GLOB - White Falcon Capital Q2 2023 Partner's Letter

2023-07-13 14:34:00 ET

Summary

- White Falcon Capital is an independent entity and have a mandate to do the right thing for the portfolio and the partners. Our goal is to protect and compound capital over the long term on a risk adjusted basis.

- In the second quarter, the portfolio benefitted from the rise in the technology stocks, especially Nu Holdings, AMD, and Amazon.com.

- EPAM remains a high quality founder led business that has hit a rough patch. We believe that this is a small bump and EPAM will get back to growth in a few quarters.

Dear Partners,

While individual client returns may differ based on their inception dates, consolidated performance of all accounts for the period ending June 30, 2023 is as follows:

| Q2 2023 |

| YTD 2023 |

| 2022 |

| ITD* |

| White Falcon (net of fees) |

| 6.9% |

| 20.04% |

| -9.3% |

| 7.3% |

| S&P 500 TR ((CAD)) |

| 6.5% |

| 14.2% |

| -12.6% |

| 3.0% |

| MSCI All Country ((CAD)) |

| 3.9% |

| 10.9% |

| -11.9% |

| -0.8% |

| S&P TSX |

| 1.2% |

| 5.8% |

| -5.8% |

| -0.9% |

*Inception date is Nov 8, 2021 (Cumulative return)

In the second quarter, the portfolio benefitted from the rise in the technology stocks, especially Nu Holdings, AMD, and Amazon.com. The rest of the portfolio was flat to down with EPAM Systems ( EPAM ), Converge ( CTSDF ), and Aritzia ( ATZAF ) being notable detractors. We trimmed some of our technology stocks and allocated capital to deep value, commodity and special situation equities. Despite decent performance, we believe the margin of safety in the portfolio is satisfactory as the ‘value today’ exposure has languished and can propel the portfolio if it were to participate with the market. Due to this, cash levels have risen but to only about 5% of the overall portfolio.

While we show other indices above, White Falcon does not manage against any index. Our portfolio is an esoteric group of businesses where each company is underwritten based on expected returns and where risk is managed by buying good quality and growing businesses run by competent management teams. We also manage risk/reward at a portfolio level by owning a balance of ‘compounders’, ‘value today’ and ‘value tomorrow’ with the relative weight of each dependent on the opportunity at hand.

White Falcon’s mission remains to compound capital on a risk adjusted basis over the long term. We believe that even small advantages when compounded over time can lead to big differences in outcomes. We calculated the compounded value of $100,000 at 5%, 10% and 15% for 10, 20 and 30 years. It is always remarkable to see how relatively small differences in returns add up to very significant sums over a period of years.

“Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn't, pays it”

-Albert Einstein

| 5% |

| 10% |

| 15% |

| 10 Years |

| $162,889 |

| $259,374 |

| $404,553 |

| 20 Years |

| $265,328 |

| $672,748 |

| $1,636,640 |

| 30 Years |

| $432,191 |

| $1,744,930 |

| $6,621,140 |

We, of course, cannot promise results. There will be times when we will lead the markets and there will be times when we will lag the markets. What we can promise is the following:

- My family and I will have our entire liquid net-worth invested alongside you

- We will not take undue risks with your capital. We do not use leverage, or derivatives/options or short selling to enhance our results.

- We will be diligent in our stock selection and portfolio management responsibilities

The last point is particularly important and will determine if we will be able to achieve our mission over the long term. Here we eschew dogma for pragmatism and let bottom up fundamentals and individual risk/rewards guide our decisions.

Some partners have asked about the sustainability of the current market rally.

Last year, the markets were pricing in a recession which never materialized. This tells you all you need to know about ‘expert’ opinions - all of whom were calling for a recession. We believe these experts have underestimated the amount of fiscal stimulus injected into the economy. Importantly, technology companies benefited from cost cuts and the advent of Artificial Intelligence ((AI)) which helped investors get comfortable with future earnings growth. The above two factors along with bearish positioning acted as rocket fuel to propel the market upward.

Also, in previous letters, we have repeatedly made the point that, (a) earnings are nominal, and (b) higher interest rates are not an anathema for stocks. Emerging markets such as India and Brazil have high inflation and high central bank rates but also high multiples. Good companies have been able to pass on pricing and increase their earnings on a nominal basis. Remember, a discounted cash flow model ((DCF)) used to value a business has a discount rate (which has been increasing) but also a growth rate (which has also been increasing, albeit nominally). Now, while most market observers believe that declining inflation will be positive for risk assets, the reality may be much more nuanced where businesses may struggle to grow earnings. That would be a time to be very cautious!

"Bull-markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria."

- John Templeton

Most bull markets start with a short covering rally which then expands to multiple expansions and then finally followed by earnings growth. In all this time, investors remain skeptical and the market’s climb a proverbial ‘wall of worry’. Market multiples have expanded and, now, we have to see if earnings will cooperate!

White Falcon’s modus operandi in all this is anchored by valuations. When stocks have lower valuations a lot less has to go right for one to make money while when stocks have high valuations a lot has to go right for investors to make money. As valuations of technology companies climbed, we took the opportunity to trim and sell out of some of these businesses in the portfolio. While we were early in our selling (as we were in our buying last year!), we believe valuations here did not leave any margin of safety. We have recycled this capital into deep value, commodity, and special situation equities including merger arbitrage opportunities where spreads have been some of the widest on record.

Due to these changes, the portfolio’s current allocation is as follows: 31% to ‘Compounders’, 14% to ‘Value Tomorrow’ and 42% to ‘Value Today’.

Top 5 positions at quarter end were Precious metals royalty basket, Nu Holdings, AMD, Amazon.com, and Teck Resources. At this half year mark, I’ll give a bit of an update on these companies as well as the key detractors.

- Nu Holdings ( NU ): Nu is a neo-bank based in Brazil. Nu is running the Capital One playbook where the business model is to lend to a credit starved population and leverage data and analytics to offer a superior product. Then, with this data, cross sell higher margin products to a subset of the customers. Nu has data and cost to serve advantages (no branches) and is gaining market share as it can lend at lower yields, have relatively lower NPLs and still make a high ROE. We believe Nu is a world class institution in every sense of the word. We initiated this position at 10x 2025E earnings estimate of $0.38 per share. Since then, management has executed well and brought forward profitability due to which current consensus estimate for 2025E earnings is $0.48 per share for a forward P/E of 15x.

- Advanced Micro Devices ( AMD ): Under CEO Lisa Su, AMD has made one successful bet after another - both on technology and strategy. Chiplet architecture, advanced 3D packaging, modularity and adaptability in chip design, strong TSMC partnership for leading nodes all helped AMD differentiate itself in the marketplace. We also liked the fact that AMD was diversified in product lines as well as end markets. Further, it was free cash flow positive at the bottom of the cycle and had a net-cash balance sheet. AMD was a secularly growing company that was facing cyclical issues available at 18x earnings, and these earnings had been revised down several times. The risk was that further revision in earnings will be needed and we were happy to buy more if that was the case. Today, the stock is more than fully valued but Nvidia’s guide and AMD’s optionality in GPU’s give us second thoughts in trimming more.

- Amazon.com ( AMZN ): Amazon is a controversial investment. It had been ‘profitless’ for much of its existence and divided investors on the ultimate sustainability of the business model. We believe that Amazon has two very strong businesses - an e-commerce business (including ads) backed by a top-notch logistics network and an internet infrastructure business called AWS that is an oligopoly with Microsoft (MSFT) and Google (GOOG)(GOOGL). We believe Amazon has a superior culture that allows it to succeed in its various business lines. Importantly, Amazon is inflecting on free cash flow ((FCF)). We model that it will produce $6+ in FCF per share in three years. If this is valued at 3-3.5% FCF yield then Amazon is a $200 stock. Amazon also has a portfolio of venture bets (which consume a lot of capital) and all these are upside options for an investor.

- Precious Metals Royalty basket ([[WPM]], [[SSL]], [[TFPM]]): In the current macroeconomic environment, there are many ways to ‘win’ with gold. It is remarkable that even with record positive real yields, gold is flirting with all time highs. Why? Western central banks are increasing interest rates which means that they will have to pay more interest on the record levels of debt that their government’s owe. Where will the money come from to pay the higher interest expense? The answer is simple - more debt and more money printing! We believe the gold knows this! We believe that precious metals will protect real purchasing power and act as a hedge to the portfolio when macroeconomic uncertainty arises. Owning royalty companies at reasonable valuations gives us a high quality exposure to precious metals without project or cost inflation risks inherent in a mining company.

- Teck Resources ( TECK.B:CA ): Teck Resources is a diversified mining company and produces essential natural resources such as zinc, copper, steel making coal. A new mine in Chile called QB2 has come online this year meaning that all capital expenditures to build this mine (and project risks) are behind us and all free cash flows from selling resources from this mine are in front of us. The world is short copper and not enough capital has been spent to explore for copper in the last 10 years. Given leads and lags in bringing new supply into the market and increasing use in electrification, we believe copper will be a structural winner over the next 10 years. Also, Teck is currently in ‘play’ which means that other companies are vying for its assets. It is uncertain how this all plays out but we believe this puts a floor under the stock price. Recently, we increased our position in Teck to make it a top 5 position.

Barring a few gainers, most of the portfolio was flat to down over the quarter. Within this, EPAM Systems ((EPAM)), Converge Technology Solutions ((CTS)) , and Aritzia ((ATZ)) were notable detractors.

“All happy families are alike; each unhappy family is unhappy in its own way”

- Leo Tolstoy

The above Tolstoy quote also applies to the winners and losers in the portfolio! Each loser has its own set of (often complicated) problems. With these companies above, anything and everything that could go wrong has gone wrong and we are currently sitting at very trough multiples on trough estimates. We have added to some of these positions as we believe the risk reward from these valuations is very attractive.

In the appendix to this letter, we present our updated thoughts on EPAM. EPAM Systems was a big winner for White Falcon last year (we first wrote about it in our Q1 2022 letter). We trimmed about half of our position close to the highs but the other half of the position is down close to 50% from the highs and back to the original cost base. After growing at high rates for the last 10 years, EPAM has stumbled and guided to negative revenue growth for this year. In addition, some investors are worried about the impact of AI on IT services businesses. We have increased our position in EPAM and our conviction in the future of the IT services space has led us to a new position in Endava ( DAVA ). Endava is a UK based company that, like EPAM, provides digital transformation consulting, agile software development and various automation solutions to clients all over the world.

Other

I am not only trying to compound capital but also knowledge, relationships and time. Being your partner in this endeavor has been a fulfilling and rewarding experience. Please feel free to get in touch with me if you have any questions or feedback.

Referrals are the lifeblood of a small business such as ours. If you know someone who would be a good fit for White Falcon and can benefit from an allocation to the White Falcon portfolio please let me know and I’m happy to start a conversation.

Have a great summer!

With gratitude,

Balkar Sivia, CFA

Founder and Portfolio Manager

White Falcon Capital Management Ltd.

Appendix: EPAM Systems (Updated) Research Report

"In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value."

- Warren Buffett

{kind=link}

EPAM Systems is a high quality IT service provider that has been a compounder stock. EPAM's winning streak came to an end in 2022.

With Russia’s invasion of Ukraine the stock fell from $550 per share to $180 per share as the market was worried about EPAM’s workforce/delivery centers in Ukraine, Belarus and Russia. The management at EPAM did a wonderful job derisking the company from this exposure. They exited Russia by not only leaving their clients there but also by closing their delivery centers in the country. By the end of 2022, EPAM’s exposure to these volatile countries had reduced from 60% of overall workforce to 30% of overall workforce. EPAM moved some of the affected employees to neighboring countries and ramped up their hiring efforts in India and Latam. Due to this, the stock moved up to $450 per share a few months later in August 2022.

However, very recently, EPAM reduced their guidance for 2023. They first reduced their guidance during their earnings but then followed this up with a further reduction in guidance a few weeks later. The management is now expecting negative growth in 2023.

We first got involved with EPAM after it sold off in March 2022 but have recently added to the position. EPAM is currently available for 21x depressed 2023 earnings per share. It is a $12 bn market capitalization company with $1.7 bn in net cash and a $500 mn share repurchase authorization. An investor purchasing shares at these valuations can expect to compound with earnings growth with the added call option of multiple expansion if EPAM is once again seen as a durable growth franchise. We believe that is the most likely outcome.

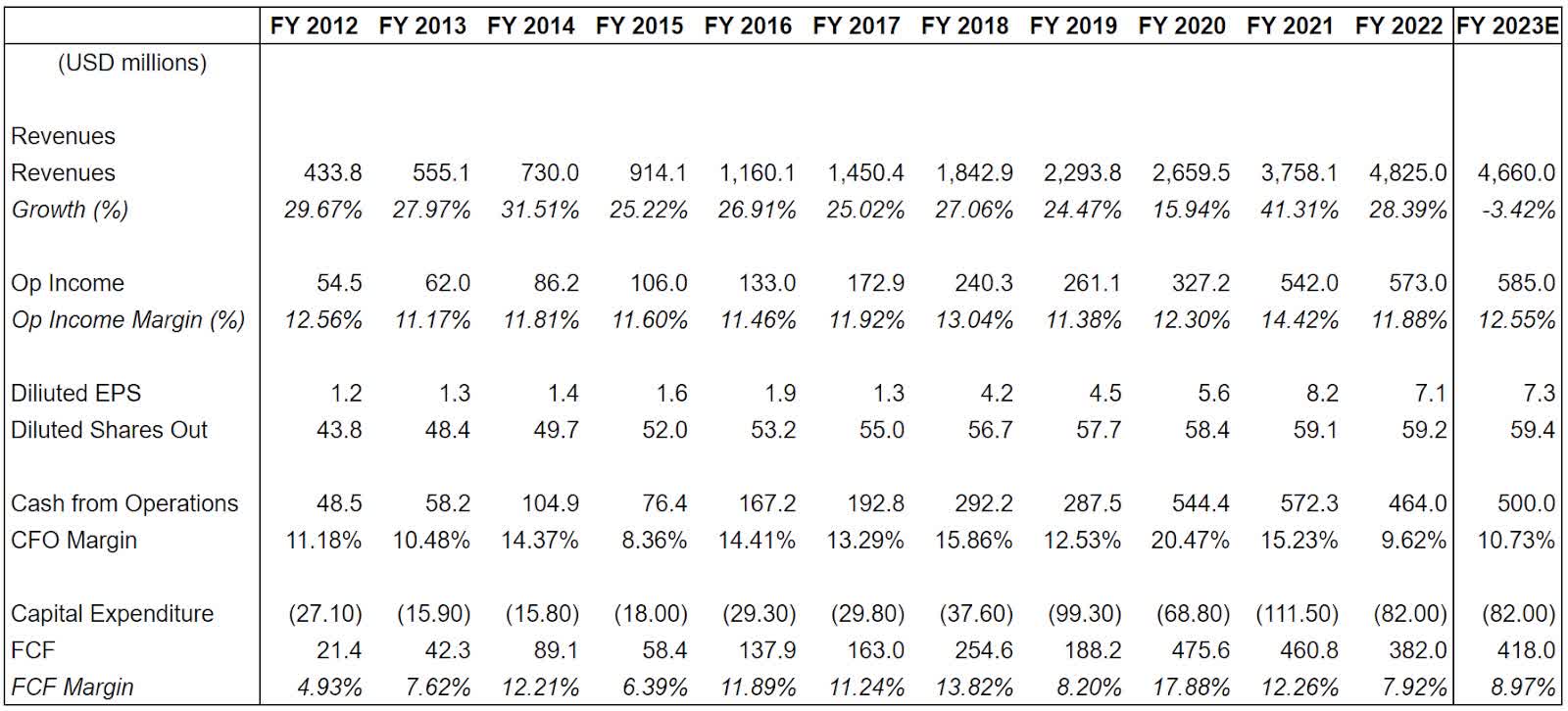

Here are the historical financials:

{kind=link}

EPAM is a global IT services firm. It competes with the likes of Accenture and provides IT services to a diversified end-market consisting of clients in the financial services, travel, retail, software, healthcare among other industries. EPAM held its IPO in 2012, and since then, has grown more than 10x until the year ended 2022 with revenues of $4.8 bn and EBIT of $573 mn. Like all IT services companies, EPAM is well placed as a ‘toll booth’ between technology and corporations who increasingly need technology to transform their business.

Their stellar track record came to an end in 2022. For 2023, EPAM guidance that its revenues will de-grow from 2022 levels. Management mentioned that clients are deferring projects due to which there will be little or no growth for the next few quarters. They guided for growth to come back in 2-4 quarters as clients can pause these projects but not cancel them.

What happened?

- IT spending is indeed slow. Like many other industries, IT services also ‘over earned’ during covid and had a stellar performance in 2022. Some of this is now normalizing.

- Some clients have de-risked EPAM due to their still substantial exposure to Ukraine.

- Overall, revenue growth in this industry is very dependent on employee growth. EPAM has not grown its net employees - the losses in Russia and Ukraine have been made up by gains in India and Latam. It takes time in this to train employees and bring them up to high levels of productivity.

In addition to all these issues, there is debate amongst investors on AI - Are EPAM and other IT services providers AI winners or AI losers? Most IT services are billed on a ‘time and material’ basis and the ‘bear’ argument is that as software engineers become more productive; fewer software engineers will be needed thus affecting growth for all IT services companies.

In this report, we will highlight EPAM’s strengths and debunk some of the narratives surrounding the thesis. We believe the risk reward on EPAM is very attractive.

IT services and EPAM’s competitive advantages

All IT services companies look the same. They all provide bodies that specialize in technology to businesses that need to either cut costs or improve processes. Under the hood, however, they are all a little different. Understanding these nuances can be the difference between a value trap and a compounder.

According to Gartner, IT services is one of the fastest growing segments of overall IT spend. The IT service providers play in this bucket and grow due to three factors,

- Increasing IT spends: These spends are typically a function of IT budgets. These budgets are typically a certain percentage of revenues and can be economically sensitive. The trend is that most corporations are allocating a larger and larger part of their spends to technology - software is in fact eating the world. These spends have further tailwinds from Cloud computing, Cybersecurity, Work from home and Digital marketing.

- Increasing outsourcing: Larger businesses can afford in house technology departments but for most businesses technology is not their core expertise. It is also difficult to hire and retain good technology talent. So, they rely on consultants to keep them abreast of the latest technology trends. In the past, most companies let IT companies manage their costs but increasing IT services companies are helping businesses transform the way they do business.

Confirming this, Gartner mentioned that, through 2025, organizations will increase their reliance on external consultants, as the greater urgency and accelerated pace of change widen the gap between organizations’ digital business ambitions and their internal resources and capabilities.

The two biggest competitive advantages in this industry are scale and culture .

If you look at the history of IT services companies we observe that the big get bigger. Accenture currently has 700,000 employees. Why? Because scale matters in more than one way.

On the revenue side it matters because an IT services company will not get a $10 mn project from a client until they have done a $10 mn project in that practice in their industry and can provide a good reference . Many times, an IT services business has to organically get to that level or acquire another company that has a good reputation in that practice and industry. The phrase, ‘no one gets fired for hiring IBM’ came from the fact that until you have a proven history or executing and become a low risk choice for customers, you will not get hired. EPAM has a reputation for being a good partner for corporations.

On the cost side, scale matters as a company needs resources to train their workforce on the newest technology - something that changes all the time. The successful companies were able to transition their business from application development to ERP implementation to cloud migrations and now they will have to transition to AI related technologies. All this requires significant resources and a margin buffer that only the larger IT service providers can absorb.

Warren Buffett had been reading IBM’s annual report for 50 years before he bought the stock. He talked to Berkshire companies and reasoned that most companies do not switch their IT providers. He was absolutely right in his assessment of the industry - it is a very sticky business - but picked the wrong horse (he should have bought Accenture instead!).

EPAM is a founder-led Company. Culture is key. IT services are execution heavy businesses. Projects have to be delivered on time and on budget to satisfy the client. While projects start and finish, good IT services companies remain entrenched with the clients and endeavor to gain a bigger share of their IT budget. The financial services industry, for example, has a constant need for IT services due to complicated back offices, changing compliance requirements, mergers and acquisitions, or digitizing services. An IT service provider needs to work hard to take its fair share of the client’s IT budget but the good ones do just that. Whatever the client’s need, the IT service provider has a solution. EPAM is good at this! Due to this, the business generates more recurring revenue and is much higher quality than the market realizes.

With the IT services industry, there are some net winners and then some net losers. IT work is continuously getting commoditized. Companies such as Accenture or Infosys have a ‘legacy’ business that is facing pricing pressures and has negative growth as well as new ‘digital’ business lines that are growing like a weed. Newer IT service companies with very strong engineering capabilities such as EPAM, Endava, Globant ( GLOB ), Luxoft (now acquired by DXC) have much more of these ‘digital’ revenues due to which they grow much faster but this also makes them more dependent on discretionary spend.

EPAM’s historical core competency is full life-cycle software development services including design and prototyping, product development and testing, component design and integration, product deployment, performance tuning, porting and cross-platform migration.

EPAM is well diversified within verticals (financial services, travel, business information & media, software, and life sciences). It takes a lot of time and effort to methodically diversify your business in this sector and each vertical can be thought of as a new business line. EPAM also not does not have large concentration risks when it comes to clients with top 10 clients making up about 23% of revenues.

"I would say in my experience in working directly with EPAM is that they have a core engineering expertise that is top shelf. They can bring that to bear on whatever projects or programs that they're involved with. They seem to have a team of core scientific engineers that aren't necessarily dedicated to any particular project but are there to help in any fashion to accelerate or solve very difficult problems that come into play that may stall a project. Their ability to do that is pretty profound."

-EPAM Competitor Jan 2022

“In my opinion, they're probably the best at doing this in the industry. They far away are better than TCS, Cognizant, your typical offshore vendors. They're really a specialist at modernization of product stacks, which has been great. They have a really good practice around DevOps and modernization. They've been fabulous. I use them also at Shutterstock when we did something similar for AWS, and they were just as good.”

-CTO of Priceline.com (June 2023)

The other way to get scale and capabilities is acquisitions. Good providers do many tuck-in acquisitions to gain either expertise or clients. EPAM had done many successful acquisitions over its history and integrated them into their culture. We have not seen large acquisitions succeed in the industry due to cultural differences.

"When they identified in the past that there's a capability that's going to be in higher demand in the market, and they lack the capability internally, they did the smart thing in my estimation. They went ahead and purchased one or two or several really strong players, and integrated them."

-EPAM competitor (Jan 2022)

We believe that EPAM is a superior business and is shielded from the common problems in the industry. Its services are essential to its clients' success. EPAM has proven to be a good IT services company and invested ahead of new technologies in order to stay relevant with its clients and increase its share of wallet. There is very little reason to believe that this will not be the case going forward.

AI Narrative

We think IT services companies such as EPAM are AI winners. Indulge me here but I asked chat GPT on how AI can help businesses and here is the response:

“Here are some key areas where corporations can leverage AI for benefits:

- Automation and Efficiency: AI can automate repetitive and mundane tasks, enabling corporations to increase operational efficiency and productivity.

- Decision Making and Analytics: AI-powered analytics can process vast amounts of data and provide valuable insights for decision-making.

- Personalized Customer Experiences: By leveraging machine learning algorithms, corporations can analyze customer data, preferences, and behavior to tailor product recommendations, marketing messages, and customer support interactions.

- Enhanced Customer Service: AI-powered chatbots and virtual assistants can provide instant and round-the-clock customer support.

- Risk Management and Fraud Detection: Machine learning algorithms can analyze patterns in financial transactions, customer behavior, and cybersecurity data to identify potential risks, anomalies, or fraudulent behavior.

- Product Development and Innovation: AI techniques like natural language processing and computer vision can assist in product development and innovation. By analyzing customer feedback, social media sentiment, market trends, and competitor data, AI can identify customer needs, suggest product enhancements, and support the development of new offerings."

And on and on and on…..

AI is great but how does a corporation incorporate AI into their business? It seems like machine learning is an integral part of the process. So, what does one need for machine learning? I again asked chat GPT:

“To effectively implement machine learning, several key components and considerations are necessary. Here are the main requirements for machine learning:

- Quality Data: This involves relevant, accurate, and properly labeled or annotated data. The data should be representative of the problem domain and cover a wide range of scenarios and examples.

- Data Preprocessing: Before feeding data into machine learning algorithms, preprocessing is often required. This includes cleaning the data by removing noise, handling missing values, normalizing or standardizing features, and performing feature engineering to extract meaningful representations.

- Machine Learning Algorithms: A variety of machine learning algorithms exist, including supervised learning, unsupervised learning, reinforcement learning, and more. Selecting the appropriate algorithm(s) for the specific task at hand is crucial.

- Training Set: A labeled training set is needed for supervised learning, where the input data and their corresponding target values are available. The training set is used to train the machine learning model by adjusting its parameters or weights based on the provided examples.

The other key points mentioned are Model Selection and Tuning, Model Training, Model Evaluation, Deployment and Integration and finally, Monitoring and Maintenance”

In essence, what we read above is that there is a LOT of work that needs to be done in order to enable a corporation to reap the benefits of AI. All this work has to be performed by someone! We think EPAM and other engineering focused IT services providers will be the key enablers of this move to AI. Further to this, corporations that still have their data on premises on different platforms and they first need to bring it in one place and on the cloud to even begin implementing AI. This work is also performed by EPAM.

There is an excellent transcript on Stream by the CTO of Priceline.com that sheds light on these factors:

“I've had prior experience working with EPAM in prior companies. They are what I'd say a best-in-class company for modernizing tech stacks and moving them to the cloud. We hired them to accelerate our move out of our data centers and into Google Cloud.”

“They were doing cloud modernization, I'd say, about 10 years ago before it was a big thing and now it's a big thing. They have really good relationships with Google and AWS. They bring EPAM into deals as well with customers. What winds up happening is for AWS or Google contracts, if you lock in to, say, a five-year deal worth $500 billion, Google then gives you what they call PSF, which is professional service funding, in order to make the migration to the cloud. They'll give you, say, $60 million, $70 million to do that. You can only spend that PSF money against certified Google partners. Quite honestly, there's maybe a half dozen that are really good and EPAM is one of those.”

“They're ((EPAM)) building out our real-time data infrastructure for us now to train and build out all of our machine learning models. They're doing that right now and they're well-positioned to do that. The generative AI stuff, we're going to do in-house just because we have a large data science population already and have been doing machine learning for quite some time. Any of the heavy lifting around modernizing our data infrastructure over the next couple of years, EPAM will be doing that work.”

-CTO of Priceline.com (June 2023)

The current narrative is that corporations are going to hire a team of software engineers and then with the help of chat GPT or Bard they will be successful in enabling corporations to build AI capabilities. We believe this is totally wrong.

The IT services industry has suffered from these false narratives in the past. A few examples:

Initially, all IT work was application development but when SAP and Oracle brought packaged software the narrative was that IT services is done but IT services pivoted to implementing ERP and made out like bandits. Then cloud software started to become dominant and this software did not require a lot of implementation and the narrative again shifted to the death of the IT services business. But, IT services pivoted to cloud migrations and digitally enabled custom projects that were increasingly possible because of the flexibility offered by the cloud. We believe this current shift of narrative where investors believe that IT service companies are net losers from AI is misplaced.

As long as IT budgets are increasing, the better IT service providers will find things to do. Cloud providers such as AWS and GCP bring EPAM into deals so that they can more effectively modernize tech stacks for clients! We believe AI is a net enabler and will lead to accelerated growth in revenues and earnings for IT services companies like EPAM.

Conclusion

EPAM remains a high quality founder led business that has hit a rough patch. We believe that this is a small bump and EPAM will get back to growth in a few quarters.

Overall, the company can be had for 21x depressed 2023 guided earnings. This is on a non-GAAP basis. Before 2022, analysts had estimates going to $16 per share in earnings for EPAM by 2025. While this is no longer possible, we model $14 per share in 2025 and $16+ per share in 2026. In addition to the reduction in growth, EPAM is also not optimized when it comes to margins. We believe it can move on to high teens margins in a more normalized environment.

In all this, AI remains a big variable and we think the surprise is likely to be on the upside.

This is a $320-400 stock in three years if they can do $16+ in earnings per share in 3 years and get valued at 20-25x earnings. It is more likely than not that the multiple will be much higher if they do return to 20% plus growth.

Importantly, EPAM has a strong balance sheet with $1.7 bn in net cash and can buy back more shares or do tuck in M&A to further enhance shareholder value. EPAM has a $500 mn buyback authorization in place which should help with dilution and earnings accretion.

Economic cycle is a big risk. IT service providers are dependent on IT budgets which are then dependent on revenues. If there is a downturn in the economy and revenues come down - that will affect IT budgets.

Disclosure: White Falcon has a long position in the shares of EPAM Systems.

Disclaimer

- Past performance is not necessarily indicative of future results. All investments involve risk including the loss of principal. It should not be assumed that any of the transactions or investments discussed herein were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the investments discussed herein. Specific companies or investments shown in this presentation are meant to demonstrate White Falcon’s active investment style

- White Falcon may change its views about or its investment positions in any of the securities mentioned at any time, for any reason or no reason.

- White Falcon disclaims any obligation to notify the market of any such changes.

- The information and opinions expressed in this presentation is based on publicly available information about the securities.

- The letter and thesis includes forward-looking statements, estimates, projections, and opinions, as well as more general conclusions. Such statements, estimates, projections, opinions, and conclusions may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond White Falcon’s control.

- Although White Falcon believes the data and numbers are substantially accurate in all material respects, White Falcon makes no representation or warranty, express or implied, as to the accuracy or completeness of any written or oral communication. Readers and others should conduct their own independent investigation and analysis of the thesis of any and all companies mentioned in this document.

- The letter is not investment advice or a recommendation or solicitation to buy or sell any securities. White Falcon undertakes no obligation to correct, update, or revise the Presentation or to otherwise provide any additional materials.

- White Falcon also undertakes no commitment to take or refrain from taking any action with respect any of the companies mentioned in this letter.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

White Falcon Capital Q2 2023 Partner's Letter