ROK - Where Fundamentals Meet Technicals: Cautious Of The AI Craze

2023-06-05 16:54:30 ET

Summary

- The article discusses the potential overvaluation of AI-related stocks, specifically Microsoft and Rockwell Automation, despite their solid fundamentals.

- It highlights the importance of considering the cost of capital and risk-adjusted return outlook when evaluating stocks in the current market environment.

- Investors should be cautious with tech stocks like Microsoft and Rockwell Automation, as their forward expected returns may be limited at current valuation levels.

Fundamental analysis can give us a good idea if a stock is likely to do well over a 5-year period.

Technical analysis and various measures of liquidity and sentiment, meanwhile, can point towards things being overly stretched to one side or the other, and due for a rebound in the more tactical sense.

For Stock Waves , I provide occasional short-form highlights for where both fundamental analysis (my focus) and technical analysis (by Zac Mannes and Garrett Patten) suggest that the probabilities are in the favor of a stock to move one way or another. Some of them, like this one, I make public.

This issue takes a look at two stocks that have some potential storm clouds on the horizon.

{kind=link}

The AI Craze

Artificial intelligence has existed for decades, but over the past six months, it has been having a big moment.

People imagine technology to be an exponential growth trend, but really it's more of a stepwise trend. We stagnate for periods of time, find a breakthrough, experience an exponential growth period, hit a ceiling, and then stagnate for a while again. That's the cycle we tend to go through.

For example, humans spent thousands of years wanting to fly with practically no progress. Then in the late 1700s, we invented the hot air balloon and then the airship and played with those for a century and a half with middling success. But ultimately, it was the combination of discovering petroleum, making engines, and processing aluminum, that made true flight possible.

Once we put those pieces together, we went from the Wright Brothers' first powered flight to the Apollo 11 moon landing within the span of one human lifetime (1903-1966; just 66 years). It was an absolutely explosive period for aerospace innovation. But then we stagnated. In 1969, we had the first flight of the Concorde supersonic commercial airplane, and today we don't even have that anymore for various technical and economic reasons that we couldn't overcome. Our maximum flight speeds and ease of space travel have generally flat lined, outside of some niche military use cases.

AI seems to be going in a similar "stagnant and then exponential" trajectory. For decades, it was "neat" and gave us marginal gains in various areas. But finally, with enough processing power and computer science breakthroughs, it has reached the point of being broadly applicable.

Generally speaking, AI can automate all sorts of tedious things, and will likely get better at it over the next several years. The creation of art, videos, music, code, and engineering designs can be made easier with text-based generative content. And it's recursive; AI can review code and make programming easier, which accelerates software development, including AI software.

So, I think the impact from AI will be real and long-lasting. AI wrote the summary bullet points at the top of this article (with one small edit to the third one) and did a better job than I would have done on them.

However, that doesn't mean we can pay any price for AI-related stocks. Just like how the development of the internet in the 1990s was real and long-lasting, it didn't mean that dot-com stocks could be bought at any price. Many of them, including internet backbone companies like Cisco ( CSCO ) became wildly overvalued and had to spend a long time growing into their valuation even as the internet continued to take off in terms of adoption.

Here are some examples that have gotten ahead of themselves.

Microsoft

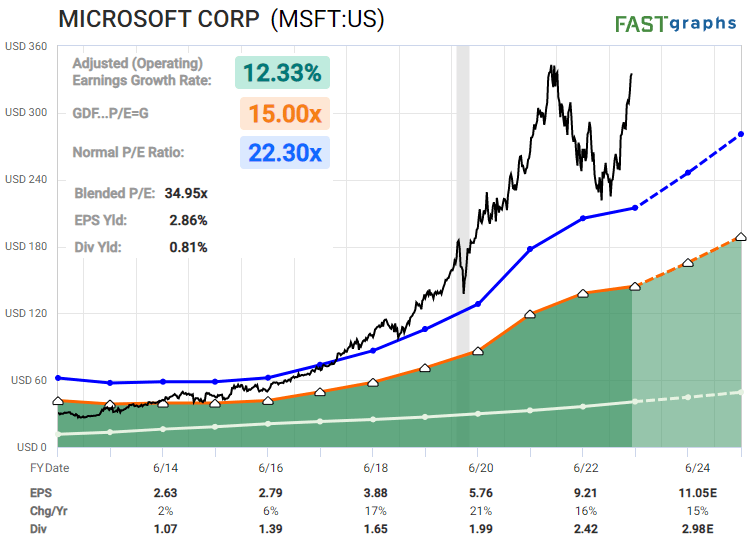

Microsoft ( MSFT ) is one of the biggest, most profitable, widest-moat, and most ubiquitous companies in the world. It's one of only two corporations with a perfect AAA credit rating, which ironically according to S&P Global Ratings implies they are slightly less likely to default on their creditors than the U.S. federal government is over any given period.

In 2023, it has also become rather expensive again. The stock trades at 30x forward earnings despite already being a $2.5 trillion company.

{kind=link}

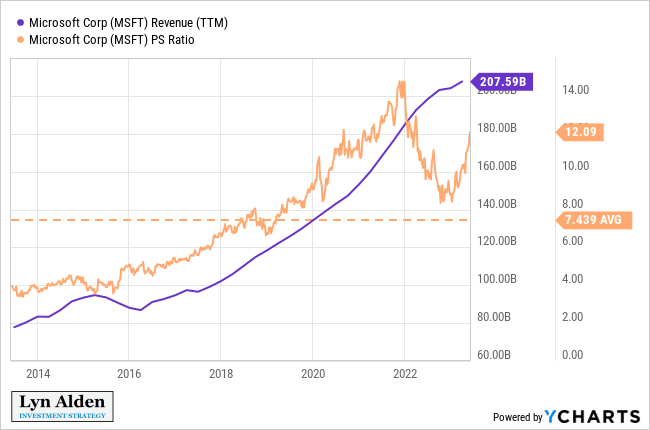

The price/sales ratio is currently back over 12x, compared to the 10-year average of less than 7.5x:

{kind=link}

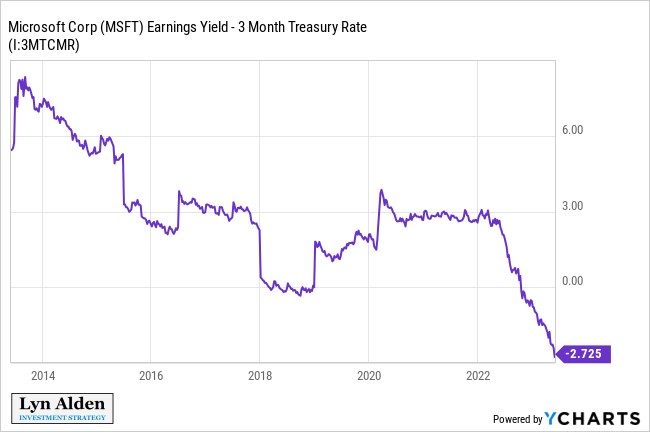

This is despite the fact that the cost of capital is way higher today than at any other time during that 10-year period. In other words, the opportunity cost for owning any particular equity is higher now; investors can get over 5% nominal gains on money markets and T-bills now, rather than the near-zero yield they would have gotten during most of this period.

An earnings yield is a company's earnings per share divided by its share price (the inverse of a price/earnings ratio). If we take Microsoft's earnings yield and subtract the 3-month Treasury yield from it and chart that spread over time, then Microsoft's rate-adjusted earnings yield is currently at a rather low level:

{kind=link}

Going forward, I don't necessarily expect tech stocks to crash and go straight down like they did in 2022. They might just chop along in a range for a long time as earnings catch up. There are a number of different variables that can affect this.

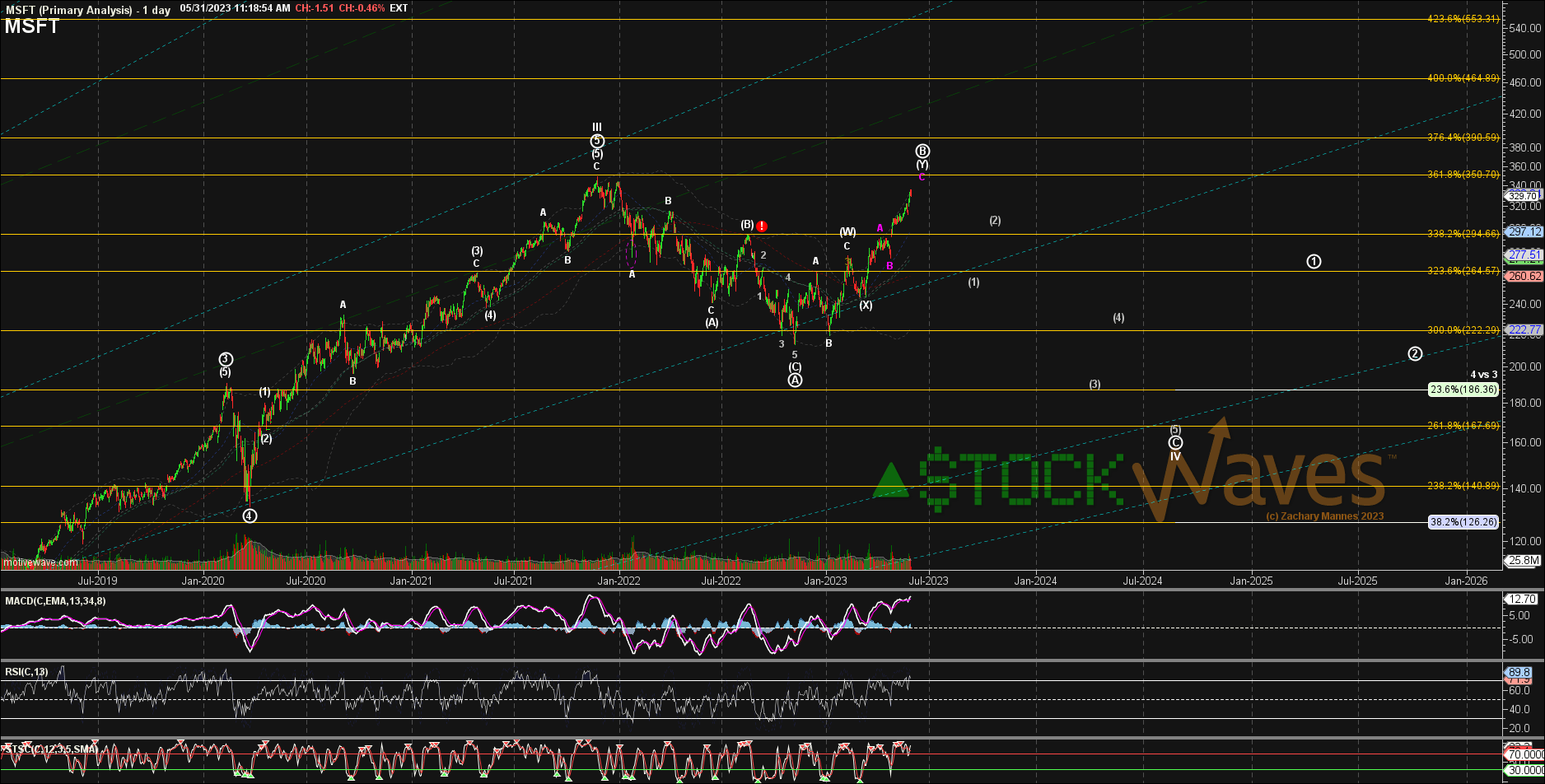

My colleague Zac has a negative technical outlook for the stock:

{kind=link}

Overall, I'd just be cautious when it comes to mapping out the forward expected returns of tech stocks like Microsoft from these levels, despite the fact that many of them are solid companies. I wouldn't chase many of them here.

Rockwell Automation

Rockwell Automation ( ROK ) is a leading producer of industrial automation products. In terms of both hardware and software, they help manufacturing companies automate their production.

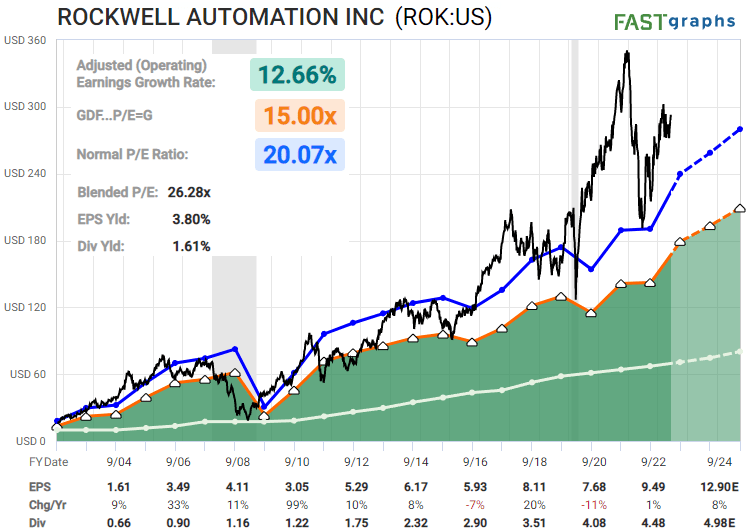

Naturally, continued automation is the future, and AI should make it even better. But that doesn't mean the stock can't get ahead of itself. Much like Microsoft, Rockwell became very overextended in 2020 and 2021, and had a big correction in 2022. And now in 2023, it's expensive again.

{kind=link}

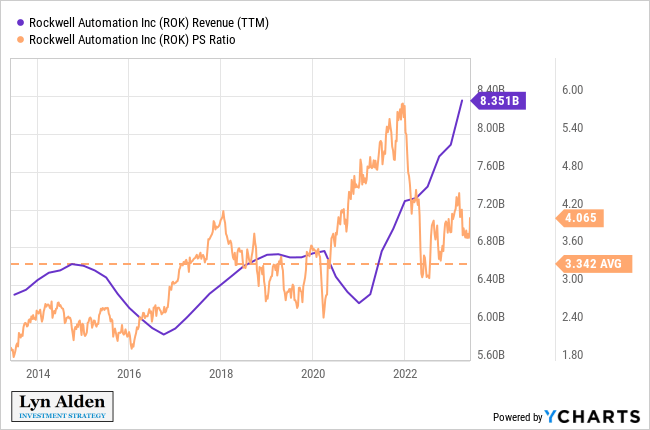

Being partially hardware-focused, Rockwell's price/sales ratio is more reasonable than Microsoft's. However, it's still above the 10-year average, despite the fact that the cost of capital is now at record highs relative to the rest of this period:

{kind=link}

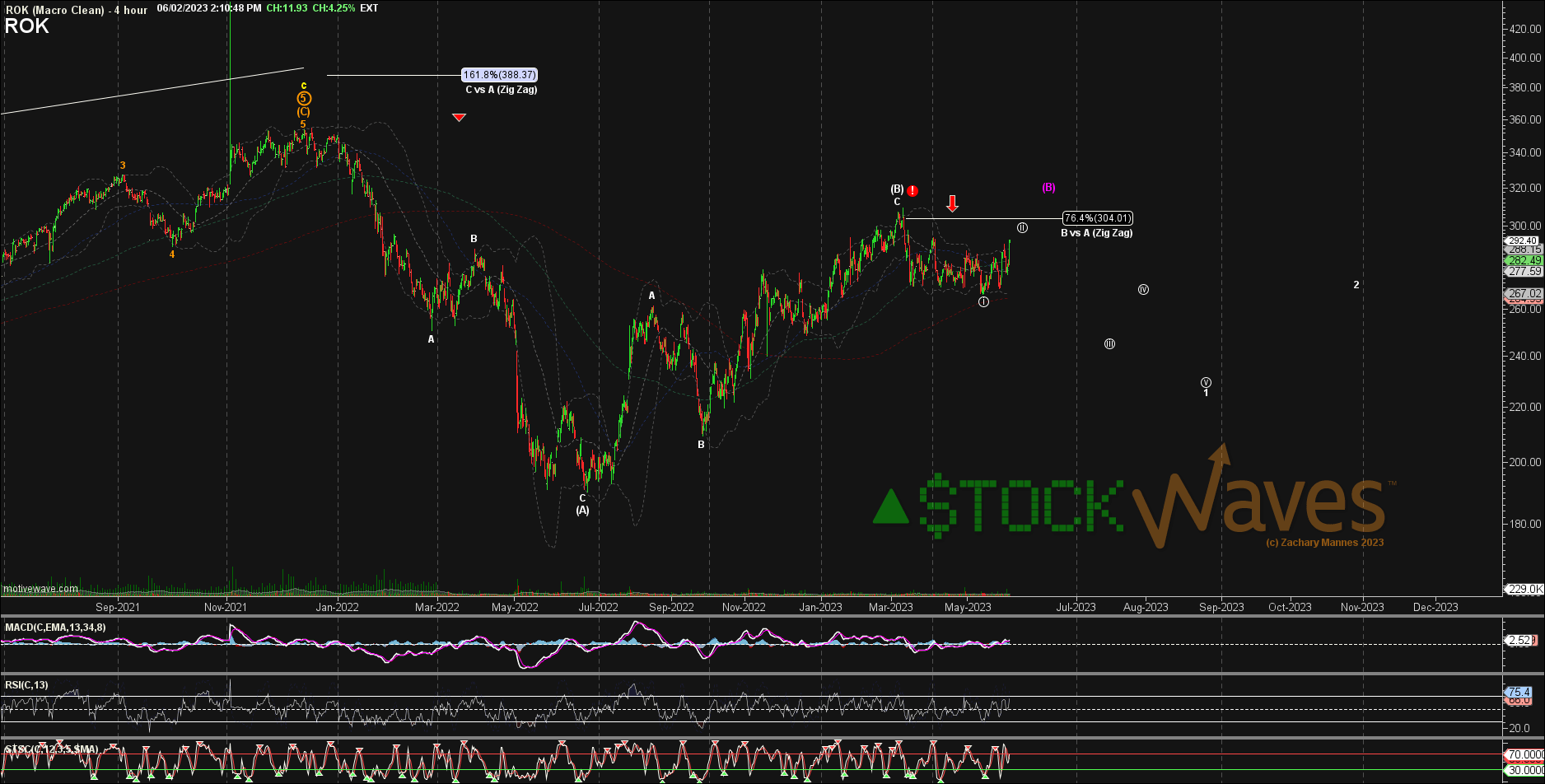

Zac's technical analysis expects some weakness in the year ahead:

{kind=link}

Would I short Rockwell? No. It's a good company, and I expect their fundamentals to be better five years and ten years from now. But it's not a bargain at these levels, especially given the yield that investors can get on cash equivalents in this environment. The risk-adjusted return outlook appears to be pretty unattractive over the next few years from these levels.

That doesn't mean it can't surprise to the upside, but there are likely better alternatives out there until Rockwell settles at a more attractive valuation.

For further details see:

Where Fundamentals Meet Technicals: Cautious Of The AI Craze