TAK - What To Expect From Bristol-Myers Squibb In 2023

Summary

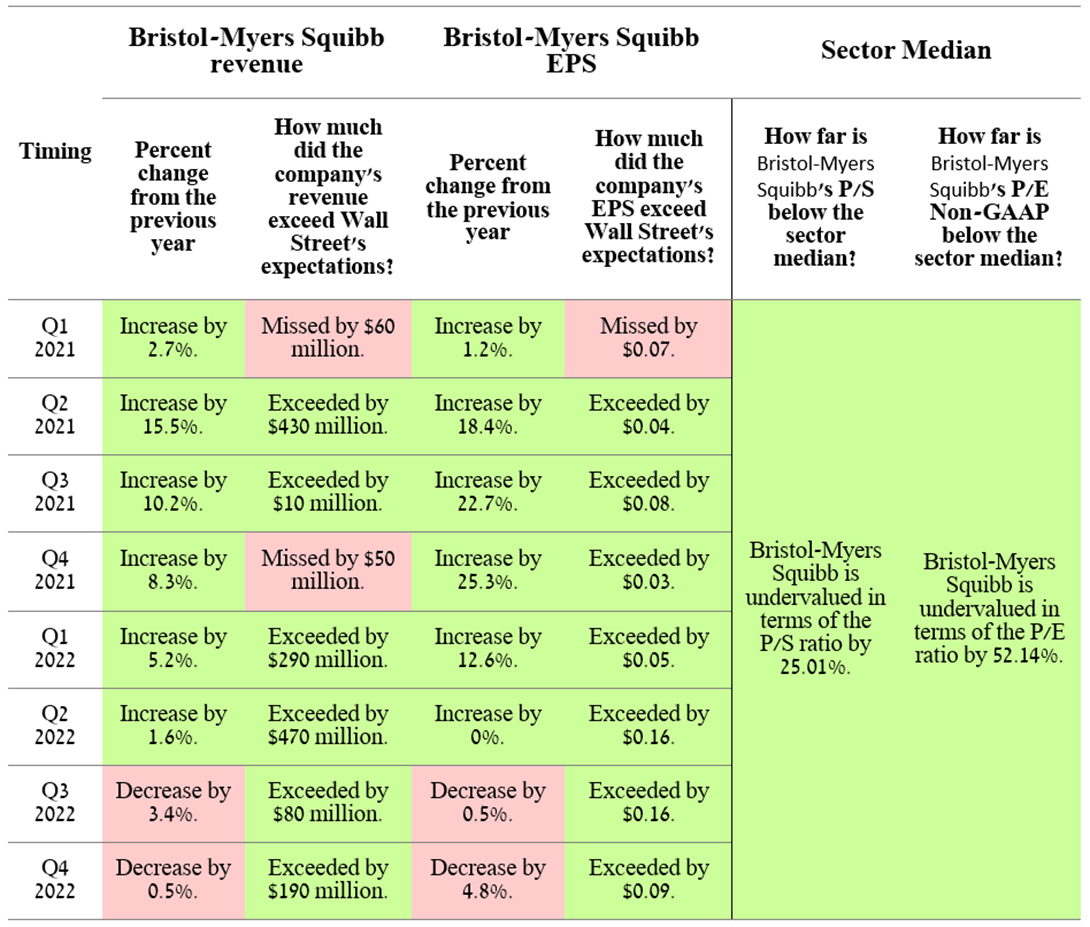

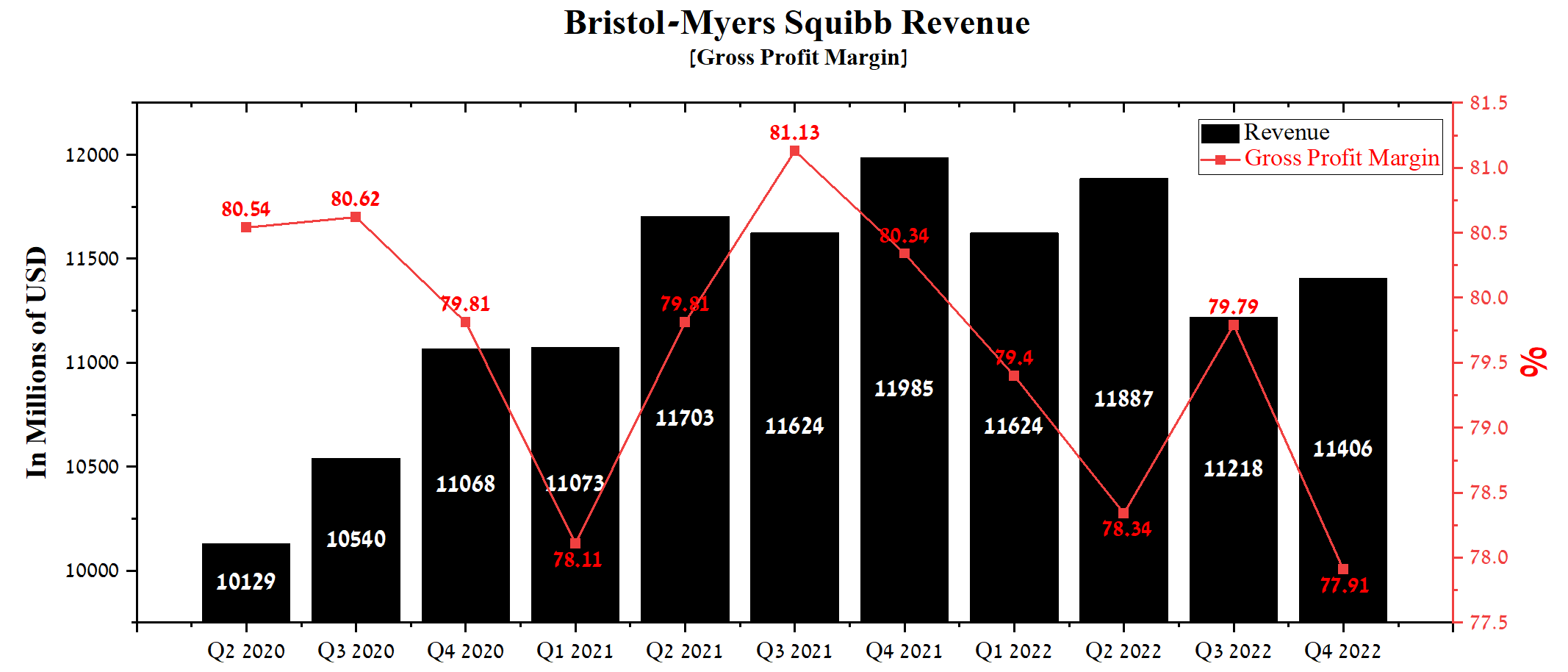

- Bristol-Myers Squibb's revenue was $11,406 million in Q4 2022, showing mixed results compared to previous quarters, and there are many explanations for this, which will be discussed in the article.

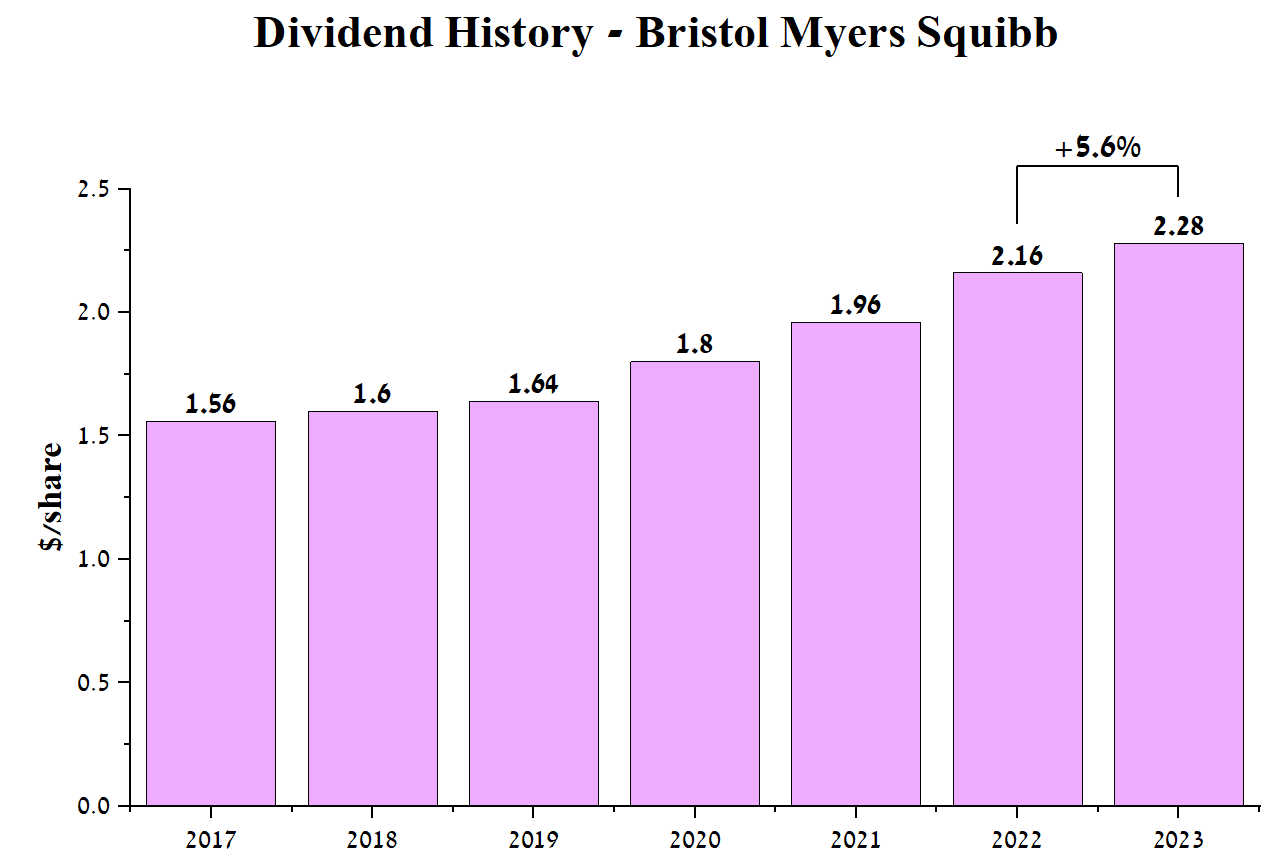

- In 2023, the company's investors should receive a dividend of $2.28 per share, up 5.6% from a year earlier.

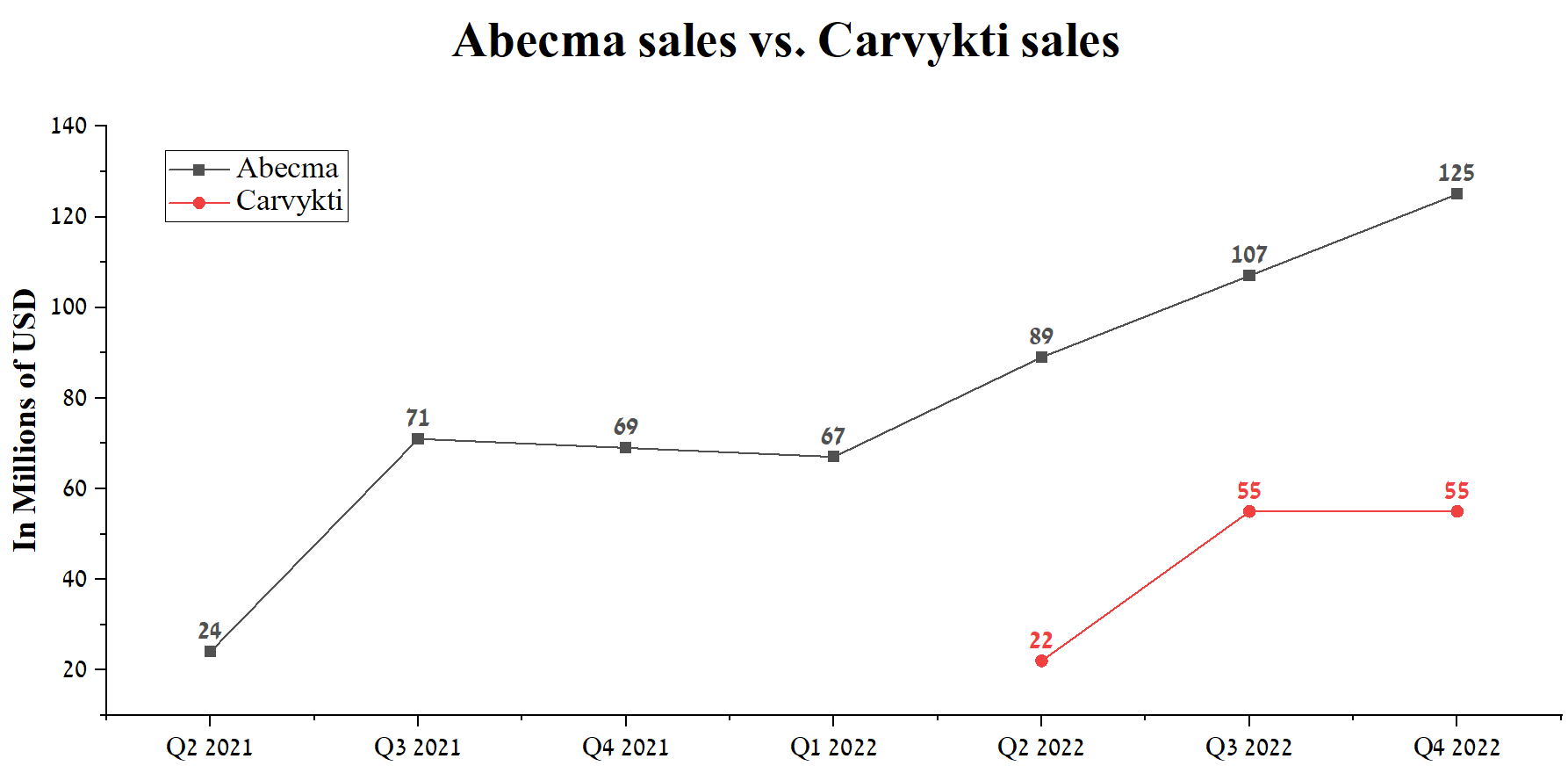

- Abecma's revenue was $388 million in 2022, up 136.6% compared to 2021, while Carvykti's sales in Q3 and Q4 2022 remained the same.

- Bristol-Myers Squibb's current dividend yield of 3.21% is well above the healthcare sector average and in line with many companies in other sectors, such as Exxon Mobil and Chevron Corporation.

- Breyanzi, Abecma, Sotyktu, and Opdualag are showing impressive sales growth rates and will be key contributors to the company's total revenue growth over the next five years.

Bristol-Myers Squibb ( BMY ), a pharmaceutical company with a long history, has managed to withstand numerous economic and geopolitical challenges and prioritized developing and commercializing innovative products in areas including oncology, hematology, and cardiovascular disease.

Sales of most of Bristol-Myers Squibb's blockbusters show significant growth not only on an annualized basis but, more importantly, quarterly, thus delivering the company's management's ability to turn the competitive advantages of medicines into profit. Due to increased competition with generic versions of Revlimid and Abraxane, Bristol-Myers Squibb continues to resort to a share buyback policy, which not only contributes to exceeding Wall Street analysts' forecasts but also indicates the correctness of the chosen business development vector, as it helps to reduce speculative interest in companies. With high business margins, reduced debt, and multiple drug approvals in 2022, Bristol-Myers Squibb could be an excellent choice for long-term investors.

Author's elaboration, based on Investing.com

{kind=link}

Bristol-Myers Squibb's financial position and business prospects in the coming years

Bristol-Myers Squibb's revenue was $11,406 million in Q4 2022, showing mixed results compared to previous quarters, and there are many explanations for this, which will be discussed later in this article.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

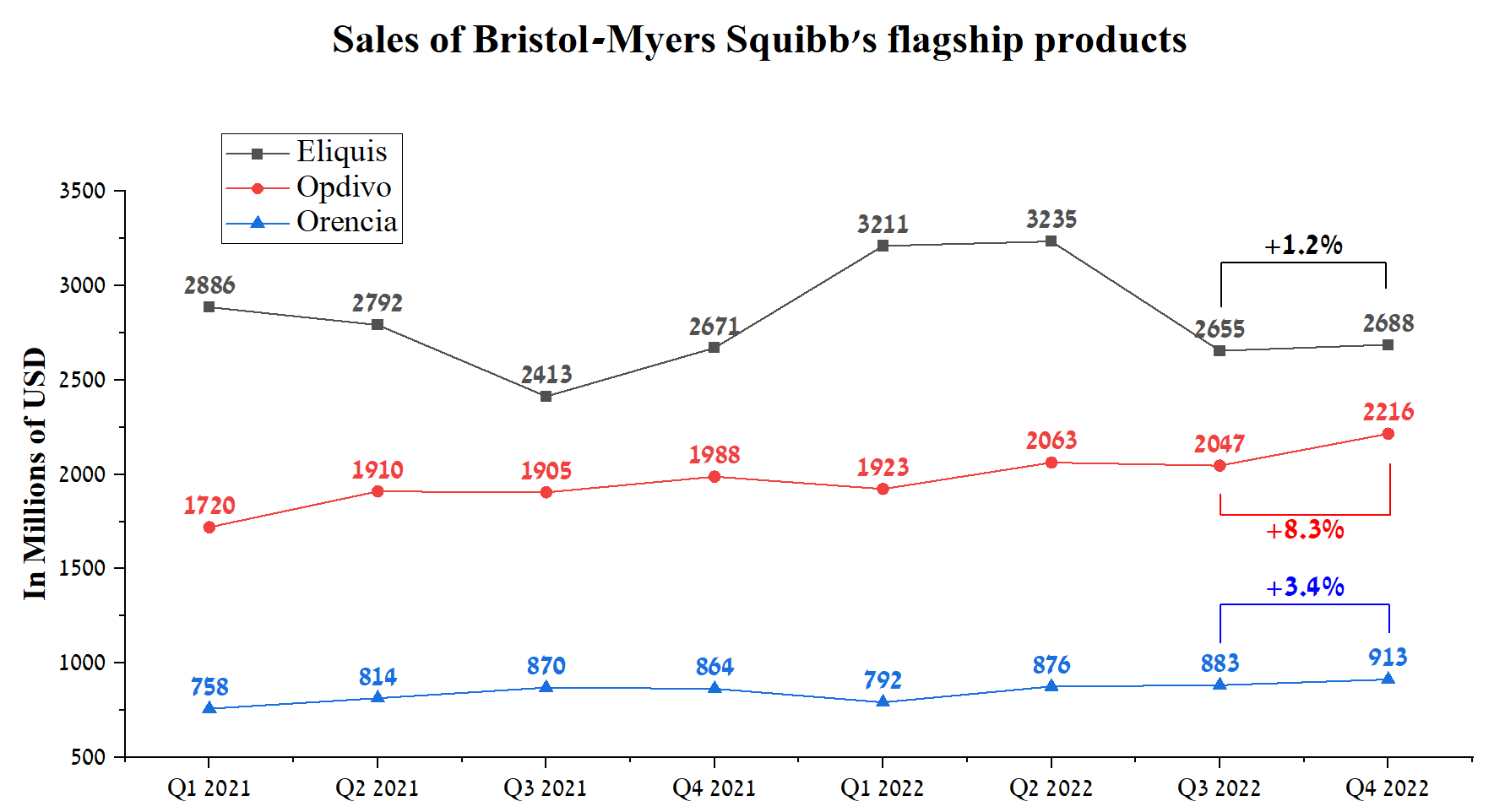

The company's QoQ revenue growth was driven primarily by three flagship branded medicines, Eliquis, Opdivo, and Orencia, whose combined sales were $5,817 million in Q4 2022, an increase of $232 million.

Author's elaboration, based on quarterly securities reports

{kind=link}

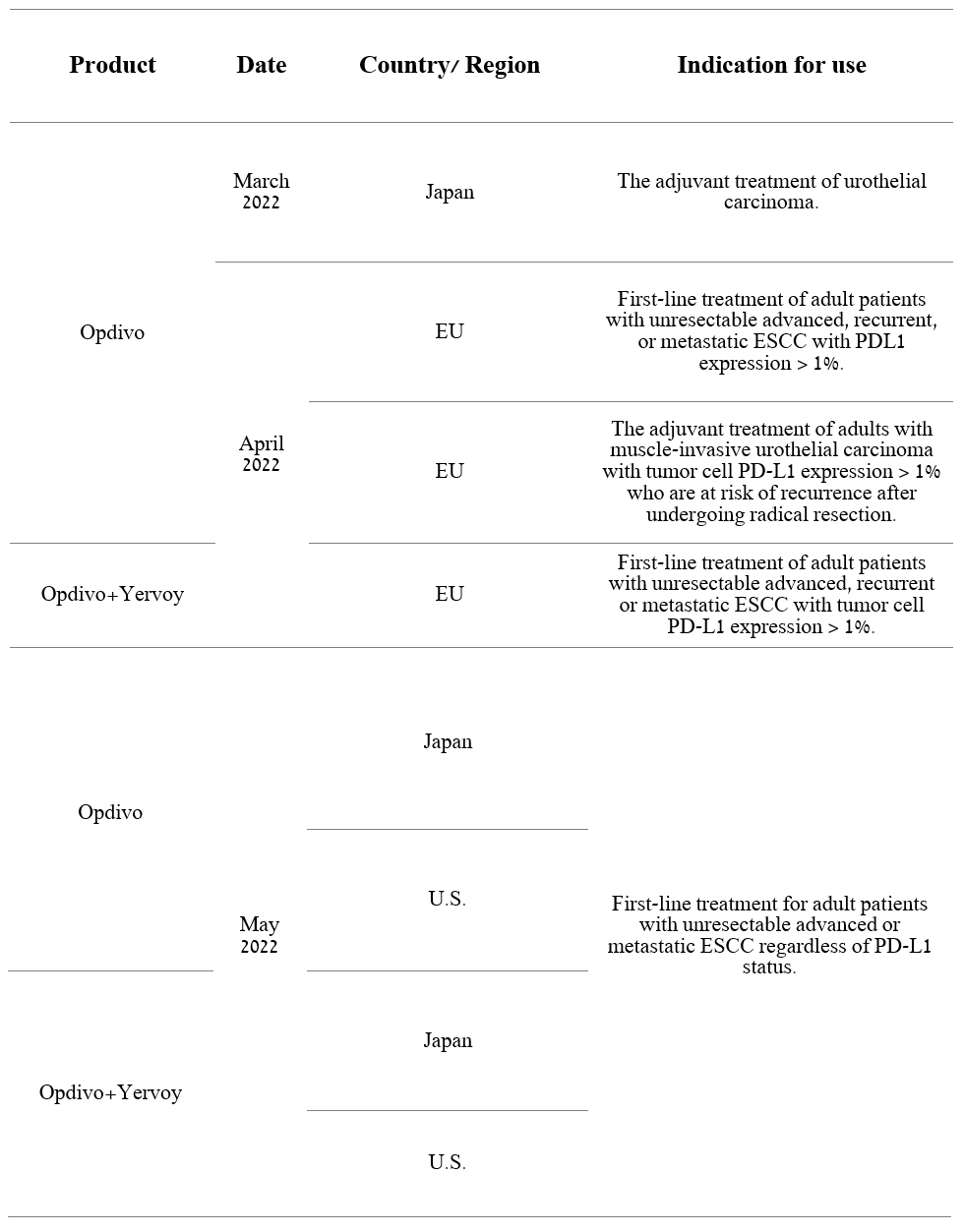

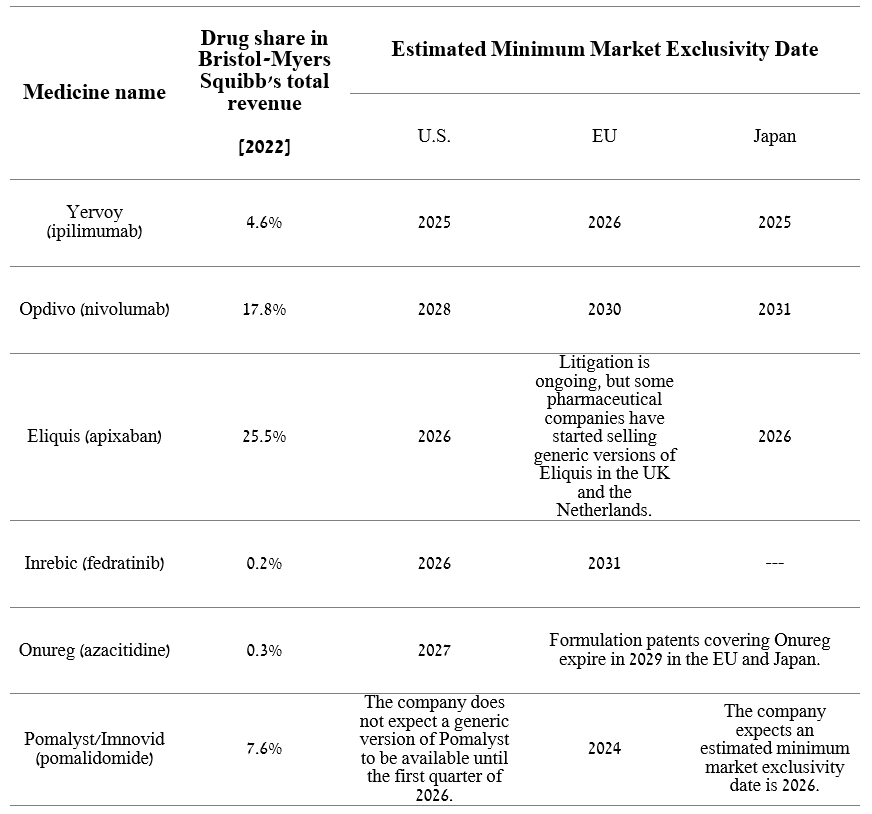

The growth in sales of these medicines was mainly due to higher demand and selling prices in the United States. The key competitor to Merck's world-famous Keytruda (NYSE: MRK ), Opdivo is finally posting more substantial quarterly sales growth thanks to increased indications and also improved demand from clinicians for its use in combination with Yervoy to combat NSCLC and also in combination with Cabomethix for the treatment of patients with stomach and esophageal cancer and other types of cancer. In 2022, of the Bristol-Myers Squibb drugs discussed above, Opdivo received nine regulatory approvals, while Yervoy, whose patents expire in 2025-2026, received three approvals.

Source: Author's elaboration, based on 10-K

{kind=link}

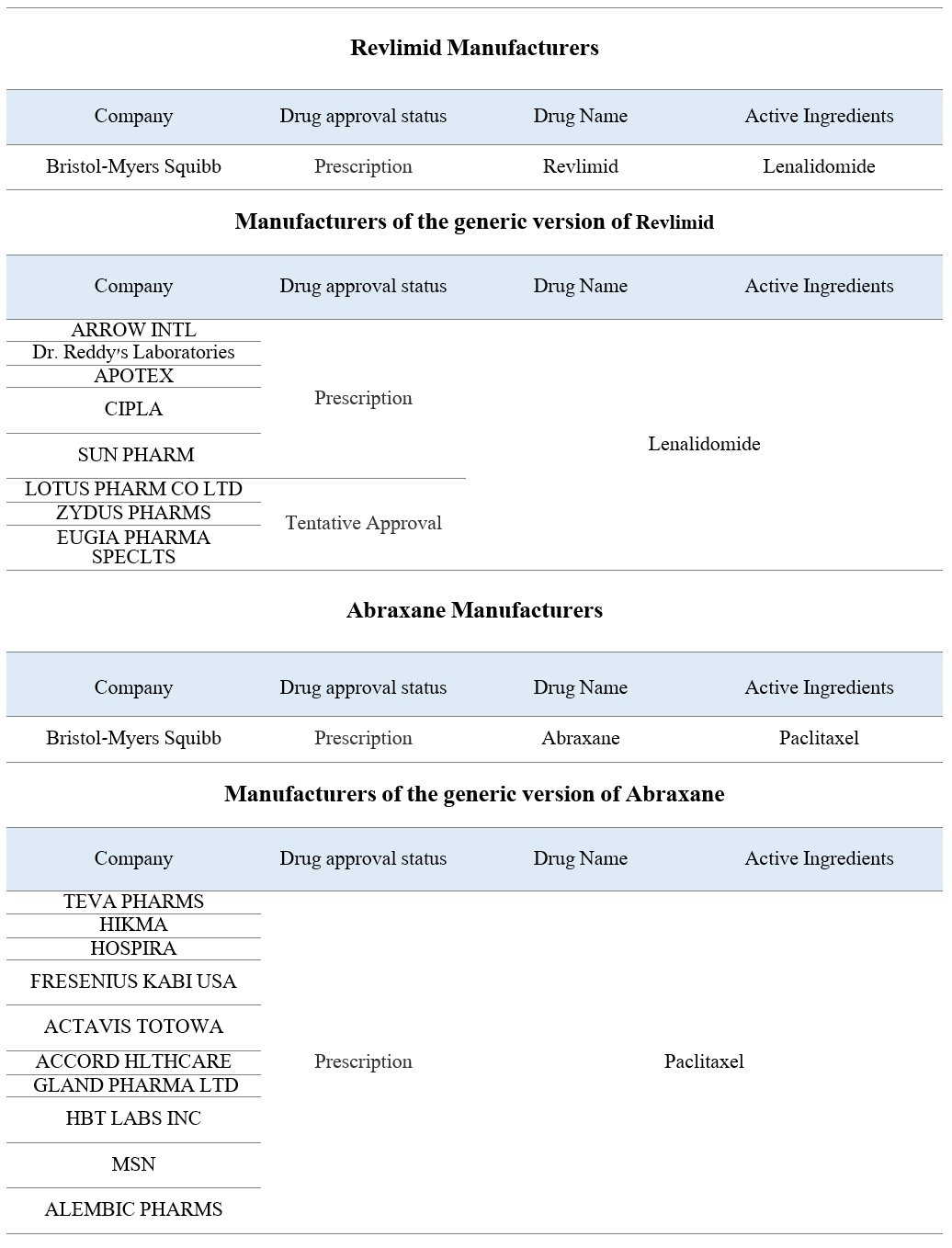

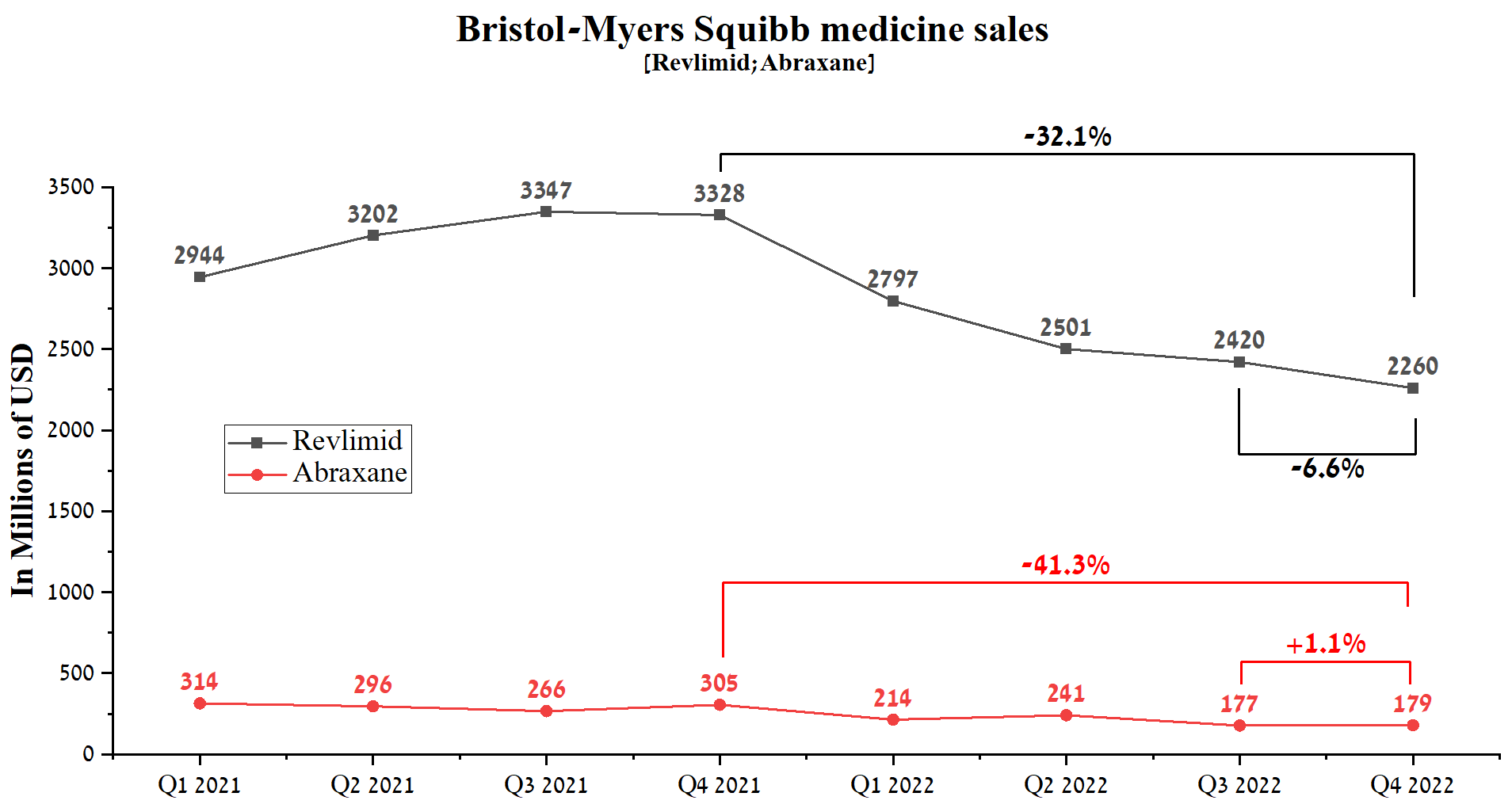

At that time, the main reasons for the decline in revenue and gross margin of Bristol-Myers Squibb year-on-year are increased competition from Teva Pharmaceutical (NYSE: TEVA ), Viatris ( VTRS ), and Dr. Reddy's Laboratories ( RDY ), and other manufacturers of generic versions of Revlimid and Abraxane.

Source: Author's elaboration, based on FDA

{kind=link}

These two blockbusters' combined sales were $2,439 million in Q4 2022, or 21.4% of the company's total revenue.

Author's elaboration, based on quarterly securities reports

{kind=link}

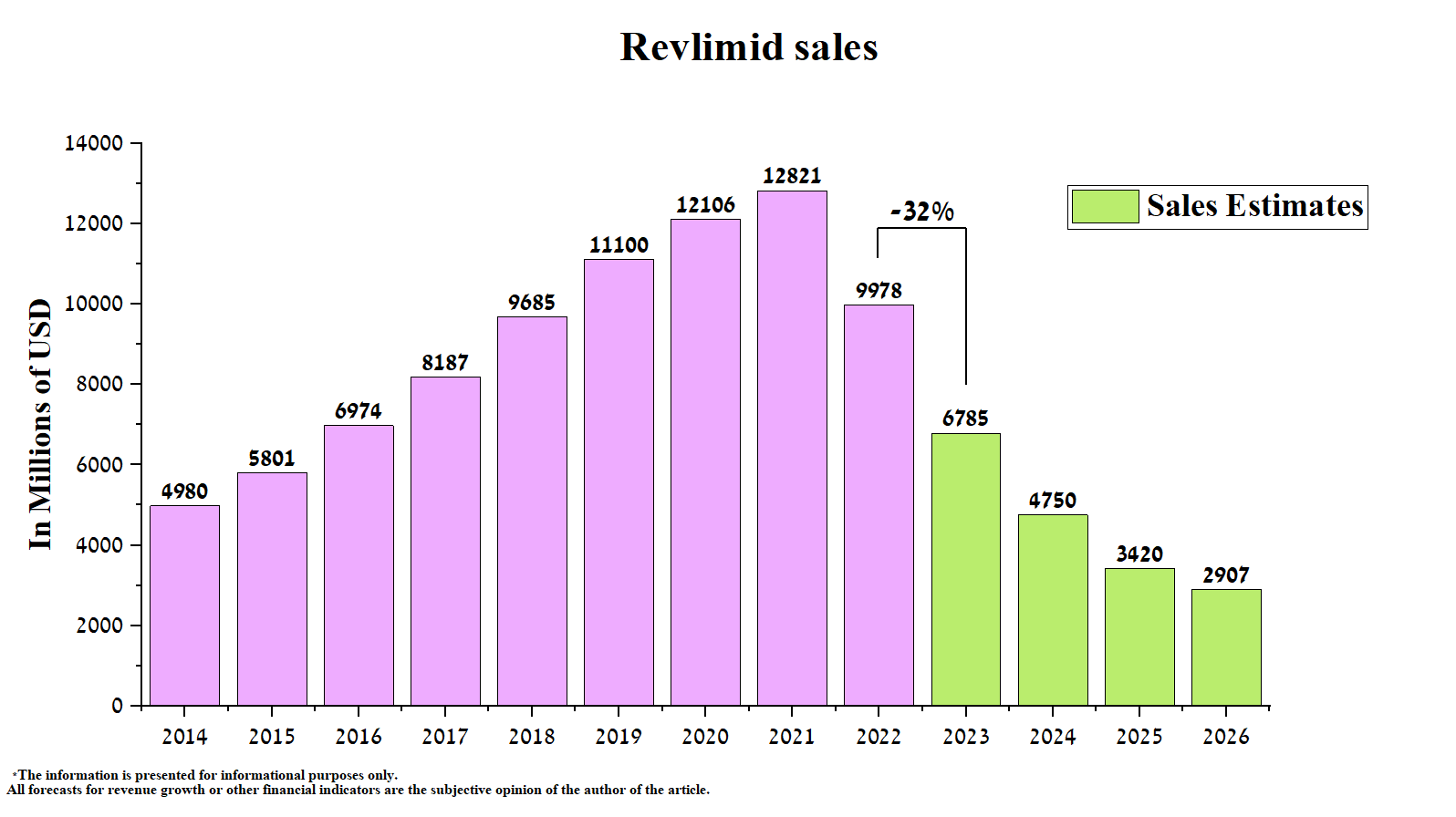

That being said, I expect the rate of decline in Revlimid and Abraxane sales to continue for at least another three years before the demand equilibrium phase between generic and branded versions of these medicines arrives. Overall, the company's management expects Revlimid's revenue to be $6.5 billion in 2023, which is $285 million less than my expectations.

{kind=link}

The situation with Bristol-Myers Squibb's EBITDA

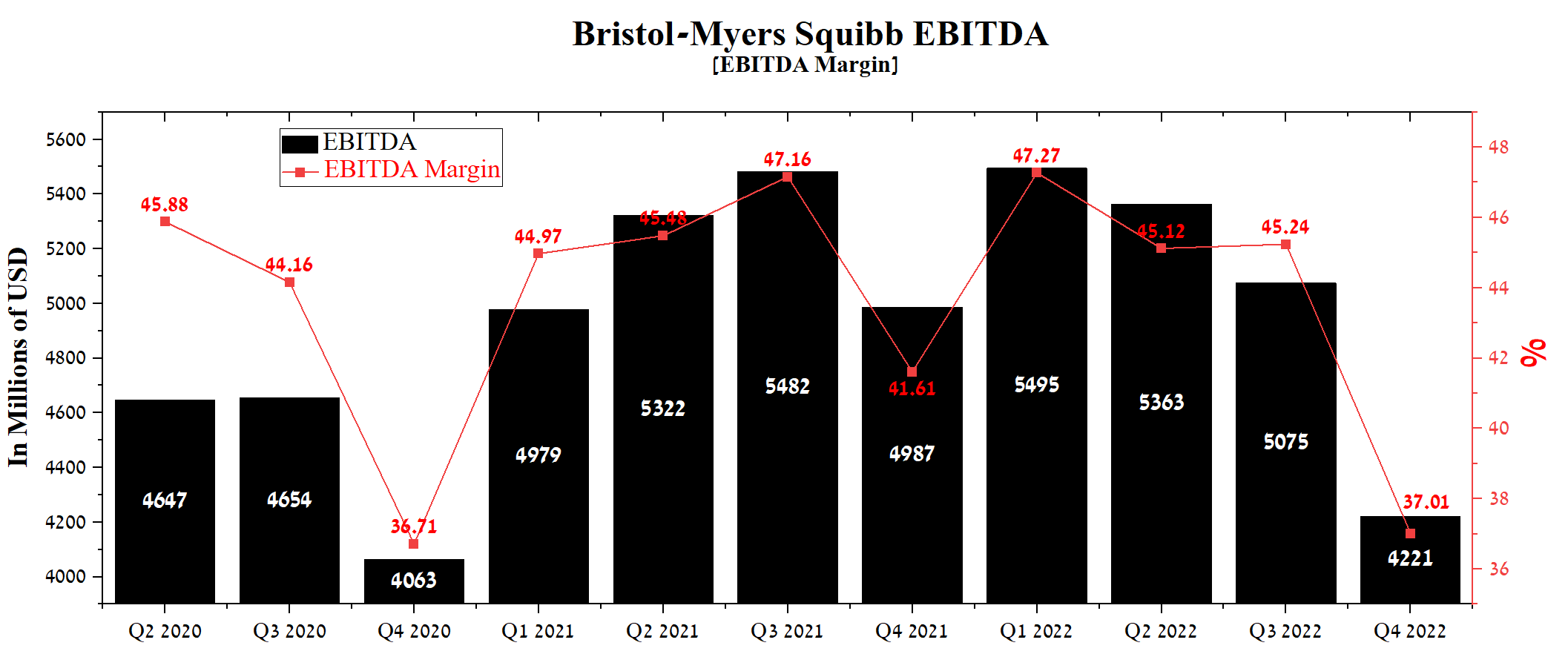

Bristol-Myers Squibb's EBITDA was $4,221 million in Q4 2022, down 15.4% from a year earlier.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

This figure continues to deteriorate quarter by a quarter due to several factors. The first and foremost of these is the expiration of patents and subsequent competition with generic versions of Revlimid and Abraxane, exerting price pressure and reducing prescription volumes for the company's branded medicines. Investors should consider the fact that speculators and market participants considering the company as a long-term investment will take into consideration the dates when the drug exclusivity ends and whether the company will be able to offset the loss of EBITDA for other products. For example, over the next six years, generic versions of the following medicines will appear on the market, collectively generating 56% of BMY's total revenue in 2022.

Author's elaboration, based on quarterly securities reports

{kind=link}

The negative dynamics of EBITDA, although on a smaller scale, were influenced by the depreciation of the euro, the Japanese yen, and other currencies against the US dollar. International sales of Bristol-Myers Squibb medicines were $13,497 million in 2022, accounting for 29.2% of the company's total revenue.

And the last factor that has led to a decrease in the company's margins is the increase in research and development expenses, which are critical for players in the pharmaceutical industry to be competitive and solve unmet medical needs. 2023 will be the year Bristol-Myers Squibb will present to investors, patients, and physicians the results of clinical trials evaluating the efficacy and safety of next-generation product candidates that can dramatically improve the quality of life for many people suffering from life-threatening diseases. For example, on February 10, 2023 , the company announced that Abecma (idecabtagene vicleucel), a first-in-class anti-BCMA CAR T cell therapy developed in partnership with 2seventy bio (NASDAQ: TSVT ), demonstrated a statistically significant improvement in progression-free survival ((PFS)) among patients with relapsed and refractory multiple myeloma in phase 3 clinical trial. According to the American Cancer Society , about 35,730 new cases of multiple myeloma will be diagnosed in the United States in 2023 alone, and as a result, the healthcare system needs more and more modern medicines that can save the lives of these people.

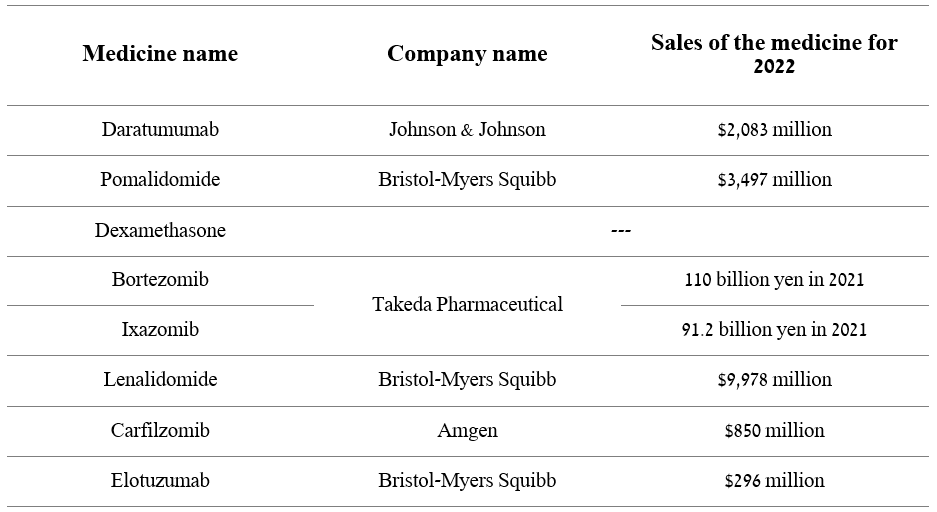

A candidate for this goal could be Abecma. Thus, in the phase 3 KarMMa-3 study, the median PFS in the group of patients using Abecma was 13.3 months relative to the PFS of 4.4 months in the group of patients with standard treatment regimens. The medicines in the group that received standard regimens were Takeda Pharmaceutical's (NYSE: TAK ) Ixazomib, Amgen's Carfilzomib (NASDAQ: AMGN ), etc.

Author's elaboration, based on clinicaltrials.gov

{kind=link}

In addition, BMY's drug reached the secondary endpoint of the overall response rate. 71% of patients treated with Abecma achieved a response, while 39% achieved a complete response, that is, there was a disappearance of signs of cancer in the patient's body after treatment was completed. At the same time, only 5% of patients receiving standard regimens had a complete response. The safety profile of Abecma was predictable, and no new safety signals were demonstrated in previous clinical studies. Currently, Abecma is approved for treating multiple myeloma in patients with four or more prior lines of therapy. However, given the fantastic results shown in the phase 3 KarMMa-3 study, I expect the company to be able to file the necessary documents with regulators around the world. With a high degree of probability, Abecma will be approved for treating patients with relapsed and refractory multiple myeloma at earlier stages and thereby save tens of thousands of people worldwide.

This drug's growth rate is encouraging, despite specific production difficulties observed in 2022 and, most importantly, outpacing the sales dynamics of Carvykti manufactured by Legend Biotech (NASDAQ: LEGN ) and Johnson & Johnson (NYSE: JNJ ). Thus, Abecma's revenue was $388 million in 2022, up 136.6% compared to 2021, while Carvykti's sales in Q3 and Q4 2022 remained the same.

Source: Author's elaboration, based on quarterly securities reports

{kind=link}

Bristol-Myers Squibb dividend policy and share buyback

Despite increased competition from generics and industry mastodons such as Pfizer (NYSE: PFE ), Novartis (NYSE: NVS ), and AbbVie (NYSE: ABBV ), Bristol-Myers Squibb continues to control costs, which is positively reflected in the stable cash flow needed to increase dividend payouts in recent years. In 2023, the company's investors should receive a dividend of $2.28 per share, up 5.6% from a year earlier. At the same time, the dividend payout ratio, which reflects what percentage of the company's net income goes to pay dividends, is 28.44%. The relatively low value of this financial ratio is a positive sign for investors looking for the potential for long-term business growth since, firstly, Bristol-Myers Squibb's management has the financial ability to continue increasing dividends in subsequent years, but also indicates an understanding of the company's management of the need to solve difficulties associated with expanding the portfolio of products to offset the loss of exclusivity of some blockbusters.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

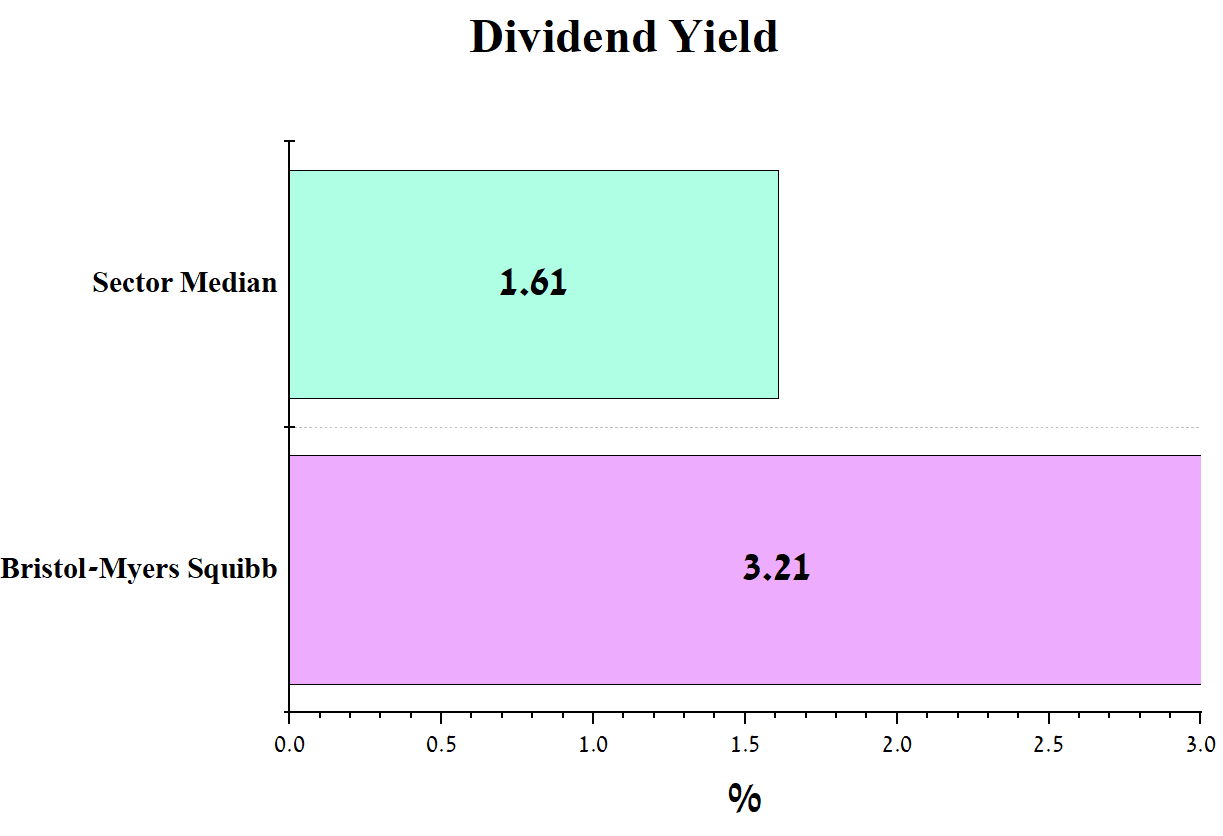

Bristol-Myers Squibb's current dividend yield of 3.21% is well above the healthcare sector average and in line with many companies in other sectors, such as Exxon Mobil ( XOM ) and Chevron Corporation ( CVX ).

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

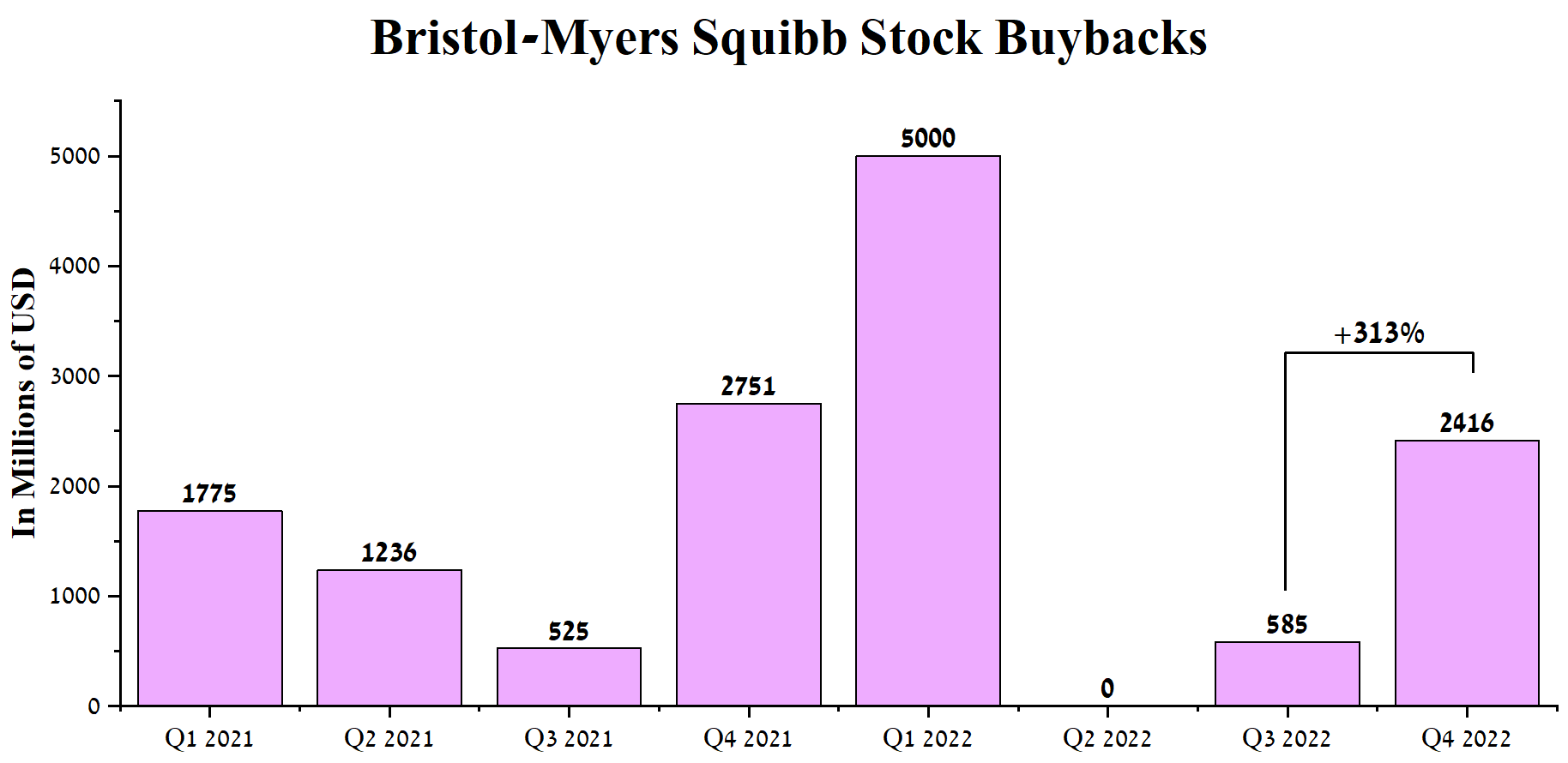

In addition to paying dividends, Giovanni Caforio, as CEO of Bristol-Myers Squibb, actively uses the company's share buyback policy to return capital to shareholders and increase earnings per share, which ultimately improves the company's investment attractiveness on Wall Street. In the fourth quarter of 2022, the company repurchased about $2.4 billion worth of shares, up 313% from the previous quarter. At the end of 2022, the remaining buyback option for Bristol-Myers Squibb shares was $7.2 billion, and thus the company's management has the necessary financial tool to offset the impact of potential macroeconomic shocks on the company's share price.

Source: Author's elaboration, based on quarterly securities reports

{kind=link}

Bristol-Myers Squibb's debt situation

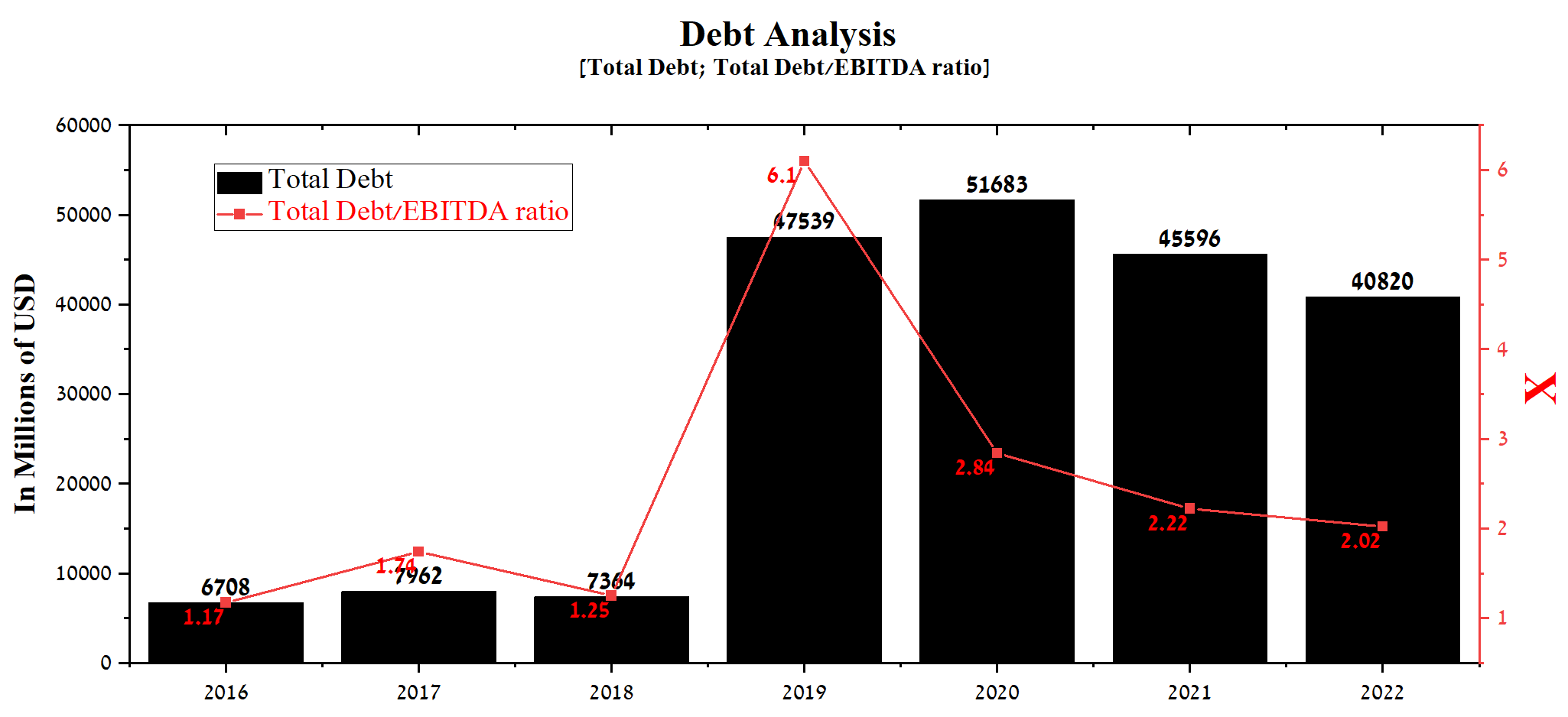

Following the acquisition of Celgene in 2019 and MyoKardia in 2020, Bristol-Myers Squibb's total debt has increased significantly. However, the acquisition of these two companies and Turning Point Therapeutics in 2022 has allowed the company to dramatically increase its portfolio of approved drugs and product candidates, which play a crucial role in Bristol-Myers Squibb's revenue growth. At the end of 2022, the company's total debt was $40,820 million, down $10,863 million from its peak. More importantly, the total debt/EBITDA ratio continues to decline year on year to 2.02x, a positive indication of the company's ability to manage debt and have the financial capacity to continue investing in growth opportunities.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

Conclusion

Despite facing numerous economic and geopolitical challenges, Bristol-Myers Squibb has maintained its resilience as one of the oldest pharmaceutical companies in the world. The company's primary focus is developing and commercializing innovative products in various therapeutic areas, such as oncology, hematology, and cardiovascular disease.

2023 will be the year of necessary transformations in the company and will test the effectiveness of the business model built under the control of the CEO of the company. A slight decline in Bristol-Myers Squibb's revenue due to the loss of exclusivity of Revlimid, which is the company's mega-blockbuster and saves hundreds of thousands of cancer patients, will temporarily reduce interest from Wall Street speculators. On the other hand, a temporary decline in speculative interest could make Bristol-Myers Squibb's share price less volatile and more closely linked to its underlying fundamentals. In addition, the decrease in speculative interest will be offset by the company's share buyback, high dividend yield, and continued expansion of the portfolio of approved medicines that can dramatically improve the quality of life and stay ahead of the competition. The remaining buyback option for Bristol-Myers Squibb's shares was $7.2 billion, giving the company's management the necessary financial tool to mitigate the potential impact of macroeconomic and geopolitical shocks on the company's share price.

Breyanzi, Abecma, Sotyktu, and Opdualag are showing impressive sales growth rates and will be key contributors to the company's total revenue growth over the next five years. The mechanisms of action of many of Bristol-Myers Squibb's product candidates are revolutionary and, as a result, show high efficacy and a favorable safety profile in phase 2/3 clinical trials and, more importantly, outperform competitors. Given its status as a global pharmaceutical company and its marketing capabilities, Bristol-Myers Squibb is likely to be able to convert its clinical outcomes into billions of dollars in cash flow.

In addition, when using P/S and P/E ratios, which are among the most commonly used financial ratios to assess the attractiveness of an asset, due to their ability to provide an investor with an estimate of how much an asset is undervalued or overvalued compared to its peers or the industry as a whole. Moreover, thanks to them, it is possible to assess the risks of the analyzed asset, and the lower these financial ratios, the less risky the shares are for investors. Low P/S, P/E ratios that are significantly below those of many large pharmaceutical companies, and continued high margins indicate that the company is undervalued relative to other members of the S&P 500 (NYSEARCA: SPY ) and, as a result, provide an excellent opportunity for long-term investors to consider Bristol-Myers Squibb as an investment.

For further details see:

What To Expect From Bristol-Myers Squibb In 2023