AQUA - What To Make Of Xylem's Evoqua Acquisition

Summary

- Xylem just announced they have agreed to acquire Evoqua, offering 0.48 shares of Xylem per Evoqua share.

- Management expects the transaction to generate scale benefits, and to result in ~$140 million in synergies.

- We believe both companies were overvalued prior to the transaction, and a ~12% EBITDA improvement from synergies does very little to reduce an overly stretched valuation.

Xylem ( XYL ) recently announced that they have agreed to acquire Evoqua ( AQUA ) in a $7.5 billion transaction. While this purchase would give Xylem access to Evoqua's strong portfolio of water and wastewater treatment solutions, which complement Xylem's existing offerings, we believe the company is overpaying significantly. That seems to be the way the market is interpreting it too, as shares of Evoqua moved higher after the announcement, as would be expected, but what is more surprising is how much Xylem's shares dropped after the news. Clearly the market believes that Xylem's shareholders are getting a bad deal, and we agree.

There are, however, some synergy opportunities as the two companies have compatible cultures and complementary operations. The way management is describing the rational is that this would create the "most advanced water solutions and services business at scale".

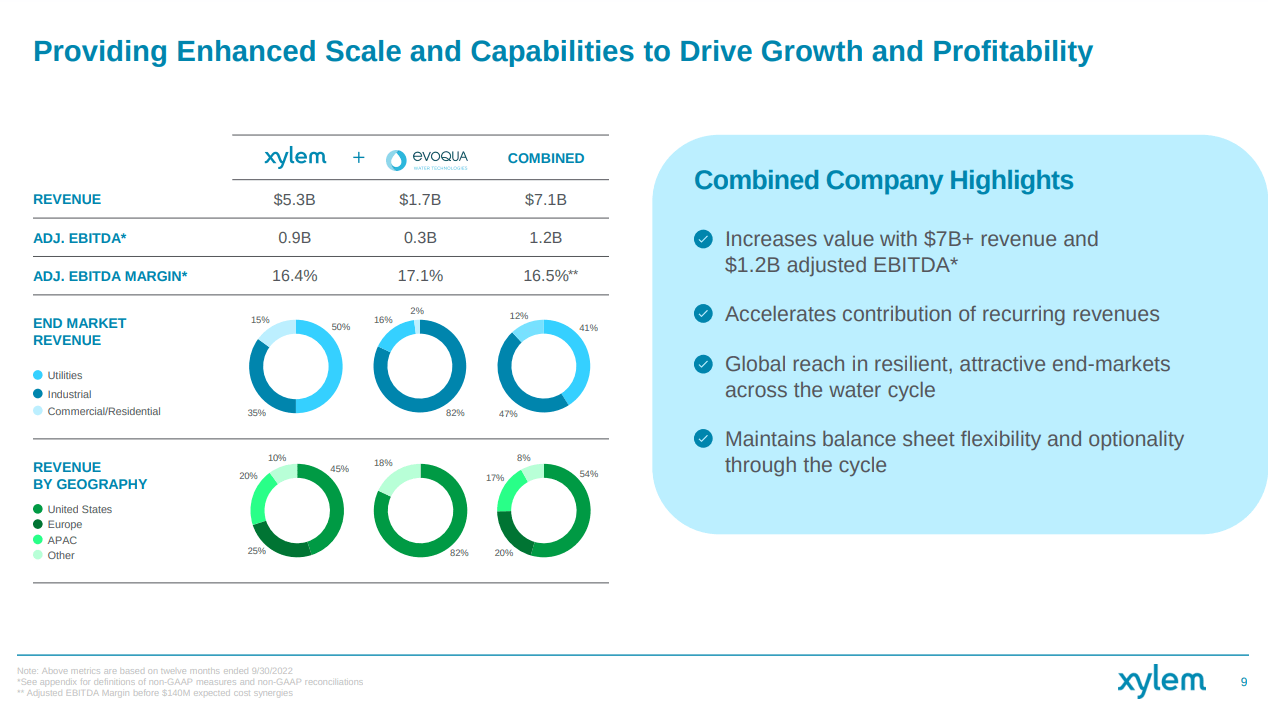

The combined company

Management expects $140M of expected run-rate cost synergies within three years, from things like enhanced purchasing power, logistics and freight savings, optimization of their office and branch footprint, increased utilization of their manufacturing facilities, reduced public company costs, etc. The slide below shows how the revenue by end market and by geography would look like for the combined company. Importantly, the company would have ~$7.1 billion in annual revenue and ~$1.2 billion in adjusted EBITDA before synergies. Synergies should add ~12% to the total adjusted EBITDA once realized.

{kind=link}

In terms of revenue growth, Evoqua was growing a little bit faster at ~7% on average compared to a ~4% average for Xylem. The combined company should be expected to grow somewhere in the middle. While Xylem has a bigger weighting, there could be some revenue synergies that might be realized.

Transaction details

At least Xylem is using its own overvalued shares as currency for the acquisition, as this is an all-stock transaction at a 0.480 exchange ratio. This means that Evoqua shareholders should receive 0.48 shares of Xylem for every share of Evoqua they own. Evoqua shareholders are expected to own approximately 25% of the combined company.

With Xylem shares currently at $101.42, this would value Evoqua shares at $48.68. They are currently at 47.28, meaning there is still a ~3% spread that arbitrageurs could target. The fact that the spread is so low means the market believes the transaction has a high likelihood of being completed. The acquisition is expected to close mid-2023, and is subject to approval from shareholders of both companies, as well as required regulatory approvals and other customary closing conditions.

Balance Sheets

The fact that it is an all-stock transaction means that at least Xylem will not over-leverage its balance sheet. This is important because Xylem was already carrying ~$2.3 billion in debt, and Evoqua ~$880 million that Xylem will now assume. Both companies have a similar financial debt to EBITDA ratio of ~3.6x, which means that if they meet the synergy targets their leverage could actually end up lower.

Valuation

We believe this transaction changes very little the reality that both companies were overvalued before the acquisition, and look overvalued even assuming EBITDA grows ~12% thanks to synergies. We therefore believe at current prices both companies are a 'Sell', as the synergies and revenue growth rates don't justify such stretched valuation multiples.

We agree with Seeking Alpha, which gives Xylem an 'F' valuation grade. The only metric where it doesn't do that bad is the dividend yield, and even then we would argue that a ~1.18% yield is nothing to get too excited about.

Seeking Alpha

Risks

There are two main risks that we believe both Evoqua and Xylem shareholders should consider in regards to the merged company. One is the integration risk, as mergers can sometimes be messy, and there are times when there are dis-synergies in addition to synergies, especially when company cultures clash.

The bigger risk, however, we believe is the extremely stretched valuation, even assuming a 12% increase in EBITDA from synergies.

Conclusion

We believe both Evoqua and Xylem are well run companies, operating in an attractive industry, and doing very important work for society. We have covered them previously, and we usually found them to be overvalued. While this transaction is expected to create some synergies, they do very little to bring down the extremely stretched valuation. We believe the risk/reward for shareholders is very poor, and are therefore rating both as 'Sell'.

For further details see:

What To Make Of Xylem's Evoqua Acquisition