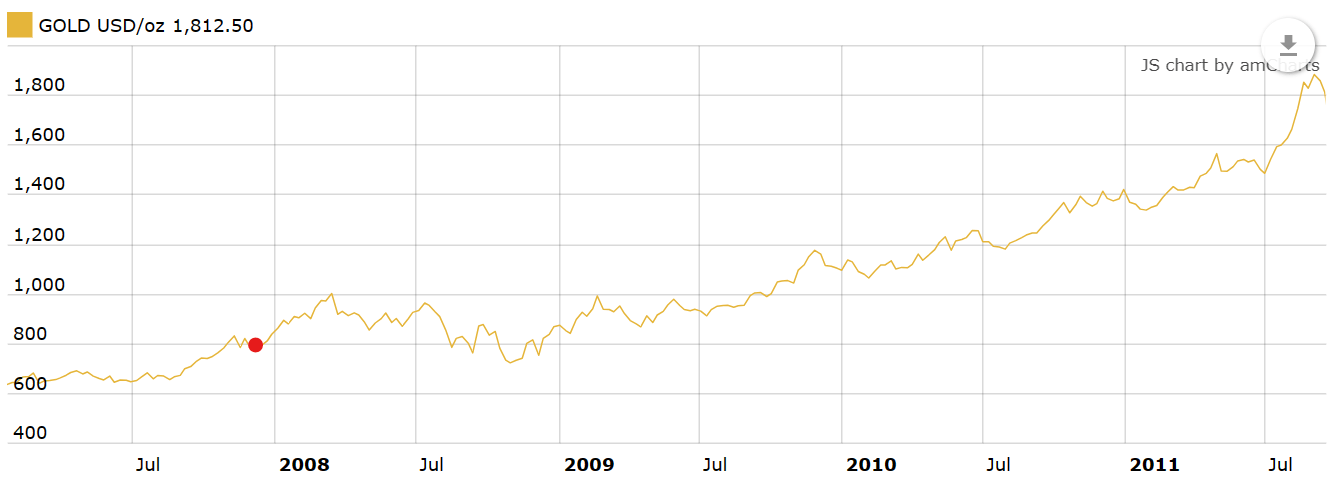

Next is The Great Recession which started in December of 2007, indicated by the red dot:

{kind=link}

Here too the case could be made that the global shock resulted in a flight to the safety of gold, where prices pushed up by $200 in a few short months. However, the surge was short-lived. Before year end the price of gold had dipped below the recession start price, then starting a slow march upward that matched the global economic recovery.

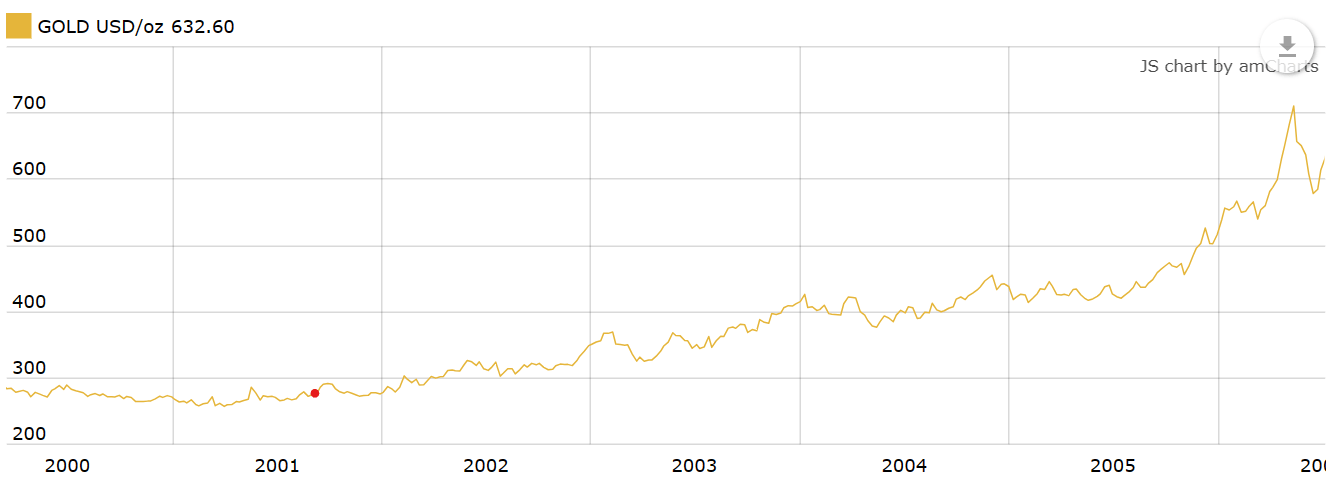

Now we look at September 11th, a day that changed the world. The price of gold went up by $20 in the immediate aftermath, but the settled back down quickly, flattening for a few months, and then slowly climbed through subsequent years. If this amounts to a flight to safety, it was cool and calculated. More of a meander to safety.

{kind=link}

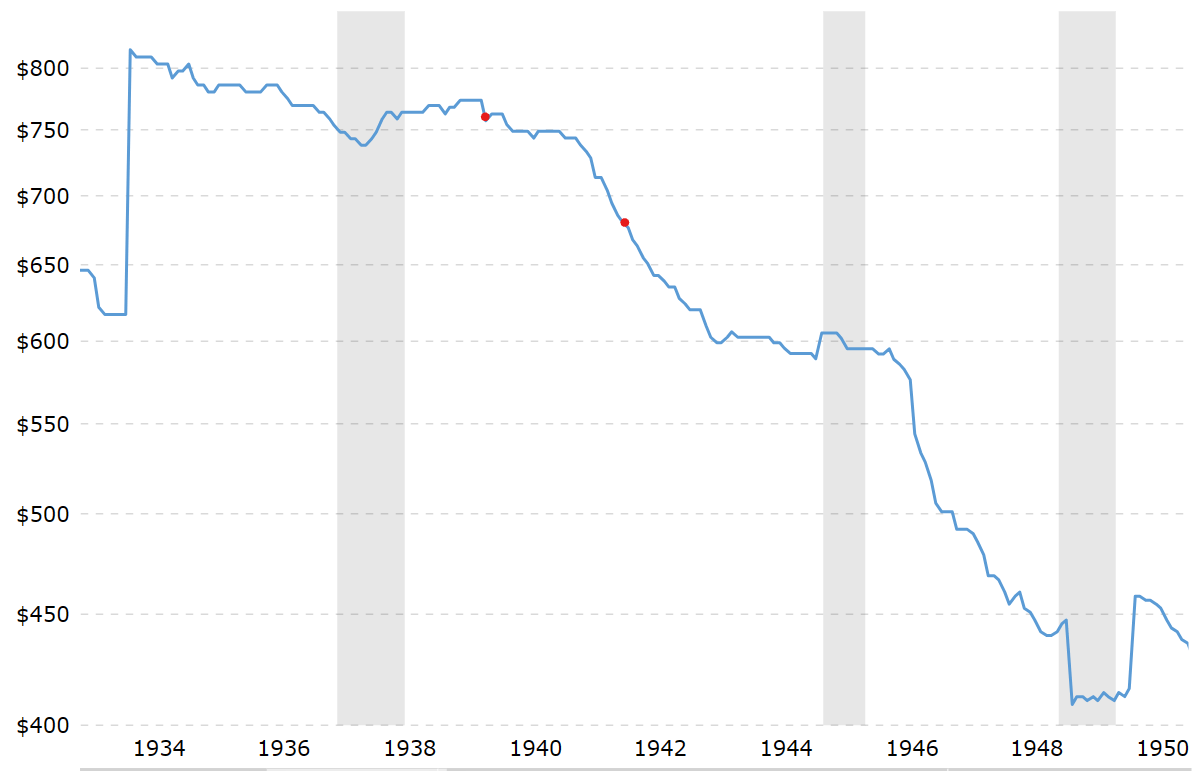

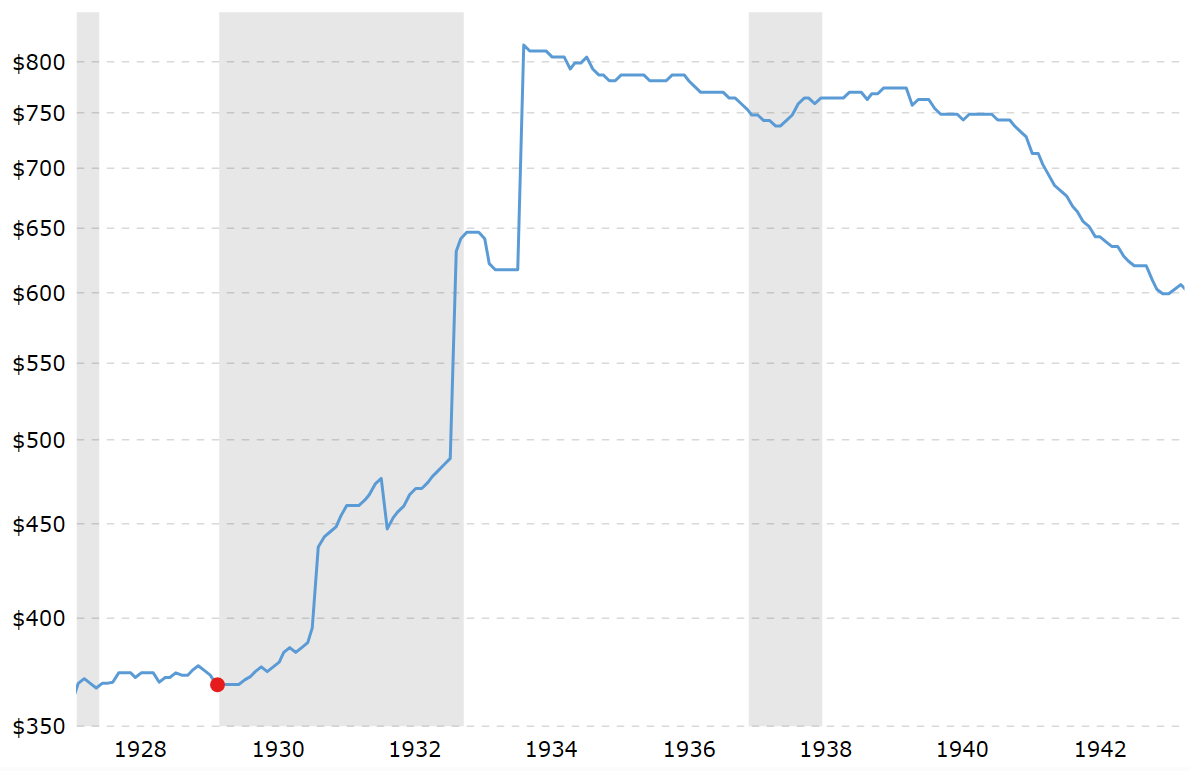

Looking at WWII, where Germany invaded Poland in 1939 (first red dot) and then when Japan brought the United States into the conflict in 1941 (second red dot), both were in the midst of a significant fall in the price of gold. Global unrest indeed, but no surge in gold.

{kind=link}

The final example from the Great Depression certainly makes the strongest case for gold being a wise investment in instances of economic shock. From $360 to $800 in just a couple years:

{kind=link}

This list was not intended to be exhaustive. And it is certainly beyond the scope of this article to try and surmise fully why the price of gold behaved as it did in each given instance. The point is that significant events by themselves don't seem to send gold in a particular direction. Trying therefore to invest according to some potential doomsday event is an error, if history is any indicator. It's a mixed bag.

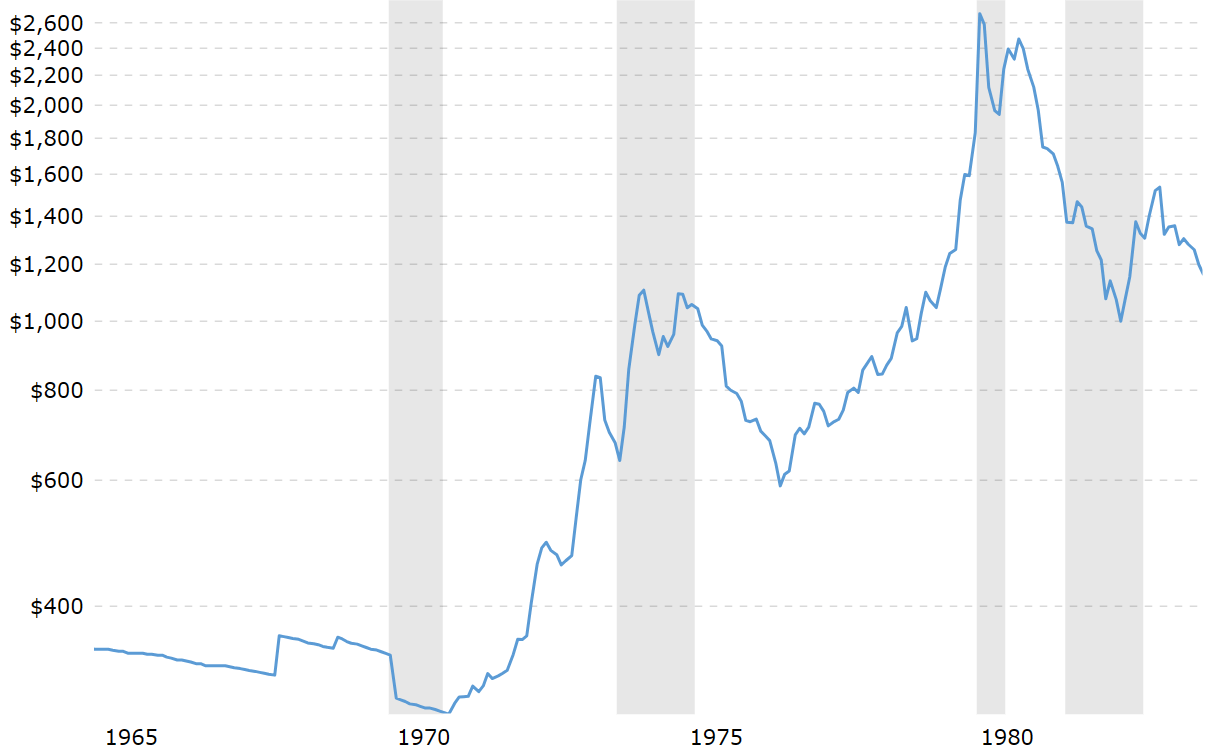

But let's talk about an instance where there was no single shock to set things off, but rather a series of smaller events and conditions combined to create a climate that may have contributed to the meteoric rise in the value of gold that happened in the 1970s:

{kind=link}

From ~$280 to $2,600 over ten years is a 25% annual growth rate. What a decade. What was going on that might explain some of the rise? Some things that have plenty of resemblance to today:

- Cold War with Russia

- Stagflation

- Oil embargo and subsequent energy crisis

- Iranian hostage situation, with 60 US citizens taken

- Russia's military posturing and invasion of Afghanistan

- Yom Kippur or 4th Arab-Israeli war

Eerie, is it not? Replace a few words or names and those bullets basically describe today. None of those things individually had the same scope as WWII or the same shock as 9/11, but taken together they clearly pushed people's investing dollars into a perceived safe haven, gold of course.

Now, to be perfectly clear, I am not predicting some meteoric rise in gold. Far from. Who knows what will or will not happen? However, it does underscore the importance of diversification among asset classes with an informed proportion of the portfolio sitting in precious metals, more so perhaps in instances where many monetary and socio-geo-political elements are in play.

Conclusion

I am no gold bug. If I wanted to achieve one thing with this article, it was the hope that I could dampen the voices of the firms trying to make a profit by using current circumstances and in my opinion, using scare tactics to get people to buy precious metals. There is simply no proof that gold reliably spikes as a result of inflation and/or big global events. That being said, it is one basket in which folks should have an egg or two as part of a long-term strategy of preserving wealth. Other baskets are real-estate, stocks, bonds, other commodities, and perhaps even a dash of foreign currency. No one knows what the future will bring on the U.S. or global stage. Therefore, touching various asset classes is wise. Limiting overt exposure to any single one is key.

Fear of missing out and fear of loss should not be drivers of investment decisions. Data should drive investment decisions. I hope I provided here data that could round out the picture a bit and prevent folks from doing anything drastic. Buy gold and silver, but do so in a measured way that agrees with your overall life situation and goals.

For further details see:

What Affects The Price Of Gold: Conventional Wisdom Vs. History