MPC - What To Make Of Marathon Petroleum's Dividend

2023-06-21 08:51:12 ET

Summary

- Marathon Petroleum presents a compelling opportunity for long-term investors seeking downstream energy exposure, with strong financial performance and potential for growth.

- The refining industry is experiencing a secular tailwind due to subdued supply growth, leading to elevated prices for refined products.

- MPC rewards investors through dividends and buybacks, with a track record of consistent payouts, but refinery stocks can be cyclical and volatile.

Introduction

When it comes to the nation's largest (pure-play) refinery company, Marathon Petroleum ( MPC ) , there are two things to keep in mind.

- As we'll discuss in this article, MPC is an extremely well-run business with high margins and the ability to generate tremendous shareholder value and stock price outperformance.

- (Some) investors tend to avoid MPC as it never seems to be really cheap, while it also doesn't come with a juicy yield, which is often the reason why people buy energy stocks.

While I'm writing this, MPC shares are down roughly 20% from their all-time high as a result of rising recession risks and the rotation from value to growth stocks.

Although I would make the case that some de-risking is justified, I'm not a seller on strength but a buyer on weakness.

As I will explain in this article, I believe that MPC is starting to present an appealing opportunity for long-term investors looking for downstream energy exposure.

Or, to put it differently, after focusing on high-quality upstream and midstream companies, it's now time to give you one of the best downstream plays on the market.

So, let's get to it!

The Refining Boom

I have to be honest. When it comes to energy, I prefer upstream companies. These are the companies that produce oil and gas, which are then shipped to customers through midstream companies. I prefer upstream companies because I believe that long-term demand growth will be lower than expected - that's the short version. This tends to come with tremendous pricing benefits.

Midstream is great for income-oriented investors, especially because some of these companies are also undervalued. While some upstream companies come with high dividends during energy upswings, midstream income is more reliable.

Eland Cables

Then there's downstream. The companies that turn oil into refined products like gasoline, diesel, and kerosene.

I started buying exposure in this industry in 2020 when the pandemic caused demand to implode. Back then, it came with tremendous buying opportunities. I bought one of the most beaten-down stocks back then: Valero Energy ( VLO ).

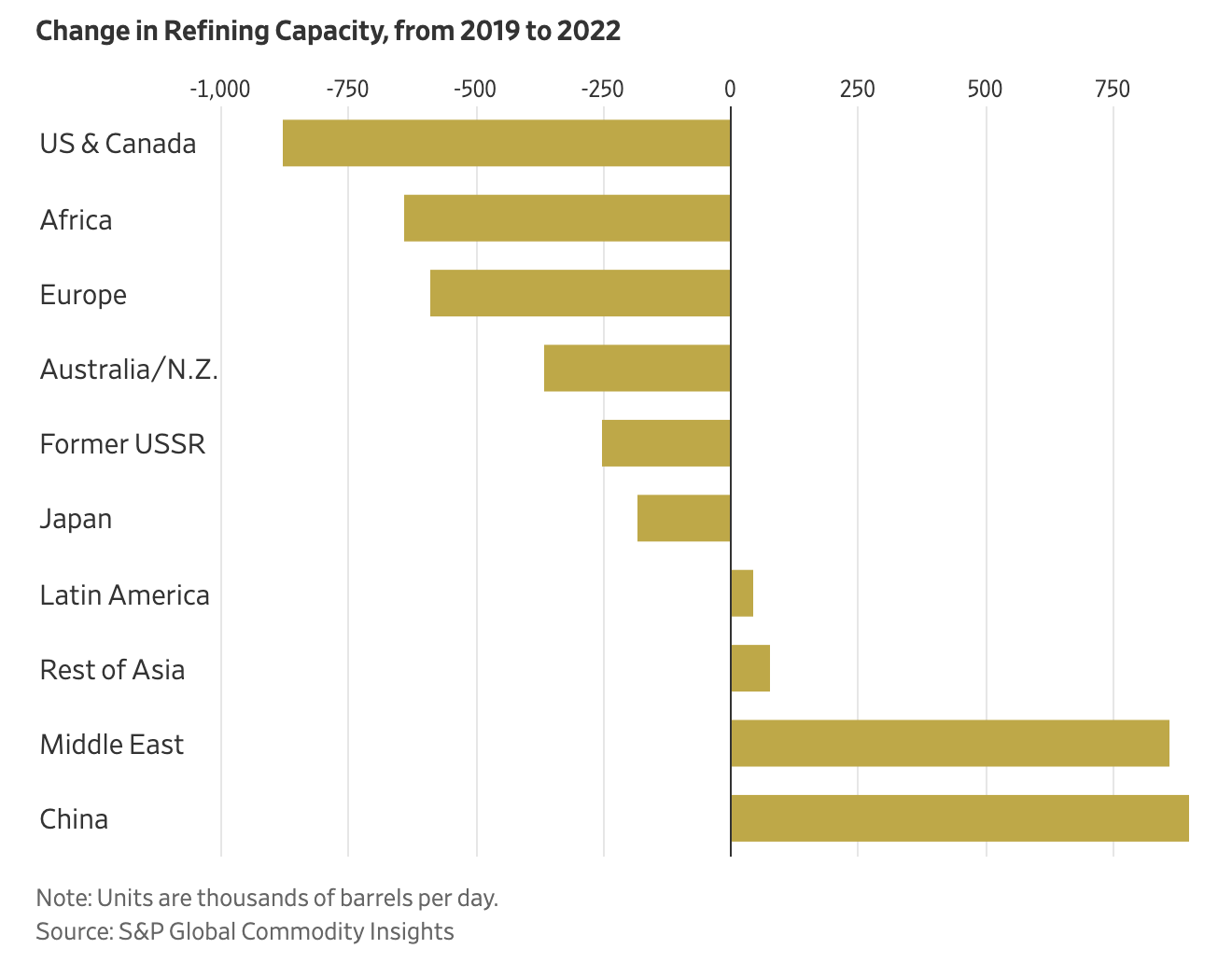

What's interesting about refining is the secular tailwind that consists of subdued supply growth.

As reported by the Wall Street Journal earlier this year and according to S&P Global Commodity Insights, global refinery capacity has diminished by 921,000 barrels per day since 2019, while the International Energy Agency forecasts demand for oil products exceeding 2019 levels by more than 1 million barrels per day this year.

{kind=link}

Wall Street Journal

Analysts suggest that this disparity is a key factor behind the persistence of elevated prices for gasoline, diesel, and jet fuel relative to crude oil.

Rick Joswick, the head of global oil analytics at S&P Global Commodity Insights, indicates that new refineries capable of adding 3 million barrels per day in capacity are slated to begin operations this year. However, it typically takes a year or longer for a refinery to reach its maximum output potential.

Hence, despite getting crushed during the pandemic, two of three pure-play refining companies in the United States have outperformed the S&P 500 over the past ten years. MPC stock has returned more than 310% over the past ten years.

Moreover, after Exxon Mobil ( XOM ) launched the Beaumont expansion this year, all future refinery additions will be in Asia and Africa, as developed nations aren't investing in expensive refineries anymore.

So, while the biggest post-pandemic supply tailwinds are fading, the bull case for North American refiners remains strong.

A Strong Financial Performance

Excluding dividends, MPC shares are down close to 20% from their all-time high. This makes it the second-worst sell-off since the start of 2022.

Right now, the question on everyone's mind is: when do we start buying?

So far, MPC is doing extremely well.

In the first quarter , the company highlighted the volatile global energy market influenced by factors such as potential recession, China's economic recovery, and Russian product sanctions. Despite these uncertainties, global demand for affordable and reliable energy continues to grow.

- The International Energy Agency projects a 2 million barrels per day increase in demand for 2023. Refining margins are expected to remain strong throughout the year due to supply constraints and growing demand.

- While distillate cracks have decreased, gasoline cracks have improved with the onset of the summer driving season.

Hence, MPC remained optimistic about gasoline strength improving the diesel situation while jet fuel demand continued to recover. However, the ongoing recovery in China and potential recessionary impacts will impact the outlook for the rest of the year.

In its first quarter, the company generated $35.1 billion in revenue, which missed estimates by $90 million.

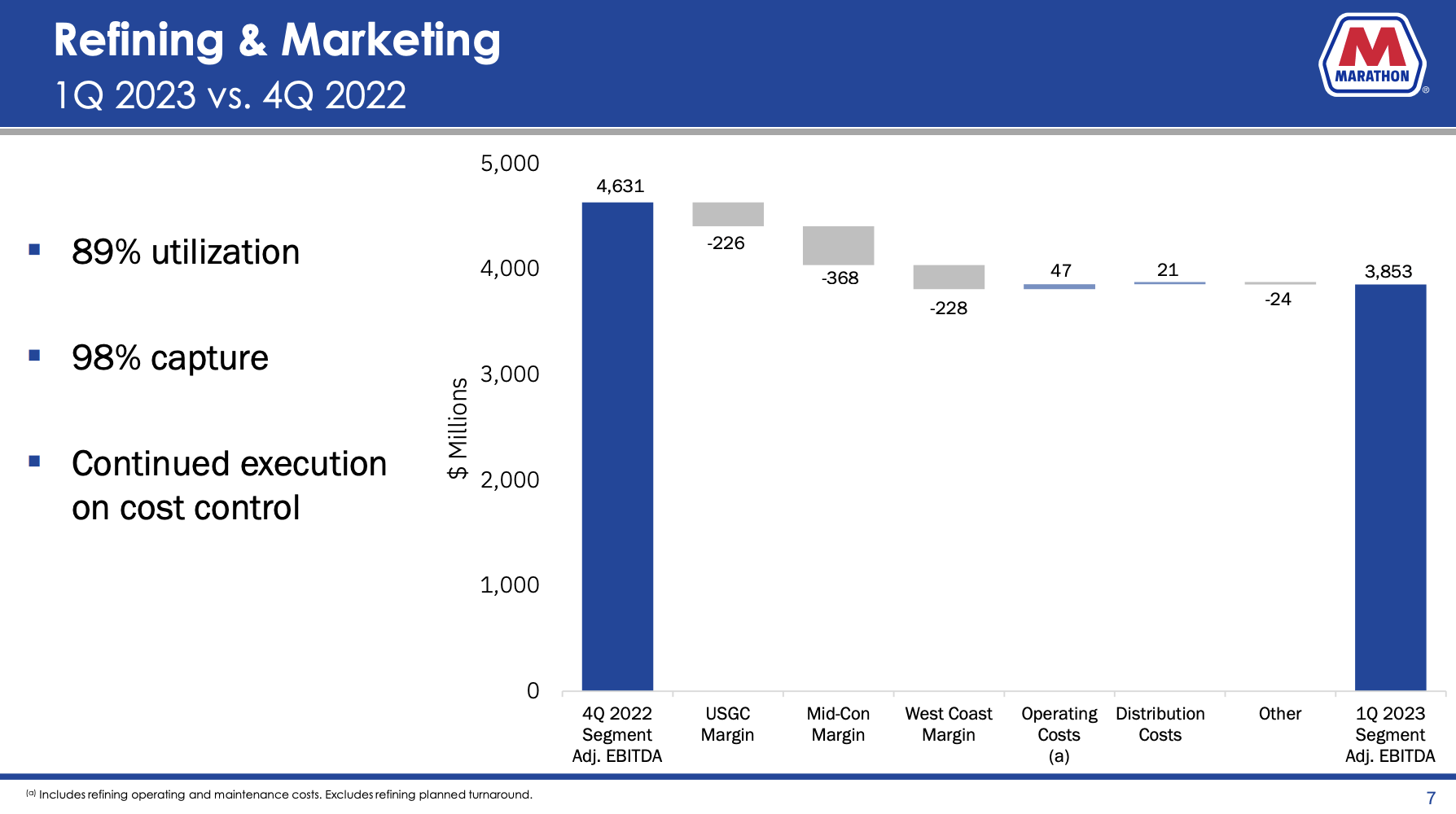

This was caused by the Refining & Marketing segment facing challenges in the first quarter.

Winter Storm Elliot and planned maintenance activities impacted several refineries, resulting in a 3 million barrel reduction in crude throughput and a 5% decrease in refining utilization to 89%.

Refining margins per barrel were lower sequentially in all regions compared to the previous quarter.

However, the segment's commercial team achieved a capture rate of 98%, and refining operating costs per barrel remained relatively flat at $5.68. Operating costs per barrel were expected to decrease in the second quarter.

{kind=link}

Marathon Petroleum

MPC also has midstream operations, as it owns the majority of MPLX LP ( MPLX ), the company which operates its pipelines. I recently covered MPLX from a dividend investor's point of view.

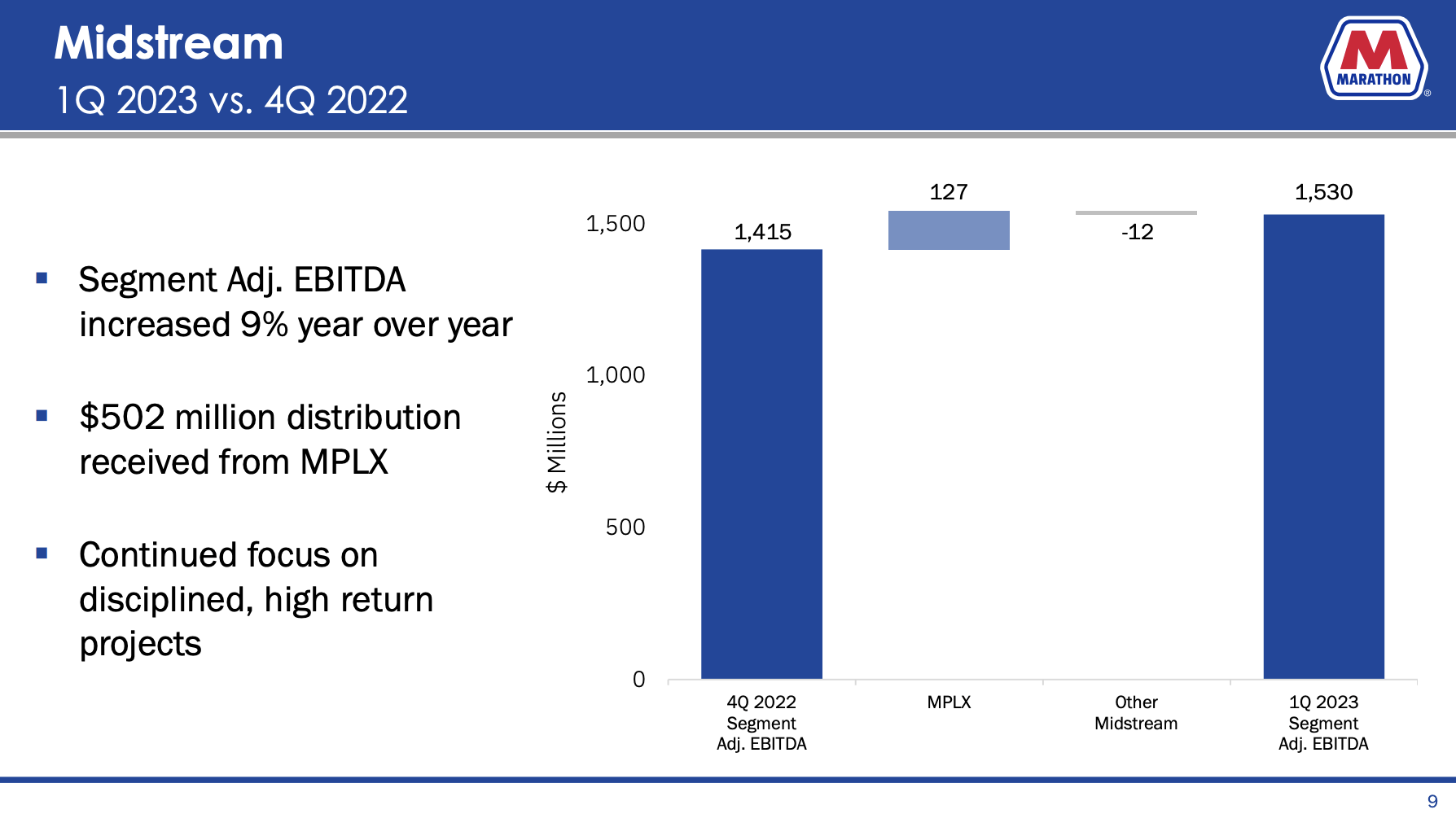

This Midstream segment delivered resilient results in the first quarter, with a 9% year-over-year increase in adjusted EBITDA, reflecting solid demand growth.

The company is focused on investments in high-return projects in the Marcellus, Permian, and Bakken basins, which I expect to benefit from long-term production growth - albeit at slowing growth rates.

The Midstream business generated strong cash flows, contributing $502 million in cash flow to MPC through MPLX distributions.

{kind=link}

Marathon Petroleum

According to MPC, its stake in MPLX provides durable earnings and serves as a differentiator for MPC compared to peers without Midstream businesses.

Furthermore, the company expanded its business.

During the first quarter, MPC made progress on value-creating projects. At the Galveston Bay facility, the STAR project was completed. Instead of expanding the GBR cokers, MPC upgraded the resid hydrocracker unit to enhance conversion and liquid volume yield.

Fractionation modifications increased diesel recovery, allowing the refinery to process more discounted heavy crude.

The STAR project is expected to add 40,000 barrels per day of incremental crude capacity and 17,000 barrels per day of resid processing capacity. Start-up activities are progressing, with ramp-up anticipated throughout the second quarter of 2023.

Needless to say, the project's profitability will depend on the spread between heavy crude and untreated diesel over the incremental crude capacity.

At the Martinez renewable fuels facility, MPC achieved a full Phase I production capacity of 260 million gallons per year of renewable fuels as planned.

Construction activities for Phase II are on schedule, and pretreatment capabilities are expected to come online in the second half of 2023.

This will enable the facility to reach its full expected capacity of 730 million gallons per year by the end of 2023.

{kind=link}

Marathon Petroleum

Adding to that, the company had favorable guidance.

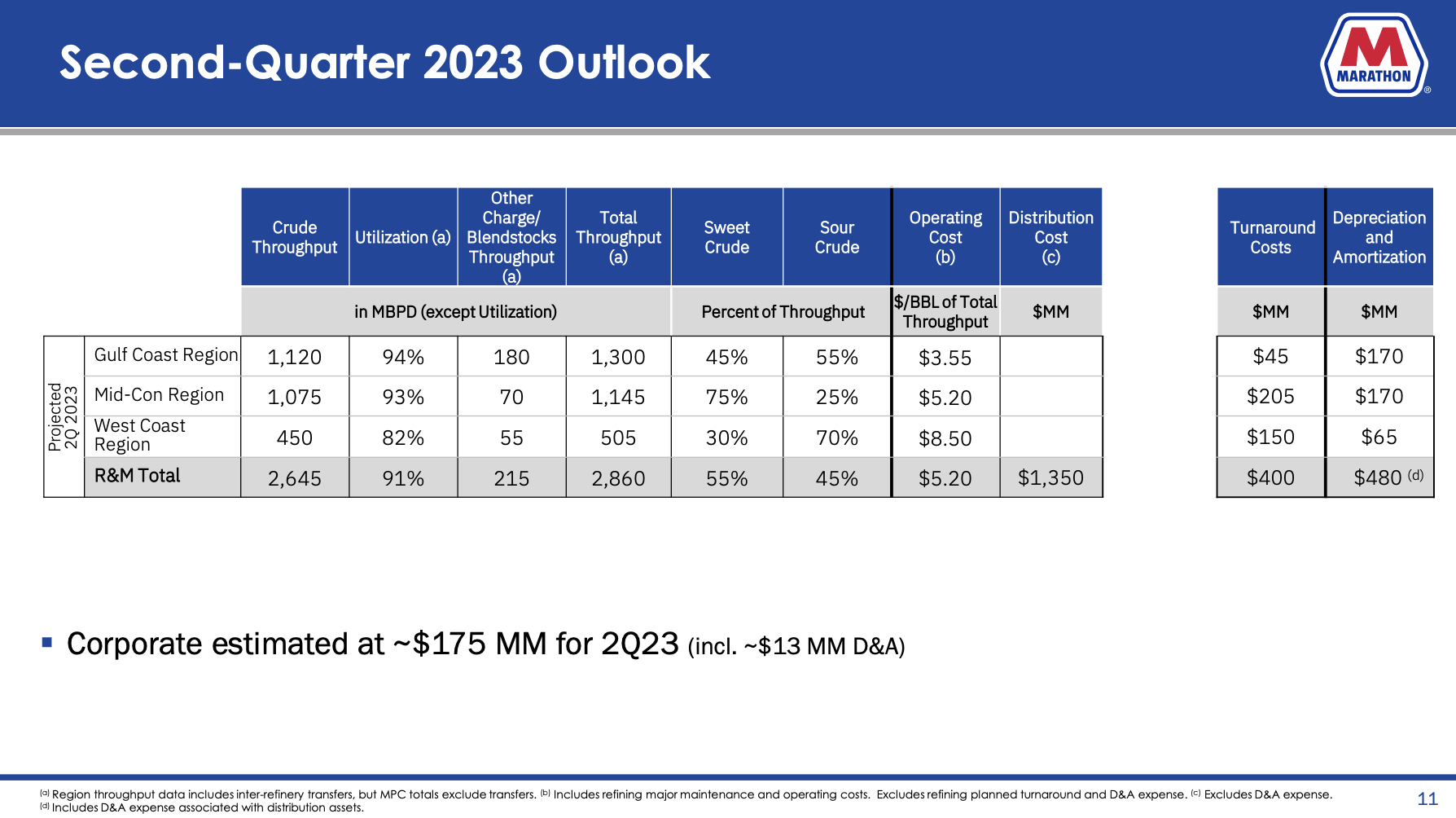

- For the second quarter, MPC expects crude throughput volumes of roughly 2.6 million barrels per day, which translates to a utilization rate of 91%.

- Operating cost per barrel is expected to decrease to $5.20, benefiting from higher throughput and lower energy costs.

- MPC anticipates a decline in operating cost per barrel towards a normalized level of $5 per barrel as turnaround and project activity is completed.

Where's The Shareholder Value?

MPC rewards investors through both dividends and buybacks.

The company currently yields 2.7%, which comes with a payout ratio of (currently) less than 10% and 10.5% average annual dividend growth over the past five years.

In November 2022, the company hiked its dividend by 29.3% to adjust the dividend to stronger post-pandemic earnings and cash flow.

Since the spin-off from Marathon Oil ( MRO ) in 2011, the MPC dividend hasn't been cut. Not even during the pandemic, when the company used debt to protect its dividend.

In the first quarter, MPC reported an operating cash flow of nearly $4.2 billion, excluding changes in working capital. Working capital was a $98 million headwind primarily driven by increases in crude and product inventory.

Capital expenditures and investments amounted to $664 million.

MPC returned over $3.5 billion to shareholders through share repurchases and dividends, representing an 85% payout of operating cash flow. The company has $9 billion remaining under its current share repurchase authorization and $11.5 billion in cash and short-term investments.

Over the past three years, the company has bought back more than a third of its shares, which added to the strong performance of its stock price, as buybacks support per-share earnings and similar metrics.

Furthermore, the company has a 1.2x 2023E net leverage ratio, which underlines its financial health. Since the pandemic, the company has significantly lowered net debt. This includes the sale of its Speedway assets in 2021.

The company enjoys a BBB credit rating.

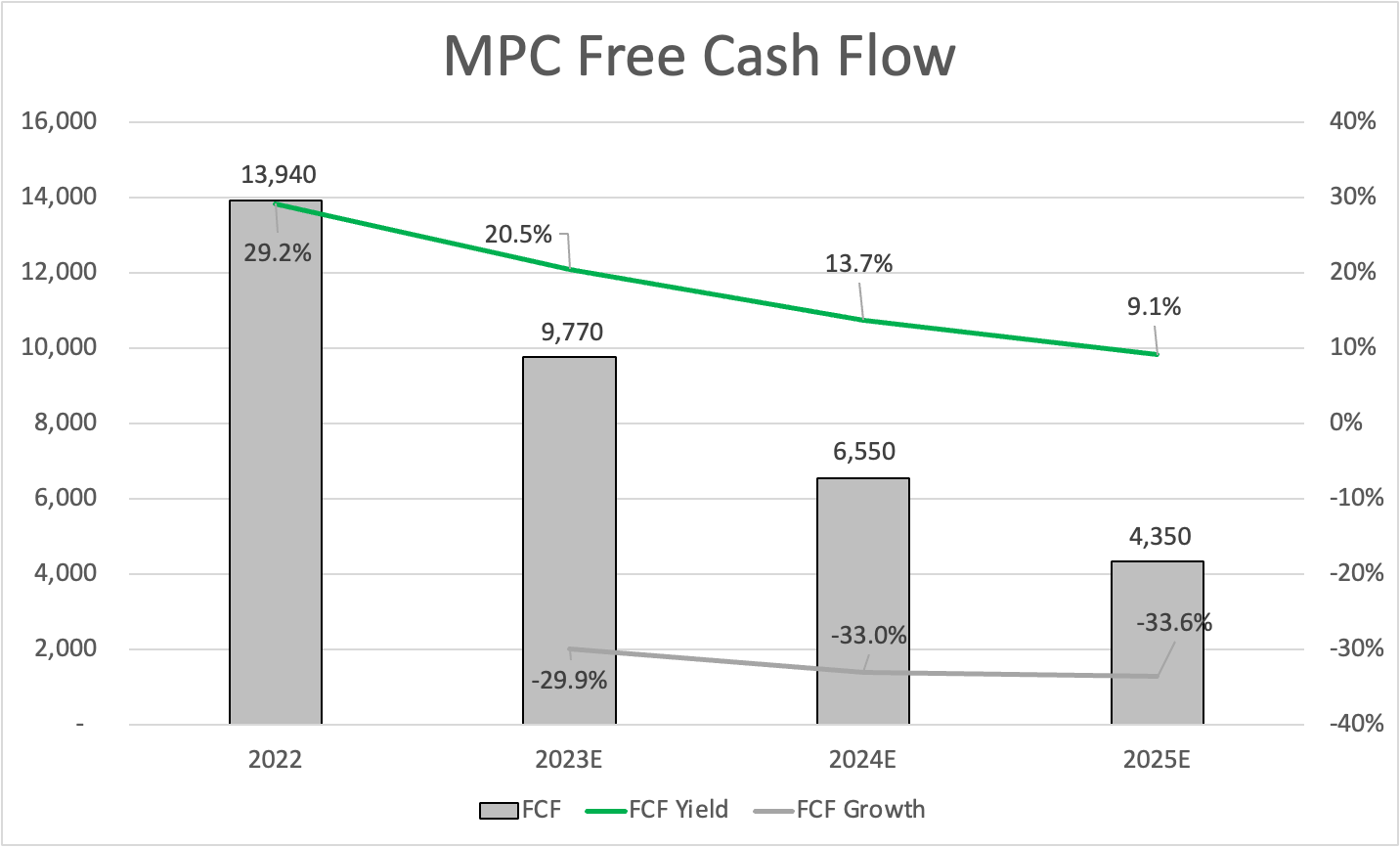

With that said, looking at the chart below, we see that analysts expect the company's free cash flow to normalize in the years ahead. This isn't because of bad economic news but because of normalizing margins as new supply comes online. While I believe that the 2024 and 2025 numbers could be stronger than expected, we're still dealing with a 9% implied free cash flow yield using 2025 estimates. This indicates a dividend payout ratio of just 38%.

Prior to the pandemic, the company's free cash flow usually came in below $3 billion.

{kind=link}

Leo Nelissen

In other words, the company is in a fantastic spot to boost distributions on a prolonged basis.

We will invest in sustaining our asset base while paying a secure competitive dividend with the potential for growth. We want to grow the company's earnings and we will exercise strict capital discipline beyond these three priorities we are committed to returning excess capital through share repurchases to meaningfully lower our share count. - Maryann Mannen , MPC EVP & CFO

Given that the company prioritizes buybacks over dividends, I believe that MPC will continue to be the best-performing refinery stock for the time being.

With that said, the valuation is fair. The company is trading at 7.3x 2024E free cash flow, which incorporates a 33% free cash flow decline versus 2023.

Prior to the pandemic, shares usually traded close to 12x free cash flow, which is fair.

In other words, if we incorporate a free cash flow decline to $4 billion, we get a fair valuation at MPC's current stock price.

Just one billion more in revenue would indicate a 25% upside.

The current consensus price target is $143, which is 30% above the current price. I agree with that.

However, MPC shares are under pressure.

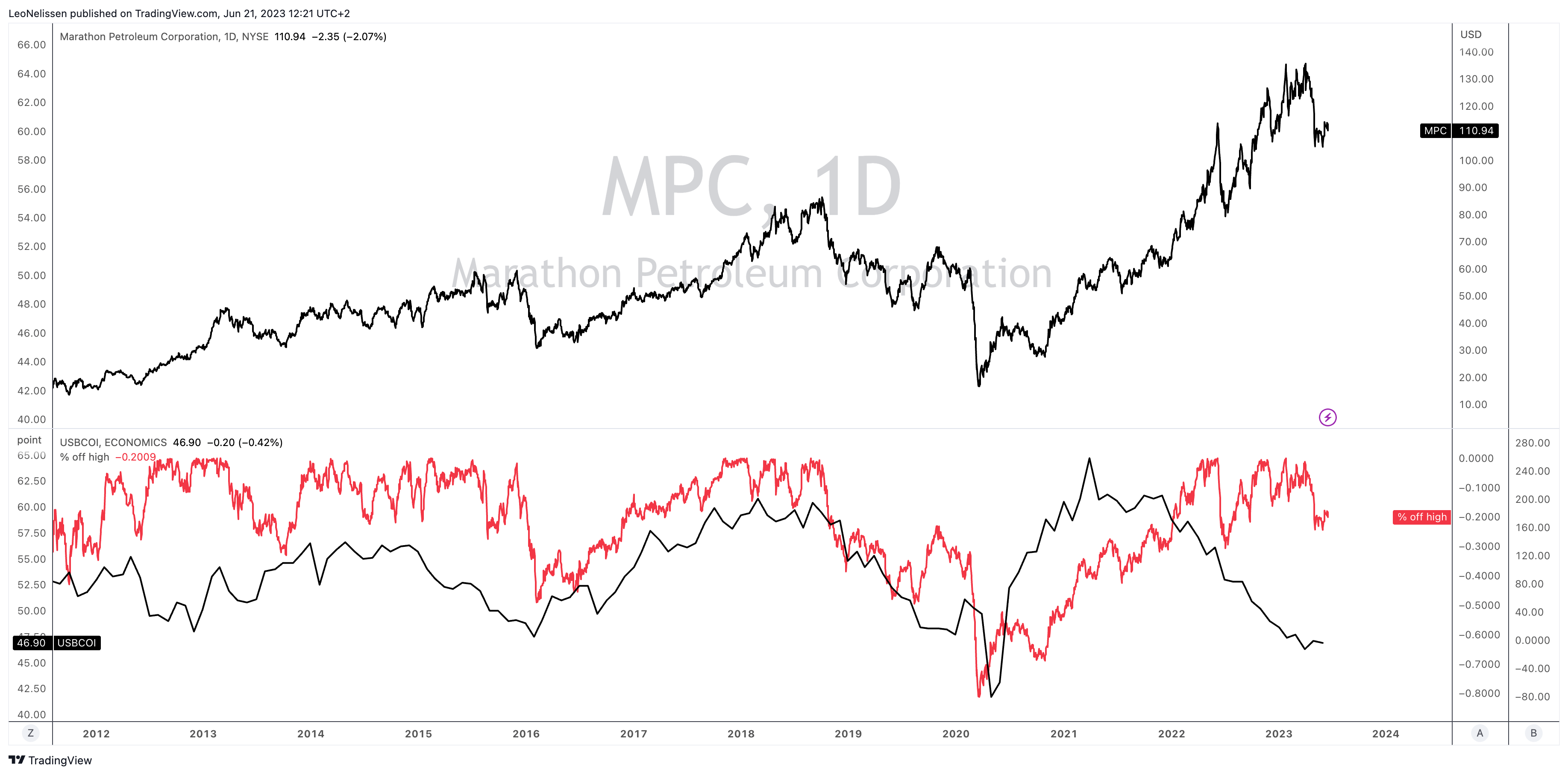

The chart below compares the MPC stock price (% below their all-time high) to the ISM Manufacturing Index (the black line in the lower part of the chart).

{kind=link}

TradingView (MPC, ISM Index)

Usually, when the ISM index is this low, MPC shares are at least 40% below their all-time high.

This time, however, they continue to enjoy secular tailwinds that didn't exist in prior downturns.

So, unless something breaks in the economy, I wouldn't bet on a sudden 20% decline in MPC shares.

With that said, if I were in the market for high-quality downstream exposure, I would be a gradual buyer of MPC shares. I would break up my initial investment and gradually buy shares over time. If shares dip, investors can average down. If the stock price suddenly takes off (I don't expect that to happen), investors will have a foot in the door.

Hence, for the time being, I remain neutral and urge investors to be careful, as refinery stocks tend to be highly cyclical and volatile. They are not as safe as the dividend aristocrats you may have in your portfolio.

Pros & Cons

Pros:

- Strong financial performance and resilient results.

- Secular tailwinds in the refining industry.

- Diversification through midstream operations.

- Shareholder-friendly with consistent dividends and significant share buybacks.

- Potential for growth with ongoing expansion projects.

Cons:

- Cyclical and volatile nature of refinery stocks.

- Market and economic risks.

Takeaway

Marathon Petroleum presents a compelling opportunity for long-term investors seeking downstream energy exposure. Despite the recent decline in stock price, MPC is a well-run business with the potential to generate significant shareholder value.

The refining industry is experiencing a secular tailwind due to subdued supply growth, leading to elevated prices for refined products.

MPC's strong financial performance, including resilient results in the first quarter and a focus on high-return projects, positions it well for future growth.

The company rewards investors through dividends and buybacks, with a track record of consistent payouts.

While refinery stocks can be cyclical and volatile, gradual buying of MPC shares could be a prudent strategy for those seeking high-quality midstream exposure.

Hence, for the time being, I'll maintain a neutral rating. Given the risk/reward, I will update my rating if MPC drops by 10% to 15% or if economic demand shows signs of an upswing.

For now, I stick to buying on weakness.

For further details see:

What To Make Of Marathon Petroleum's Dividend