PSPC - White Brook Capital Partners First Quarter 2023 Commentary

2023-04-26 12:29:00 ET

Summary

- White Brook Capital LLC is an independent investment advisory firm. The Firm was founded with the belief that there is a shortage of managers who charge a reasonable price, invest for the long term, and maintain a socially responsible threshold while also beating the market.

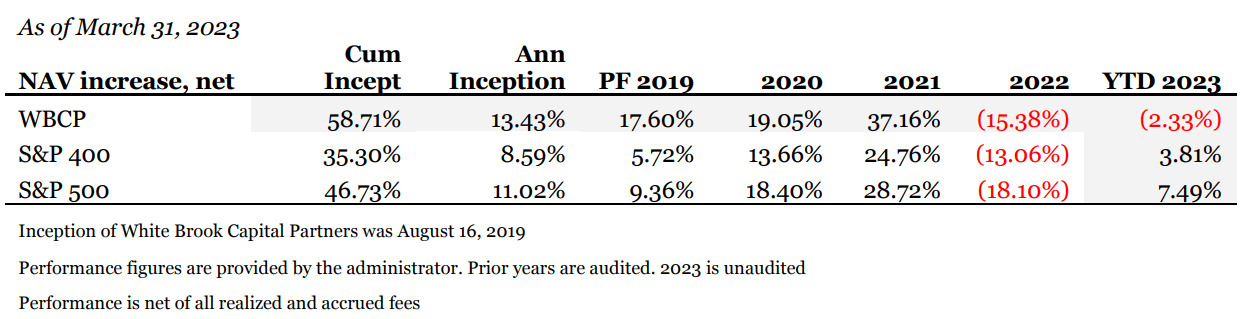

- The Portfolio underperformed during the quarter down 2.33% vs the Midcap 400 up 3.81% and the S&P 500 up 7.49%.

- During the quarter, the Firm exited its position in Itron as it became clearer that despite growth and a better business model, the Company suffered from a management-agency problem that, despite solid end-market dynamics, would result in poorer than expected free cash flow.

- Today, the portfolio is more concentrated in historically cyclically sensitive companies than previously.

Performance Review

{kind=link}

Portfolio Update

The Portfolio underperformed during the quarter down 2.33% vs the Midcap 400 up 3.81% and the S&P 500 up 7.49%. While the portfolio performed well in January and February, it suffered as Silicon Valley Bank, Signature Bank of New York, and Credit Suisse failed, despite a lack of direct banking exposure. Underperformance was widespread across positions except for Builders FirstSource, Inc (BLDR).

Builders FirstSource and Mosaic, Inc (MOS) were the portfolio's top performers, while Afya Inc (AFYA) and B. Riley Financial (RILY) were the worst underperformers.

During the quarter, we entered positions in Green Plains, Inc (GPRE) and in ITV PLC (ITVPF)[1].

Green Plains is an ethanol producer undergoing company specific change by enabling its plants to produce additional products (clean sugar and ultra-high proteins) with the same feedstock - increasing margins and the return on invested capital of the business. This is a common vision for ethanol producers, but Green Plains is amongst the best capitalized to complete the transformation, has unique intellectual property, and is further along in the process than many in the industry. With over 50% of its plants converted to produce clean sugars, and an activist investor now involved, the stock price is unchanged from when I first became interested in Green Plains a year and a half ago.

Crucially, two things have occurred today since I began to consider Green Plains for investment.

- The Company is further along in its plant transformation

- The outlook of the base business has improved.

The ethanol business was unprofitable during much of 2022 as the corn crush margin turned negative. Today, it is profitable again as imbalances created from Covid and Russia's invasion of Ukraine have rebalanced - ethanol prices have increased, corn prices have come significantly off their highs, and natural gas is cheap again. Additionally, during the quarter, six midwestern states announced that they would be mandating E15 blends in their states - thereby significantly increasing demand in those states for ethanol.

Moving forward, Green Plain's gross margins should be significantly positive on the base business. With 50% of the Company's refinery output outfitted to produce new products, valuation undemanding, and the demand improving, cash flow generation should resume and grow strongly for the next several years. If it does, Green Plains will prove to be extremely compelling at these prices.

I'll have more on the ITV position as it becomes fully established.

During the quarter, the Firm exited its position in Itron, Inc (ITRI) as it became clearer that despite growth and a better business model, the Company suffered from a management-agency problem that, despite solid end-market dynamics, would result in poorer than expected free cash flow. This exit was years ahead of expectations, and while it was a moderately profitable investment, the early exit was a surprise and a disappointment.

The Firm also exited its position in Post Holdings Partnering Corporation (PSPC). The Company was an unusual SPAC, and our investment had two potential outcomes, either we would be wrong and not lose much, or we'd be right and do exceptionally well. Management indicated that potential target prices remained unattractive and were unlikely to consummate a transaction during their latest earnings call. Rather than wait for liquidation, we exited the investment to have cash available for possible opportunities. The Fund was flat on the investment.

Today, the portfolio is more concentrated in historically cyclically sensitive companies than previously. While industrials have traded in unison on the back of macroeconomic concerns, particularly in March, different industries continue to have very different economic drivers and outlooks, even in a potentially recessionary environment. I expect expansion in each that we have exposure.

I continue to believe that select investments in the stock market are the best opportunity for capital appreciation, and I advocate for higher allocations at these prices. I am extremely bullish on the prospects of the individual companies in the portfolio in the short, medium, and long term.

Clients should reach out if interested in more specific advice.

Market Review

The first quarter had two impactful "real economy" events. The first, the regional banking crises, combined the inverted yield curve - long talked about, but short on obvious impact - with relatively high short-term interest rates to create a funding crisis for reckless banks. While the problem now appears contained, there are several near-term implications from the crises.

- While the details are important, SBNY and SVB failed because low yielding bond investments, even if paid in full, in many cases, will never be worth 100% of their par value, valued in today's dollars. Their barbell approach of investing in "low-risk" long-term low-yielding bonds and high risk, start-up warrants, and venture-stage loans, was, despite traditional economic thought, an exceptionally high-risk strategy.

- Commercial real estate shares many of the same properties as fixed income. Many commercial real estate investments were priced at inopportune times and are no longer economic. Those deals are often levered and when repriced, equity real estate returns are likely to be abysmal and the holders of the debt may also be impaired. That could feedback to the banks but will certainly impact non-bank financial institutions who lent to them.

- The run on banks and ensuing fear caused many consumers to realize that much better and safer yields could be had in money market funds than in bank deposits which pay near zero yield and are at least somewhat sensitive to the bank's solvency.

- Non-bank financial lenders curtailed much of their lending activity as short term rates increased, but banks, able to tap low-cost deposits filled the gap and retook market share. With deposits leaving banks for money market funds, banks' deposits will become more expensive for banks as they seek to become more competitive or they will exit altogether. The disappearance of the deposit funding source, means that banks will become choosier about where to lend, liquidity is/will become less available.

- The availableness of funding heretofore has blunted the impact of Federal Reserve's policies, the removal of that funding, means the Federal Reserve's policies are more likely to be impactful.

The second long-term impactful development in the quarter was OpenAI's release of ChatGPT 4.0 and the release of their platform for focused artificial intelligence models to work with OpenAI. Today, ChatGPT is at the level of an achieving, but not yet brilliant high school graduate in most disciplines and something better than that in a few. There are a couple of quick takeaways around likely impact over the medium term.

- Over some relatively short period of time, the value in many industries is going to shift to unreplaceable sources - which, given the "creativity" of today's AI, are vanishingly few. For instance, while the US auto industry produces more cars today than ever, it does it with 14% of the workforce of its peak. The news industry was decimated by the internet as it nationalized and demonetized news production. Humans will be needed to interact with other humans, but generally, much less.

- Even if needed, however, it's unclear where the new profit centers lie. Using the previous examples, the automation and robot manufacturers at the auto plant makes more than anyone that works at the factory; Internet giants make more from the news than journalists do.[2]

- The easy answer used to be that programmers would be the kings, and they have been, but these AI models can code too. If our job as a society is to prepare the next generation to contribute, it's difficult to see a path to success that looks anything like my generation's or those previous.

- For AIs to progress, they need to consume data. Data definitionally is common, replicable, and usually undifferentiated. It is the output of a relatively cheap process or sensor. Particular data sets, however, will be almost priceless. Those priceless data sets will likely be bundled with undifferentiated data to sell to artificial intelligence. Music and cable television are the analog, where Michael Jackson, Taylor Swift, and Drake carry a lot of weight for music labels, and ESPN, NBC, and CBS did the same for the video bundle. Ironically, AI already makes decent music, too.

- While incumbents in any industry horde data, emergent players share insights freely to market themselves. AIs have and will continue to consume from the public sphere freely, and consume the content of the youngest, most ambitious, emerging minds, but also the least experienced, dumbest, and most socially inept as well. That's a hard problem.

- AI's application is chemistry, not physics. Small changes to models will have a big impact, making it, and its adoption hard to predict. Even as this letter entered the editing phase, a Google official noted that the Company's AI had learned Bengali, based on just a few inquiries even though no one had directed it to. That's scary, but also hints at how powerful AI can be for countries and demographics not typically catered to.

Before the fourth quarter of 2022, I recommended holding needed cash over investing in bonds. Recent events highlight the importance of specificity - emergency cash should be invested in short-term money market funds. Still, bond securities of intermediate duration are preferable to money market investments, if held for the medium term, in my view, as money market funds suffer from the need to consistently reinvest to earn their yield. If the Fed lowers its benchmark rate for any reason, money market funds will yield less.

Portfolio Company Updates:

B. Riley Financial Services (RILY): A misguided short report significantly hurt the stock price and has whipped short sellers into an ideologically based fervor that, given Riley's lack of sell-side coverage, the company's execution and time will have to unwind. The regional banking crises accentuated the stock's weakness despite the Company not being a bank, not having banking deposits, and not competing in the markets of a traditional non-bank financial institution.

I fundamentally disagree with many of the allegations of the report. Several of the conclusions made are built on facts/contentions that are verifiably untrue. However, the instigating short seller has credibility within the investment community as he has been loud and right before. B. Riley has no sell-side coverage, buys distressed assets, and by virtue of its portfolio of non-public investments, is somewhat opaque and therefore difficult for an analyst to step into an investment committee meeting to risk his or her reputation defending. The stock will take time to rise beyond its previous highs, but the environment is constructive. I added to our position during the stock's decline.

KAR Auction Services (KAR): More constrained banks have resulted in higher yields for incumbent non-bank dealer floorplan financing companies. This should positively impact the ability of KAR, a very large dealer floorplan lender, to lend profitably at higher yields.

KAR's loans are typically installment loans where the principal must be paid along with interest. Higher yields on still high used car prices should incentivize dealers to wholesale cars they cannot retail more quickly and to accept lower bids for those cars when they do try to wholesale them. This is a positive for the fundamentals of both company divisions that has gone largely unappreciated.

Greenbrier (GBX) : Greenbrier positively preannounced its quarter in the waning days of March, but the stock, after an initially positive reaction, did not have a sustained positive response. The unveiling of its full quarterly report and subsequent first-ever investor day during the second week of April has undone many of the concerns raised after the previous report and supports the view that it is successfully addressing its operational problems. Demand is also strong. While the stock rallied on the strong full results, it has since sold off - back to the levels of its problematic release in early January - and is as undervalued as we previously related, but with less risk than previously thought. I continue to believe the stock is significantly undervalued.

Mosaic, Inc (MOS): Despite favorable midterm fertilizer dynamics, Mosaic (MOS) performed worse than expected during the quarter. Significantly, the Company began to rally in the last days of the quarter after it preannounced production at the low end of the guidance for the first quarter when market fears were for an even worse outcome. Given March weather, particularly in the northern United States, where a significant snowpack continued to cover farmland (as of the first days of April), I expect their 1st quarter earnings call will speak to significant second-quarter demand, particularly as the weather was more favorable for fertilizer usage in early April. Prices during the second week of April for fertilizers broadly also have begun to lessen their decline despite a continued rapid decline in other feedstock commodities.

The stock has been driven by concern about destroyed 2023 demand that I believe, given the state of the world's depleted fields, misses that demand can no longer be destroyed, only delayed, and even that may not be necessary given the rapid improvement of the US's northern grain basket and the solid fundamentals in Brazil. The Company continues to trade for a very cheap valuation even though it generates strong free cash flow, returns that cash flow to shareholders, and is underlevered. We continue to hold our position.

Afya, Inc (AFYA), the Brazilian medical school company, declined almost 30% in the quarter. Reasons for the decline leave me wanting. The Company missed headline fourth quarter earnings expectations - but the miss was slight. The Company continues to grow revenue and EBITDA by approximately 20% per year while generating impressive free cash flow and trading for reasonable multiples of cash flow. The underlying medical education business prospects are bright, with the Brazilian education ministry likely to continue to grow available medical education seats, Afya's reputation continuing its ascent, and its more rural roots a benefit to future government plans.

Its online SaaS businesses have proven less profitable than hoped, but they continue to grow while being refocused on running profitably. Further acquisitions in the space are likely to be limited, with additional products added to the platform organically or through small acquisitions. The biggest obstacle to growing our position is that getting much bigger would violate White Brook's average daily trading volume based risk mitigation restrictions. We continue to hold, have not sold shares, and would grow the position if shares were more available to trade. That said, the Company, despite its already low float, also believes its shares are undervalued and is buying back shares.

This was a disappointing quarter, but not one that I believe is indicative of future prospects. As always, feel free to reach out to discuss this or any of your investments at White Brook Capital. I thank you for your support and will strive to continue to earn your trust.

Sincerely,

Basil F. Alsikafi, Portfolio Manager, White Brook Capital, LLC

All investments involve risk, including loss of principal. This document provides information not intended to meet the objectives or suitability requirements of any specific individual. This information is provided for educational or discussion purposes only and should not be considered investment advice or a solicitation to buy or sell securities. The information contained herein has been drawn from sources that we believe to be reliable; however, its accuracy or completeness is not guaranteed. This report is not to be construed as an offer, solicitation, or recommendation to buy or sell any securities herein named. We may or may not continue to hold any of the securities mentioned. White Brook Capital LLC and/or their respective officers, directors, partners, or employees may, from time to time, acquire, hold or sell securities named in this report. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

Footnotes

1 This is the Firm's first international investment. Accounts held at Schwab were unable to participate. If you hold a taxable account with White Brook Capital, reach out about becoming a partner of White Brook Capital Partners.

2 This is a guess, but a reasonable one.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

White Brook Capital Partners First Quarter 2023 Commentary