PDO - What The Fed Really Wants

2023-03-28 13:21:51 ET

Summary

- The Fed is very worried indeed: systemic financial risk is growing.

- Fed credibility will support financial markets for a while. It is a crucial asset now to engineer a soft landing.

- There is a window of opportunity this year to cure the macroeconomic problem before it gets worse.

The Federal Reserve has just raised the Federal funds rate by another 0.25%. They did it - for the ninth time in a year - in spite of the fact that, in their own words : "Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring and inflation. The extent of these effects is uncertain".

We were told that the Fed was "between a rock and a hard place" and "under pressure to pivot away from its inflation control efforts", to contain financial instability. But the Fed not only raised rates again; it also did not rule out further hikes in the coming months. Does this mean that they are underestimating the risk of financial instability? Not at all. The Fed is very worried indeed, and is in a hurry: time is short. The truth is, a quick and complete disinflation is probably the only path to financial stability in the current situation.

To see this, please consider the structure of commercial bank's balance sheet. As we now all know, the present looming financial crisis originates in a broad interest rate risk mismanagement. Banks' assets are mostly long term (average duration is almost 6 years), fixed interest rate securities; unfortunately, these were bought when their yield was very low, and the banks are almost stuck with them. While banks' liabilities are mostly short term; and short-term rates have been sharply rising for a year .

Banks: balance sheet structure (Banking for society)

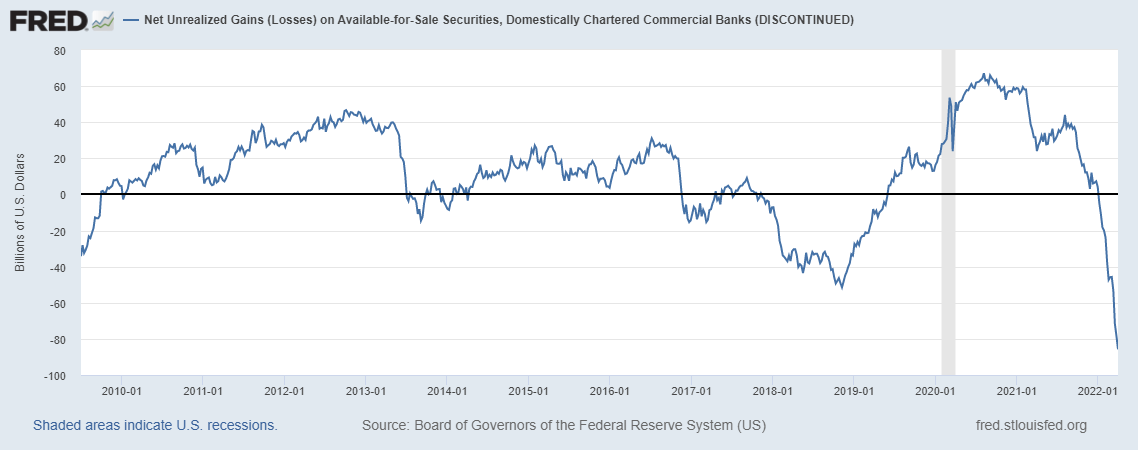

So where do they stand now? Take the asset side first. Banks' balance sheets are loaded with huge unrealized losses, based on declining market values in their portfolios (mortgages, consumer loans, bonds), caused by rising interest rates. The graph below shows the kind of headwind faced by commercial banks since the Fed begun hiking: you see the losses on what are mostly Government bonds, as they were already a year ago (end of March 2022).

{kind=link}

Furthermore, over the past year U.S. bank securities may have lost 10% of their value . But it is only when we add all the Mortgage Backed Securities, Loans, and other assets , (although there are no recent precise data available on losses) that we see the systemic problem. It is pretty straightforward to estimate that: "the total unrealized losses on total bank credit as of December 2022 is... $1.7 trillion. This is only slightly less than total bank equity capital of $2.1 trillion in 2022". (Paper here , page 6).

So what we have here is a castle of cards. But this is no surprise. The financial system is by construction a sophisticated castle of cards: that stands until confidence supports it. That's why the Federal Reserve was created: an almighty lender of last resort to preserve confidence and stability. Almighty? Hmm... Almost, not quite! But I digress.

In my opinion, the banks need to contain their losses on the asset side by year-end. To do so, they need a big fall in long term yields - or, if you prefer, a price recovery of long-term US$ securities and assets. If it happens, banks will be able to sell their assets again when in need, without incurring in huge losses that would eat away their capital ratios. It would then be easier for them to address any "liquidity" issue that may arise in (likely) recessionary times.

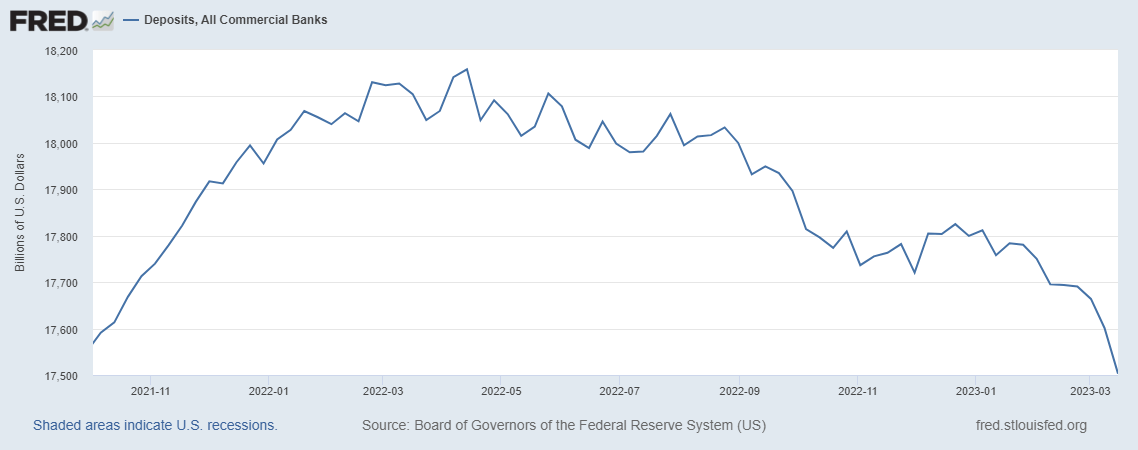

Take the liability side now. Here, it's the short-term rates that are creating havoc. And that's because short term instruments such as T-Bills and Money Market funds compete with, and erode, financial institutions' deposit base. The graph below shows the deposits situation on march 15, when the SVB panic was barely starting to have an impact. Yes, large banks may benefit from outflows from regional banks, but the banking system as a whole is losing deposits.

Commercial Bank deposits (FRED)

{kind=link}

New expensive Fed lending facilities may bolster commercial banks stability in the short run; but the liquidity outflow has become a structural problem that the Fed lending cannot solve. High short-term rates also make more problematic borrowing for long from the interbank market. To face this mounting competition for liquidity, banks could raise deposit rates - many of them are already doing it - : but given the low returns they earn on their long-term assets, rising deposit rates would deteriorate their balance sheets and capital ratios.

So how can monetary policy help financial institutions?

On the asset side, the Fed is clearly trying to engineer a bond market rally, either now or (at the latest) in Q4. On the liability side, they aim at lowering interest rates in a prolonged and sustainable way (in 2024). And here's the thing. Lowering interest rates prematurely, allowing (expected) inflation to persist, would be a disaster not just on the inflation front, but also for the stability of financial institutions. On the asset side, long-term bonds could crash, widening the banks' losses. On the liability side, the fall of short-term rates would be limited and brief, extending the pressure on deposits.

The most destabilizing scenario of all would be stagflation. It could happen if inflation expectations are allowed to remain high while a recession develops. It would add credit risk issues to interest rate risk issues. It could provoke a true systemic crisis of confidence. A great financial crash would ultimately hit the real economy: wall street and main street would go down in tandem. That's why the Fed is ready to take all possible short-term risks in order to manage inflation expectations in the short run, and avoid stagflation in the long run.

True, a deep and prolonged recession (hard landing) would destabilize the financial system: mounting bad loans would add a lot of pressure on the banks bottom line. But the banking system today is well capitalized, and - this is Powell's gamble - can resist some short term headwinds for a few months, if confidence is not lost along the way. What the Fed really wants is a quick and brief recession: they might very well raise rates further this year, and keep them high until year-end.

How are the banks to survive this year? The March 22 Fed hike was a de facto invitation for banks to raise the deposit rate (the loan rate where possible). Under an implicit promise: "this will not last long"; and "while it lasts, we will protect you". At the same time, the Fed is supporting the long end of the yield curve (most sensitive to the promise of a quick disinflation). They will offset the (stimulative) wealth effects of rising Treasuries with higher policy rates: if they stick to their plan, I expect the yield curve to remain inverted this year. One final, medium-term implication is that the Fed plans to pivot quickly and very decisively as soon as inflationary pressures abate (they believe, early in 2024).

Confidence in the Fed strategy will likely support somewhat the US long-dated quality bonds, bank stability, and equity markets in the months to come. On the other hand, the incipient recession and the Fed's hawkish stance will regularly scare equity investors. The result is likely to be a soaring bond market by this summer (I would buy ZROZ at $85-90), falling commodity prices, widening spreads (I would not buy PDO and PTY right now: I will wait to see them below $11-11.5), a falling dollar in 2023:H2 ( DXY ) from current levels, and more volatility in a (mildly) declining equity market (I expect SPX to test again the October lows). This fragile equilibrium may to hold, until the Fed difficult balancing act will prove to succeed or fail.

For further details see:

What The Fed Really Wants