DCBO - White Falcon Capital - Docebo: Expect 30%+ Growth EBITDA Margins Of 20-25% In Maturity

2023-05-11 23:50:00 ET

Summary

- Docebo has #1 market share in the Learning Management Solutions software category.

- In its initial years, Docebo grew through in-bound inquiries and without investments in S&M.

- We believe that the business can grow 30% plus and produce EBITDA margins of 20-25% in maturity.

The following segment was excerpted from this fund letter.

Docebo, Inc. ( DCBO )

In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value. - Warren Buffett

{kind=link}

Executive Summary

- Docebo has #1 market share in the Learning Management Solutions ((LMS)) software category

- Docebo is an innovative company that has an extensive product portfolio in the learning management category that is full featured but easy to use. In its initial years, Docebo grew through in-bound inquiries and without investments in S&M.

- The Software as a Service ((SaaS)) product that Docebo sells is sticky and produces recurring revenues for the company. Once a customer builds training materials with Docebo software, it is difficult to switch to another provider.

- Docebo further entrenches itself in the customer’s workflow by making it easy to install, integrate and operate. Furthermore, the social and AI aspects of the product are tremendously value added for customers.

- Throughout its history, Docebo efficiency on its S&M spend is high which validates the unit economics of the business. Until 2019, most growth was driven by in-bound calls.

- Docebo is led by Claudio Erba who has a passion for learning and funded by Intercap Equity which has a successful track record investing in technology companies.

- White Falcon bought the stock for 10-13x look through operating earnings when the market was worried about all technology stocks. We believe that the business can grow 30% plus and produce EBITDA margins of 20-25% in maturity.

Introduction

Docebo (Latin for ‘I will teach”) was founded in 2005 by Claudio Erba in Italy as a learning management software ((SaaS)) company that develops and provides a learning management platform for training both internal and external workforces, partners and customers. Docebo was incorporated in 2016 in Canada as Docebo Canada Inc. after receiving a significant investment from Intercap Capital, a family office based in Toronto and Klass Capital, a PE firm focused on software, also based in Toronto.

Docebo completed its Canadian IPO in October 2019 raising $75 mn at C$16 per share. This was followed up by the US IPO in December 2020, at a price of $48.00 per share for gross proceeds of $165.6 million. It is important to note that Docebo has ‘burned’ about $12 mn in cash since its incorporation in Canada in 2016 so it has been fairly conservative with capital. Intercap currently owns 41% (down from ~60%) and Klass Capital owns 1.83% (down from 11%) as they have sold down their stakes over the last two years. Cat Rock Capital, a Tiger grandcub has taken a substantial 14.67% stake in Docebo over the past year making it the top position in the fund.

{kind=link}

Source: Docebo

Docebo provides an easy-to-use and highly configurable learning platform with the end-to-end capabilities and functionality needed to train both internal and external workforces, partners and customers. Docebo also operates a content marketplace where companies can buy courses covering broad subjects like digital marketing, leadership, or sales. The social aspects of the software differentiate it from run of the mill LMS where administrators can ‘gamify’ learning and employees can contribute content to the platform. With incorporation of AI, when a skills gap is identified, targeted recommendations can be provided in a more personalized format than may be possible without the use of AI - yielding more effective and efficient learning outcomes overall. In addition to above, Docebo can be white-labeled and seamlessly integrated into the enterprise’s software stack for ease of use.

Management and other sources believe that this market will be worth ~$29.9bn by 2025 from $9.5 bn in 2019 growing at a CAGR of 21%. The market is changing where new learning functionalities like social learning, learning on the job, and communities designed to drive organizational change are increasingly becoming important.

Docebo has executed and proved their credibility by winning major clientele such as Uber, Amazon AWS Cloud, Walmart, Chipotle and over 3,000+ businesses across North America and Europe. Here is the customer profile:

{kind=link}

Source: Docebo

Product

The software ensures efficient online course delivery and the tracking of learning progress with advanced reporting tools and analytics.

The main platforms include:

- Docebo Learn - This is their foundational module, it helps learning administrators like HR centralize, organize and distribute learning content, track certifications and measure results with customer analytics.

- Docebo Discover, Coach & Share - It provides learners with access to social learning by encouraging the sharing of knowledge through formal, social, interactive and experiential learning across an organization.

- Docebo Extended Enterprises - It allows businesses to manage multiple portals for different audiences or organizations with their own administration, branding and authentication.

- Docebo Content - Marketplace for external content so that client can have one vendor

- Docebo Connect - Seamlessly connect Docebo in client’s softwares stack

In this software vertical, Docebo may have a number of possible competitive advantages :

- Switching Costs - Docebo sells to mid-market and enterprise customers. Typically these contracts are for multi-year periods and require integration.These customers will become accustomed to their learning management system software. Switching platforms, moving courses, and inputting employee, customer, and partner information will all be tedious work and the potential costs may outweigh any potential savings.

- Social collaboration elements - Docebo's platform is built around the notion that 70% of learning is in the form of social learning rather than solely instructor-led learning. Hence, the platform makes it easy to create, upload & share with peers. They make it enticing with rewards and relative ranking amongst peers. They allow the collaboration to extend to external organizations which is unique.

- User generated content - Users are empowered and feel they can contribute to the platform's success by uploading content. This helps in retaining and spreading institutional knowledge.

- AI - Docebo is also very focused on using AI and machine learning algorithms to improve the recommendations on the application, so it is easier for users to find content that caters to them.

- Multiple modules and integration: Docebo Content gives the customer an opportunity to not have to establish another contract with another content vendor, and have a single relationship with Docebo. Docebo Connect gives the client an ability to integrate the LMS software with multiple systems without the hassle of custom integrations. For example, in Q1 2022 earnings call mgmt mentioned that, “Docebo Connect is being deployed by one of the largest cryptocurrency exchanges in the United States. Our solution will enable automation of their learning processes that touch other applications in the data software stack, while getting learning data where it needs to be, all at scale”.

Source: Docebo

A customer commenting on choosing Docebo,

I think it's the design flexibility that we have. It's super easy to set everything up like you want. Others said you can make everything look fairly unique and white-labeled for yourself. I think that is what I'm really happy with. I don't know, the gamification feature is pretty good. The reporting is very exhaustive as well, so it's really cool. I really like their support also. It's quick. They're quick to respond, quick to fix even more difficult issues. These are some of the things I like the best. Hard for me to say which one is the very best. -Samsung - Senior Training Manager

The same customer on social and gamification of learning,

We give rewards for completing training fields as an encouragement, as an incentive for people to actually go and look for new training materials. We also have some small rewards also for sharing your own content if you find lots of content online that are public and sharing. -Samsung - Senior Training Manager

Like many leading companies, Docebo has the potential to be one of the leading companies in this growing industry. The Company faces direct and/or indirect competition from a variety of players, including:

- Legacy corporate e-learning service providers such as Cornerstone On Demand, SAP SuccessFactors and SumTotal Systems (owned by Skillsoft);

- Corporate e-learning service providers such as SAP Litmos, Absorb LMS, MindTickle, Lessonly and SkillJar.

These companies compete directly with Docebo:

- Lower priced solutions such as 360Learning, TalentLMS, Totara and LearnUpon;

- Legacy training vendors such as Global Knowledge, General Assembly and New Horizons;

- Individual-focused e-learning services such as LinkedIn Learning, Udemy, Udacity and Pluralsight

An executive a a competitor when asked who he respected in the industry:

I'd say Docebo and Skilljar. Docebo, because they have been doing it for a long time very well, they have evolved with the market and they can serve a broad range of use cases in a way that doesn't meaningfully deflate their ability to serve others. Skilljar, because they're a pure play for customer training and they do it really well, particularly in marketing. In a sub100-person size when they first really started getting going, they were able to establish themselves as one of the leading names. They were punching a bit above their weight class there. - Executive, Thought Industries

While there are a lot of ‘competitors’, we observe in the software industry that a better ‘mousetrap’ can grow significantly faster than legacy solutions especially as it solves pain points for both administrators as well as learners. It is also important to note that for many competitors above LMS is an ‘add-on’ and not a core. LMS can and should be relevant to any industry. In this regard, Docebo’s software is configurable to fit any industry and need. If a software solution is easy to install, easy to upload and integrate and then easy to administer and adopt, it can grow significantly faster than the second best solution. We believe that this is the case with Docebo.

It is remarkable that Docebo has grown from $10 mn ARR in 2016 to $143 mn in ARR in 2022 even with all this competition. Docebo has not done this by ‘buying’ revenues - we know that they have ‘burned’ a cumulative $12 mn since their IPO. Importantly, a large part of their customer segment is the mid-market segment which is notoriously difficult to penetrate due to low ticket sizes and a large marketing effort. Docebo has been able to penetrate this sector mostly led by its superior product where 80% of lead generation came from in-bound calls. The return on Docebo’s S&M is remarkably high and we estimate that every $1 spent in S&M produces $1.2 mn revenues. Management has also mentioned that 70% of their wins are coming from replacing a legacy player. We believe this speaks directly to the quality of the solution offered by Docebo.

The other aspect that has helped the company is acknowledging its sub-par scale in initial years and sourcing partners. Customers can white-label Docebo’s solution. Docebo’s first OEM partner, HR software provider Ceridian, took nearly two years to ramp up, but is now one of the company’s largest customers by ARR (~10%). With several new partnerships signed over recent quarters and an expanding pipeline with parties from beyond traditional HR (e.g. managed services, sales enablement, and talent management), we see potential for meaningful upside to street expectations as Docebo’s partner channel continues to scale, allowing the company to tap into new markets and drive more profitable growth in the years ahead.

Revenue growth at Docebo has both been led by the number of customers as well as the growth in average deal size ((ACV)) as can be seen below:

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Subscription Rev |

| 23,881 |

| 37,283 |

| 57,415 |

| 95,936 |

| 131,597 |

| Growth % |

| 56.12% |

| 54.00% |

| 67.09% |

| 37.17% |

| Professional Rev |

| 3,193 |

| 4,160 |

| 5,502 |

| 8,306 |

| 11,315 |

| Growth % |

| 30.28% |

| 32.26% |

| 50.96% |

| 36.23% |

| Customers |

| 1,400 |

| 1,700 |

| 2,200 |

| 2,800 |

| 3,400 |

| Additions |

| 200 |

| 300 |

| 500 |

| 600 |

| 600 |

| Avg Contract Value (,000) |

| 21,000 |

| 27,000 |

| 34,000 |

| 42,000 |

| 46,000 |

| Growth |

| 31.25% |

| 28.57% |

| 25.93% |

| 23.53% |

| 9.52% |

| ARR |

| 29,400 |

| 45,900 |

| 74,800 |

| 117,600 |

| 153,400 |

The growth at the company will be a result of adding more customers and adding bigger customers. This trend took a bit of a hiatus in Q2 2022. The following from the earnings transcripts give a good picture.

Q4 2021 Earnings Transcript: “We continue to see traction from enterprise customers as Docebo is being selected for more complex, multiple-use case deployments. This is reflected in the ACV for new logos and cross-sells added in the fourth quarter, which was close to $60,000. In addition, approximately 45% of the ARR generated from new and cross-sell logos this quarter came from deals valued at over $100,000.”

Q1 2022 Earnings Transcript: “New and cross star logos with ARR greater than $100,000 represented approximately 50% of the net new ARR, underscoring continued momentum with larger commercial and enterprise customers, and we take confidence in the fact that our pipeline continues to be strong. ACV for new customers in the quarter was approximately $60,000 driven by our continued shift in mixed to enterprise-size deals and adding incremental products.”

Q2 2022 Earnings Transcript: “ACV for new customers in the quarter was approximately $45,000. New and cross sell logos with ARR greater than $100,000 represented approximately 30% of the net new ARR. ACV from new customers declined sequentially as the result of the lower contribution from deals valued over $100,000. This is a direct result of the elongation of the enterprise sales cycle. The reason why we’re seeing that happen in deals, generally speaking, deals above $100,000 and/or you can associate that with our more enterprise type customer is we’re seeing our companies changing or making the buying process more complex within their own environment. Among those changes is the inclusion or introduction of a C suite that wasn’t prior necessarily involved in certain spend thresholds at all levels.”

All other commentary from management from a market demand perspective remains robust. As an example, the CEO has mentioned multiple times that the market for external training is twice the size of internal training and that they have only scratched the surface here. Further, more and more customers are deploying Docebo for multiple use cases such as onboarding, enablement, professional education, compliance, to name a few. They disclose that in Q4 2021 , 61% of revenues and 80% of use cases are hybrid - meaning covering more than one department.

Customer Mix:

- Commercial < 50K ARR

- Mid-market >50K<100K ARR

- Enterprise > 100K ARR

The company discloses that more than 80% of ARR is multiple use cases which means that these customers are likely to be sticker.

In order to keep growing at a fast pace Docebo is embarking on a two pronged strategy:

-

- Hired a CMO and other senior personnel in the sales division in order to properly cover the enterprise division. The whole focus of the management is in penetrating and growing the enterprise division. Not only is it good business but it is also needed at this point in time due to base effects.

- Geographical expansion starting with Europe. Docebo indexes heavily to the US; which leaves a lot of space to grow revenues from ROW. This ROW revenue comes with extra complexity (language etc.) but Dacebo seems to be learning and adapting.

Financials and valuation

Docebo trades in both US and Canada but reports in USD. We’ll use USD financials here:

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Total Revenue |

| 27,074 |

| 41,443 |

| 62,917 |

| 104,242 |

| 142,912 |

| Growth % |

| 53.07% |

| 51.82% |

| 65.68% |

| 37.10% |

| Total COGS |

| 5,650 |

| 8,261 |

| 11,539 |

| 20,786 |

| 28,178 |

| Gross Profit |

| 21,424 |

| 33,182 |

| 51,378 |

| 83,456 |

| 114,734 |

| Gross Profit Margin % |

| 79.13% |

| 80.07% |

| 81.66% |

| 80.06% |

| 80.28% |

| R&D |

| 6,612 |

| 8,579 |

| 13,384 |

| 20,363 |

| 24,778 |

| Margin % |

| 24.42% |

| 20.70% |

| 21.27% |

| 19.53% |

| 17.34% |

| S&M |

| 11,630 |

| 16,266 |

| 24,020 |

| 43,346 |

| 59,654 |

| Margin % |

| 42.96% |

| 39.25% |

| 38.18% |

| 41.58% |

| 41.74% |

| G&A |

| 10,940 |

| 15,872 |

| 16,998 |

| 28,443 |

| 30,183 |

| Margin % |

| 40.41% |

| 38.30% |

| 27.02% |

| 27.29% |

| 21.12% |

| SBC |

| 253 |

| 659 |

| 1,619 |

| 2,261 |

| 4,713 |

| Margin % |

| 0.93% |

| 1.59% |

| 2.57% |

| 2.17% |

| 3.30% |

| FX loss/gain |

| 775 |

| 922 |

| 1,775 |

| 473 |

| -11,112 |

| Depreciation |

| 169 |

| 693 |

| 1,209 |

| 2,019 |

| 2,333 |

| Margin % |

| 0.62% |

| 1.67% |

| 1.92% |

| 1.94% |

| 1.63% |

| Total Opex |

| 30,379 |

| 42,991 |

| 59,005 |

| 96,905 |

| 110,549 |

| EBIT |

| (8,955) |

| (9,809) |

| (7,627) |

| (13,449) |

| 4,185 |

| EBIT Margin |

| -33.08% |

| -23.67% |

| -12.12% |

| -12.90% |

| 2.93% |

We can see the operating leverage in almost all cost items. The G&A expenses bumped up in 2021 due to US listing expenses. The EBIT in 2022 was affected by very high FX, absent which the EBIT would have been $11 mn higher! In our call with the CFO he mentioned that there should be continuous operating leverage on both G&A and R&D but less so on S&M as management will focus on investing in the business. In the Q4 call, the CFO mentioned that there is no reason why G&A cannot go to 10-12% of revenues. This is a 10% bump in EBIT margin!

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| 2024 |

| 2025 |

| Customers |

| 1,400 |

| 1,700 |

| 2,200 |

| 2,800 |

| 3,400 |

| 3,950 |

| 4,450 |

| 4,900 |

| Avg Contract Value (,000) |

| 21,000 |

| 27,000 |

| 34,000 |

| 42,000 |

| 46,000 |

| 51,000 |

| 56,000 |

| 60,500 |

| Growth |

| 31.25% |

| 28.57% |

| 25.93% |

| 23.53% |

| 9.52% |

| 10.87% |

| 9.80% |

| 8.04% |

| ARR |

| 29,400 |

| 45,900 |

| 74,800 |

| 117,600 |

| 156,400 |

| 201,450 |

| 249,200 |

| 296,450 |

| Growth |

| 56.12% |

| 62.96% |

| 57.22% |

| 32.99% |

| 28.80% |

| 23.70% |

| 18.96% |

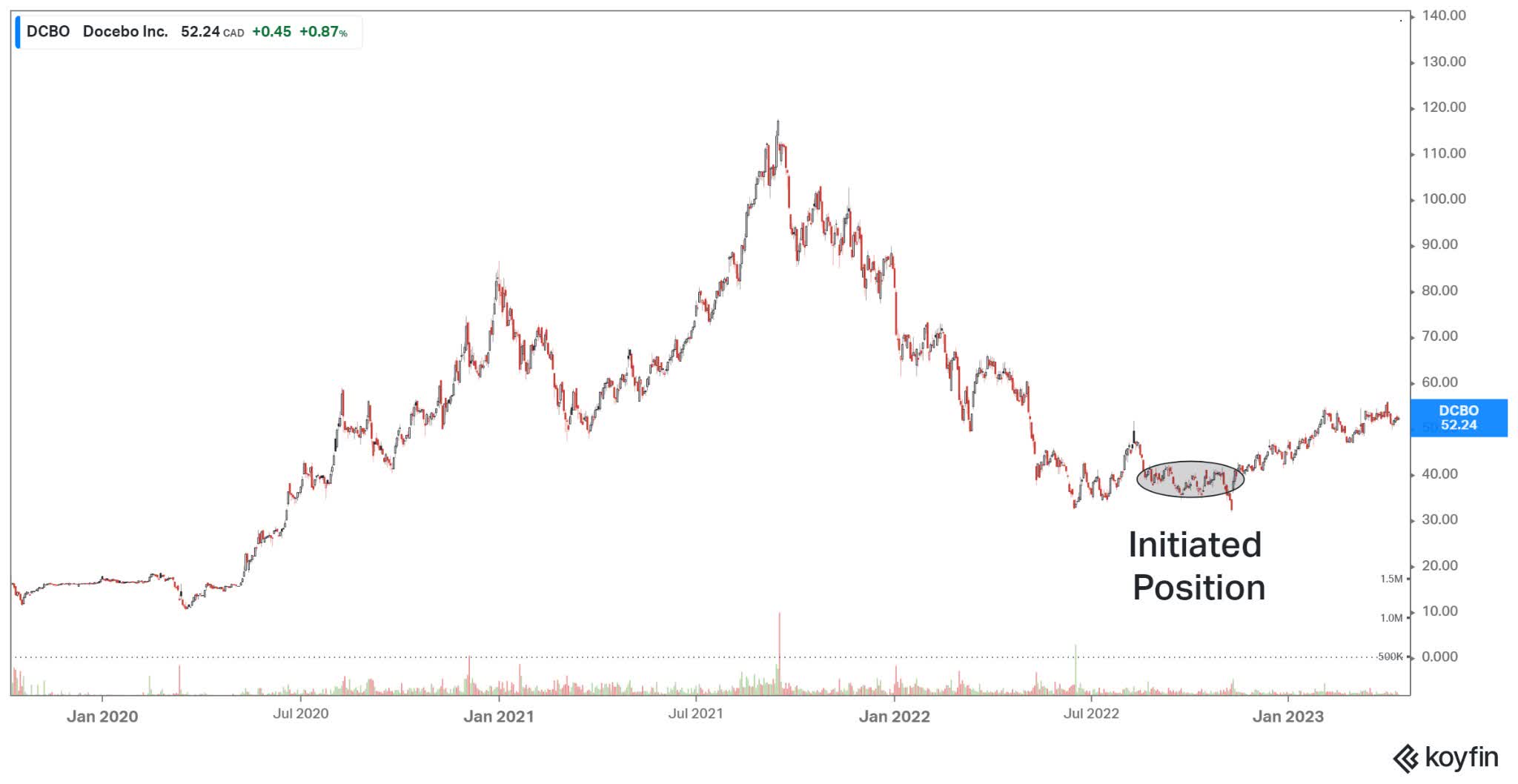

When we initiated our position, its valuation looked as follows:

| ($ USD millions) |

| Stock Price |

| 27 |

| Shares Out |

| 33 |

| Mcap |

| 891 |

| Cash |

| 211 |

| EV |

| 680 |

| EV/S 2022 |

| 4.76 |

| EV/S 2023 |

| 3.58 |

| EV/S 2024 |

| 2.79 |

| Look Through EV/EBITDA |

| @20% EBITDA |

| @25% EBITDA |

| EV/EBITDA 2022 |

| 23.79 |

| 19.03 |

| EV/EBITDA 2023 |

| 17.89 |

| 14.32 |

| EV/EBITDA 2024 |

| 13.93 |

| 11.15 |

| EV/EBITDA 2025 |

| 11.43 |

| 9.14 |

We reckon that these valuation multiples were not high given the quality and growth profile of the business.

Docebo is also good at share based dilution because perhaps a large part of the float is held by insiders or controlling shareholders. Docebo is 41% owned by Intercap which has the same shares as everyone else but a shareholder agreement that allows them to appoint directors in proportion of their shareholding. The founder and CEO, Claudio Erba holds about 4% in stock.

The company has close to $260 mn net cash. One of the things we have not seen here is any buybacks. Management clarified that buybacks are not a priority and that they may look for accretive targets in this market.

Conclusion

In conclusion, I believe Docebo has the following characteristics,

- Large TAM

- Good product with good execution

- Insiders with significant skin in the game

- Depressed valuation due to quarterly deceleration

For further details see:

White Falcon Capital - Docebo: Expect 30%+ Growth, EBITDA Margins Of 20-25% In Maturity