HBCYF - What HSBC's SVB U.K. Deal Could Mean For Investors

2023-03-14 09:53:00 ET

Summary

- HSBC Holdings plc agrees to acquire SVB Financial Group's UK-based business for merely £1.

- Although a distressed asset, SVB's UK-based segment is a going concern with an accounting surplus.

- HSBC's liquidity might prevent SVB UK's depositors from heading for the floodgates. Moreover, the acquisition will likely form part of HSBC's long-term growth strategy.

- The target's risk profile is unlikely to deter HSBC's balance sheet as the latter possesses a substantial asset base and risk-off capital adequacy metrics.

- In our view, HSBC stock's current risks pertain to a newly evolved countercyclical environment and mainstream's "flight to safety" instead of potential structural breaks within the firm.

In a drastic turn of events, HSBC Holdings plc ( HBCYF ) has snapped up SVB Financial Group's (NASDAQ: SIVB ) UK lending division. After a cry for help from UK-based tech firms, it was revealed on Monday morning that the UK government would collateralize SVB's UK-based deposits. However, in a plot twist, news broke shortly after that HSBC had agreed to acquire SVB's UK lending unit instead.

According to HSBC, the deal is worth a mere £1 , which includes a holistic buyout of SVB's UK segment, less any non-financial assets and liabilities. Although the finer details are yet to be revealed, it is understood that SVB's UK unit will operate as usual, with all future benefits and liabilities accruing to HSBC.

Considering the opaqueness of the acquisition, we decided to assess the scenario based on parsimonious material and public information. This thesis provides a somewhat subjective opinion on what the acquisition means for HSBC's shareholders.

A Holistic Risk Assessment

SVB UK looks like a going concern

First and foremost, the central question needs to be defined: Is this a bailout by HSBC to prevent systemic risk, or does HSBC believe that SVB's UK-based unit will provide future value?

Well, it is not a simple yes or no answer. However, it can be gleaned that SVB UK is being acquired as a going concern because reports suggest that SVB Financial Group's failure was driven by its U.S.-based business activities. Moreover, the segment's most recent impairment test conveyed that the entity possesses approximately $6.8 billion in loans, around $8.14 billion in deposits, and anticipated tangible equity of $1.82 billion.

At face value, the deal brings a significant amount of financial prospects with it as it does not only include sufficient deposits to cover its outstanding loans but also tangible equity. Nevertheless, matters should not be looked at discretely as the debt market is in shaky territory.

Debt Portfolio's Prospects Assessed

SVB's UK business offers a range of banking solutions to its clients ranging from current accounts for start-ups, fundraising, and public market activities such as SPAC deals or regular IPOs.

After scanning the mother company's financial statements, it became increasingly clear that limited segmental information is provided as the firm consolidates its results at any given opportunity. Thus, providing little transparency about its balance sheet's composition.

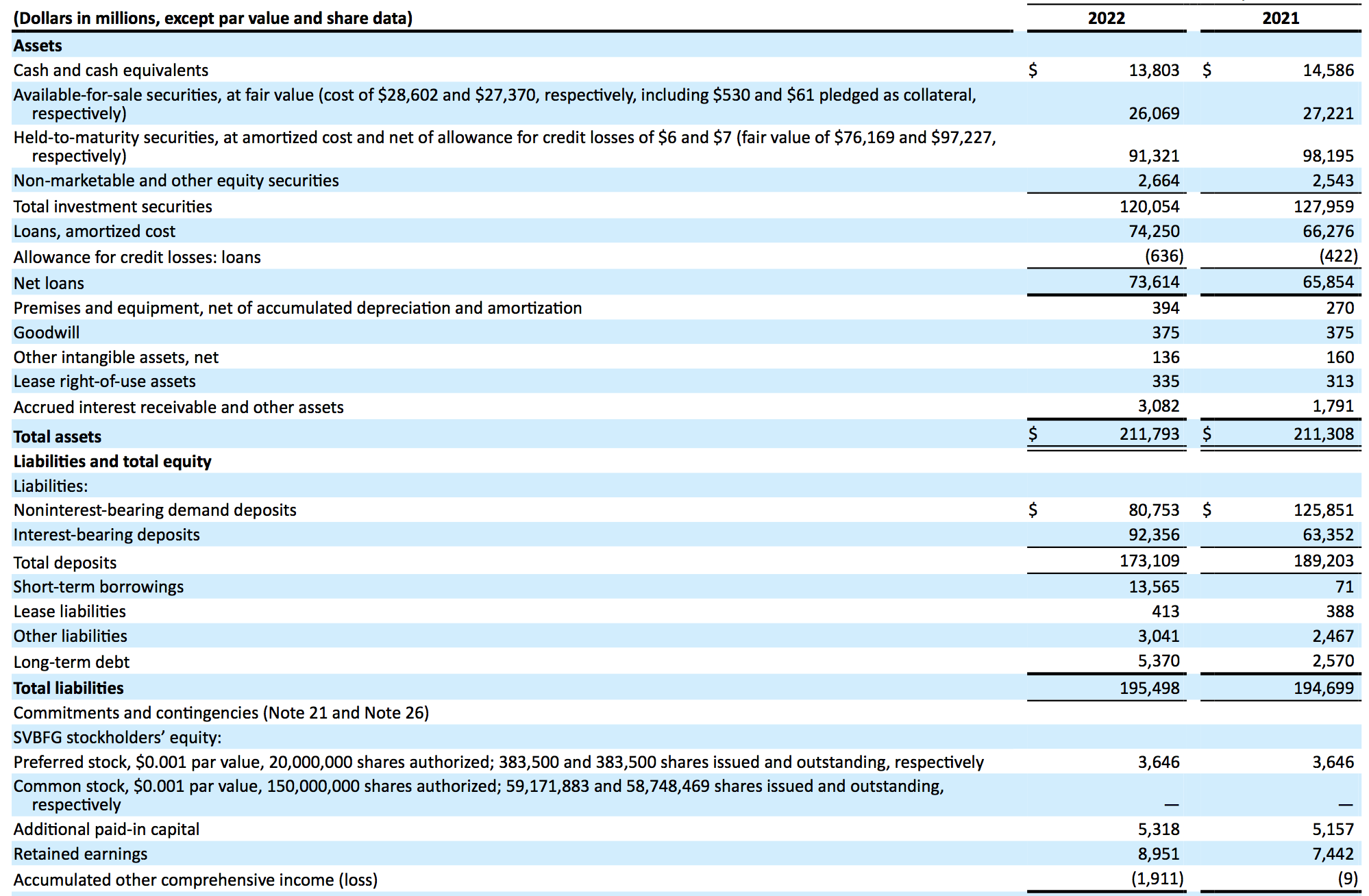

SVB UK and SVB's broad-based business model have shared the same concerns over the past twelve months, which relates to surging demand for start-up deposit withdrawals and limited returns on invested securities. Many of the bank's clients started spotting these concerns a few quarters ago, which caused an exponential draw on deposits as anxiety started developing regarding the bank's ability to sufficiently cover its deposits. The bank's broad-based balance sheet, included below, provides a visual of what I just mentioned.

Click on Image to Enlarge (SVB Financial's Balance Sheet)

{kind=link}

From here on in, the question becomes: Will the aforementioned risks persist after HSBC's acquisition of SVB Financial's UK-based bank?

Again, I must stress that limited transparency is provided on SVB's asset base. However, a parsimonious opinion provides an indication of what is to come.

In our opinion, venture-based deposits and ancillary services will continue to struggle until we experience a macroeconomic recovery. I say this because early-stage businesses are pro-cyclical and usually suffer significant setbacks during economic contractions . In addition, the volume of creative public market offerings, such as SPACs and small-cap IPOs, is still in decline, disincentivizing prospective clients of SVB's UK-based unit.

{kind=link}

Despite SVB UK's ongoing fundamental risks, as discussed in-depth later in the article, HSBC's takeover will probably back out most of the target's capital adequacy risk as HSBC possesses a significant amount of liquidity relative to SVB Financial.

In essence, we argue that SVB's UK-based business unit will sustain its short-term risks due to the uncertain global macroeconomic environment. However, HSBC's acquisition will probably provide depositors with less fear of counterparty risk.

Assessing HSBC's risk

In a broader context, we do not believe HSBC's SVB acquisition will alter the company's risk profile as SVB's risky asset base of $6.8 billion in loans is a drop in the ocean versus HSBC's existing asset base of more than $3 trillion.

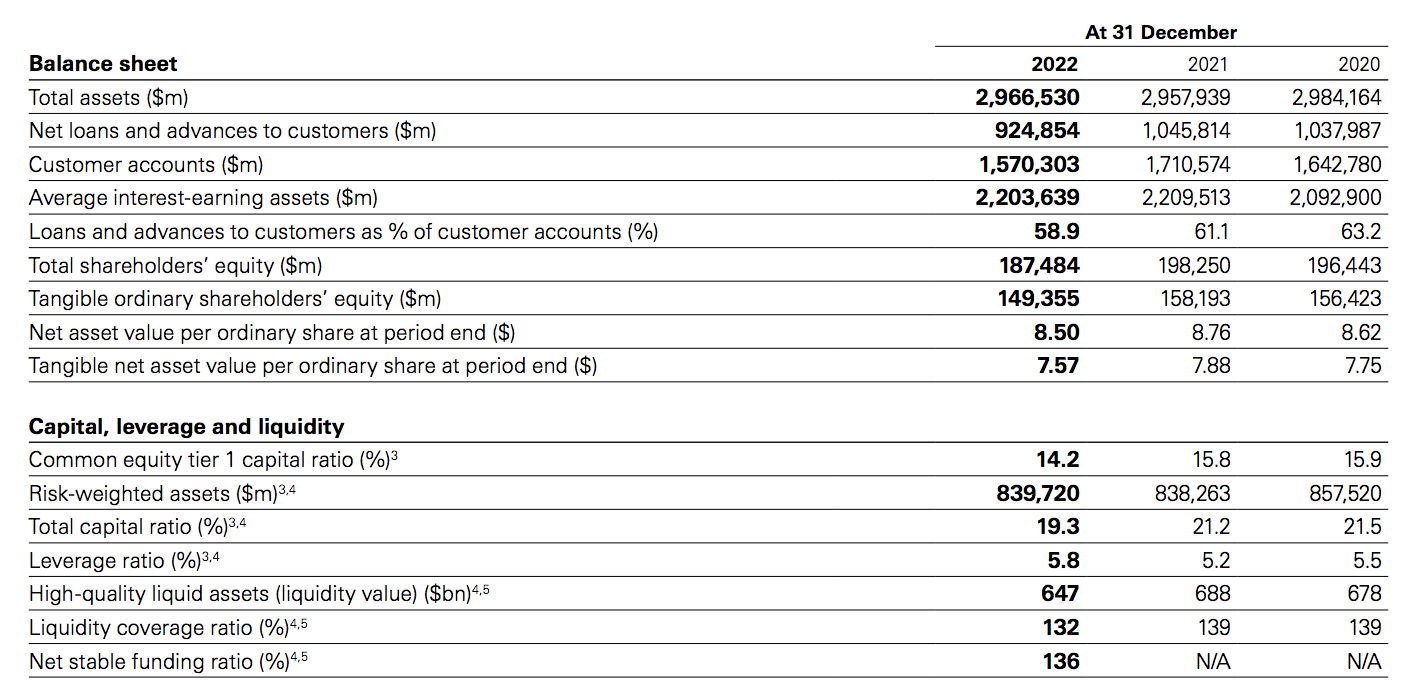

Furthermore, HSBC hosts a Common Tier 1 Equity Ratio of 14.2%, which is phenomenal considering the regulatory requirement is 4.5% . Additionally, the bank's net stable funding and liquidity coverage ratios both comfortably exceed 100, meaning HSBC possesses enough stable funding to cover its projected short-term outflows and its asset bases' default risk.

{kind=link}

In our opinion, HSBC's investors will not price the SVB UK acquisition's risk. However, we might see a scenario where depositors start withdrawing funds based on the mainstream narrative, which is that the biggest banking failure since 2008 has occurred, meaning a pending banking crisis is en route. In simpler terms, there is little correlation between the balance sheets of HSBC and SVB Financial Group; however, the general population might not think that far and instead withdraw capital from HSBC in fear of counterparty risk.

Furthermore, SVB Financial Group's failure will likely spark a prolonged cyclical stock sell-off as the bank's failure conveys the fragilities baked into today's economic environment.

Final Word

In our view, HSBC's acquisition of SVB Financial Group's UK-based banking business is a tactical play to secure a high-yielding going concern. HSBC will likely prop up the bank's balance sheet and use it as part of its holistic, long-term growth strategy.

Furthermore, despite concerns about the global banking system, we have not identified any structural risks embedded into HSBC's framework; however, we urge investors to think about what impact the "flight to safety" mainstream narrative might have on the bank's deposits and its stock price.

For further details see:

What HSBC's SVB U.K. Deal Could Mean For Investors