PLDGP - What To Do After STORE Capital Buyout?

Summary

- The buyout for STOR has received some criticism from investors feeling the price is too low.

- Shares aren’t getting the premium we’ve seen in some buyouts, but the valuation is still better than where some peers are trading.

- Comparing STOR to peers across the last 5 years, we can see that this relative value for STOR is respectable. Not great, but it isn't a mess either.

- If most REITs were trading at relatively high prices, this deal would stink. However, investors can reinvest while many REITs are cheap. The timing makes the deal.

- Looking at pricing today, I see many great choices for shareholders in STOR to redeploy their capital. I'll share 12 of them.

STORE Capital ( STOR ) announced a buyout at $32.25 per share. That's a 20% premium to the prior share price, but for many investors it still feels too low. However, the transaction is within the range that I would consider fair. It's not the upper end of that range, but it's not an awful deal given the current market environment. Why is the market so relevant? Because the market determines what opportunities investors have for reinvesting.

Note: The first 3 charts here only run through the closing price before the buyout was announced. Consequently, I've added some commentary to clarify the relative valuations.

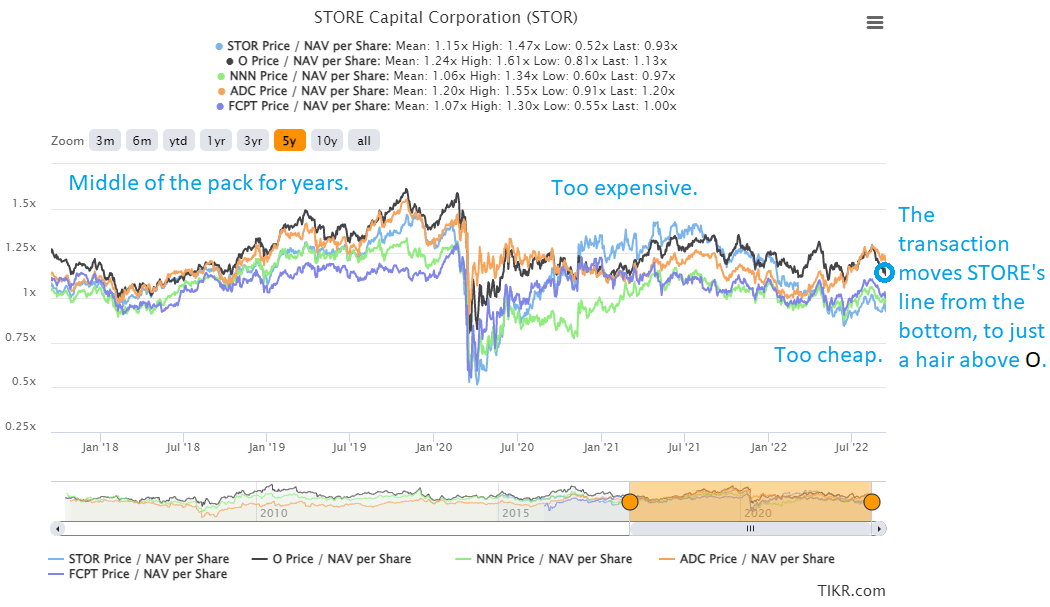

Historical Valuation using NAV

For comparison, I'm adding four peers:

- Realty Income ( O )

- National Retail Properties ( NNN )

- Agree Realty ( ADC )

- Four Corners Property Trust ( FCPT )

We could use more, but I think this is a fair batch.

If we use price-to-consensus-NAV to evaluate the REITs, we can see an interesting story:

{kind=link}

Here's a timeline for my view:

- Shares were trading around the middle of the pack.

- I felt they were too expensive before the pandemic.

- They got hammered during the pandemic and dropped to the bottom. Great deal.

- Then they recovered hard and ended up at the top. Too expensive.

- Shares fell too far again, making them the net lease REIT furthest into our target range.

- Buyout announced, bringing STOR roughly in line with historical averages while many peers are below their historical average.

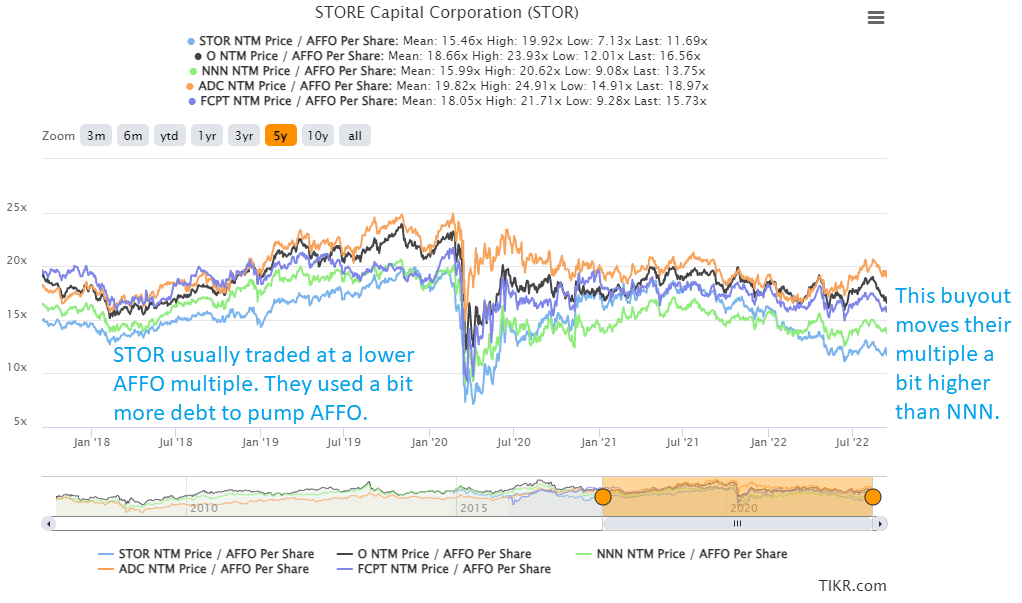

Historical Valuation using AFFO multiples

STOR was regularly the cheapest on AFFO, which made sense since they often had slightly more leverage:

{kind=link}

Using this comparison, the buyout valuation seems to be about fair value, though it certainly doesn't have the premium we often see awarded in buyouts.

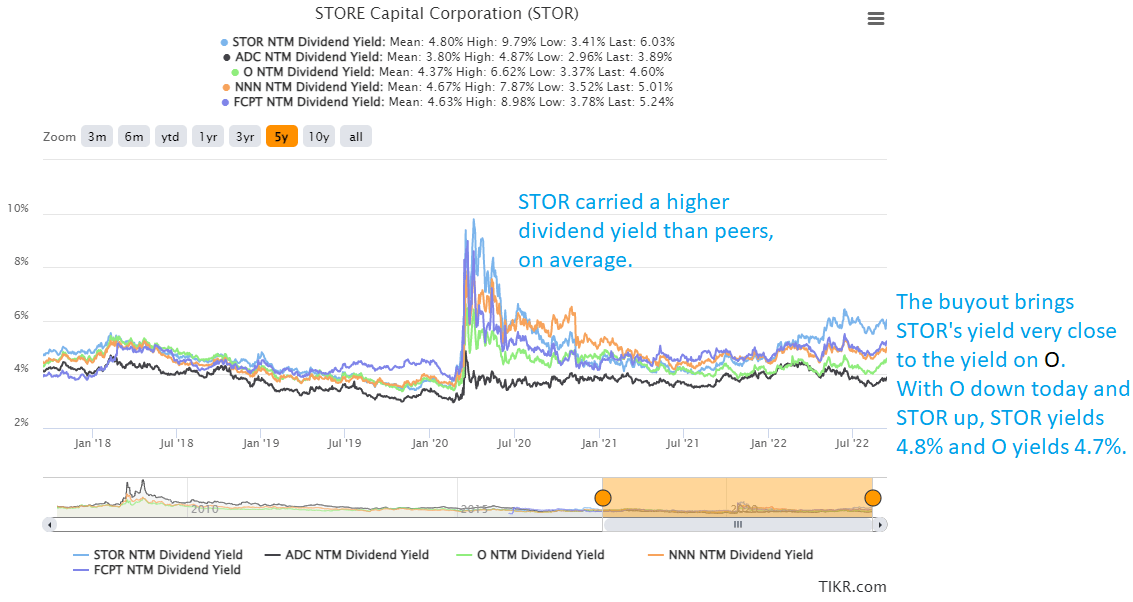

Historical Valuation Using Dividend Yield

I generally won't use this as a comparison since it can be swung by the board of directors declaring a more aggressive dividend at any point. However, it can be a helpful point of view for investors focused on the income from their position. Investors can generate a very similar amount of income by switching to Realty Income today:

{kind=link}

While O is not the equity REIT furthest in our target range, it is legitimately trading at a discount to our target values. Among the net lease REITs, it is roughly tied for first place on having the largest discount to our targets (91.8% price-to-buy for O at $63.53).

What Is Management Thinking?

We've seen two outstanding executives leave in the last few years. I felt the executives were part of the competitive advantage for STOR. If the board of directors feels the same way, then getting this valuation relative to peers is pretty good. For comparison, at $32.09 (STOR's current price, slightly below the buyout) STOR is trading about 3.3% above our "price-to-buy". That's generally pretty low for a buyout to occur, but it's a material gap when O trades at 91.8%.

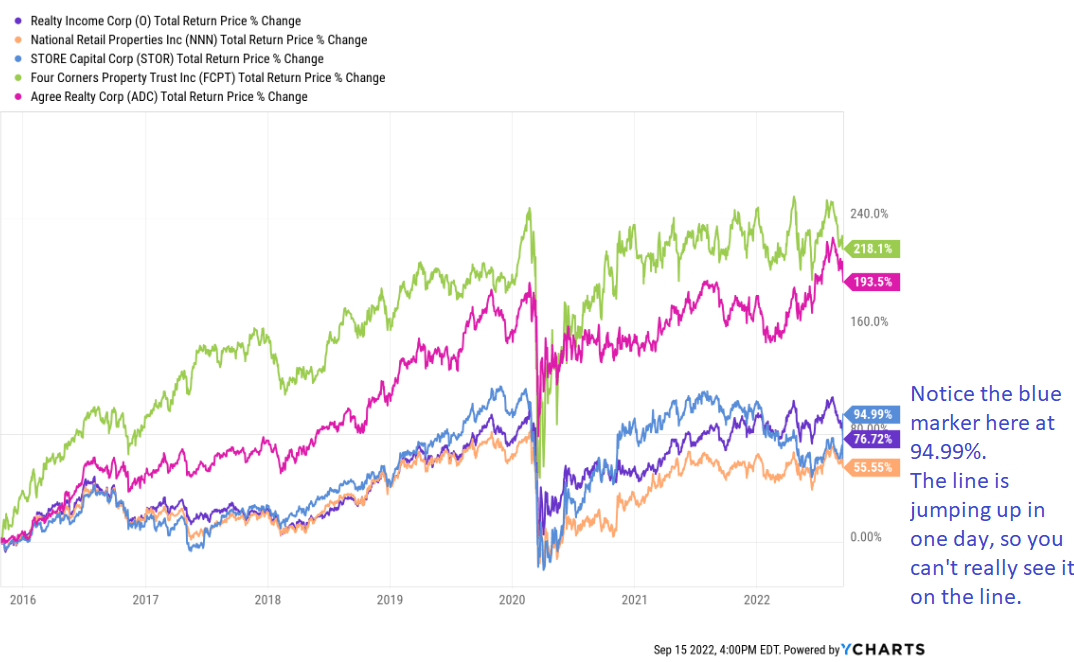

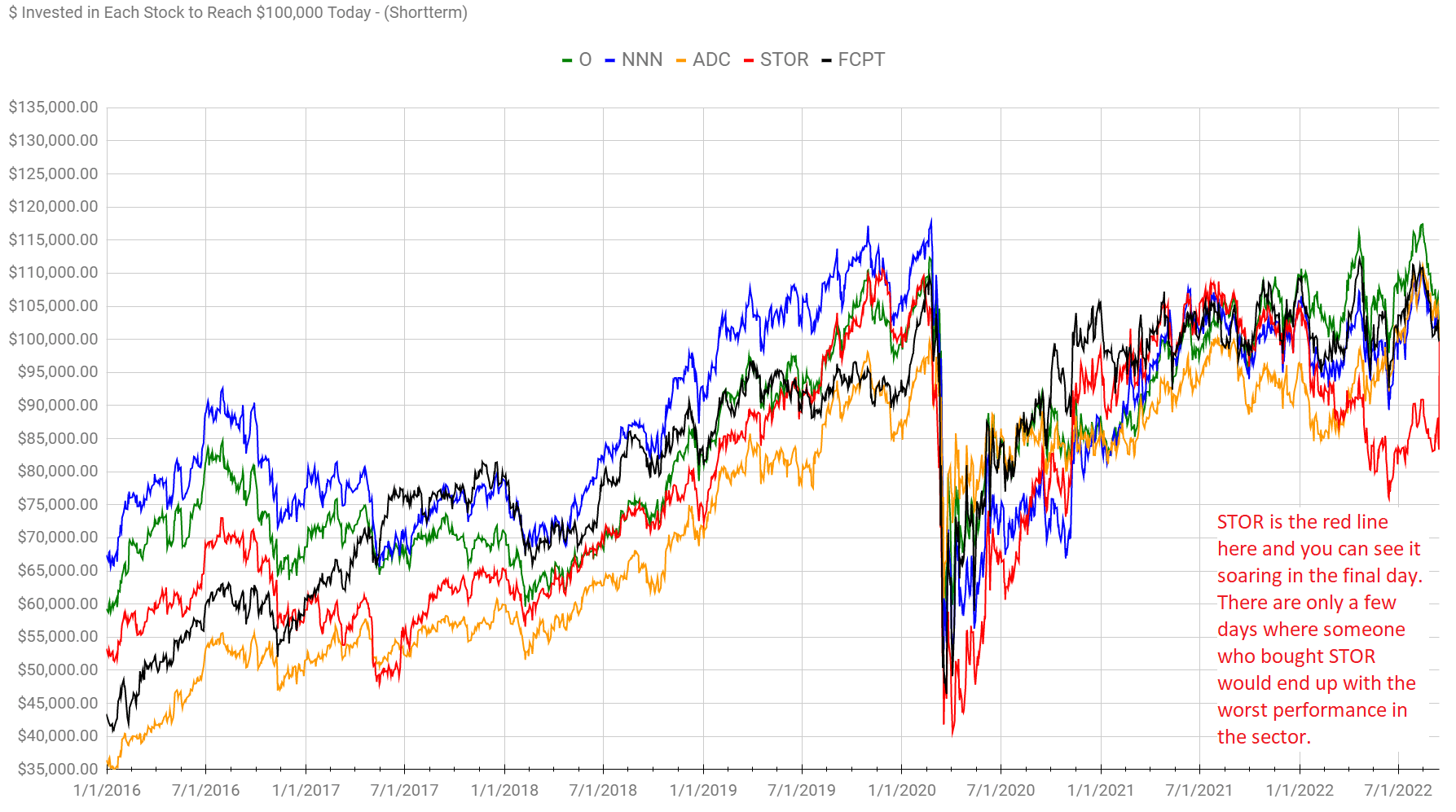

Returns Since IPO

Performance for STOR since their IPO has been great. They didn't keep up with ADC and FCPT, but they did come out ahead of O and NNN:

{kind=link}

That's strong enough that I think most investors can be happy, though a few that opened positions in late 2019 or very early 2020 may feel far less impressed. Using the $100k chart, we can verify that any buy-and-hold investors in STOR aren't getting the worst performance for the sector unless they bought on a very unfortunate day. Using the $100k chart below, we can see that investors in STOR performed pretty well based on most starting points:

{kind=link}

Conclusion

I think this is an acceptable deal. It could be a pain for those with a large taxable capital gain. However, putting that aside, this feels like an okay deal. It's not a home run by any means, but STOR achieved better pricing than average for the sector today. This deal wouldn't have been a good deal when peers were hitting 52-week highs. However, today there are vastly more alternatives for reinvesting than there were before.

Since there are so many great alternatives, I think the board is making a reasonable decision to simply give the shareholders cash. That has to come into play. If the buyer for STOR was bidding $40.00 today, they would be severely overpaying compared to peers. This always comes back to relative values. The deal gives STOR shareholders a valuation high enough to make sense when so many REITs are on sale.

There's a chance the board can get an even higher offer. They have 30 days to look for alternative offers. They might get a higher offer, but I think competitors would be unwise to come in much higher. It's a possibility, it just isn't a strong one. I would favor some of the other equity REITs that are residing in our "Strong Buy" range already. That includes Essex Property Trust ( ESS ), Sun Communities ( SUI ), Equinix ( EQIX ), Digital Realty ( DLR ), Crown Castle ( CCI ), and Terreno ( TRNO ).

Looking at relative price performance over the last year, I think weakness for Camden Property Trust ( CPT ) and Realty Income should also put them on the radar as solid targets. I would also add Prologis ( PLD ), Rexford ( REXR ), STAG Industrial ( STAG ), and EastGroup Properties ( EGP ) to the list. STAG and EGP are not currently under coverage (so no precise targets, but I've dug far enough to say they are undervalued). The other 10 REITs mentioned are under coverage in our service. That gives investors several alternatives for how to put their capital to work.

Except for O, these REITs all have materially lower dividends yields. Investors looking to include some higher yield could check out the preferred shares we frequently write about. Mixing them with these equity REITs creates an attractive combination of yield (from the preferred shares) and dividend growth (from the common shares).

- Ratings: Neutral outlook on STOR

- Bullish outlook on ESS, SUI, EQIX, DLR, CCI, TRNO, CPT, O, PLD, REXR, STAG, EGP

For further details see:

What To Do After STORE Capital Buyout?