FOVL - What The Market Needs: More CPI Reports

Summary

- November CPI further confirmed a peak in the CPI time series.

- The stock market initially celebrated the good news but got stymied by the reality of minimal changes in the outlook for monetary policy.

- Future CPI reports providing ongoing reassurance of a downtrend should create a sustained mood change, but the Fed still may not cooperate soon enough for the market's tastes.

Now that U.S. inflation has apparently peaked , odds favor month-over-month declines in the CPI (consumer price index). The November CPI numbers delivered on the month-over-month declines the market wanted to see and then some. The core CPI delivered its smallest increase since August 2021 and came in 0.1% points below “expectations.” The market’s initial massive response reflects a rebound from the brooding negativity going into this week’s 1-2 punch of CPI and next the Federal Reserve. The S&P 500 ( SPY ) rallied back to the 4100 level and was up as much as 2.7% on the day. With a CPI downtrend underway, the market seems like it could really use more frequent CPI reports.

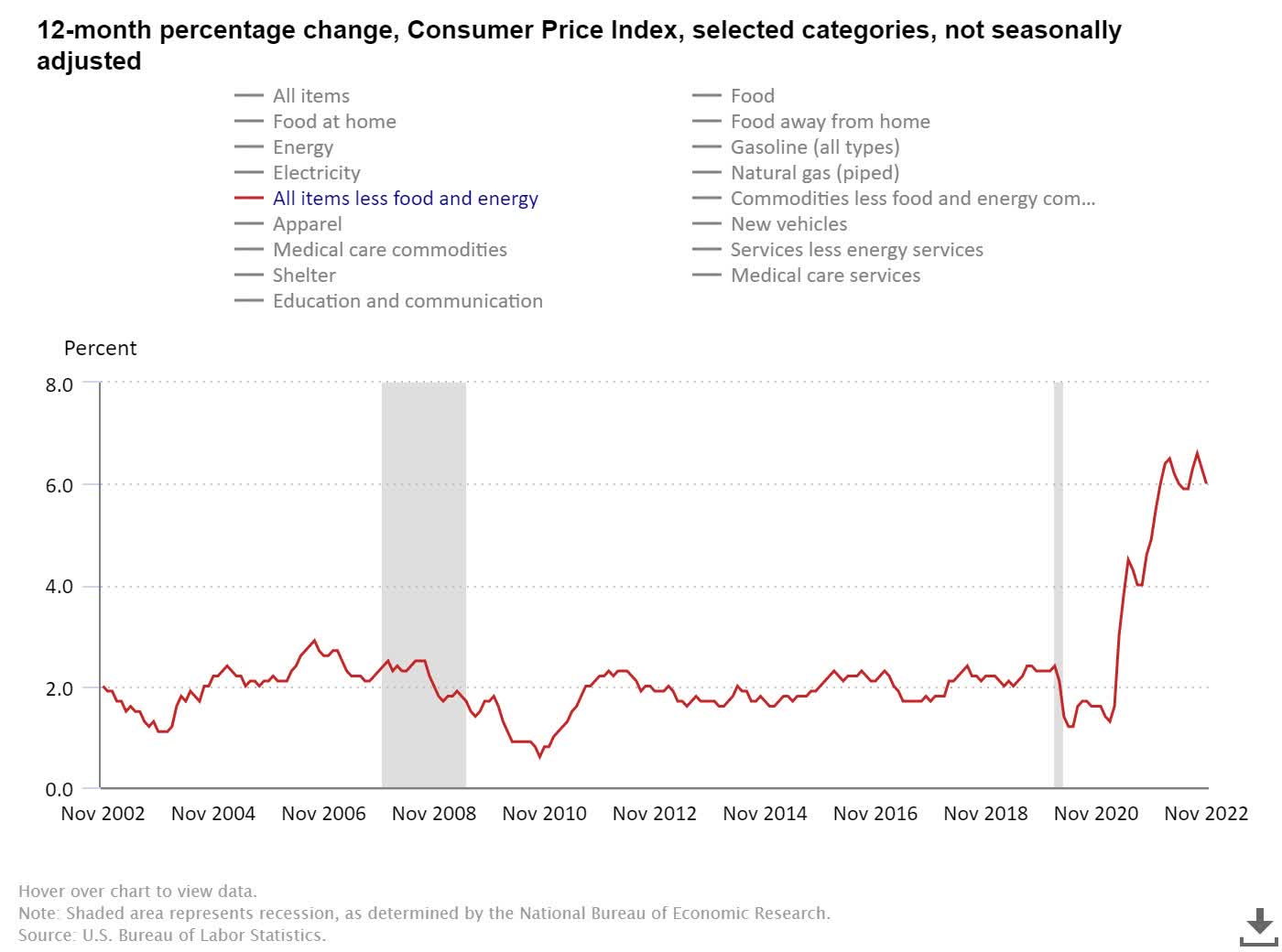

Unfortunately, translating the peak in inflation to a change in the relationship between the Fed and the stock market is not so straightforward. Indeed, at the time of writing, sellers faded the S&P 500 enough to push it back under its 200-day moving average ((DMA)) and almost flat on the day. The Fed has indicated that it wants to see substantial evidence that inflation is going down for the count. The graph of core CPI shows a peak, but it does not show a downtrend underway just yet.

November's CPI data seems to have confirmed a much welcome peak in CPI. (U.S. Bureau of Labor Statistics)

{kind=link}

As has been the case for some time, the cost of shelter is the biggest component offsetting the price declines in other CPI components. These costs have yet to peak even as the housing market entered a recession months ago . While these costs should come down in coming months, the Fed’s risk management framework requires it to keep pressing until the evidence shows up in the final data. Moreover, it's not yet clear how far prices can or will come down with a strong labor market and persistently tight housing inventories (on the existing homes side). Furthermore, the Fed suffers from a dilemma: The minute it declares victory, or even suggests victory is imminent, the market also will celebrate in ways that can rekindle inflationary pressures well before inflation gets even close to the 2.0% target.

Shelter costs are driving the entire on-going uptrend in services less energy CPI. (U.S. Bureau of Labor Statistics)

{kind=link}

So, from the Fed’s perspective, the job is hardly done. Accordingly, I'm not surprised to see the fed fund futures respond to the good CPI news with just some trimming around the edges. The Fed fund futures decreased peak rate expectations from the 5.00% to 5.25% range to the 4.75% to 5.00% range. The futures now project a March peak instead of a May one, and 2023 ends with the Fed’s interest rate 25 basis points lower than earlier projections.

Fed fund futures now do not deliver a rate cut until November. (CME FedWatch Tool)

These changes seem unremarkable, especially considering the projected timing for the first rate cut. The market’s most anticipated moment for 2023 is now pushed out from July to November 2023. Suddenly, the stock market faces the prospect of an extended period of time of the Fed jawboning against inflation and leaving the stock market to fend for itself. I find it hard to imagine the Fed becoming the market’s friend again until it telegraphs the end of the tightening cycle.

The Trouble with Inflation Expectations

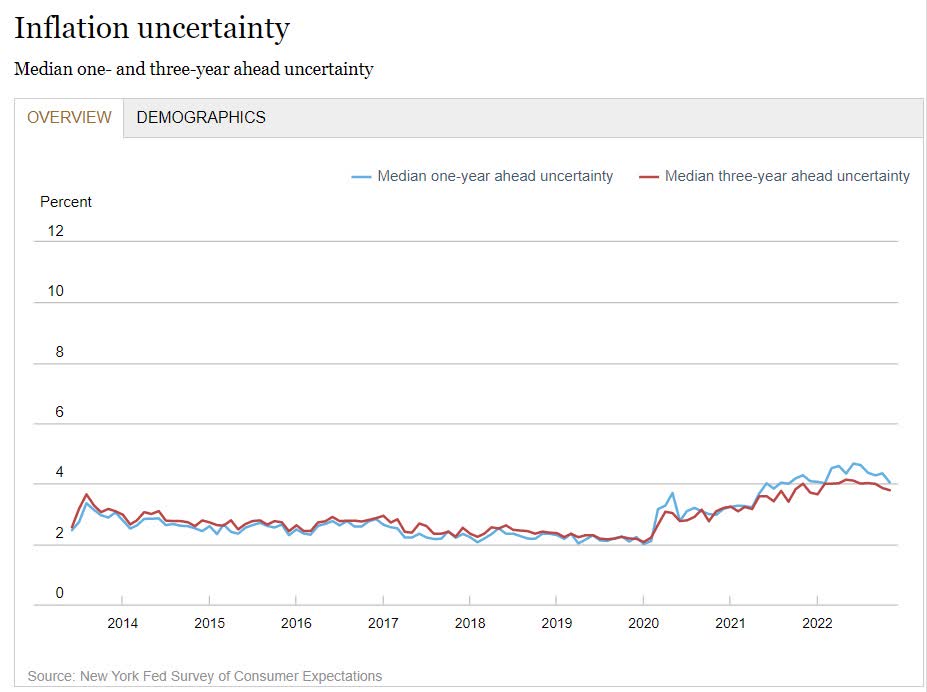

When inflation expectations were soaring last year, the stock market seemed to care little. Now, declines in inflation expectations can move the market. Yesterday’s update from the NY Fed on inflation expectations gave a timely prelude to today’s CPI print. The stock market even jumped on the news. According to the report on the November 2022 Survey of Consumer Expectations , “median inflation expectations decreased at both the one- and three-year-ahead horizons in November, by 0.7 percentage point (to 5.2%) and by 0.1 percentage point, to 3.0%, respectively. Both decreases were broad-based across education and income groups.”

Inflation expectations have peaked and are trending down after a year of soaring. (NY Fed Survey of Consumer Expectations)

{kind=link}

However, the “trouble” with this same report comes from expectations about the labor market. While the survey showed a decline in wage expectations, all other measures showed slight increases in optimism: Unemployment, the odds of losing a job, and the odds of finding a job. Moreover, “the median expected growth in household income increased by 0.2 percentage point to 4.5% in November, a new series high.” This bullishness appeared despite slight declines in other measures of expectations for household finances.

In other words, while inflation expectations have seemingly peaked along with the CPI, the inflationary environment is not showing the clear signs the Fed needs to see in its risk management framework.

The U.S. Dollar

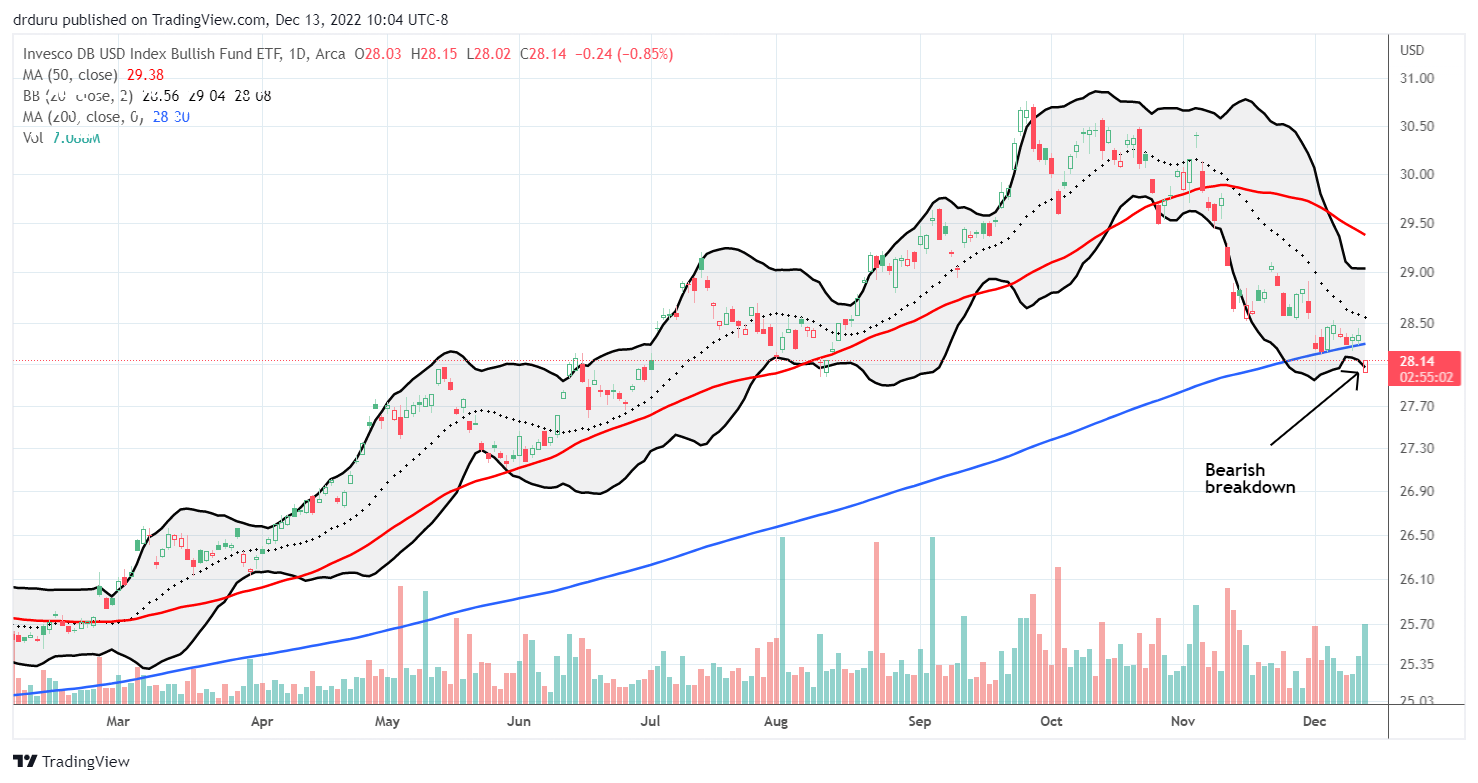

Meanwhile in the currency market, the U.S. dollar continues to point toward a less hawkish future one day. Today’s CPI pushed the Invesco DB US Dollar Index Bullish Fund ( UUP ) below its 200DMA (the blue line below) which is a very dollar-bearish move. The breakdown further confirms the trend in place and should give the stock market reasons to cheer up again at some point.

A bearish 200DMA breakdown confirms an on-going downtrend for the U.S. dollar. (TradingView.com)

{kind=link}

Everything Could Change Tomorrow

Ultimately, the CPI reports are fodder for speculating on monetary policy. The rubber hits the road with the Federal Reserve’s Dec. 14 release on monetary policy. Chair Powell can choose to go with the flow and align with the market’s celebration over CPI, or he can choose to stay the course on jawboning to maintain the pressure on inflation expectations. In the first scenario, a “Santa Rally” gets a solid launch pad. In the second scenario, the market might as well pack up the gifts, take shelter for the rest of the year, and wait for the next CPI report.

For further details see:

What The Market Needs: More CPI Reports