AA - What It Takes For Alcoa Stock To Double

2024-01-19 13:29:43 ET

Summary

- Alcoa Corporation has a history of doubling in stock price during periods of economic growth, with recent surges of 120%, 300%, and 1,500%.

- The company reported flat revenue and improved net loss in 4Q23, with lower revenues due to decreased aluminum and alumina prices.

- Alcoa's outlook suggests a potential market shortage in the alumina market and a balanced market with a slight surplus in the aluminum market in 2024.

Introduction

I have to admit, using a title that includes something related to a potential stock price double always feels a bit sketchy. After all, almost all stocks we discuss on Seeking Alpha are dividend growth opportunities that come with lower returns - at least on a short-term basis.

However, when dealing with what I like to call "macro proxies," it is not unlikely to encounter stocks that have the potential to (more than) double in certain situations.

That's where Alcoa Corporation ( AA ) comes in.

America's largest aluminum producer (The Al uminum Co mpany of A merica) is a very cyclical company because aluminum demand is tied to the health of the transportation industry, the production of appliances (housing market), consumer goods like soda cans, and other products.

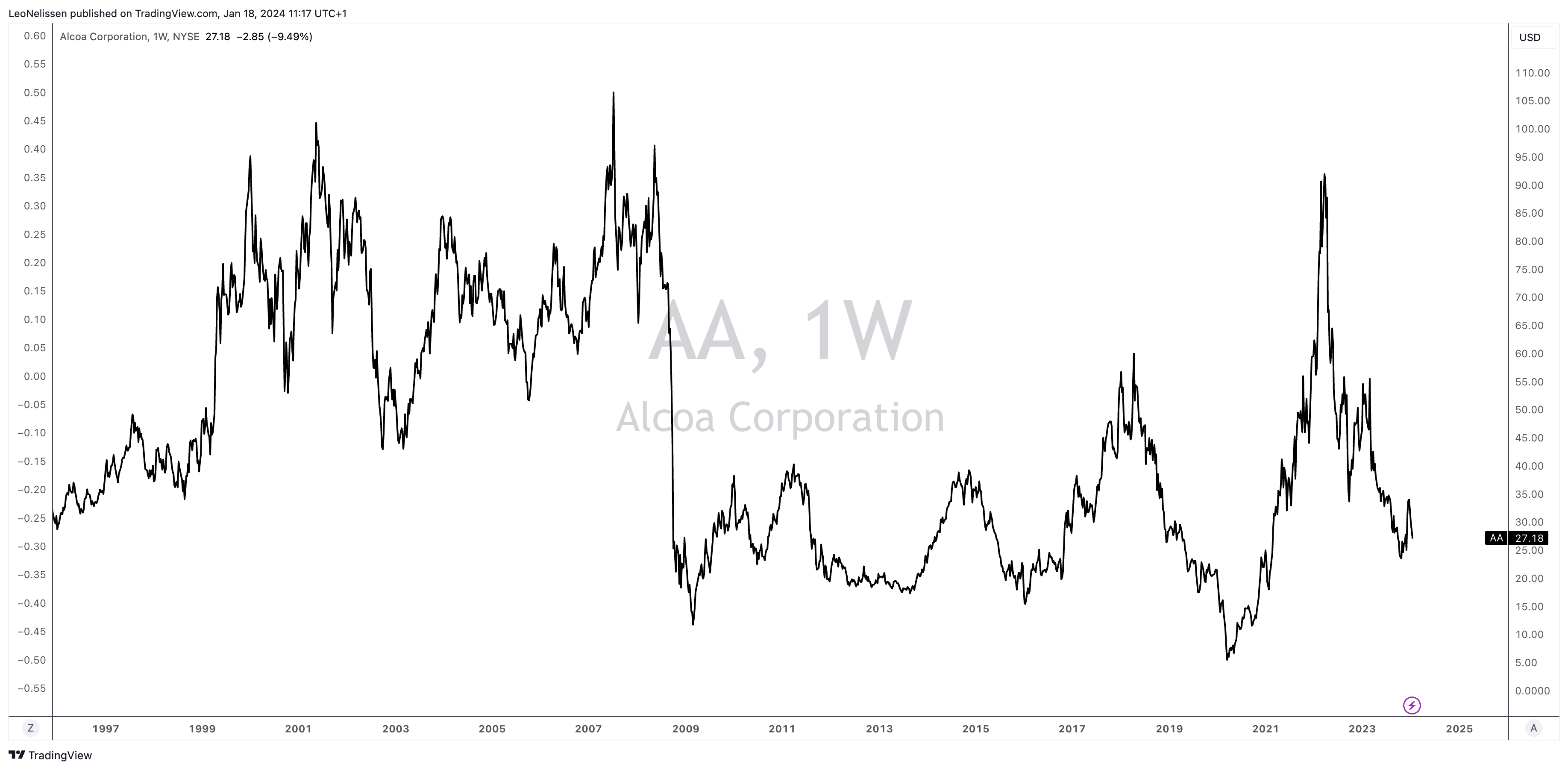

Looking at the long-term stock price chart below (this includes the past spinoffs Arconic and Howmet Aerospace ( HWM )), we see that the company has a history of doubling whenever economic growth turns from a headwind into a tailwind.

TradingView (AA)

{kind=link}

These are the most recent stock price surges that were backed by recovering economic growth (from the start of the rally to the peak):

- 2013: +120%

- 2016: +300%

- 2020: +1,500%.

In other words, the worse the selloff, the higher the return potential.

After all, none of these gains came without pain, especially not for long-term investors.

Currently, AA is trading at $27 again, which is down from its prior cycle high of roughly $91.

My most recent article on the company was written on October 23, 2023, when I used the title "Alcoa Has A Very Bright Future, But Not Without Risks."

Since then, the stock price is up 18%, beating the S&P 500 (SP500) by roughly 500 basis points.

In this article, I'll revisit my thesis, using the company's just-released quarterly earnings and macroeconomic developments.

So, let's get to it!

What's Alcoa Up To?

Let's start with the dry, somewhat boring numbers.

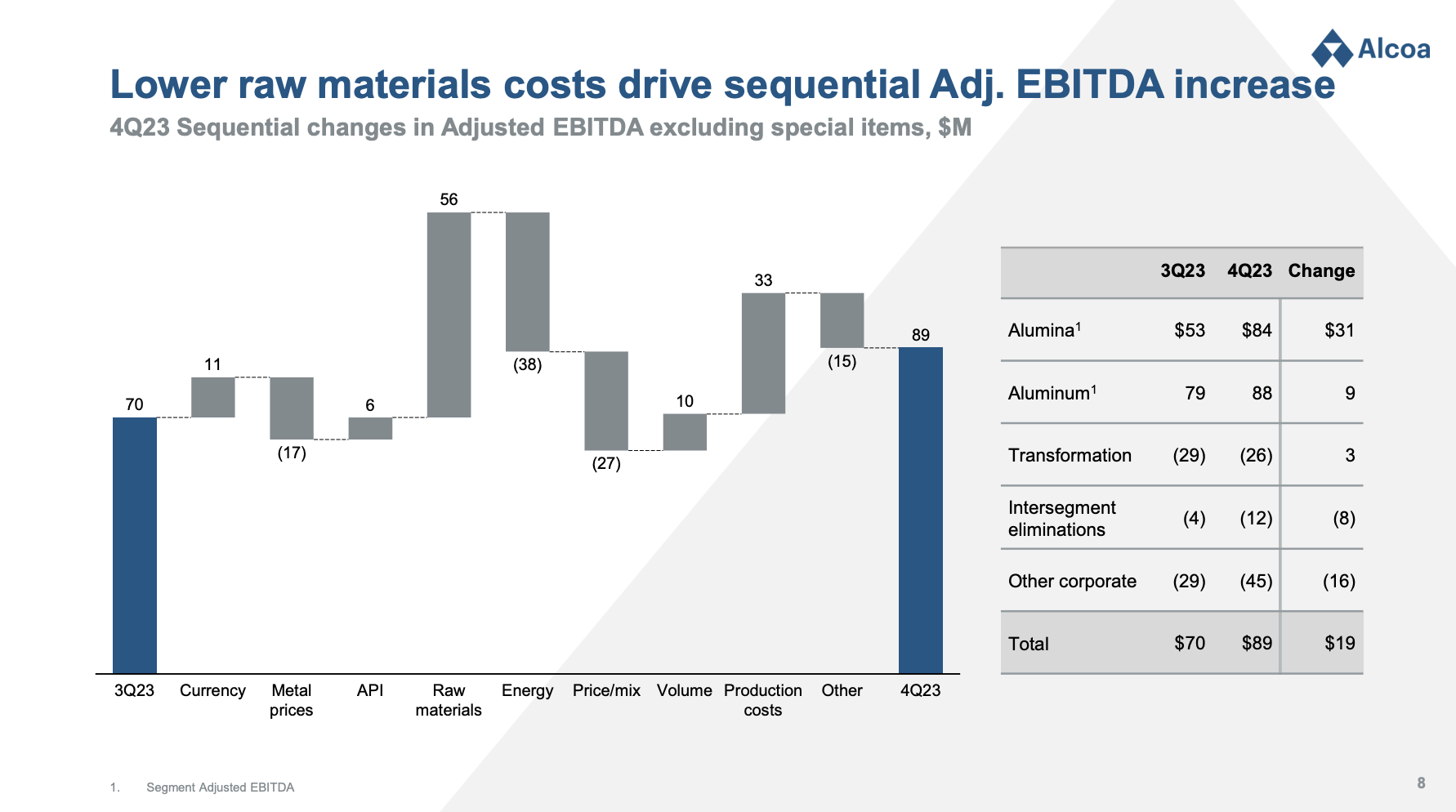

In the final quarter of last year, the company reported that revenue remained flat sequentially at $2.6 billion.

The net loss attributable to Alcoa improved to $150 million, and the adjusted EBITDA increased to $89 million.

Notably, the net loss showed improvement, and adjustments were made for the recording of a valuation allowance on deferred tax assets in Brazil, net of noncontrolling interest.

{kind=link}

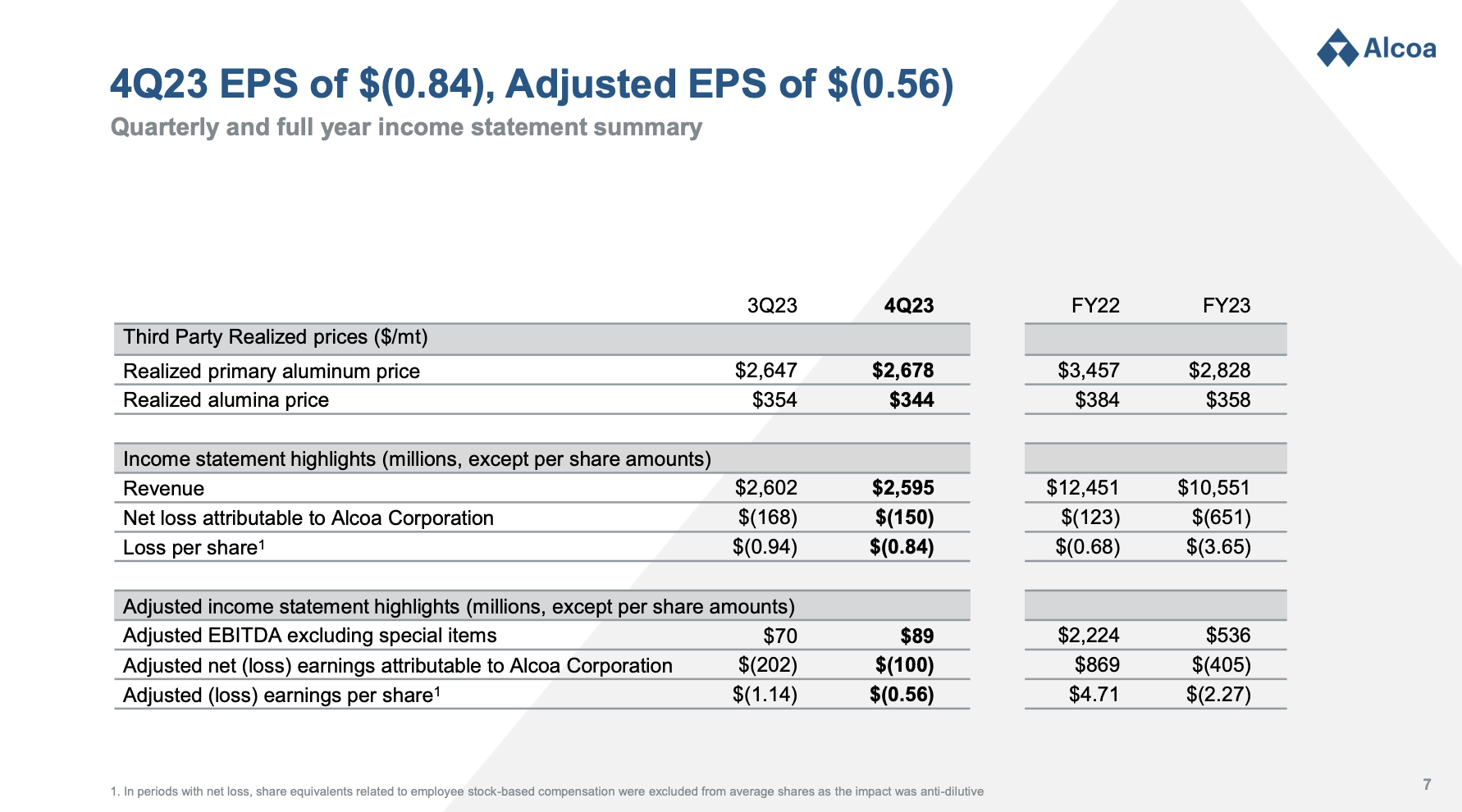

For the full year 2023, there was a year-over-year decrease in revenues by $1.9 billion to $10.6 billion. The net loss attributable to Alcoa worsened to a loss of $651 million, or $3.65 per share.

- Adjusted net income changed from $869 million in 2022 to a loss of $405 million in 2023, or $2.27 per share.

- Adjusted EBITDA, excluding special items, moved from $2.2 billion to $536 million.

{kind=link}

As we can see above, a major driver of lower revenues was pricing. Both realized aluminum and alumina prices were down compared to 2022 levels.

That is no surprise, as 2022 benefited from higher economic growth as well as the Russian invasion of Ukraine, which caused aluminum prices to fly.

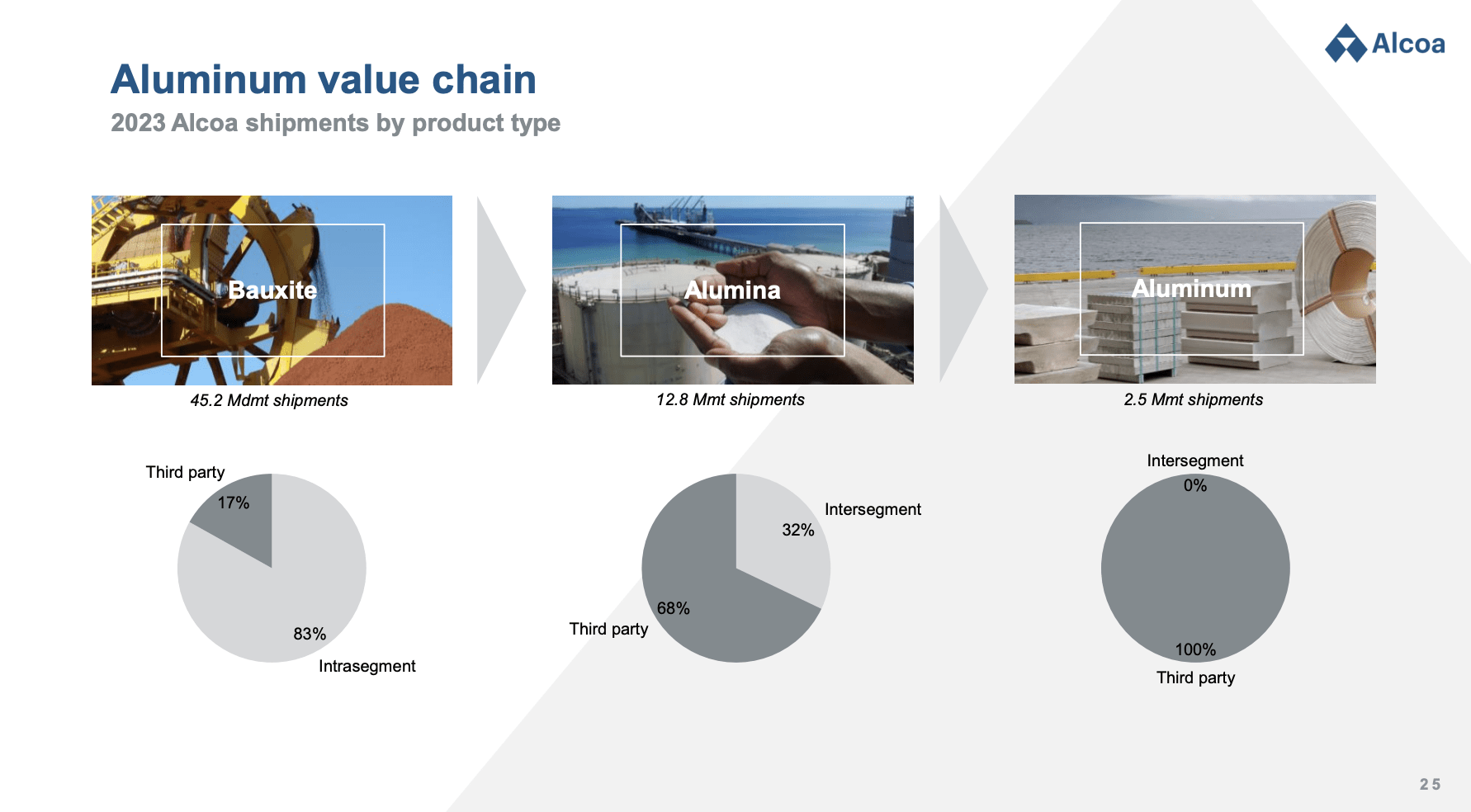

Before we move over to the very important outlook, the company noted that it achieved a significant milestone by announcing the approval of its bauxite mines in Western Australia.

The approved bauxite mines in Western Australia serve as a testament to Alcoa's commitment to securing and expanding its resource base.

Bauxite, being a primary source of aluminum, is key to Alcoa's supply chain, and the approval signals a strategic move to ensure a stable and sustainable supply of raw materials.

As we can see below, 83% of bauxite is used in its own company to produce alumina.

{kind=link}

However, on the flip side, the company also announced the curtailment of the 60-year-old Kwinana refinery located in Western Australia.

The decision to curtail the refinery (in the second quarter of this year) was based on a comprehensive assessment, considering factors such as the refinery's age, scale, operating costs, current bauxite grades, and prevailing market conditions.

{kind=link}

Speaking of market conditions, there's one big reason why I always urge investors to follow Alcoa's earnings, even if they have no exposure or any plans to ever buy Alcoa.

Alcoa, being the largest aluminum producer in America, offers valuable economic insights on top of a detailed overview of its operations.

Looking Into The Future & What It Means For Shareholders

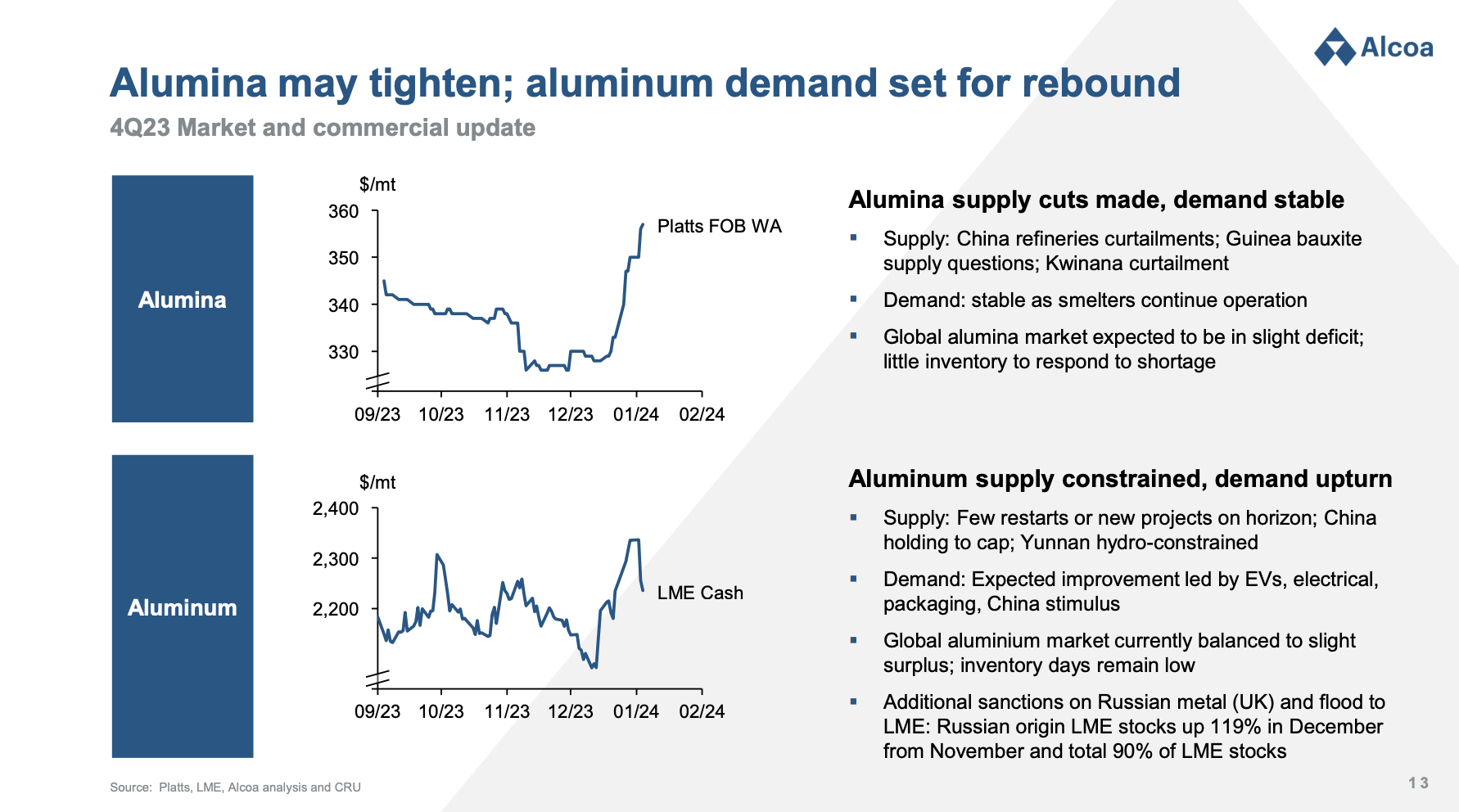

During its Q4 earnings call , the company noted that in the alumina market, prices experienced a surge at the close of the fourth quarter, primarily influenced by Chinese refinery curtailments and concerns regarding Guinea bauxite supply.

Projections for 2024 suggest a market shortage, with sustained demand from smelters and limited inventory availability, which is bullish.

In the aluminum market, the company anticipates a balanced market with a risk of a slight surplus in 2024, contingent on the pace of demand recovery throughout the year.

Several factors contribute to this outlook, including announced restarts and new projects, as well as hydropower shortages in China.

The good news is that demand stabilization in North America and Europe is noted, with regional premiums on the rise due to widening contango and increased transportation costs for imported metal.

{kind=link}

Furthermore, the company's order book indicates stabilization in value-add product orders, with premiums showing signs of firming up.

Although VAT premiums are lower than their historical peaks, they remain above conventional levels.

Meanwhile, anticipated government stimulus programs in China are expected to drive demand growth, particularly in the aluminum-intensive electric vehicles and renewable power infrastructure sectors.

Additionally, improvements in packaging demand are foreseen as inventory destocking reaches completion.

While these developments haven't been able to push Alcoa's stock price up, I expect tailwinds to get stronger once cyclical demand improves.

For now, the leading ISM Manufacturing Index does not indicate that this could be the case in the weeks ahead, especially because the Empire State Manufacturing Index made a new multi-year low in December, which does not bode well for overall manufacturing health.

Moreover, the company noted that noteworthy concern arose from the significant increase in the share of Russian metal stocks on the London Metal Exchange in December, reaching 90%.

Essentially, the predominance of Russian-origin metal, subject to tariffs and legal prohibitions, raises uncertainties about the accuracy of the LME exchange price for non-Russian aluminum.

Reuters

According to Reuters :

There are no blanket Western sanctions on Russian aluminium and the LME has previously rejected calls to suspend the warranting of Russian brands.

Rather, the exchange has tweaked its delivery rules to reflect unilateral measures such as the penal import duties on Russian metal imposed by the U.S. government in February last year.

In light of (always present) pricing uncertainty, Alcoa is focusing on its bottom line.

To enhance profitability, the company focuses on various initiatives, categorizing them into near-term actions, medium-term opportunities, and market improvement.

For example, near-term actions include targeted raw material savings, with approximately one-third already realized, and a $100 million benefit from a program aiming to reduce controllable operating costs across the organization.

Medium-term opportunities include the prospect of leveraging superior bauxite grades in Australia.

During the earnings call, the company identified market improvements, specifically emphasizing favorable trends in metal and alumina prices, as key for enhancing EBITDA, particularly within the metals segment.

Valuation

I often mention that putting a price target on stocks that are driven by commodity prices is tough.

- Analyst estimates are often based on current commodity prices (or a normalization of prices in case prices are currently elevated. Analysts tend to refrain from incorporating commodity price expectations into their models. They often keep it close to consensus expectations.

- Predicting commodity cycles is tough, as it often involves finding the exact economic bottom.

With that said, if you're bullish on Alcoa, you're probably "alone."

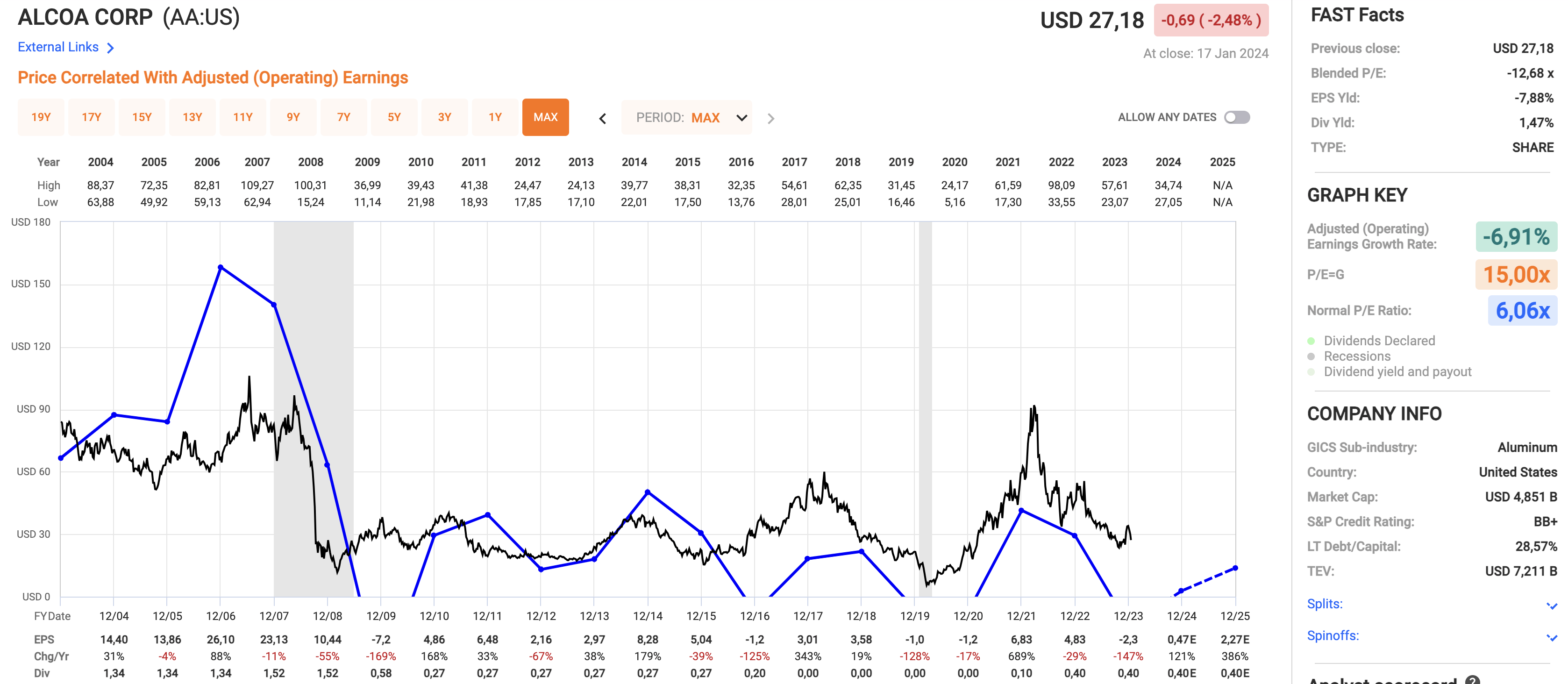

Using the data in the chart below:

- AA is expected to generate just $0.47 per share in EPS this year, which would be in line with a gradual recovery.

- In 2025, EPS is expected to be $2.27, indicating a surge of nearly 400%. Despite this growth rate, it would still be below levels seen during prior recoveries.

{kind=link}

As a result, AA does not appear to be cheap.

Using the data in the chart above again, AA's normalized valuation is 6.1x earnings, which is fair given the cyclicality of its business.

While AA's focus on value-added products will allow for a higher valuation over time, 6.1x earnings is a fair number for the time being, I think.

Based on the current projected recovery, AA has a fair price target of just $13, which is way below its current price of $27. This is purely based on its normalized valuation multiple and expected EPS growth.

That price target would certainly be fair if we were to enter a prolonged recession. However, if we get a growth recovery in the next four quarters, we will almost certainly see much higher.

The current consensus price target is $31, which is 14% above the current price.

For now, that makes sense.

However, based on improving aluminum market fundamentals and the increasing likelihood of an economic recovery in the second half of 2024, I believe the stock could bottom in the $20 to $25 area with an upside to $60 in the next two to three years.

I currently do not own AA but will likely initiate a position if we get a confirmation of a bottom in growth indicators or if AA drops below $25 again.

Takeaway

Despite its historical volatility, Alcoa has a track record of significant gains during economic upswings.

While the recent financials show some challenges, particularly in lower revenues and net losses, Alcoa remains resilient.

The approval of bauxite mines in Western Australia and strategic decisions like curtailment in the Kwinana refinery reflect a commitment to long-term stability.

Looking ahead, the alumina market projects a shortage, and the aluminum market anticipates a balanced scenario, offering potential opportunities.

While short-term projections may seem conservative, Alcoa's focus on value-added products and market improvements hints at a promising future.

Investors should keep a close eye on economic indicators and consider a position if growth indicators confirm a bottom or if the stock drops below $25.

For further details see:

What It Takes For Alcoa Stock To Double