BABA - What Awaits The Oil And Gas Industry In 2023

Summary

- Global economic uncertainty continues to be high, and downside risks are rising in most Asian and European countries due to the inability to fight inflation effectively despite ongoing monetary tightening.

- Given the sanctions imposed, Russian oil and gas companies have practically no opportunity to buy equipment to service a hydrocarbon production facility.

- A continuing tense situation in the real estate sector, the impact of restrictive measures, and the increase in the number of COVID-19 cases, led to a slowdown in China's economic growth.

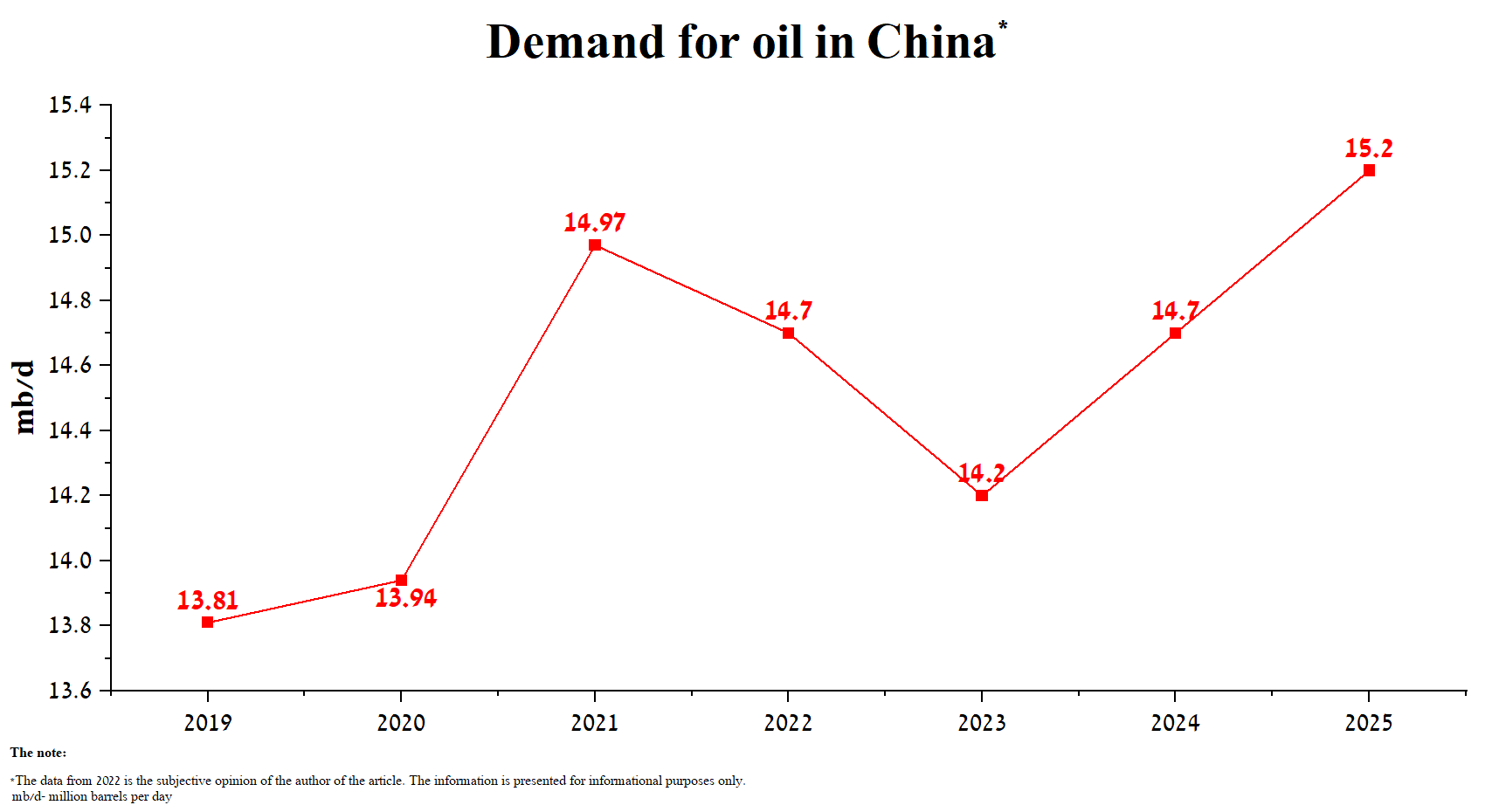

- I estimate total oil demand at 101 million barrels per day in 2023, up slightly from 2022, driven by recovering demand for diesel and jet fuel in North America and India.

- I expect the price of the Energy Select Sector SPDR ETF to rise to $88 in the short term, after which it will drop to $54 in 2023.

Since my article "The Oil And Gas Industry Likely Heading For A Long-Term Downfall", WTI crude ( CL1:COM ) and Brent futures ( CO1:COM ) have fallen more than 10%, as well as the share prices of oil and gas mastodons Exxon Mobil ( XOM ) and Chevron Corporation ( CVX ), whose combined share in the Energy Select Sector SPDR ETF ( XLE ) is around 42.46%. In addition, declining inflation is putting downward pressure on the share prices of BP ( BP ), Petrobras ( PBR ), Shell ( SHEL ), and Occidental Petroleum Corporation ( OXY ), despite massive investor euphoria in the first half of 2022.

Author's elaboration, based on Investing.com

{kind=link}

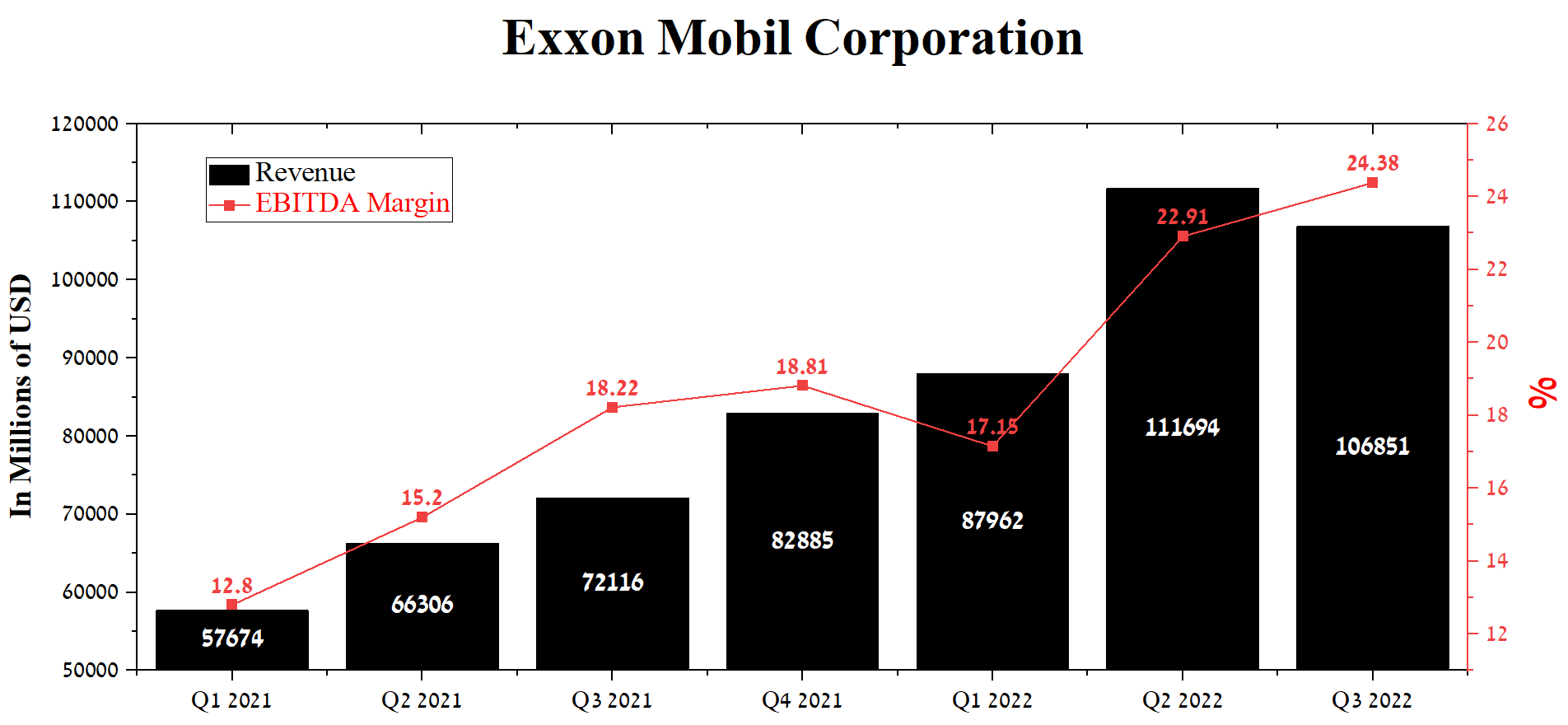

Exxon Mobil's revenue was $106,851 million in Q3 2022, down about $4.75 billion quarter-on-quarter, breaking the upward trend of this financial indicator for the first time since 2020. However, due to high energy prices, EBITDA margins continued to remain at record levels.

Author's elaboration, based on quarterly securities reports

{kind=link}

A similar situation was observed at Chevron Corporation, whose revenue was $63,508 million in Q3 2022, showing a more modest decline relative to Exxon Mobil. But unlike Exxon Mobil, the company's EBITDA showed a decline quarter-on-quarter for several reasons, one of which is a higher volume of repairs to pipelines and units required for oil operations.

Author's elaboration, based on quarterly securities reports

{kind=link}

During the recovery of the US economy, the most advantageous position was occupied by the shares of companies included in the oil and gas industry, which in general is a cyclical industry. However, as the macroeconomic situation in the world improves, investors begin to switch their gaze to more risky assets. This article will present factors that will help stabilize oil and gas prices in the short term but also those that could lead to a significant decline in 2023. These factors are the worsening economic and epidemiological situation in China, the decline in Russian oil prices, and the consequences of steps taken by the governments of European countries, the United States, and Japan to fight inflation. As a result, I expect a significant drop in the prices of many ETFs, including United States Brent Oil Fund ( BNO ), ProShares Ultra Bloomberg Crude Oil ( UCO ), and United States Oil ETF ( USO ).

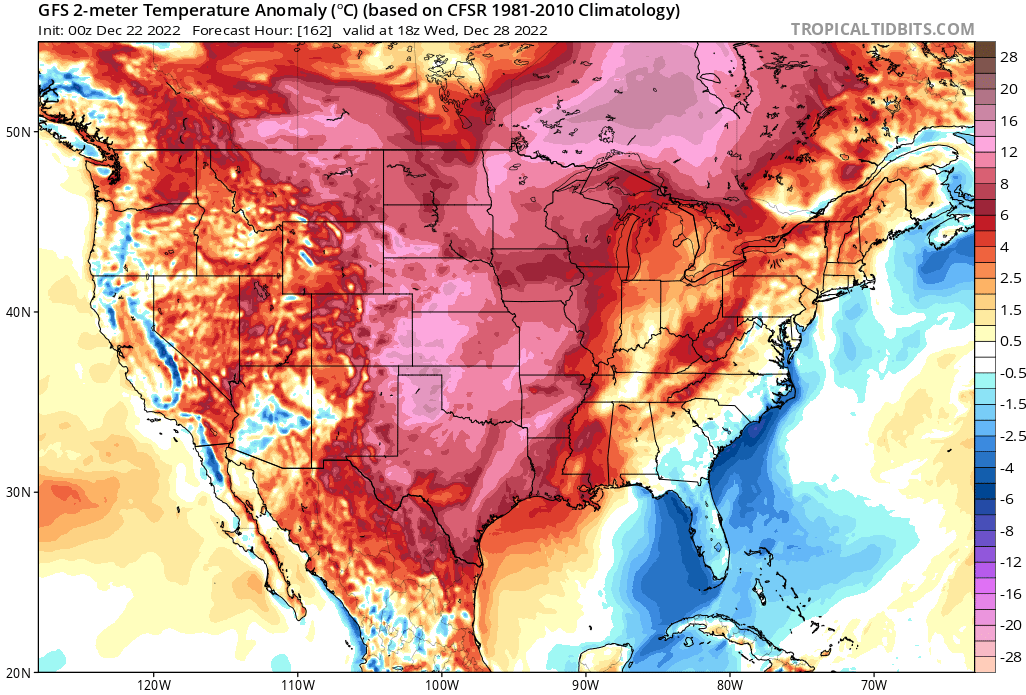

A spreading winter storm in the US

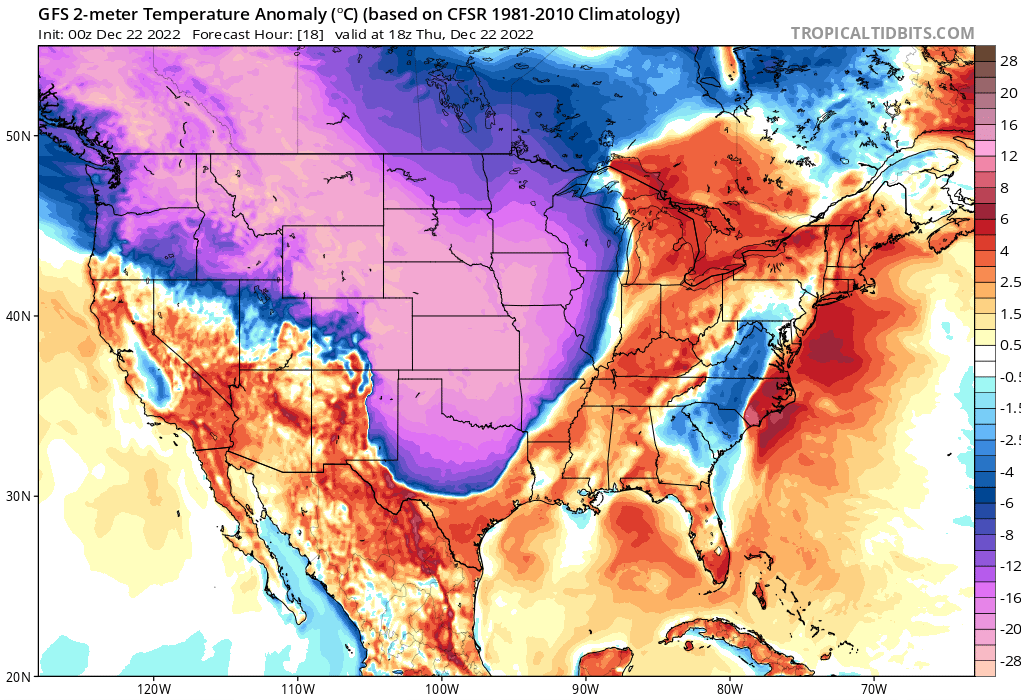

The first reason for the persistence of upward pressure on commodity prices is an event that has received little attention so far but could keep the price of Brent crude above $80/bbl and natural gas above $5.5/MMBtu in the short term. This event is a significant drop in temperature in most US states due to a raging Arctic storm.

{kind=link}

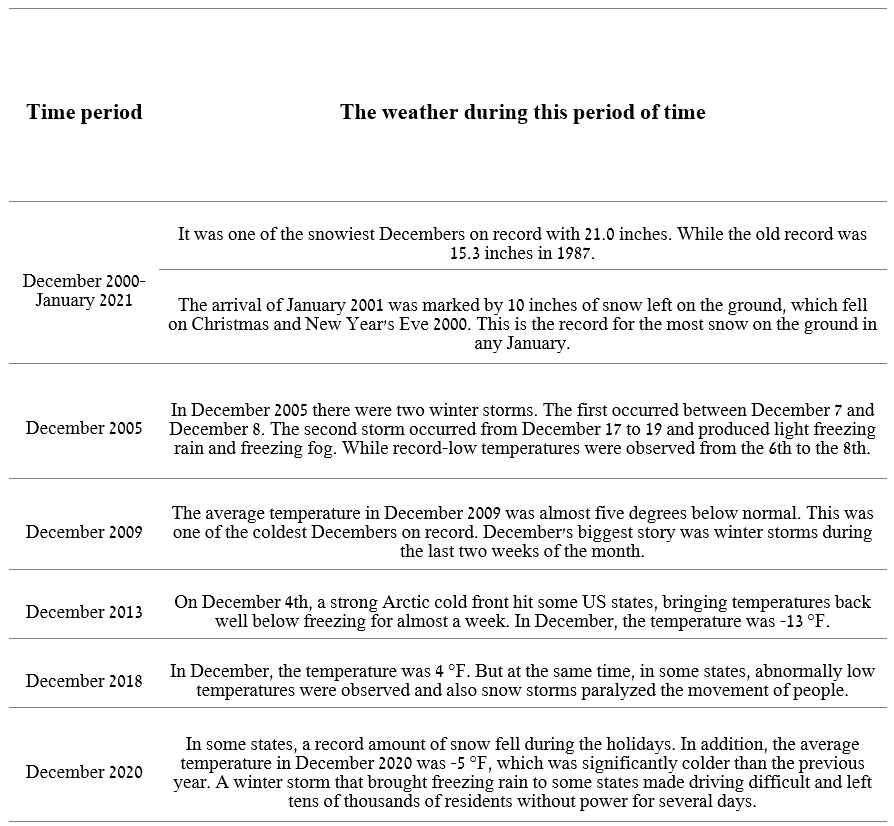

Given the current development of the winter storm, the approaching cold is reminiscent of events that took place in 2000-2001, 2009, 2013-2014, 2018, and 2020, when nature partially paralyzed the lives of millions of Americans and led to a significant increase in electricity consumption.

Author's elaboration, based on weather.gov

{kind=link}

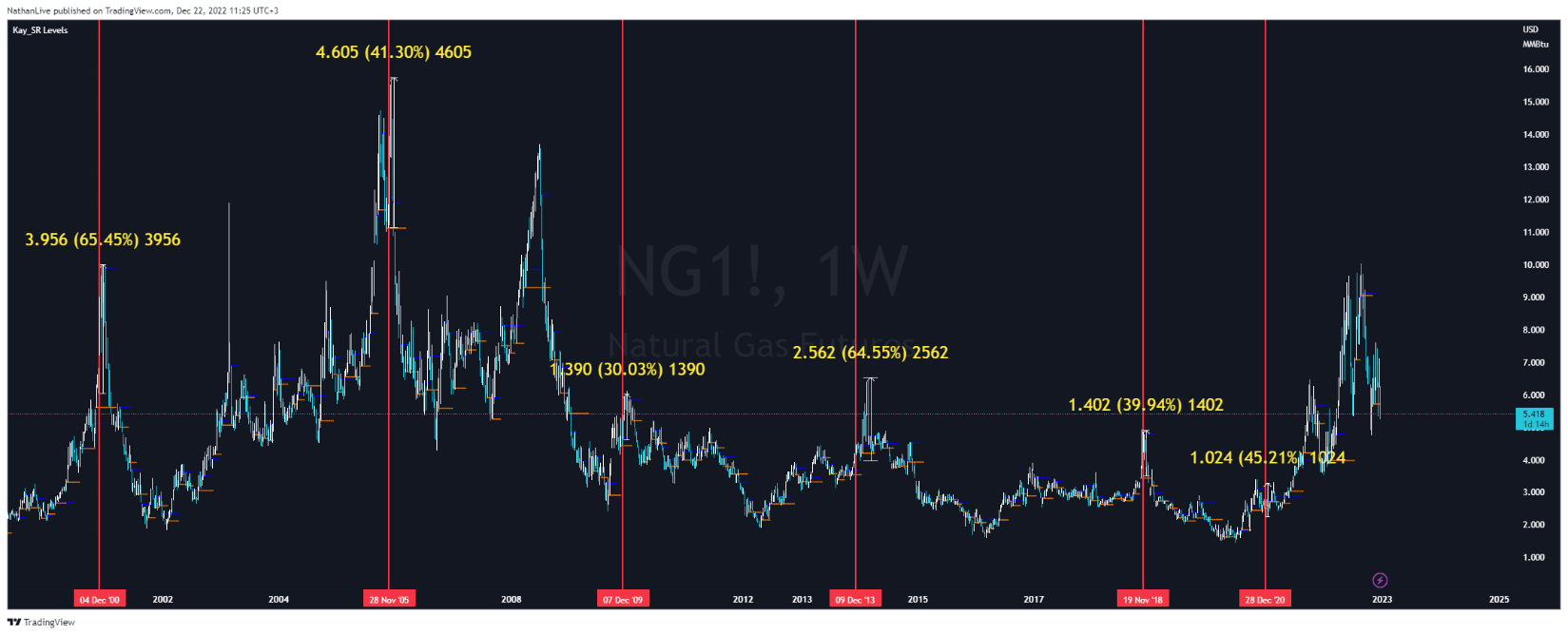

Snowstorms are expected this week and next in regions ranging from the Midwest to the northeast, including states such as Pennsylvania, Ohio, and West Virginia. What's more, temperatures over the Christmas holidays could drop well below freezing in southern regions, including Texas and Louisiana, which have some of the world's largest oil and gas fields. Historically, deteriorating weather conditions have led to a surge in the consumption of commodities, especially natural gas ( NG1:COM ) for home heating. As a result, record volumes of this fuel were taken from storage facilities, which led to an increase in its prices by at least 30%.

{kind=link}

Given the recurring historical pattern of the Arctic storm spreading across the US, I expect excessive demand for heating, which could lead to a significant increase in demand for hydrocarbons and also a decrease in their production due to freezing gas wells. Thus, this will temporarily aggravate the risks of a physical shortage of gas until the end of December 2022. As of December 21, natural gas prices stood at $5.332 per MMBtu, up slightly from the day before. According to my model, the natural gas spot price could rise to $6.8/MMBtu and stay in the $6.5-7/MMBtu range until the end of December. However, after that, prices will again fall below $6 due to the expected warming in the US and the progress made in resolving the crisis in the European energy sector.

{kind=link}

The weather is capricious and difficult to predict for the medium term, however, according to the model created by Tropical Tidbits , cold snaps are expected again at the end of the first week of January, which may affect the growth of prices not only for natural gas but may also lead to the start of a rally in prices for other non-renewable energy resources during January.

{kind=link}

Deterioration of the economic and epidemiological situation in China

China's economy continues to give warning signals despite the relaxation of the zero-tolerance policy for Covid-19, which the government has long addressed. However, after unprecedented protests swept the country, some of the restrictions were lifted. In addition, the tense situation in the real estate sector remains, the consequences of restrictive measures and the increase in the number of COVID-19 cases slow down the economic growth of the world's second economy. So, for example, the growth of industrial production on an annualized basis amounted to only 2.2%, slowing down significantly compared to the previous month, and was also lower than economists' forecasts.

Author's elaboration, based on Investing.com

{kind=link}

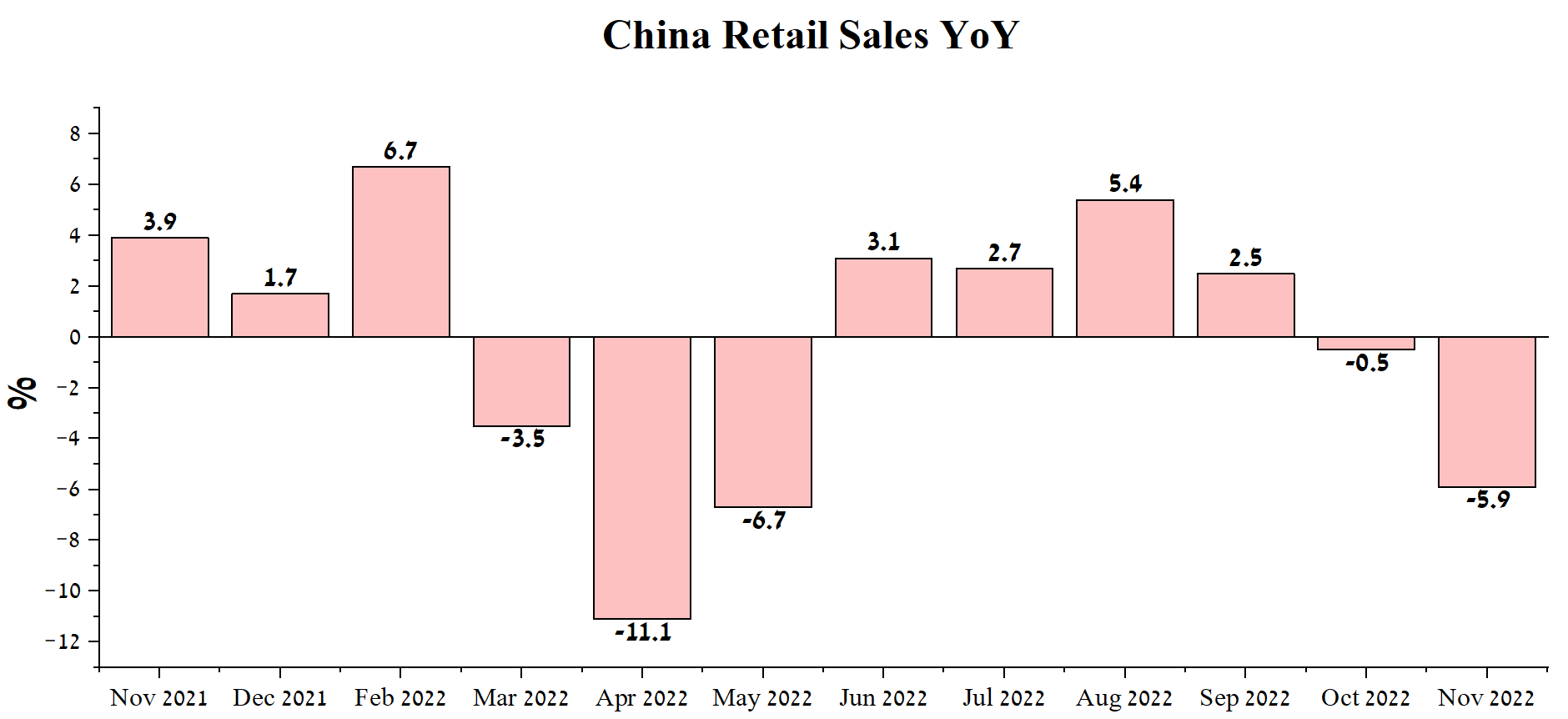

The effects of the Covid-19 zero-tolerance policy have begun to show in China's retail trade, which contracted 5.9% year-on-year in November 2022, continuing its downward trend. This was the second consecutive decline in retail sales and thus increased the risks of a recession in 2023. If it occurs, it will negatively affect the oil and gas industry, which continues to hope for a recovery in oil and gas demand from China.

Author's elaboration, based on Investing.com

{kind=link}

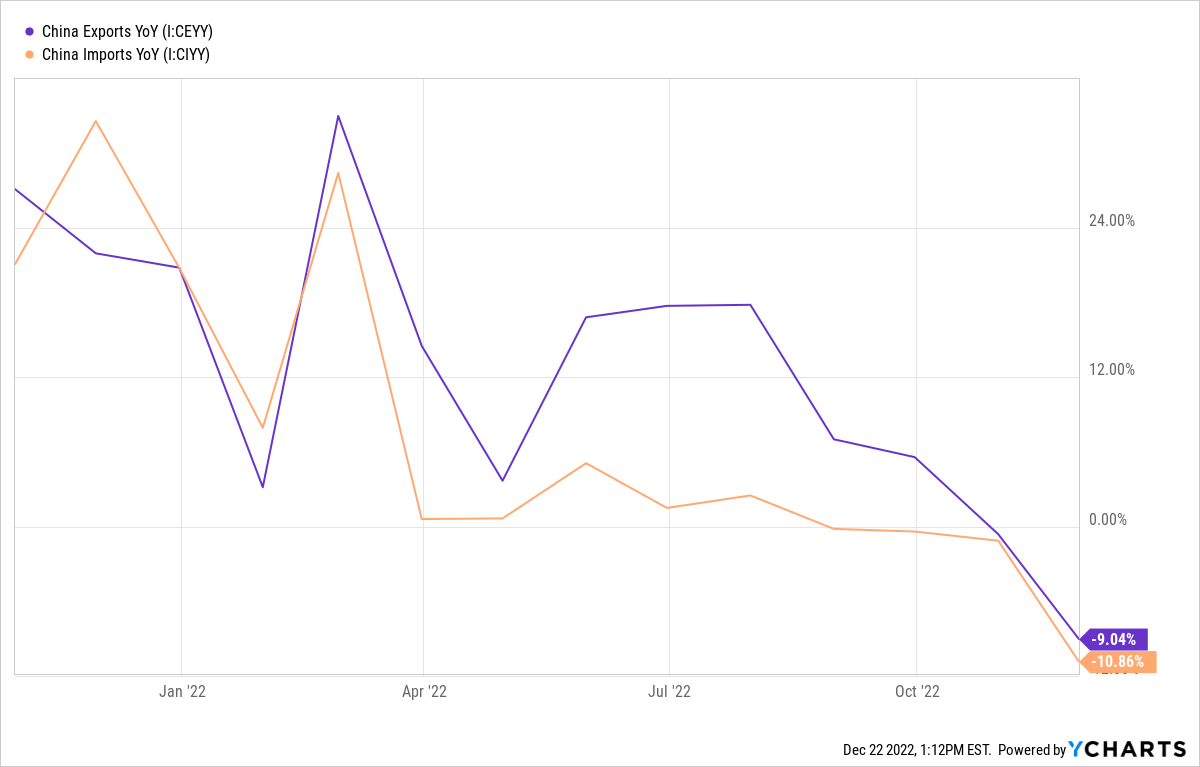

Exports fell by about 9.04% year on year due to weakening demand for Chinese goods caused by high inflation and supply chain disruptions. A more dramatic drop occurred with imports, which fell 10.86% year-over-year due to restrictions imposed by the Chinese government that weakened domestic demand.

{kind=link}

In my estimation, China's economic recovery is highly likely to be uneven due to a strong public sector and a significantly weakened private sector due to a falling real estate market. In addition, recent quarters can see a slowdown in global economic growth, which could lead to lower demand for Chinese goods and shift global demand towards services. As a result, I predict that oil demand will continue its downward trend in both 2022 and 2023 relative to 2021 and thus affect the decline in commodity prices.

{kind=link}

Russia is in a hopeless situation and is not able to threaten the global oil and gas industry

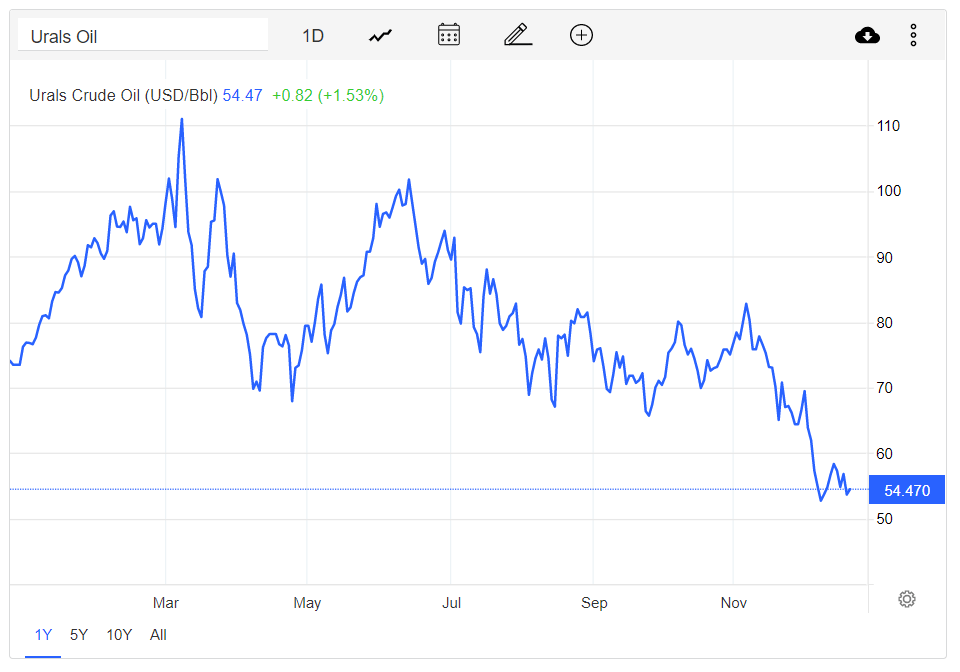

As a result of Russia's attack on Ukraine, numerous economic sanctions were imposed on the aggressor country to slow down the continuation of aggressive actions, and at the same time, the most serious of them began to operate only in the fourth quarter of 2022. Firstly, this will lead to a significant shortfall in tax revenues to the budget, with subsequent inflation higher than the Central Bank of Russia predicted in 2023. Despite the statements of the President of Russia that the economic situation in the country remains stable, this is far from the case and these statements are more aimed at an internal audience to reduce tension within society due to failures on the battlefield. As a result of the entry into force of sanctions on Russian oil, its price continues to remain below $60 per barrel and the threats of the Russian government to suspend oil supplies to countries that have imposed sanctions should not lead to real decisive action. The reasons for this are high spending rates from the National Welfare Fund ((NWF)) and limited domestic borrowing capacity.

{kind=link}

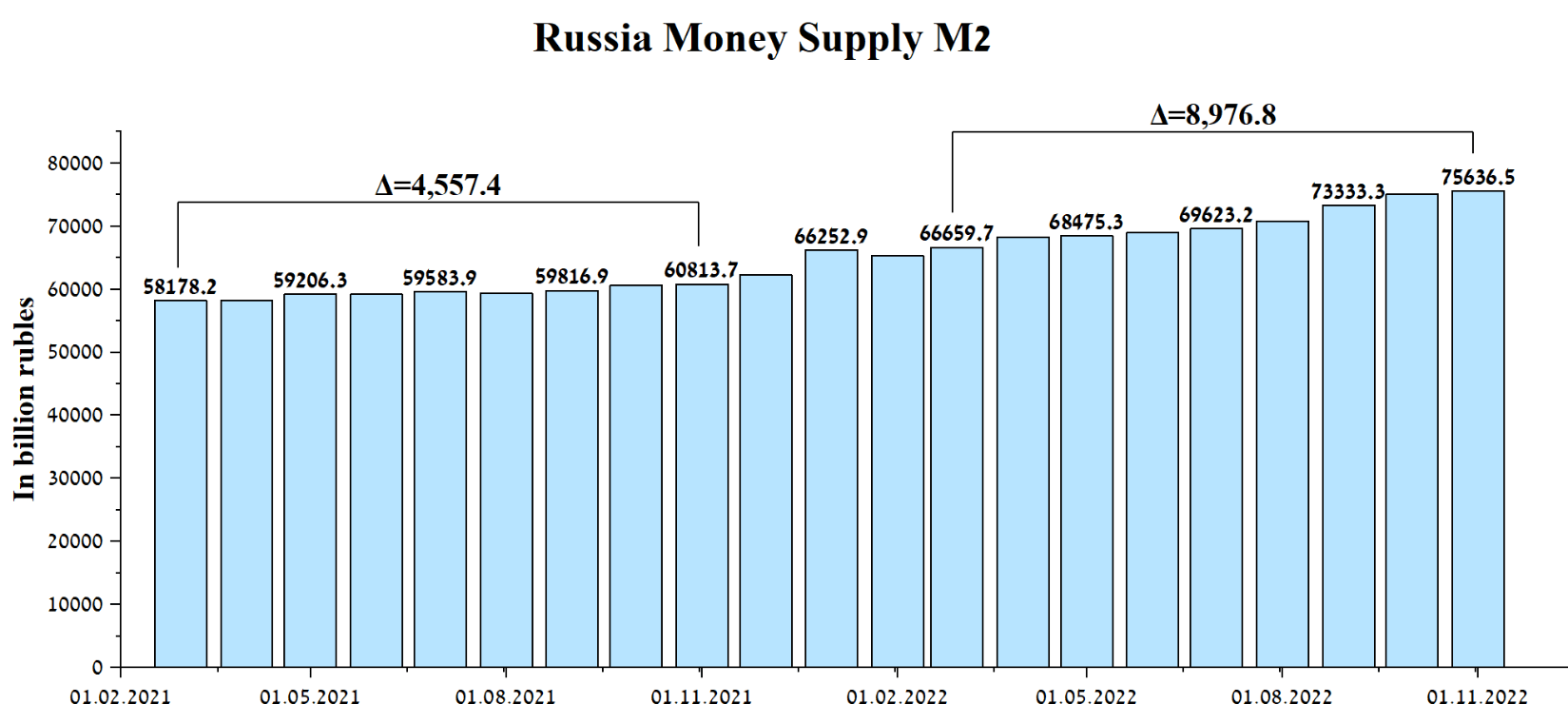

Given the ongoing freezing of Russia's international reserves, the use of the assets of the NWF is issuance financing, which ultimately leads to an increase in the money supply. In November 2022, the total money supply amounted to 75,636.5 billion rubles, an increase of almost 9 trillion rubles compared to the start of the military operation against Ukraine, which was one of the highest values since the collapse of the USSR. So, for example, for comparison, the growth rate of the M2 monetary aggregate in 2021 amounted to only 4.5 trillion rubles, and this was during the period when economic incentives were adopted to combat the consequences of the coronavirus.

Author's elaboration, based on the Central Bank of the Russian Federation

{kind=link}

In the second half of 2022, we already see a significant increase in the money supply, and a reduction in natural gas production, of which 39.1 billion cubic meters were produced in September 2022, which is 26.4% less than in September 2021. Moreover, the economic slowdown is beginning to hurt Russia's ability to snap back at US and European pressure. But even if the Russian government decides to go all the way in the confrontation with the most economically developed countries, this will only cause a rapid increase in inflation and may lead to the bankruptcy of subsidiaries Gazprom ( OGZPY ), Lukoil ( LUKOY ), etc.

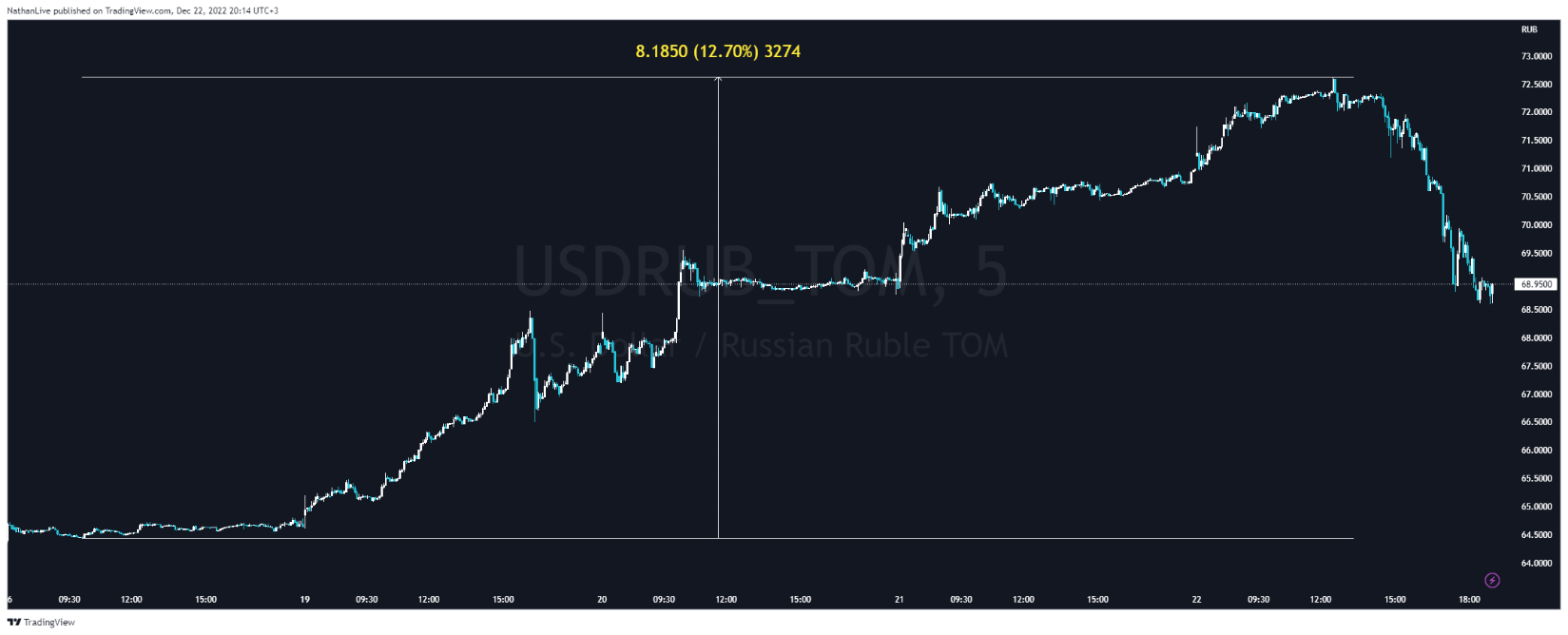

Given the sanctions imposed, Russia does not have the opportunity to buy equipment for the oil and gas sector, the demand for which should rise sharply in the coming quarters as the need to service oil production facilities grows. In addition, oil and gas companies are still limited in their ability to restore oil wells. As a result, I believe that the oligarchs and the President of Russia will not take drastic measures otherwise, they can lead to a significant deterioration in the economic situation of the country. At the moment, one can see the beginning of the weakening of the ruble against the US dollar, despite the introduction of trade sanctions, which radically limited imports and led to the accumulation of foreign currency in bank accounts. On December 22, the dollar exchange rate amounted to 72.5 rubles, having increased by 12.7% compared to the beginning of the week.

{kind=link}

US hydrocarbon reserves

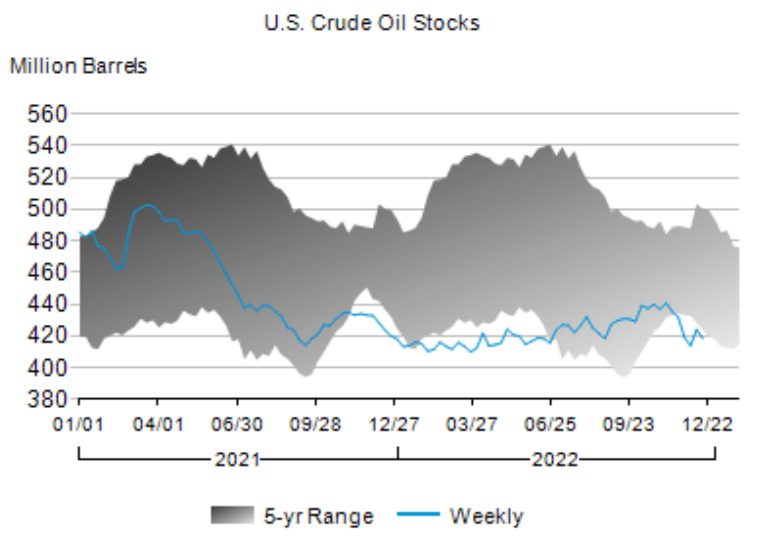

US commercial crude oil inventories , excluding those in the SPR, were 418.2 million barrels, down 5.9 million barrels from the week ended Dec. 12. Despite the hysteria in the media that occurred in the middle of summer that hydrocarbon reserves are declining at a high rate due to the desire of the US president to overcome inflation, they have remained stable in recent weeks.

Weekly Petroleum Status Report-EIA

{kind=link}

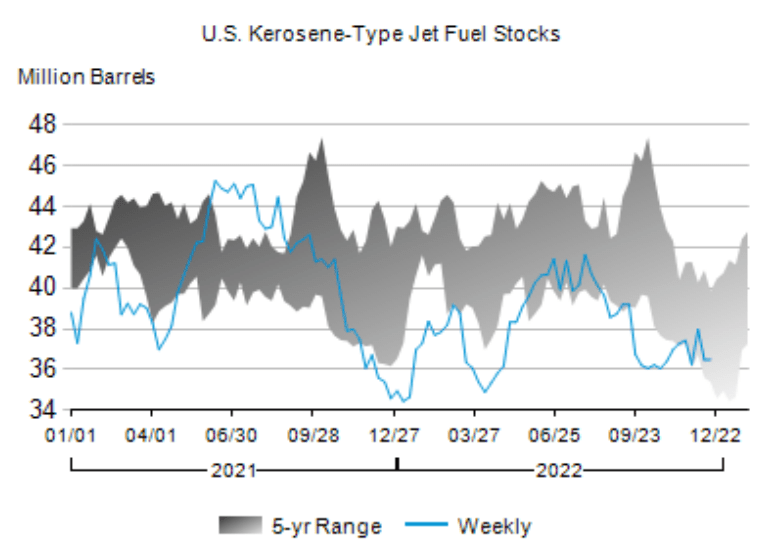

Total reserves of motor gasoline amounted to 226.1 million barrels, up 2.5 million barrels from last week and about 2 million barrels from the previous year. Moreover, stocks of kerosene-type jet fuel not only continue to be stable in recent months but have also increased relative to the end of 2021 despite a significant increase in demand for it from Delta Air Lines, American Airlines Group, and United Airlines Holdings during the holidays and the lifting of restrictive measures introduced in 2020-2021 to combat COVID-19.

Weekly Petroleum Status Report-EIA

{kind=link}

However, the negative side of the latest statistics and which may give investors hope for the short-term growth of the Energy Select Sector SPDR ETF is a decline in imports from Canada and refinery utilization, which amounted to 90.9%, showing a decrease of 1.3% compared to the previous week. The main reason for the decline in oil imports from Canada is the damage to the Keystone pipeline section. Given the spread of the snowstorm across the United States, it is not entirely clear how soon the pipeline operator TC Energy ( TRP ) will be able to restore the volume of hydrocarbon pumping to the Gulf of Mexico.

Conclusion

Global economic uncertainty continues to be high and downside risks are rising in most Asian and European countries due to the inability to fight inflation effectively despite continued monetary tightening by central banks. In the short term, hydrocarbon prices will be supported by the need for the US to replenish its Strategic Petroleum Reserve and abnormally low temperatures.

I estimate total oil demand at 101 million barrels per day (BPD) in 2023, up slightly from 2022, driven by recovering demand for diesel and jet fuel in North America and India. On the other hand, the main reasons for the lack of a significant increase in energy demand are the continued tense situation with industrial production in China and the inability of the Chinese government to effectively deal with COVID-19. The deplorable situation in the real estate sector can lead not only to a decline in demand for oil and gas but also to a decrease in purchasing power, which will negatively affect the financial position of such mastodons of the industry as Alibaba ( BABA ) and JD.com ( JD ).

The persistence of uncertainty about Russian oil and gas production after the start of sanctions should not lead to an actual decline in global hydrocarbon production. For example, the total number of drilling rigs in the United States has reached record levels since 2020, and oil and gas companies that are part of the Energy Select Sector SPDR ETF were able to restore oil drilling activities to pre-pandemic levels. In my opinion, the USA, Canada, and Brazil will become the main countries capable of radically increasing the volume of fuel production and thus leveling the impact of production quotas introduced by OPEC. In general, I expect oil production in 2023 to increase by 3 million barrels per day compared to 2022 and thereby create downward pressure on its price.

As a result of deteriorating weather conditions in most US states, increased volatility in the commodity markets should be expected in the coming weeks, which should not be underestimated by either bulls or bears. However, as temperatures rise in the southern states, this will not only reduce gas withdrawals from storage but also lead to an increase in its production by oil and gas companies in 2023. As a result, this will drive down US commodity prices and inflation in line with the policies of the Biden administration, with a consequent possible shift of institutional investors away from Treasury bonds ( US10Y ) ( US2Y ) and commodity companies towards higher-beta stocks from the technology and healthcare sectors.

For further details see:

What Awaits The Oil And Gas Industry In 2023