BHC - What To Expect From Viatris In 2023

Summary

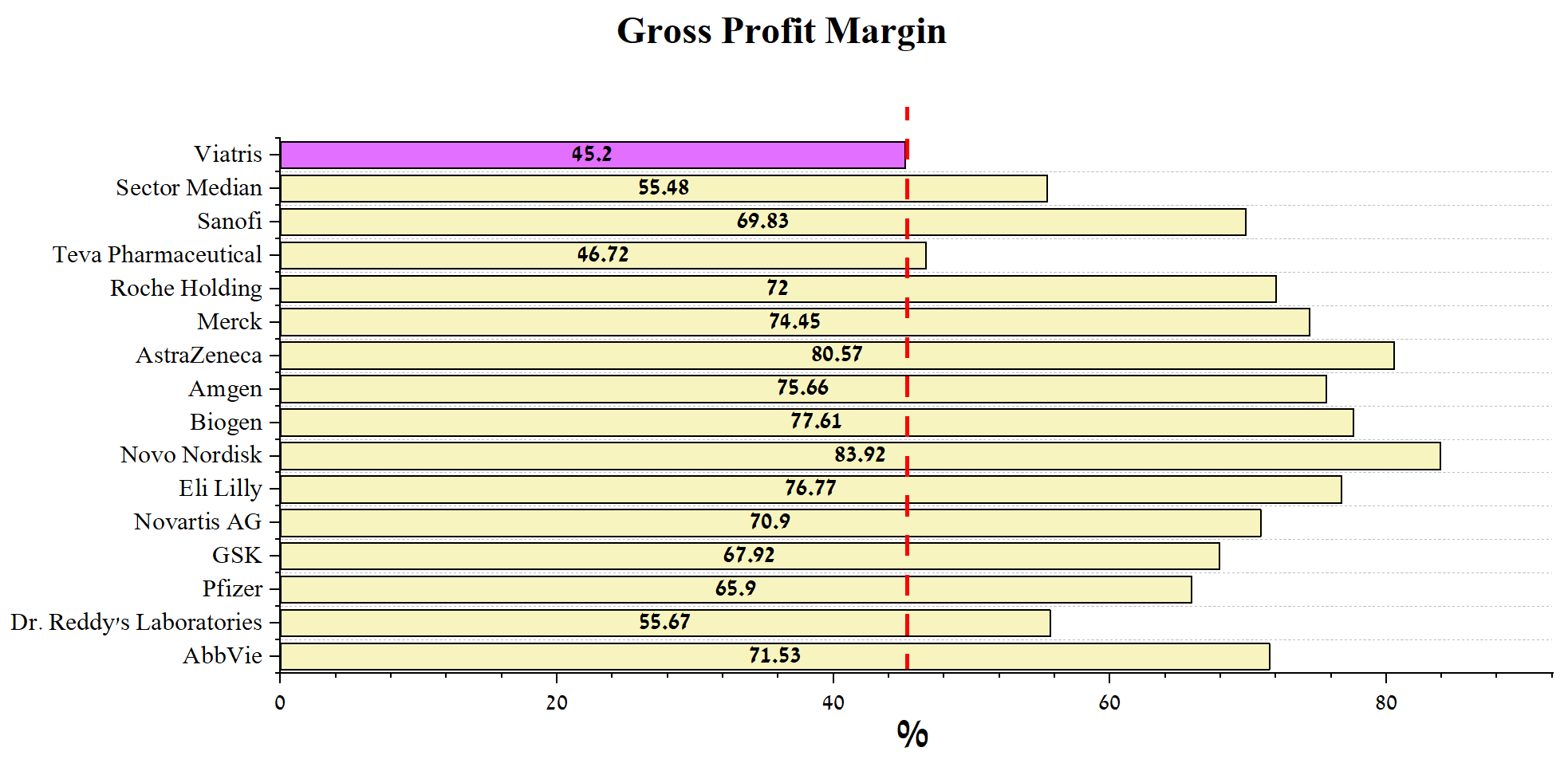

- Viatris' gross margin reached its highest level since its inception in the fourth quarter of 2020, despite rising raw material and labor costs.

- On February 27, 2023, Viatris management will publish financial results for the 4th quarter of 2022.

- Viatris' operating income for the past twelve months was $3,193.7 million, well above payments on senior notes maturing through 2030.

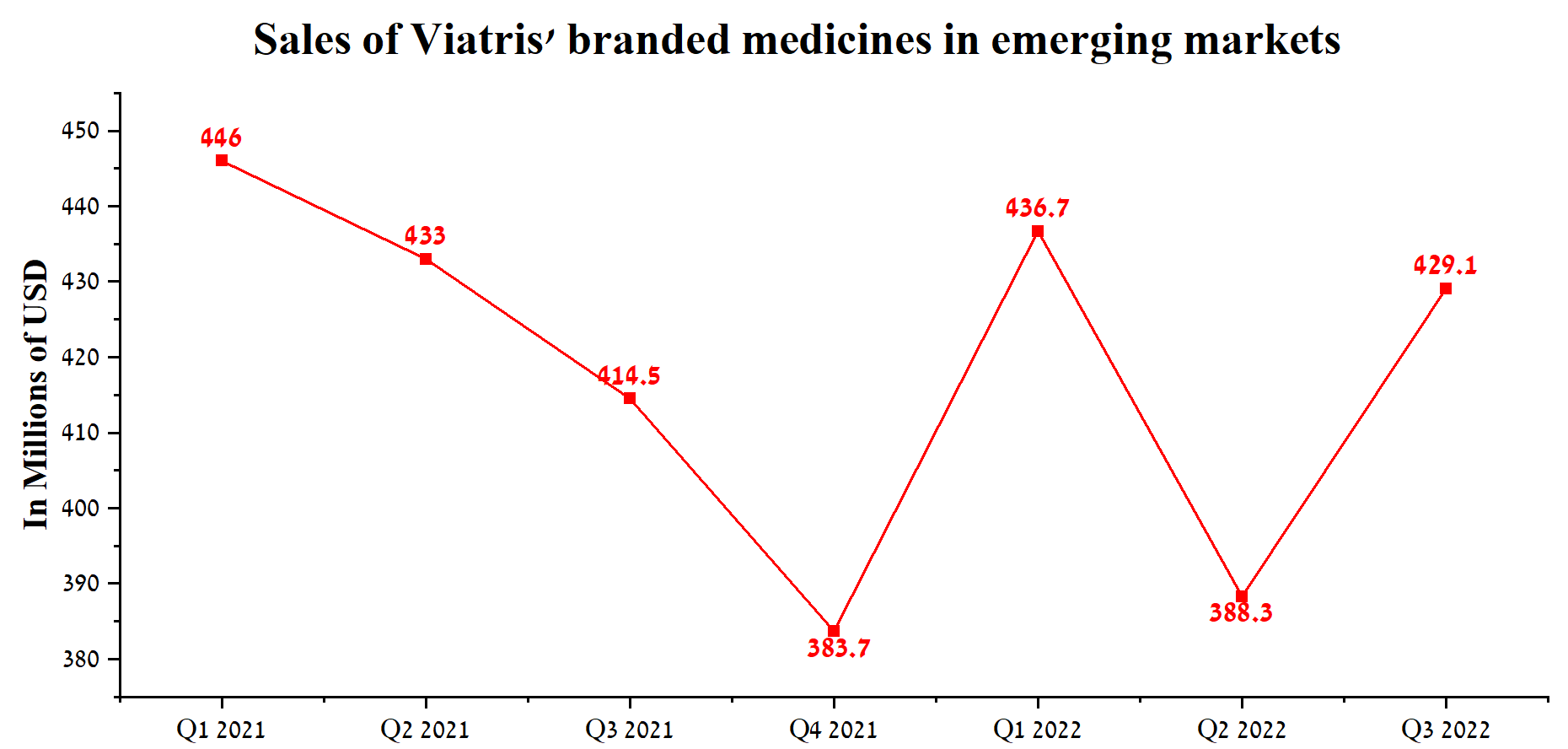

- Sales of the company's branded medications in emerging markets amounted to $429.1 million, or 10.5% of Viatris' total revenue, showing positive dynamics year-on-year and quarter-on-quarter.

- On November 7, 2022, the company announced the acquisition of Oyster Point Pharma and Famy Life Sciences to create a franchise in the ophthalmic field.

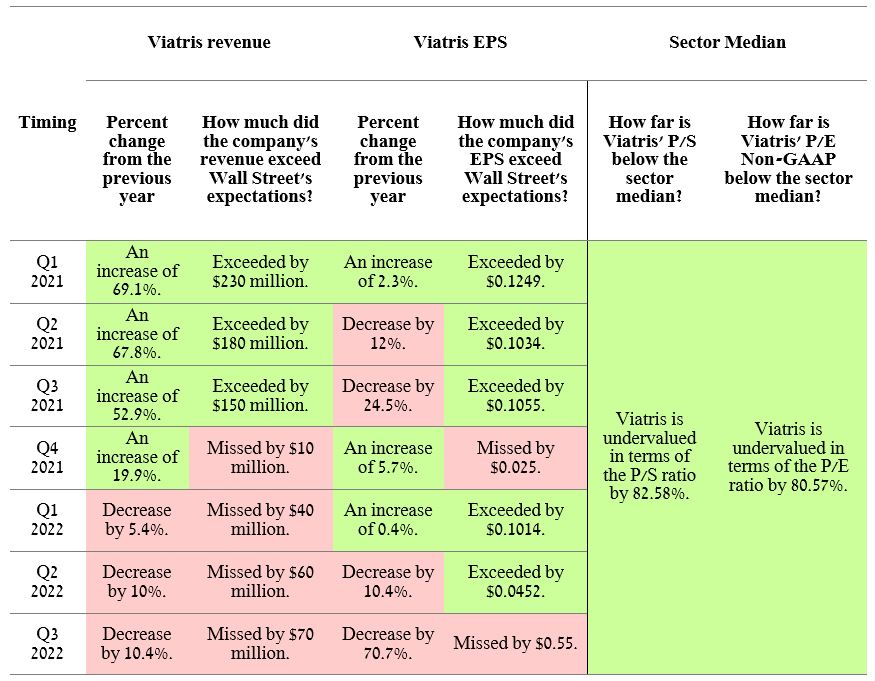

Viatris ( VTRS ) is a pharmaceutical company formed from the merger of Mylan and Upjohn in November 2020 with headquarters in Canonsburg, Pennsylvania. The goal of Viatris' management was to combine the strengths of both companies to become a leader in manufacturing, marketing, and ultimately improving patients' access to high-quality medicines. However, due to increased competition with other pharmaceutical companies in providing products and services and restrictive measures introduced due to the worsening situation with COVID-19 in 2020-2021, the company's business trajectory was far from planned. As a result, Viatris' revenue and net income have been deteriorating in recent quarters and falling short of Wall Street analysts' forecasts. However, the latest deals and news from the company's management are starting to inspire optimism not only in anticipation of the publication of the financial report for the fourth quarter of 2022 on February 27, 2023 but also in general for the coming quarters.

{kind=link}

Author's elaboration, based on Investing.com

Viatris’ financial position and business prospects in the coming years

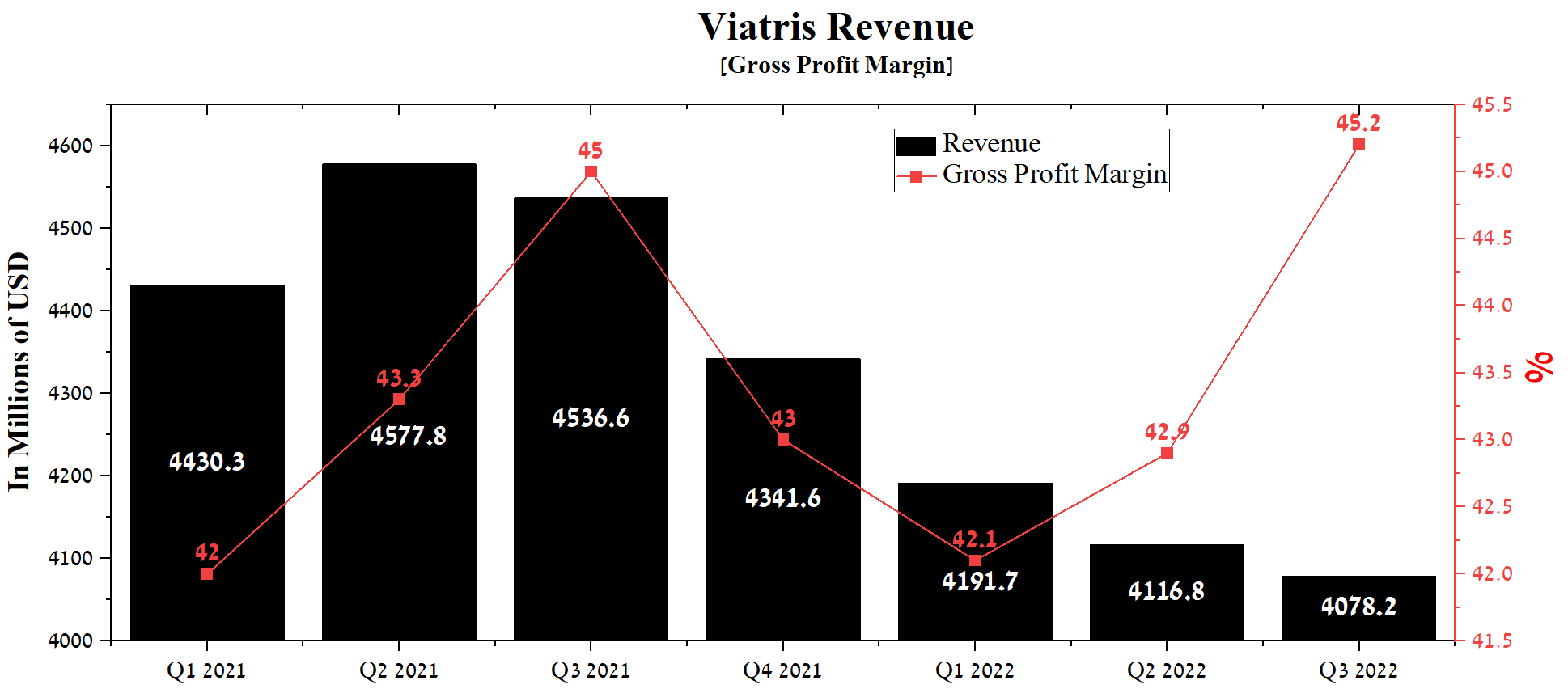

Viatris' revenue was $4,078.2 million in Q3 2022, showing a negative trend compared to previous quarters due to certain factors that will be discussed in this article. The favorable moment is that the rate of decline in sales of some medicines is decreasing, and some segments have begun to show growth.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

Viatris' gross margin has reached its highest since its inception in Q4 2020, despite the rise in raw material and labor costs due to the wave of inflation that swept the world. In addition, the growth of this financial indicator occurred despite the increasing complexity of the production of generics, which have a more complex structure and, as a result, require a more significant number of production steps and equipment purchases compared to the production in previous years. On the downside, Viatris' gross margin is still lower than generics like Teva Pharmaceutical (NYSE: TEVA ) and Dr. Reddy's Laboratories ( RDY ). The company is far behind S&P 500's mastodons AbbVie ( ABBV ), Johnson & Johnson ( JNJ ), Merck ( MRK ), and Bristol Myers Squibb ( BMY ). Viatris' gross margin will continue to grow marginally in the coming quarters, and I predict it will average 46% in 2023.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

Viatris branded drugs

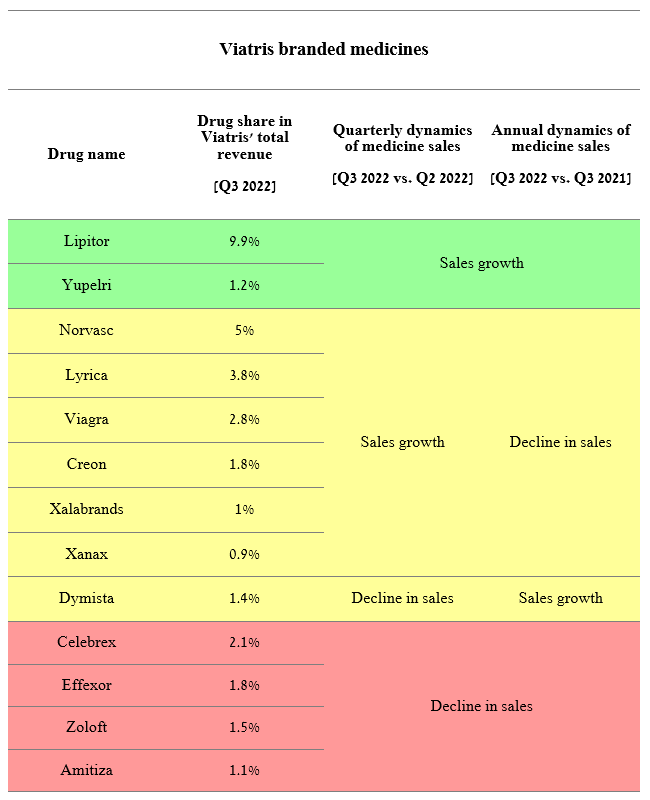

Viatris, formed from the merger of Mylan with Pfizer's (PFE) Upjohn business in 2020, has a portfolio of twenty globally recognized brands, including Viagra, Lyrica, and Lipitor, with high margins and thus make a major contribution to cash flow. But after a while, the exclusivity of these medicines ended, and the market was flooded with their generic versions. Despite increased competition, patients outside of developed markets often prefer brand-name drugs over cheaper alternatives due to a common problem with the quality of generic drugs and the efficiency of Viatris' sales managers. For example, sales of the company's branded medications in emerging markets amounted to $429.1 million, or 10.5% of Viatris' total revenue, showing positive dynamics year-on-year and quarter-on-quarter.

{kind=link}

Author's elaboration, based on quarterly securities reports

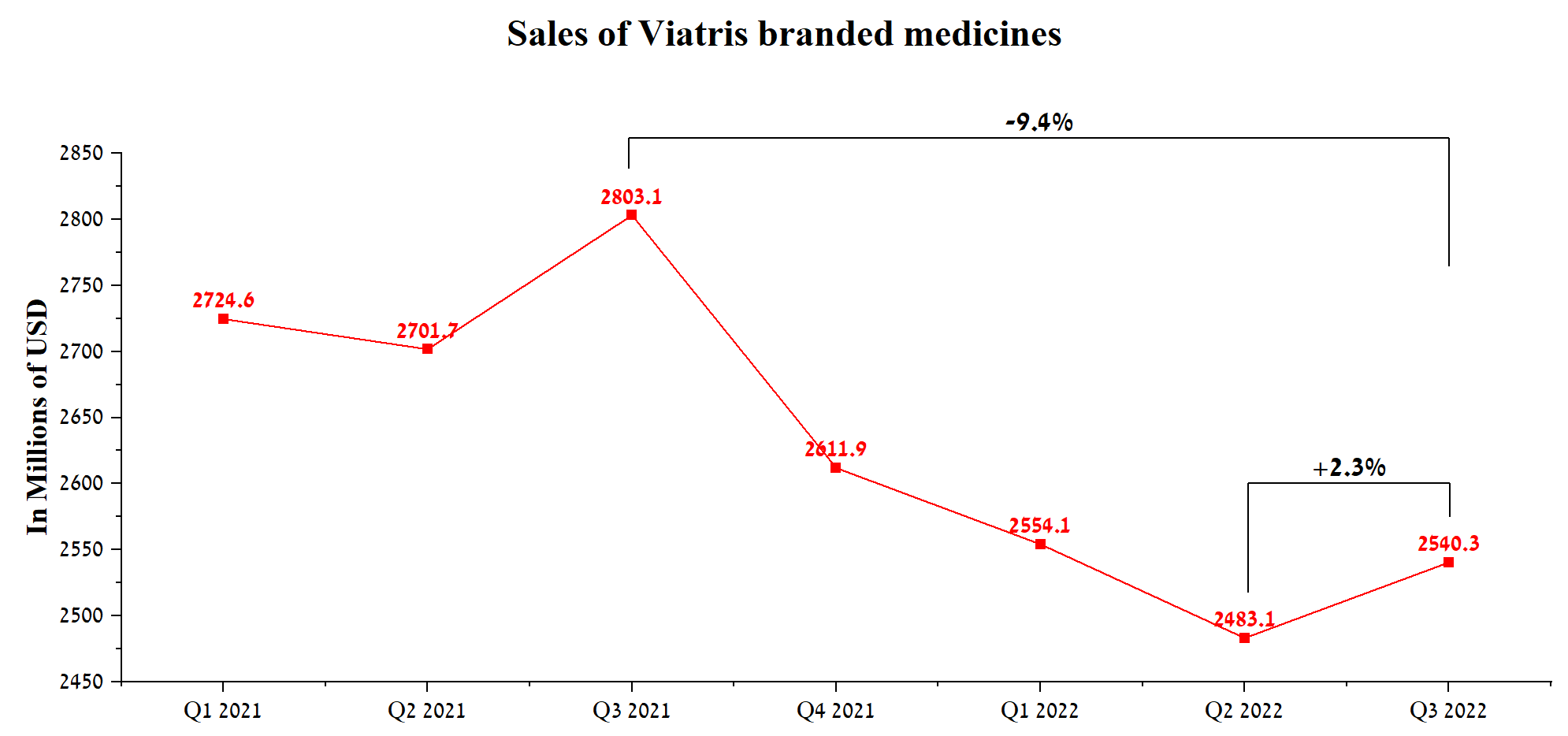

However, on a more global scale, there is a decline in sales of Viatris' branded drugs in other regions, and this negative trend is putting downward pressure on the company's investment attractiveness. So, their total sales amounted to $2,540.3 million or 62.5% of the company's total revenue for the third quarter of 2022, showing a decrease of 9.4% compared to the previous year.

{kind=link}

Author's elaboration, based on quarterly securities reports

The main reasons for the decrease in revenue in the segment focused on the sale of branded drugs are a significant increase in competition with generic drugs and regulatory approval for new-generation medicines to combat neurological and cardiovascular diseases, which can dramatically improve the quality of life of patients compared to current Viatris products.

{kind=link}

Author's elaboration, based on quarterly securities reports

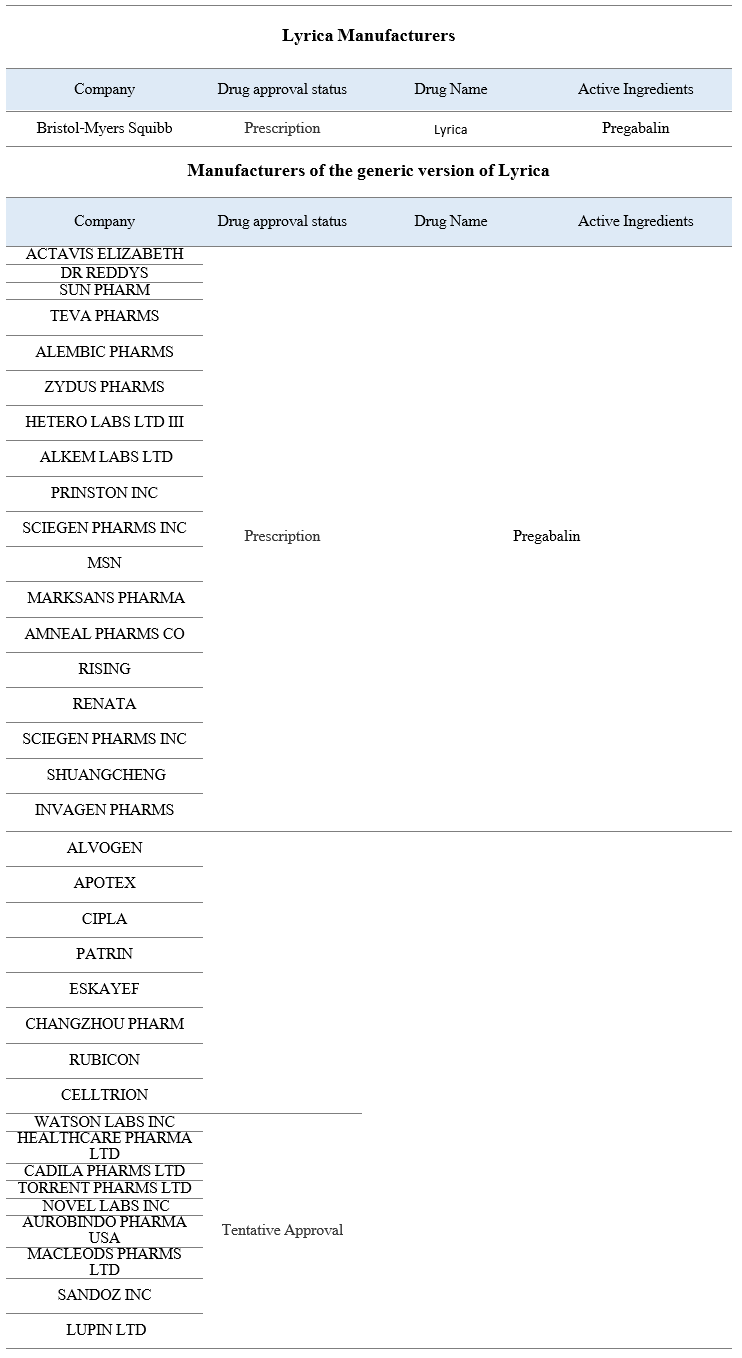

For example, Lyrica's sales were $156.5 million in Q3 2022, down 10.9% year-over-year due to competition from Amneal Pharmaceuticals ( AMRX ), Novartis' Sandoz ( NVS ), and other generic manufacturers. Moreover, several generic versions of Lyrica have "tentative approval" status. As soon as the FDA approves their entry into the US market, the erosion rate of sales of this Viatris product will also accelerate.

{kind=link}

Source: Author's elaboration, based on FDA

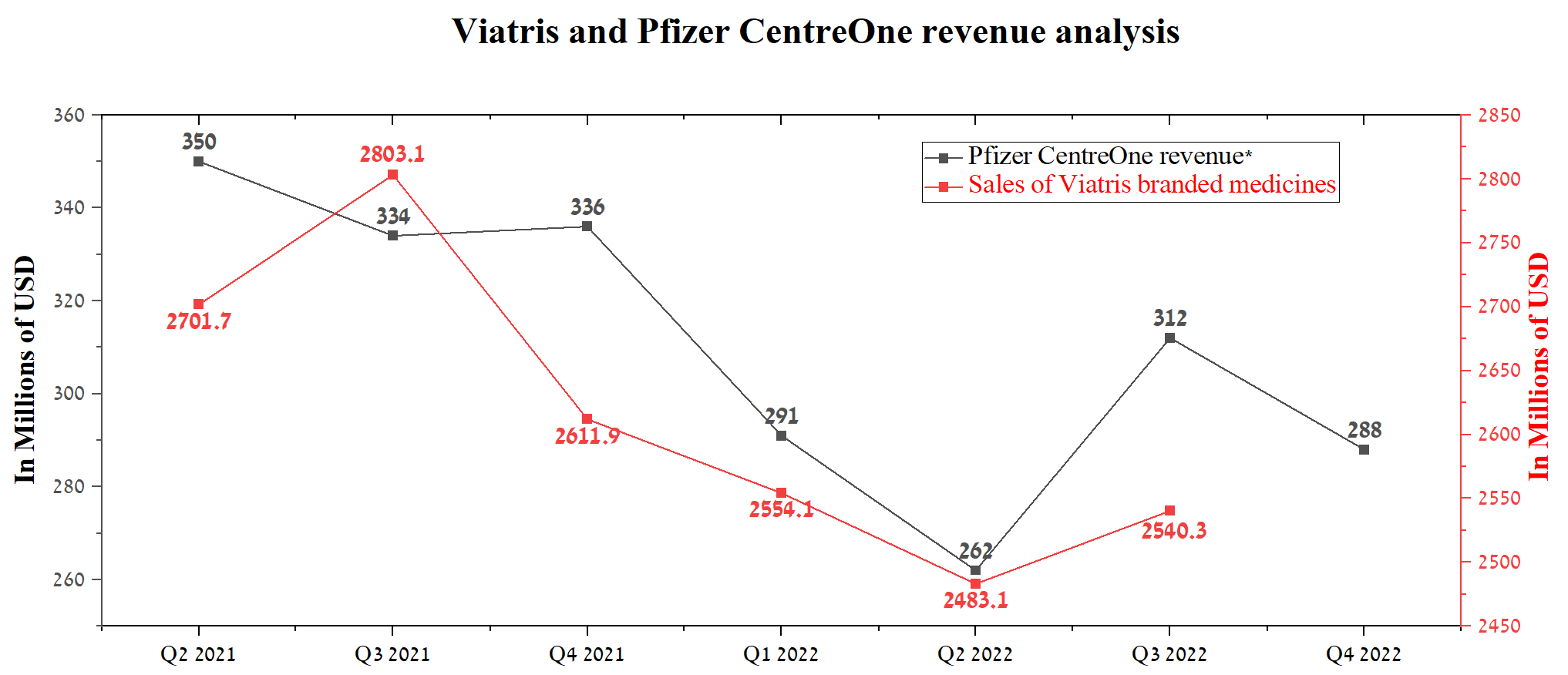

In order to predict sales of the company's medicines, I turned to Pfizer's financial statements for the past eight quarters. One of its divisions is Pfizer CentreOne, which, among other things, is engaged in producing and supplying active pharmaceutical ingredients to synthesize Viatris' branded drugs. The chart below shows Pfizer CentreOne's (PC1) revenue trend, which excludes COVID-19 vaccine manufacturing revenue under partnership agreements with BioNTech.

Although Pfizer does not disclose how much of PC1's revenue comes from sales of active pharmaceutical ingredients for Viatris medicines. However, there is a clear correlation between sales of Viatris products and Pfizer CentreOne's revenue of $288 million in Q4 2022, down 14.3% year-over-year. As a result, I expect Viatris' branded drug segment to be in the $2,400-2,450 million range for Q4 2022, down $161.9-$211.9 million from a year earlier.

{kind=link}

Author's elaboration, based on quarterly securities reports

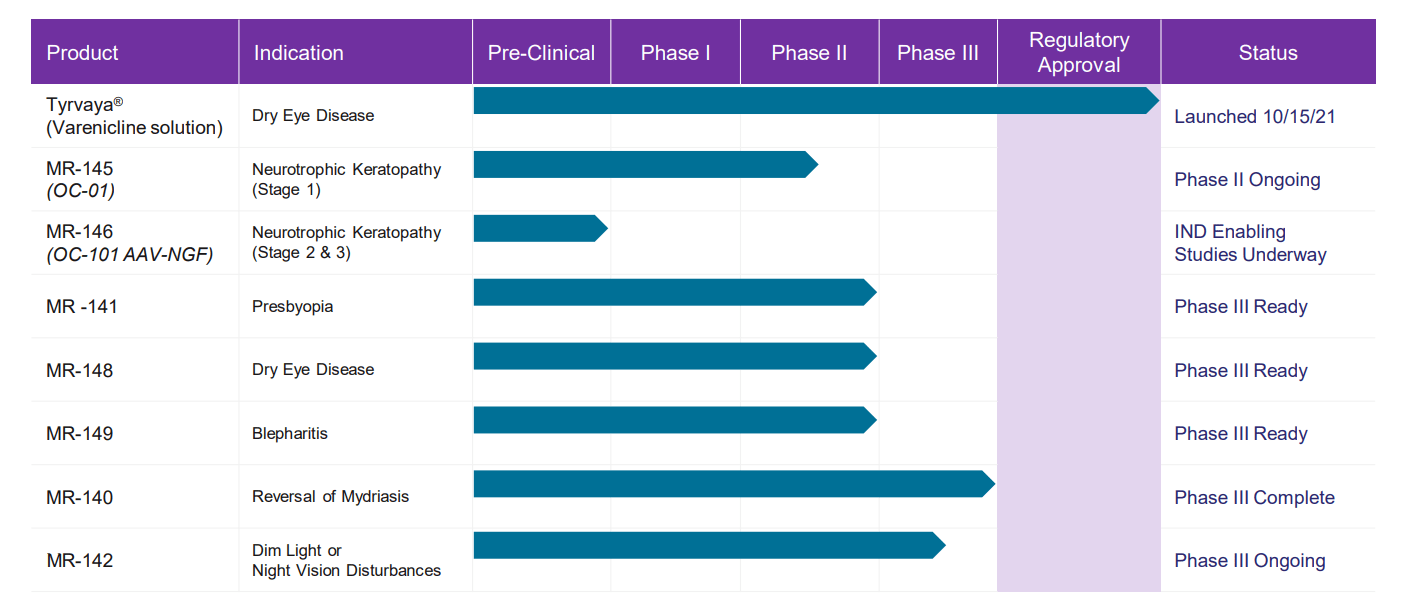

But there are also positive changes in the structure of Viatris' business, although they will not significantly impact the company's financial position in the short term. One change came on November 7, 2022 , when the company announced the acquisition of Oyster Point Pharma and Famy Life Sciences to create a franchise in the ophthalmic field.

{kind=link}

Source: Viatris Investor Presentation

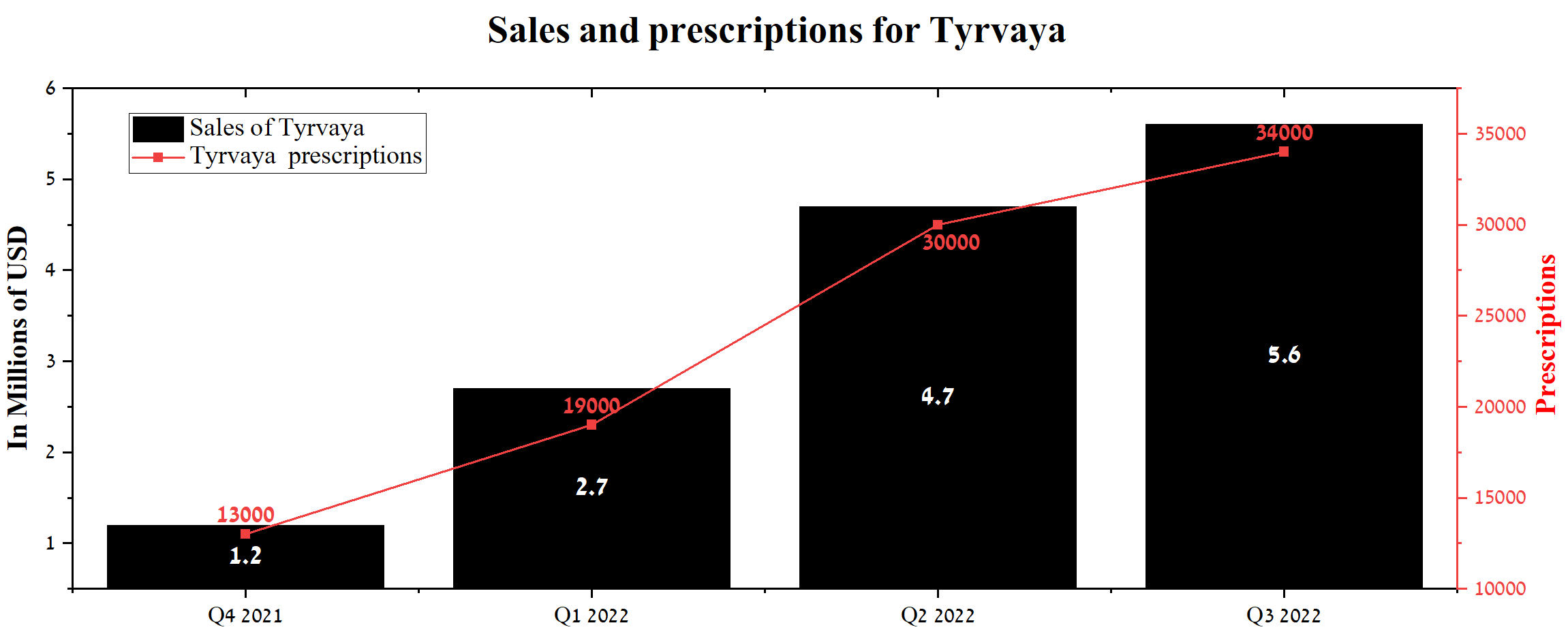

In addition to acquiring product candidates in Phase 2/3 clinical trials, Viatris has obtained the FDA-approved drug Tyrvaya for treating signs and symptoms of dry eye disease. In Q3 2022, Tyrvaya's sales were $5.6 million, up 19% from the previous quarter. Despite a more significant increase in prescriptions of 34,000 from July to September 2022, sales growth rates are still not convincing. The main reasons for this were high competition, low brand awareness, and low advertising budget for Oyster Point Pharma relative to larger pharmaceutical companies such as Roche Holding (RHHBY)(RHHBF), Daiichi Sankyo (DSNKY), and Bausch Health ( BHC ), which have the financial capacity to run more extensive advertising campaigns and raise patient awareness of their medicine potential.

{kind=link}

Author's elaboration, based on quarterly securities reports

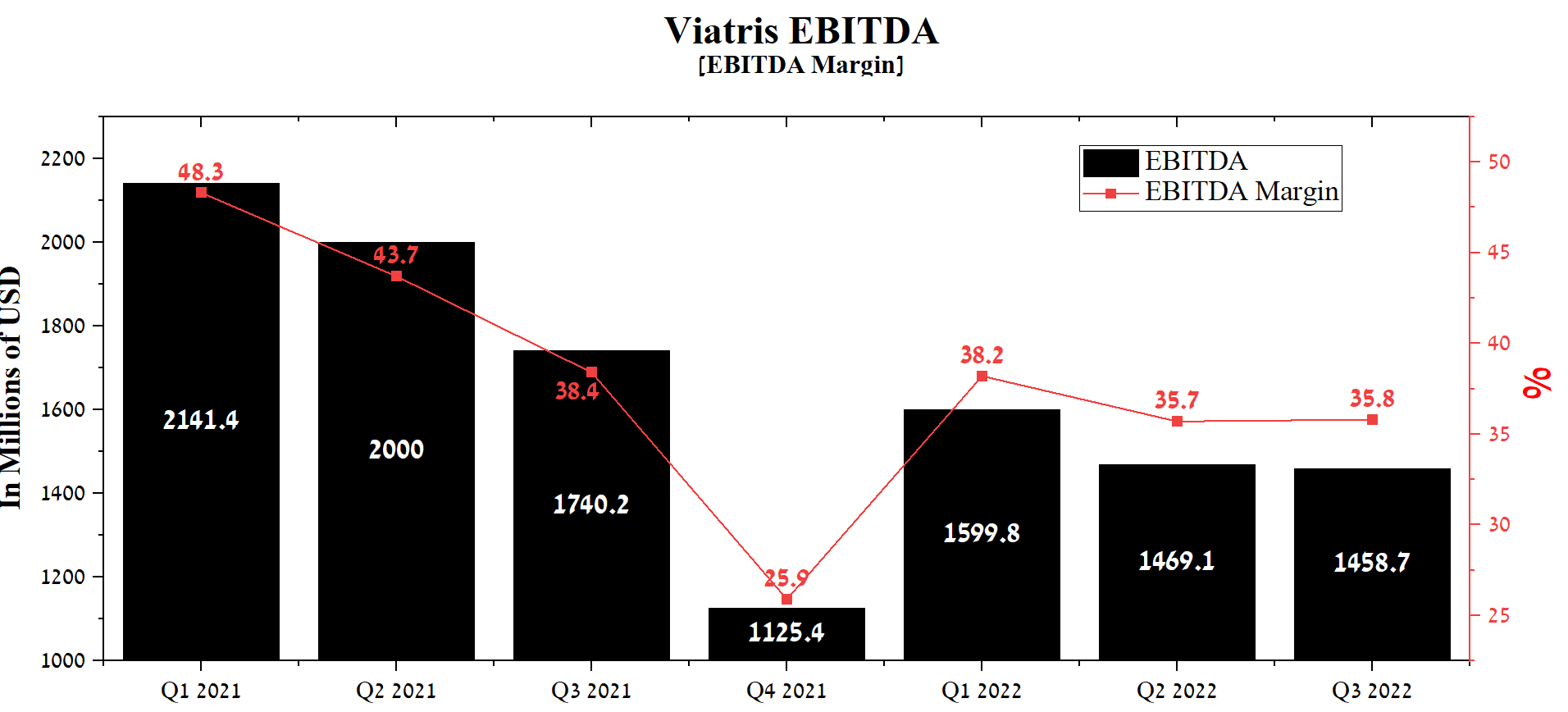

However, with the acquisition of Oyster Point Pharma, Viatris' management will be able to leverage its financial strength and sales network to accelerate dry eye sufferers' awareness of Tyrvaya's benefits over products in the multi-billion-dollar ophthalmic disease therapeutics market. According to my model, the revenue of this product will bring the company $80 million in 2023 and $125 million in 2024. But despite the increase in sales, Viatris' ophthalmic portfolio will generate negative EBITDA through the second half of 2025 due to multimillion-dollar drug launch spending and increased R&D spending. The company's EBITDA was $1,458.7 million in Q3 2022, down 16.2% from a year earlier.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

Due to the decline in this financial indicator, in conjunction with the sale of a biosimilars portfolio to Biocon Biologics and the process begun to find buyers for the company's non-core assets, Viatris' management stepped up business restructuring to improve its margins and reduce overall debt. So, for example, according to a Bloomberg report , Zentiva Advent International, CVC Capital Partners, TPG Inc. ( TPG ), and Stada Arzneimittel are considering buying the company's European OTC portfolio. The sale of these medicines could bring Viatris about 3 billion euros. But if the deal is reached, the company's total revenue may decrease by $1-$1.2 billion annually.

Viatris dividend policy

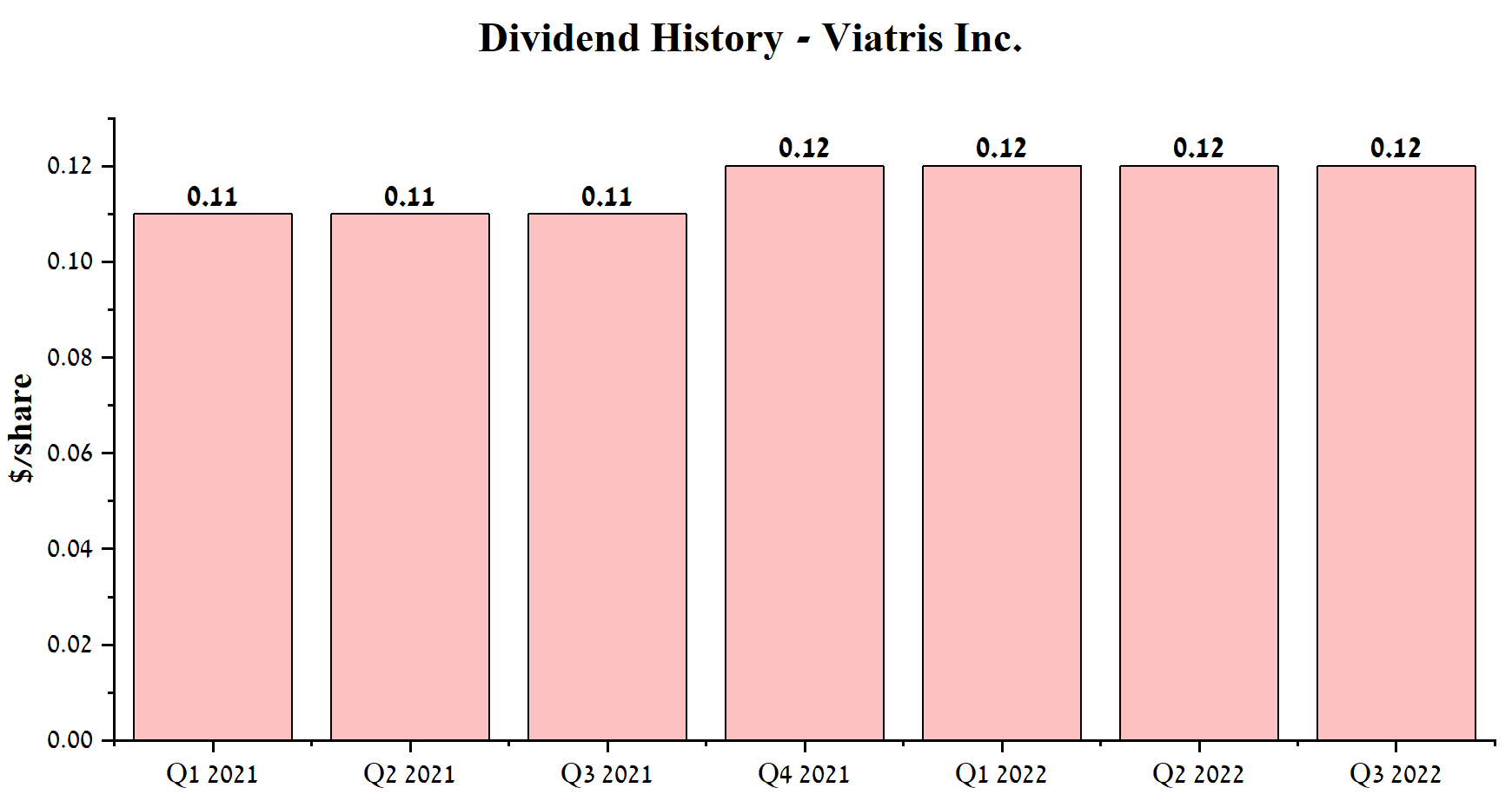

Despite declining drug sales and intensifying efforts to find potential acquisition targets to expand its portfolio of product candidates, Viatris' management continues to pursue a conservative financial policy to increase dividend payments. In 2022, the quarterly dividend payout was increased from $0.11 to $0.12, while the dividend payout ratio remained low at 13.78%.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

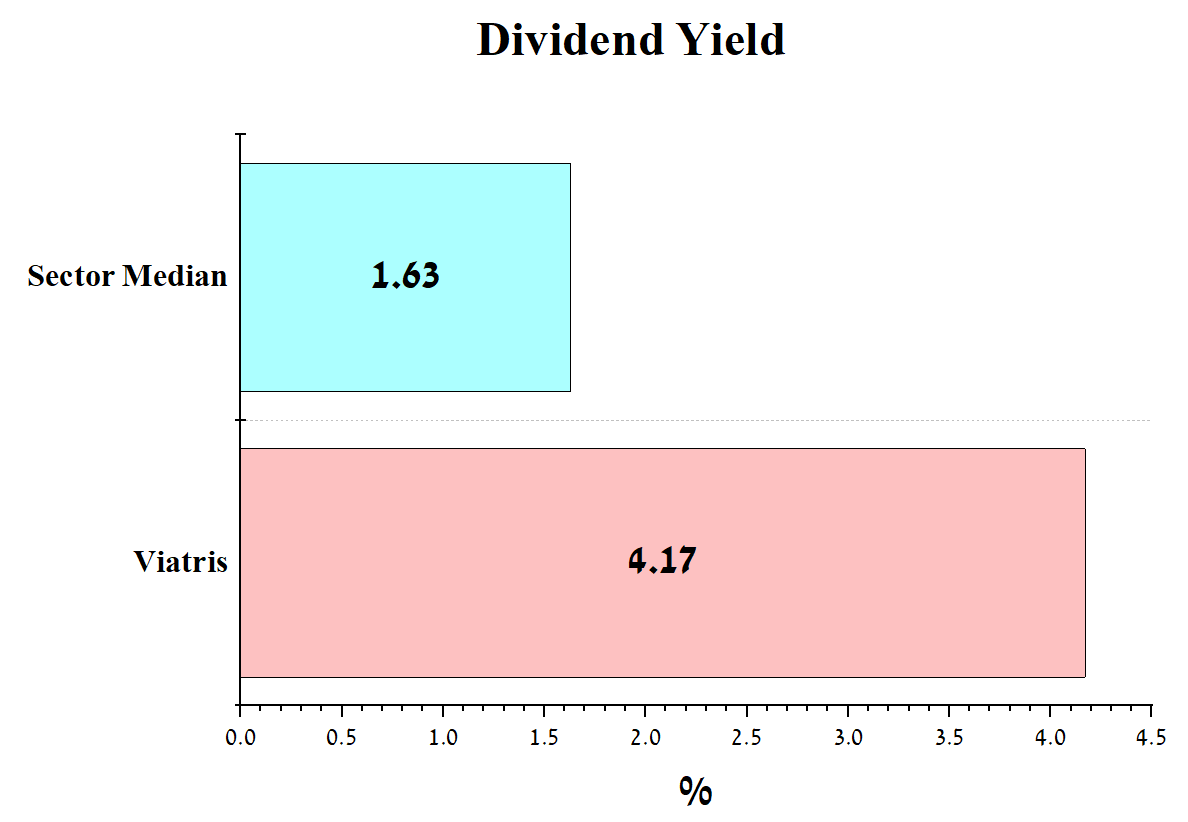

Although the company can continue to increase dividend payments in the coming years, I hope that Michael Goettler, the CEO of Viatris, will refrain from resorting to this because of the need to get the business back on the right track with growing financial indicators. Viatris' current dividend yield is 4.17%, well above that of dividend aristocrats such as Abbott Laboratories ( ABT ), Exxon Mobil ( XOM ), and Walmart ( WMT ).

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

Viatris' debt situation

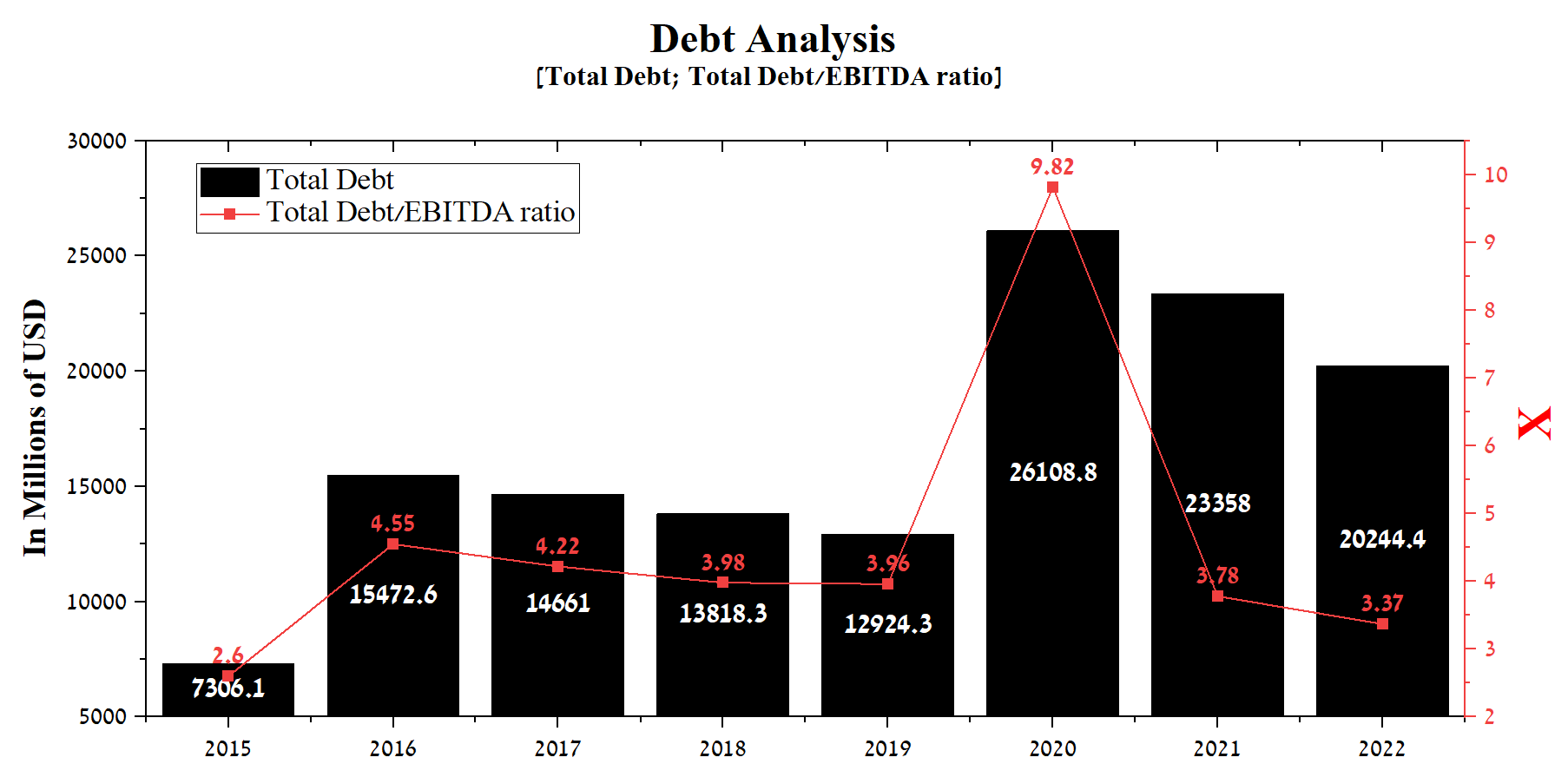

Due to the need to finance expenses associated with merging and integrating Mylan's business with Upjohn, a branded drug manufacturer, Viatris' total debt was $26,108.8 million at the end of 2020. However, due to the desire of the company's management to reduce the debt burden and, as a result, the strategic changes made, including focusing the business on developing innovative products in ophthalmology and dermatology, the total debt continues to decrease rapidly. At the end of Q3 2022, the company's total debt was $20,244.4 million, down $3,113.6 million from the end of 2021. In addition, the Total Debt/EBITDA ratio decreased to 3.37x, and with the stabilization of medicine sales in China and emerging markets, the company does not have significant debt servicing risks at the moment.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

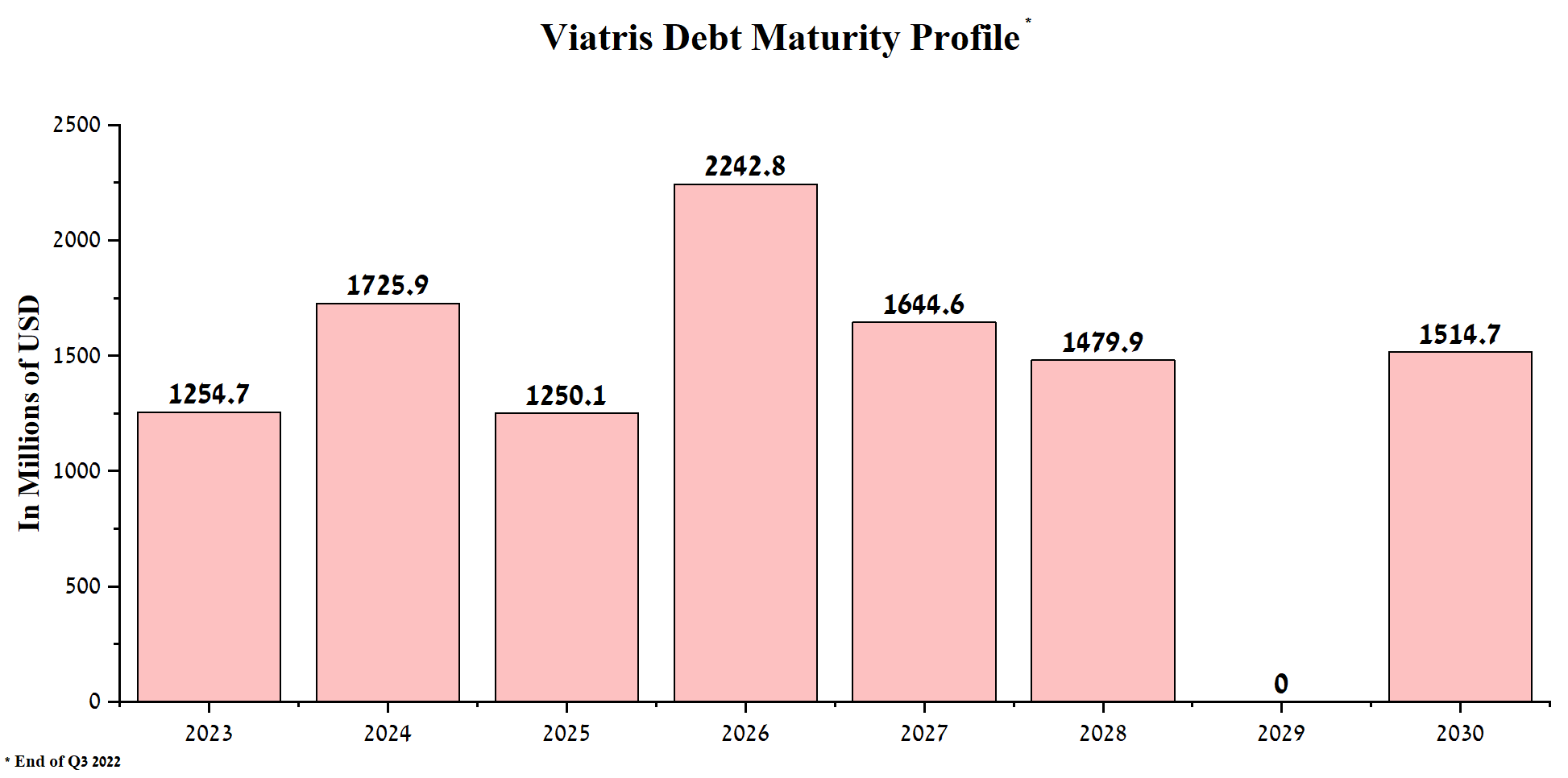

Viatris' operating income for the past twelve months was $3,193.7 million, well above payments on senior notes maturing through 2030.

{kind=link}

Author's elaboration, based on quarterly securities reports

Conclusion

Viatris, a pharmaceutical company based in Canonsburg, Pennsylvania , was established in November 2020 following the merger of Mylan and Upjohn. Viatris' management was responsible for leveraging the respective strengths of these two companies to create a top player in the pharmaceutical industry, focused on manufacturing, marketing, and enhancing patient access to superior quality medicines in rapidly expanding markets.

The company's product portfolio comprises generics and branded medicines that have lost exclusivity. Thanks to geographic diversification, Viatris' management has the tools to slow down the erosion of the business's financial position caused by lower revenues in recent quarters. Patients outside of developed markets often prefer brand-name drugs over cheaper alternatives due to a common problem with the quality of generic drugs and the efficiency of Viatris' sales managers.

If Viatris' management resolves the current risks associated with the lack of assets that can return the company to the path of growing net profit, then the company may resort to active use of the share buyback program in the amount of up to $1 billion, which has not yet been used. In my estimation, this could happen by the end of 2023 as the macroeconomic and geopolitical situation in the world improves, inflationary pressures on production processes decrease, and transactions for the sale of non-core assets totaling about $9 billion are completed.

In the previous article, "Viatris: 5% Dividend Yield Is A Threat For Investors" , I expected that after Viatris's share price reached $12.50, there would be a correction to $8.00. However, with the acquisition of Oyster Point Pharma and Famy Life Sciences to establish Viatris as one of the leading companies in the ophthalmic disease therapeutics market, in the short term, I expect the company's share price may only correct to $10.10 per share after which Mr. Market will move to the accumulation phase of the asset. If Mr. Goettler publishes more detailed strategic plans for the company's development and expanding the portfolio of Viatris' branded medicines, then my vision of the company's future will be revised in a positive direction.

For further details see:

What To Expect From Viatris In 2023