PTA - Which Type Of Income Investor Are You? And Why It Matters

2023-07-19 13:54:24 ET

Summary

- We take a look at four different income investment styles.

- These include momentum, value, yield-maximization and macro.

- Our view is that the value style which combines informed analysis combined with an eye for valuation is the style most likely to outperform over the longer term.

In this article we take a look at a number of different income investing "styles." By style we just mean the kind of mental process which drives allocation decisions. We also take a look at potential problems of each style and apply the styles to a case study of preferred closed-end funds, or CEFs.

The Different Income Investing Styles

In our view there are broadly four different key income investing styles.

The first one is what we call a momentum style which is a style that is, arguably, the most common one for stock retail investors. Investors who use this style tend to like buying whatever is going up and like to sell whatever is going down. In other words, they gain conviction about positions via the market itself. If something is going up, it's because it's an attractive asset and people like it and if it's going down that's because it's not an attractive asset.

The second style or the value style often works in reverse of the momentum style. Investors who follow this style like to buy when prices are falling and vice-versa. Although the two styles look similar as they both respond to price changes, there is often a very important difference between them which is often overlooked.

While momentum investors derive all or nearly all of their conviction from the price move, value investors derive their conviction from a more fundamental analysis of the security. This analysis allows them to override the fear and go against the "natural instinct" of selling when prices fall. It is also what allows them to sell when prices rise since they are able to compare the price at any one time to the fundamental value of the security.

A yield-maximizing style is not focused on price changes, but rather on today's yield on offer. Investors who follow this style have a yield floor below which they are just not that interested. These investors like to keep the yields of their holdings stable or rising and will rotate to higher-yielding assets when the yields of their holdings drop due to either price appreciation or distribution cuts.

Finally, a macro style is one where allocations are based on expectations about the state of the economy. For instance, investors who are worried about a potential recession would tilt to cash and vice-versa.

It's fair to say that many investors use a combination of these styles however in many cases there is a dominant style at play.

Income Style Problems

There is no perfect investment style and each style has potential drawbacks. In our view, the momentum style, while possibly well-suited to trending assets like stocks, is not well-suited to mean-reverting assets like fixed-income. Very often, a momentum style will buy high and sell low, locking in repeated losses in portfolios, resulting in poor longer-term returns.

A value style also has potential drawbacks which could be a lack of diversification and a stubbornness to mark the analysis to market. It can be difficult to have a firm analytical foundation for 20-30 positions given the usual time constraints for individual investors.

An investor with firm conviction may just hold a handful of positions, resulting in poor diversification. An investor who has done their own homework may also be unwilling to admit they made a mistake and their analysis was wrong. This could push them to double down on a losing position that has not worked out, leading to emotion-driven trading.

The yield-maximizing style has a number of drawbacks. One is that investors often mistake the distribution rate of a given security for its ability to generate a similar of amount of cashflow internally. This can often lead to disappointment as investors realize that a 15%-yielding asset has actually delivered only a 3-4% total return over a given period. Another problem is that assets with relatively high yields, particularly CEFs, are those that have been slow to adjust their distribution rates. This causes investors to flock to them, pushing up their premiums which then collapses after the fund right-sizes the distribution. Duff & Phelps Utility and Infrastructure Fund (DPG) is a recent example of this dynamic.

Another problem is that higher-yielding assets tend to also be higher-volatility assets. This can result in a loss of conviction at the worst possible time - when asset prices have taken a big tumble. Some investors will often sell near the bottom only to buy back once prices have rallied. Another issue is that investors add risk when prices rise by rotating into higher yielding securities. In effect, this means they take the most amount of risk at the top of the cycle with predictable negative effects on their portfolios.

The main problem with a macro forecast style is that few if any investors are actually good at macro timing. For instance, many investors have been expecting a recession to hit for well over a year now and yet the macro picture remains robust, if slowing down. Two, a recession is not a binary event - there is a world of difference between a tough recession or a hard landing and a mild one or a fairly soft landing. These two recession types can often lead to very different market outcomes. Investors following this style are often overly cautious and will pay the opportunity cost of being out of the market for long periods of time.

Preferred CEFs Case Study

In this section we take a look at Preferred CEFs as a concrete example of how these styles can differ. The point isn't to definitively prove one style superior to another but rather to provide an example of how they can work in practice.

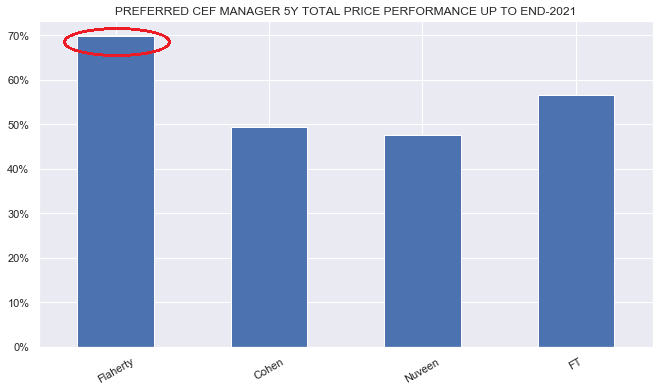

The Flaherty suite of preferreds is a good one to use here. These funds, particularly the Flaherty & Crumrine Preferred and Income Securities Fund ( FFC ) used to be viewed as the best funds in the sector. The chart below which shows performance by CEF manager in the sector for 5 years through the end of 2021 shows why it was "obvious" that the Flaherty preferred CEFs were the best.

{kind=link}

This is a good example of the momentum style in action. This stronger price return was a function of both a stronger total NAV return and stronger discount performance.

The intuition here is that if all preferred CEFs are more or less the same, then the best-performing ones are just better. Exactly what "better" means is not always clear in this style but it's often chalked up to ineffable management nous.

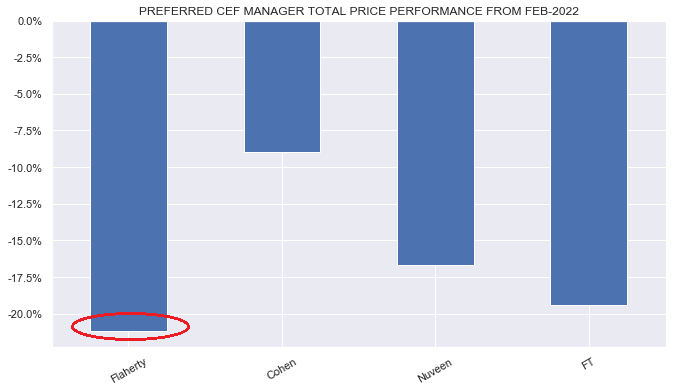

In February of 2022 we had an article which highlighted FFC in the context of the Flaherty suite and warned that because the fund did not hedge its interest rate profile, unlike the rest of the sector, it was likely to struggle in terms of both net income and total return. We also saw that the Cohen CEFs which did have hedges on also tended to trade at wider discounts. The combination of an understanding of the structural underpinnings of the sector along with an attractive value proposition is a good example of the value style in action.

This is what the total price return looks like from the date of the article to today. Clearly, whatever magic the Flaherty managers had vanished in a puff of smoke.

{kind=link}

This example highlights the inherent problem of the momentum style which is that it can't explain the drivers of performance. And while the various drivers of performance are not always obvious, it can pay to look for them.

In the case of the Flaherty suite these performance drivers were not particularly mysterious - a topic we have discussed since 2020. There is a key structural difference between Flaherty CEFs and the rest of the suite which is that the Flaherty CEFs choose not to hedge their duration profile and hedge costs. When short-term rates were low and interest rates were stable or falling, the Flaherty funds benefited as they faced no drag from the hedges. And when interest rates rose across the curve, they underperformed.

This is also why we initiated a position in the Cohen preferred CEFs in our Income Portfolios at the end of 2021 as it became clear that this suite of preferred CEFs would hold up much better in a rising rate environment.

Not only have Cohen CEFs outperformed but their distributions have held up much better. While two of the three Cohen funds had a single distribution cut recently, Cohen & Steers Tax-Advantaged Preferred Securities & Income (PTA) (our initial allocation and the fund we held for most of the time) managed a raise in the past year while the Flaherty funds had 7 cuts.

Systematic Income

It seems that the market is finally catching on to this dynamic and the Cohen funds are, unusually, trading at tighter discounts than the Flaherty funds.

Systematic Income

Part of the reason for this significant cheapening of the Flaherty funds was their underperformance in a period of rising rates. However, another motivating factor is clearly the combination of distribution cuts and relatively modest yields. The chart below shows that the Flaherty current yields are below the sector average. This relative shift in discounts could be an example of the yield-maximizing style as investors are dumping the Flaherty funds for other higher-yielding options.

Systematic Income

The pendulum is clearly swinging the other way now. If the Fed starts to cut rates while the Flaherty funds remain at wider discounts, the value style would suggest a rotation to the Flaherty suite. Their lack of duration and leverage cost hedges would shift from a liability to an asset in a rate-cutting environment.

Takeaways

Our view is that informed analysis combined with a keen eye for valuation is the income investment style that is most likely to deliver stronger performance over the longer-term. While this value style is not without potential problems, its problems are easier to mitigate than the more fundamental problems of other investment styles.

For further details see:

Which Type Of Income Investor Are You? And Why It Matters