ROVR - White Falcon Capital Q4 2023 Partner's Letter

2024-01-19 09:50:00 ET

Summary

- White Falcon Capital is an independent entity and have a mandate to do the right thing for the portfolio and the partners. Our goal is to protect and compound capital over the long term on a risk adjusted basis.

- We were able to achieve a reasonably good result in 2023 on both an absolute and relative basis.

- We will always be focused on the downside risks in the portfolio as protecting capital is a key prerequisite to compounding capital.

- Unlike the index, we employ a value investing philosophyand pick good quality businesses through bottom-up fundamental research andthen risk manage the portfolio to proactively navigate the ever-changinginvestment landscape.

Dear Partners,

While individual client returns may differ based on their inception dates, consolidated performance of all accounts for the period ending December 31, 2023 is as follows:

| 2023 |

| 2022 |

| ITD* |

| White Falcon (net of fees) |

| 36.0% |

| -9.26% |

| 21.6% |

| S&P 500 TR ('CAD') |

| 23.2% |

| -12.6% |

| 14.1% |

| MSCI All Country TR ('CAD') |

| 18.5% |

| -11.9% |

| 8.5% |

| S&P TSX TR |

| 11.8% |

| -5.8% |

| 6.9% |

| *Inception date is Nov 8, 2021 |

We were able to achieve a reasonably good result in 2023 on both an absolute and relative basis. We were helped by the contribution of technology companies in the portfolio as well as the take-out of two portfolio companies - Diversey and Rover - during the year. We like our current portfolio holdings and are optimistic about their potential for further gains. Incrementally, we have been directing capital towards the laggards in the portfolio as well as small and mid-capitalization companies, where we find valuations to be particularly appealing.

We were fortunate to have several partners heed our call to add capital to their portfolios during the 2022 drawdown. As a result, our money-weighted returns - which is what truly matters - are notably higher than our reported time-weighted returns. Adding capital during periods of uncertainty is often difficult, however, it's essential to bear in mind that, in the long term, the principle of 'lowest average cost wins' holds true.

In this letter, our focus will be on performance attribution, reflections on the year, and current portfolio positioning. For new and prospective partners, this will also help illustrate White Falcon's philosophy in practical terms.

"Metrics once invented become proxies for truth. In many businesses, they are managed by metrics and the world may have shifted from underneath them" - Jeff Bezos

First, the White Falcon portfolio is very different from the popular indexes. Our ‘metric’ for measuring success is risk adjusted absolute returns across a market cycle and not an index. Currently, only four of our portfolio companies overlap with the S&P 500 index ( SP500 , SPX ) . Also, our exposure to USD and US based stocks is at about 55% of the portfolio (balance is in CAD in Canadian listed stocks) while the S&P 500 has all of its constituents in the US. It should, therefore, be no surprise to partners that our results look very different from any index.

Our portfolio consists of a group of businesses where each company is underwritten based on expected returns and where risk is managed by buying good quality and growing businesses run by competent management teams. In order to earn better returns one has to have a variant view. Most of White Falcon’s positions are companies where,

- We have determined that growth or margins or free cash flow of a business will be better than market expectations

- Market simply does not appreciate the quality of the business or the capital allocation prowess of the management

- Business is out of favor due to temporary factors and our work shows that the stock price will recover as these issues subside. It helps that we have a longer-term view than most market participants.

- We buy securities from distressed investors that are selling for reasons other than fundamentals

We practice a style of investing called value investing. We try to buy businesses for less than they are worth. We try to buy stocks when the market has low expectations of them. Unlike the conventional definition, our style of value investing has nothing to do with low current valuations. A stock at a price to earnings ratio of 10x can be very expensive while another stock at a price to earnings ratio of 30x may be fantastic value.

“The difficulty lies not in the new ideas but in escaping from the old ones.” - John Mayrad Keyens

Rover ( ROVR ) provides an interesting case study that aptly showcases the evolving nature of value investing. Our average cost on Rover was about $4.3 per share and we featured Rover in our Q3 2023 letter when it was trading at $6.5 per share. In November 2023, Blackstone ( BX ) made a cash offer for Rover at $11 per share. By definition - as this was a cash offer - Rover was a value stock at the time we featured it last quarter and perhaps a deep value stock at our cost base. Even at $11 per share, we believe Blackstone got a very good deal and were sad to see us robbed of many years of compounding. However, in November 2023, from a headline perspective, Rover did not screen well as a value stock as it was trading at 19x EV/EBITDA and 60x P/E.

We argued in our report that Rover is underearning due to which looking at the headline valuation metrics is not appropriate. In fact, we believed that Rover had the potential to achieve 30%+ adj. EBITDA margins (vs. 10% reported). In an environment where businesses are directing investments through the income statement, the lesson from Rover is that value investors must extend their analysis beyond the surface-level reported numbers and delve into the genuine earning potential of a business.

“Friends congratulate me after a quarterly-earnings announcement and say, 'Good job, great quarter”’; and I'll say, 'Thank you, but that quarter was baked three years ago. '” - Jeff Bezos

Secondly, it is important to note that the returns depicted above actually originated in the market turmoil of 2022 and were only realized in 2023. We assess that about 75% of the returns in 2023 were derived from just 35% of the portfolio. Notably, the technology companies we acquired in 2022 - AMD , Amazon ( AMZN ), Docebo ( DCBO ), NU , Rover - performed exceptionally well. In hindsight, the decision to allocate to technology stocks appears straightforward; but it actually demanded courage and conviction to buy and add to these stocks during the fear and uncertainty of the 2022 bear market.

“You make most of your money in bear markets, you just don’t realize it at the time” - Shelby Davis

We hope more partners will add to their holdings the next time we see an opportunity like 2022.

The more discerning partners may ask: why did you not earn even higher returns by allocating 100% of the portfolio to technology stocks?

The simple answer is risk management. We have said before that our philosophy on portfolio management is to be diversified enough to survive but concentrated enough to matter. The White Falcon portfolio has 22 positions and these break down into three categories: Compounders, Value Now and Value Tomorrow . The actual percentage division among categories is to some degree planned, but to a great extent, opportunistic and based on valuations.

The reality is that technology companies - within the Compounder and Value Tomorrow categories - had a great 2023. However, it is important to acknowledge an alternative scenario where rising interest rates could have led to continued challenges for technology stocks. We will always be focused on the downside risks in the portfolio as protecting capital is a key prerequisite to compounding capital.

“Successful investing takes time, discipline and patience” - Warren Buffett

As we have said in the past, none of the above is proprietary to White Falcon. We don’t have a secret sauce. Our long-term performance will be a direct result of applying these principles with discipline. Discipline to invest in good quality companies at reasonable valuations; to go against the crowd when prudent and walk with the crowd when needed; to control emotions during market volatility; and to fight our own biases.

Our mistakes in 2023 were mostly mistakes of commission. We sold or trimmed some of our portfolio holdings only to see them put up tremendous rallies afterwards! We estimate we would have gained another 300-400 bps if I just went to the beach instead of tinkering with the portfolio. We also lost about 300 bps investing in ‘merger arbitrage’ and other ‘special situations’. Needless to say, your portfolio manager overestimated his ability to navigate these situations and a lot less of your capital will be committed to these opportunities in the future. The only special situation left in the portfolio is Lifecore Biomedical ( LFCR ) and we still expect a favorable outcome for common shareholders in due time.

How are we positioned?

At White Falcon, we will always gravitate towards opportunities with low expectations and low valuations. Technology stocks came roaring back and we had to trim some of these positions as they had become too big for our comfort. As we have mentioned before, at the margin, we allocated more capital to stocks in our portfolio that were left behind by the market rally. We also initiated a few new positions (Fortrea, Conduent, Warner Bros) but the relative weight of these positions remains small as we get comfortable with the quality of these businesses.

As of December 30, 2023, we are positioned as follows:

| By Style |

| Dec 2023 |

| Dec 2022 |

| Compounders |

| 25.8% |

| 32.4% |

| Value Now |

| 38.0% |

| 32.4% |

| Value Tomorrow |

| 25.8% |

| 33.4% |

| Total Equities |

| 89.5% |

| 98.3% |

| By Market Cap |

| Dec 2023 |

| Dec 2022 |

| Large Cap ( > $20 bn) |

| 33.8% |

| 38.5% |

| Mid-Cap ( > $1 bn < $20 bn) |

| 44.6% |

| 40.2% |

| Small-Cap ( <$1 bn) |

| 11.2% |

| 19.5% |

| Total Equities |

| 89.5% |

| 98.3% |

The top 5 positions in the portfolio were: Precious Metals royalty basket, Nu Holdings, AMD, Amazon.com and Converge Technology Services ( CTSDF ). Converge made a dramatic comeback at the end of the year and reported good earnings and FCF conversion (which was a key metric for the market). It is a cheap stock that is well positioned to serve small and medium enterprises in their technological needs. AMD has worked out great for us but we must admit that it has gotten expensive. AI was not part of our original investment thesis and AMD is a great reminder of how one can get ‘lucky’ investing in quality businesses run by competent management teams (ditto for Amazon).

We often talk about our investment in Nu Holdings but have not presented you with a detailed research report. Our cost base on Nu is about $4 per share while the stock is currently trading for $9 per share. We continue to hold this position and, in the appendix to this letter, we are attaching our thesis on Nu Holdings . We are of the opinion that Nu is a rare company with the powerful combination of substantial market opportunity, an excellent business model, and an outstanding management team.

Earnings for portfolio companies are getting better. Most CEOs are slowly realizing that the economy is not in a recession and that they need to start investing in their businesses to grow. Most businesses are now lapping weaker comparable earnings from last year.

We also observe that a lot of capital went into fixed income (GIC’s, MMFs) in 2023 as one could get rates as high as 5%. Now, as rates decline, we believe, some of this capital will be forced back into equities putting a natural bid under the market.

There may be consolidations and corrections along the way but we are of the opinion that the ‘market of stocks’ (as opposed to the ‘stock market’) is reasonably valued and has the potential to provide decent returns going forward.

In essence, we find it difficult to be bearish when faced with the combination of reasonable valuations, rising earnings, a still strong consumer and declining interest rates.

However, if inflation is not truly conquered and the Federal Reserve has to maintain a restrictive stance, then that becomes a big risk. Also, there is always a lag between changes in rates and their consequences. It is possible that the high rates will finally do some damage in 2024. As always, we will factor in new information as it becomes available and make decisions to optimize risk and reward.

In Closing

A friend recently observed that the Hong Kong stock market stock is at the same level as it was in 1997 - meaning an investor that put money in an index fund in Hong Kong has made no money for 26 years! The U.S. has had similar periods - 1929-1954, 1968-1982, and recently 2000-2013 - where investors in the indices made no money.

There is an obvious reason behind an index fund experiencing prolonged cycles of performance. An index fund essentially employs a momentum strategy, where it acquires more of what is already performing well, with no consideration for value. With every additional dollar invested in an index fund, a larger portion is allocated to the best-performing stocks, which then leads to an increase in their weight within the index, creating a self reinforcing cycle. What happens when the top stocks actually stop working? Well, it then takes a long time for their weights to come down leading to long periods of stagnation. Due to this, it is important for investors to recognize that indexing is no panacea. On the other hand, portfolio managers have found it hard to resist the siren song of big technology companies and many active funds increasingly resemble the indices they aim to outperform. As a result, everybody owns the same stocks!

It is in these circumstances that we were compelled to launch White Falcon. Unlike the index, we employ a value investing philosophy and pick good quality businesses through bottom-up fundamental research and then risk manage the portfolio to proactively navigate the ever-changing investment landscape.

Importantly, we make money with you, not from you. Our fee structure abstains from charging an asset management fee, due to which our earnings are directly tied to the success of our partners. We further substantiate our commitment by placing substantially all our liquid assets in the same portfolio as our partners.

I want to express my enduring gratitude to each and every partner of White Falcon. Your support has been invaluable, and I am truly thankful for the partnership we share. Please feel free to get in touch with me at any time for any questions, concerns, or feedback you may have. With gratitude,

Balkar Sivia, CFA

Founder and Portfolio Manager, White Falcon Capital Management Ltd.

NU Holdings Research Report

“Almost all good businesses engage in ‘pain today’, ‘gain tomorrow’ activities” - Charlie Munger

{kind=link}

Executive Summary

Nu Holdings is a $40 bn market capitalization company listed on the NYSE that provides digital banking platforms and digital financial services in Brazil, Mexico, Colombia. It offers Nu credit and debit cards; savings solutions, such as Nu Personal Accounts, and a digital account solution that supports all personal finance activities.

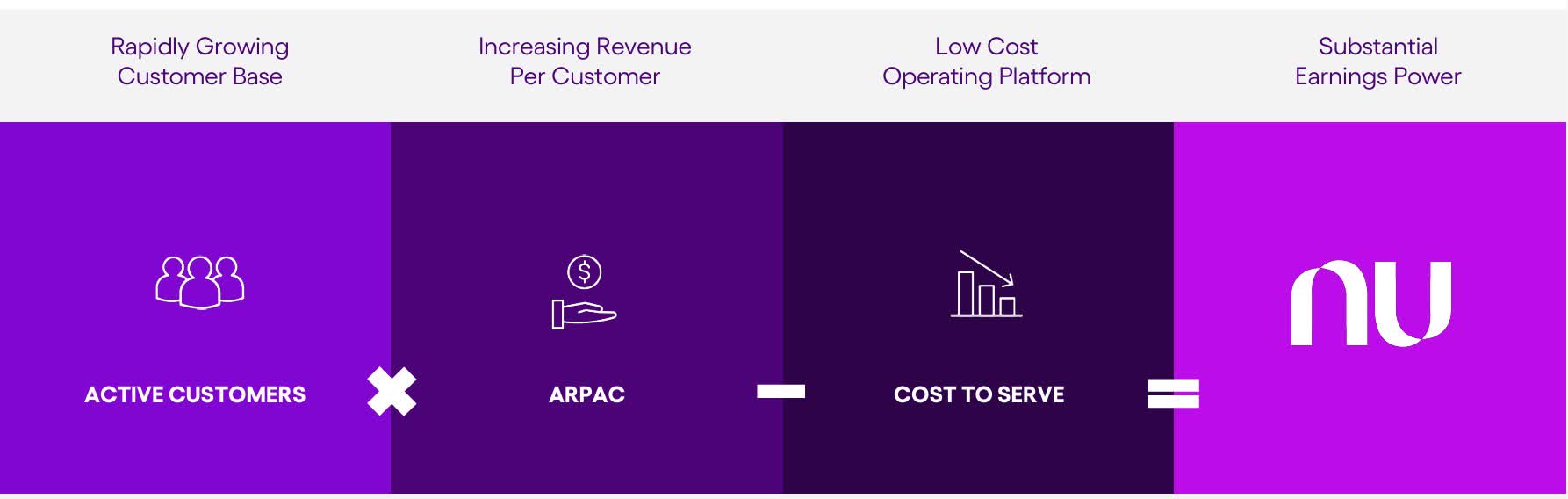

Nu has a very powerful business model exemplified by the following:

- Market with Low-Quality Financial Services and Low Credit Card Penetration:

- The model thrives in markets like Brazil where a few financial institutions control a large market share leading to high ROE’s for them but bad products and services for the consumer.

- Leveraging Data and Analytics:

- The company uses credit cards to generate data and then uses advanced analytics to manage the business. Nu pursues a “low and grow” strategy with credit limits - grant lower limits to new customers who Nu assess as higher risk and then increase those limits selectively based on a positive usage and repayment track record. Nu has a 90-day credit card delinquency rate that is consistently 25-30% better than the competitors. ? Superior Product without Opex-Heavy Investments:

? Nu does not have operational expenditures related to maintaining physical branches and instead uses technology to run its business. Further, on the marketing side, they have been able to acquire most of their customers organically and their CAC is less than $7 per customer. Both these factors lead to a much lower cost to serve compared to competitors. Nu passes on a part of these cost savings to the customers, thereby sharing their scaled economics.

- Cross-Selling Higher Margin Products:

- Once a customer is onboarded and establishes a positive credit history, Nu uses the gathered data to identify opportunities for cross-selling. This involves offering additional financial products or services with higher profit margins. An average customer now has 3 Nu products and Nu is focused on launching more products so that they can derive more and more revenue from each customer.

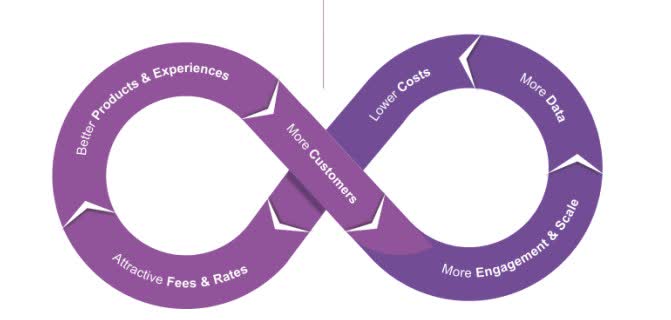

When these criteria are met, the business model can create a virtuous cycle: Nu attracts customers with a compelling product, keeps operational costs low through technology, manages risk effectively, and expands its revenue streams through cross-selling.

“The core element of our strategy is very simple. We work extremely hard to make customers love us fanatically as we build what we think are the very best products and services in the markets we operate. This obsession for our customers´ experience enables our customer base to expand, both in terms of size and engagement. By the end of Q3'23, we had achieved an impressive milestone, with over 50% of Brazil's adult population as part of our customer base, and steadily increasing market shares in Mexico and Colombia. This level of scale allows us to aggregate both structured and unstructured data which becomes an invaluable competitive asset as we currently accumulate about 30 thousand data points on each active customer annually, and this is growing exponentially over time. The momentum we are seeing over the past twelve months is a direct result of this flywheel accelerating. And in Q3 we had the opportunity to throw fuel to the flywheel with the introduction of new lending products such as payroll lending, where we decided to price at very competitive price points. The efficiency of our model also enables us to make these pricing decisions while maintaining healthy unit economics.”

- David Valez, CEO Nu Holdings (Q3 Earnings Call)

With any financial, we think it is very important to understand the management and culture of the organization and we believe that Nu is exceptional at both. Capital One’s co-founder Nigel Morris has been a major influence on the business model and risk management at Nu.

Further, we believe that Nu is under-earning due to a few reasons,

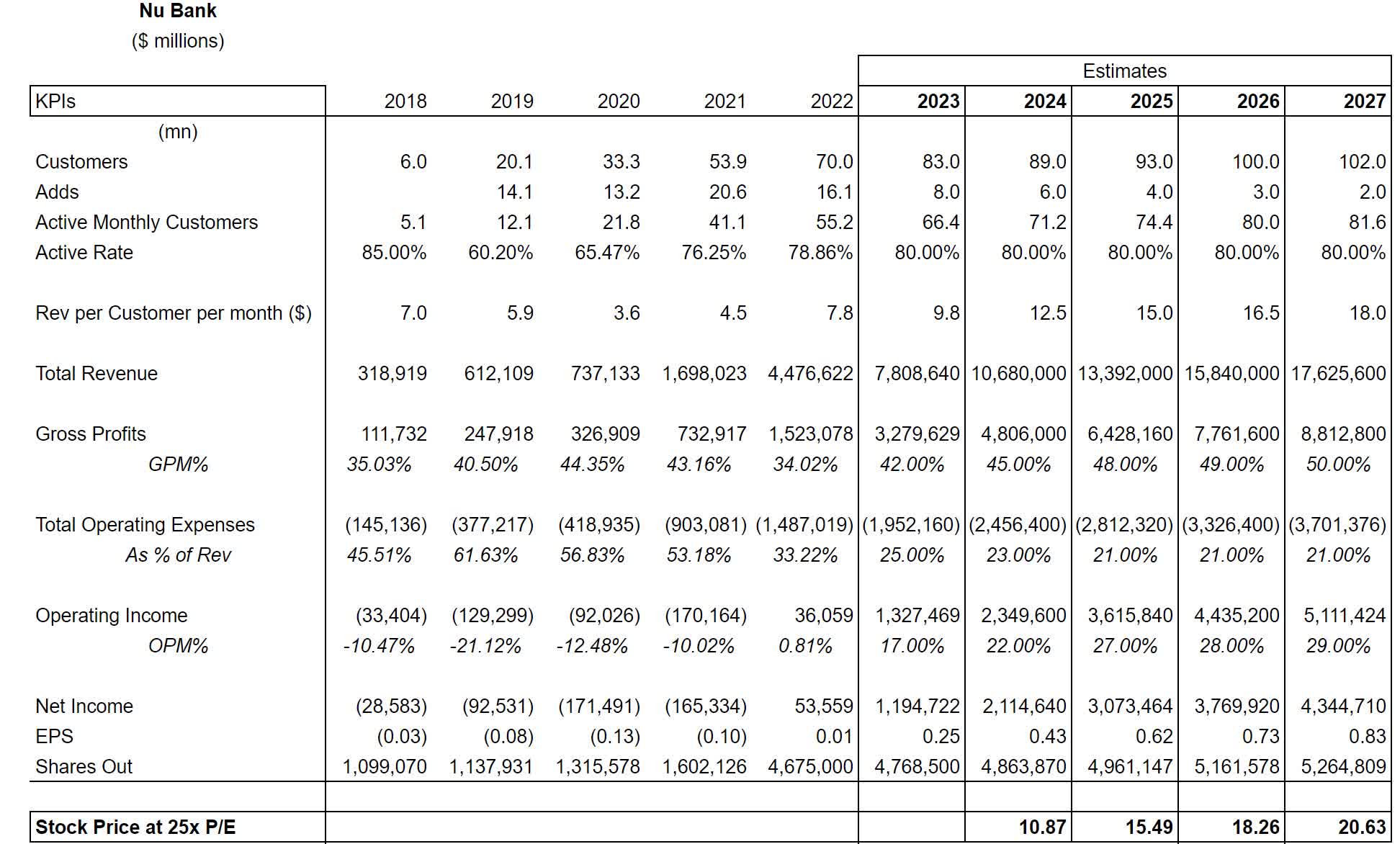

- As cohorts mature the average revenue per customer will increase: Nu has 89 mn clients and makes revenue of about $10 per client per month. Some mature cohorts are already at $20+ in revenue per month. While customer growth will slow on a percentage basis with incremental customers coming from Mexico and Colombia, revenue per client should be going up for a while.

- IFRS9 means it has to pre-provision for loan losses. Accounting regulations require Nu to take provisions against credit risk up front. So while Nu generates revenue (and credit losses) from these credit card and personal loan customers over time, the impact of upfront provisioning means that gross profits are artificially depressed especially when growth is high.

- Nu has built up costs faster than revenues. In fact, 40% of its costs are in products that have not even launched yet.

{kind=link}

Due to this and other factors we believe that Nu has tremendous operating leverage in the business.

At White Falcon, we initiated this position at around $4 per share. Currently, at a market price of $9 per share, Nu is trading for 21x next year’s earnings (we then essentially bought our position at 10x 2024E earnings!). We have confidence in the credibility of these earnings projections, and we anticipate that this growth can compound consistently at substantial rates over an extended period of time.

We are happy to maintain a foundational investment in Nu for the foreseeable future.

Product

The banking sector in Brazil is highly concentrated and controlled by a small number of incumbent financial institutions. The five giants that tower over the country’s financial system Itaú, Bradesco, Santander Brasil, Banco do Brasil and Caixa Econômica Federal - have over

85% market share in the country. Each of the five incumbents in Brazil has between 2,000 and 5,000 branches and around 50,000 - 80,000 employees each. We believe this legacy infrastructure has translated into a higher cost to serve, incentivizing incumbents to sell high-margin products while excluding a large segment of the population from the financial system. It is estimated that there are 45 mn unbanked individuals in Brazil while at the same time the ROE’s in Brazil are some of the highest in the world due to the highly concentrated nature of the industry. These ROE’s are a direct result of high fees as well as very high interest rates charged to consumers for credit. Brazilian credit cards had interests running 200% to 400% a year!

Nubank launched its first product in 2014. "Roxinho" is a credit card with no annual fee or maintenance fees and is fully digital. This was a purple Mastercard-branded credit card in Brazil.

This card grew like wildfire due to two factors:

- It was 10x better than anything in the market

- Nu created scarcity which was clever marketing

First, this card was better than anything else on the market - it was free, it had low interest rates, and it was all digital. To apply for a card, prospective clients had to download an app and enter some details. They would then receive a preliminary decision within two minutes. Second, a referral programme was built into the app, where someone had to refer you in order to get a card - not everybody could have it! Hundreds of thousands joined the company's waitlist - eager to get a hold of one of the purple cards.

{kind=link}

Nu Bank’s strategy was to start with a single product to ensure they delivered a great user experience but also to gain insights about these customers to refine and improve data models. Again, it is important to remember that customers use their credit cards frequently, making it relatively simple to launch a new product.

Nu Bank followed this initial launch with a rewards program that was again revolutionary in the county for its radical transparency.

According to Nu, their Customer Acquisition Cost ('CAC') was US$7.0 per customer in 2023 and they have acquired approximately 80%-90% of our customers organically on average per year since inception. This has been a key competitive advantage of Nu Bank. They will make money from these customers on credit cards but also when they sell them other services due to which unit economics here are very good.

Nu makes money with interchange fees and net interest income on revolving balances.

Every transaction made in Brazil has a 5% interchange fee shared by the company that produced the card machine (called acquirer), the credit card network (in Nubank’s case is MasterCard) and the emitter banks - Nubank. In addition, Brazil's credit system gives issuers like Nubank thirty days to pay a merchant for a consumer purchase. This is very different from the US, where merchants receive funds in just two days. This dynamic serves Nubank well — the average consumer paid Nubank back in 26 days, meaning the company had a positive cash flow cycle, with four days of float. This essentially means that ROE’s in this business are exceptionally high.

Credit cards are priced at an interest rate of 12% per month which is in-line within the industry. Personal loans, however, is where their data comes into play and rates vary based on the quality of credit. They average 5.6% per month in personal loans while peers charge much higher. It is important to emphasize that credit cards are a high risk/high reward business - while delinquencies can be high - the high interest rates on the remaining portfolio can buttress overall profitability and result in good ROE’s - which is what matters at the end of the day.

In 2017, Nu launched a fully digital banking account solution which offered customers the ability to make deposits, peer-to-peer transfers, payments, and cash withdrawals. The bank also started paying interest on customers’ balances in order to attract deposits and further increase customer’s business with Nu Bank. Unlike competitors, these accounts had no fees or transaction costs which customers appreciated. In 2018, this was followed up with the launch of a debit card. It is important to note that the customers who join by acquiring only a NuAccount typically generate lower initial revenue than customers who start off with multiple products, such as a credit card and a NuAccount. However, these NuAccount-only customers are highly attractive and strategic as Nu become their primary banking account provider and captures a greater share wallet. In 2019, Nu launched a personal loan product for people with larger credit needs. Also in 2019, Nu also launched a Nu business checking account in order to target SME businesses. In 2020, Nu launched insurance brokerage services and investments, following the acquisition of Easynvest, a retail investment platform.

Technology/Costs

Nu Bank’s competitors in Brazil have a lot of branches and a lot of employees - both of which are expensive! In addition, all legacy banks have large and increasing IT expenses - some to maintain the legacy systems and some to enable banks to ‘pretend’ to be digital.

In contrast, Nu’s all-digital, cloud-based platform is low cost, highly efficient and scalable. Nu estimates that their cost to serve and general and administrative expense per active customer is approximately 85% lower than incumbent financial institutions in Brazil.

It is, at its core, a technology company that happens to be in the financial services business. Further, a part of Nu’s mission is to ‘fight complexity’. Nu Bank has built all of its technology stack from scratch using the Clojure programming language. Nu Bank has to solve for scale. As mentioned before, financial services is a scale business. Nu Bank’s technology needs to perform - without complexity - at scale.

{kind=link}

In addition to technology and administrative costs, the other cost that a financial institution has to contend with is cost of funding. In a bank, capital is your basic raw material - you borrow it at a lower level to lend it at a higher level and make a margin. Since the introduction of NuAccount in 2017, Nu Bank has been accumulating deposits which have reduced the cost of funds. Currently Nu is paying the full interbank rate on deposits. The longer term strategy is to offer customers saving products where they can invest their balances in fixed income products and this should further lower the cost of funds. Management believes that their cost of funds can come down to 70-80% of interbank rate which is not that much higher than legacy players whose cost of deposits are ~65% of interbank rate.

At this juncture, it is important to recall Nick Sleep’s lessons. Sleep coined the term “scale economics shared” in reference to Costco’s business model where he found that their strategy of passing the advantages of expanding scale on to customers in further reduced prices, instead of taking profits themselves, gave the business a long-term compounding power unlike its competitors. Nu is no different! It passes the benefits of its advantaged cost structure to customers with no fee and low interest credit cards. With further scale and better data, Nu retains an ability to accelerate this flywheel and pass on lowering of unit costs to customers in either superior products with lower interest rates or better services.

{kind=link}

Risk Management

In their own words, Nu pursues a “low and grow” strategy with credit limits: grant lower limits to new customers who Nu assess as higher risk and then increase those limits selectively based on a positive usage and repayment track record.

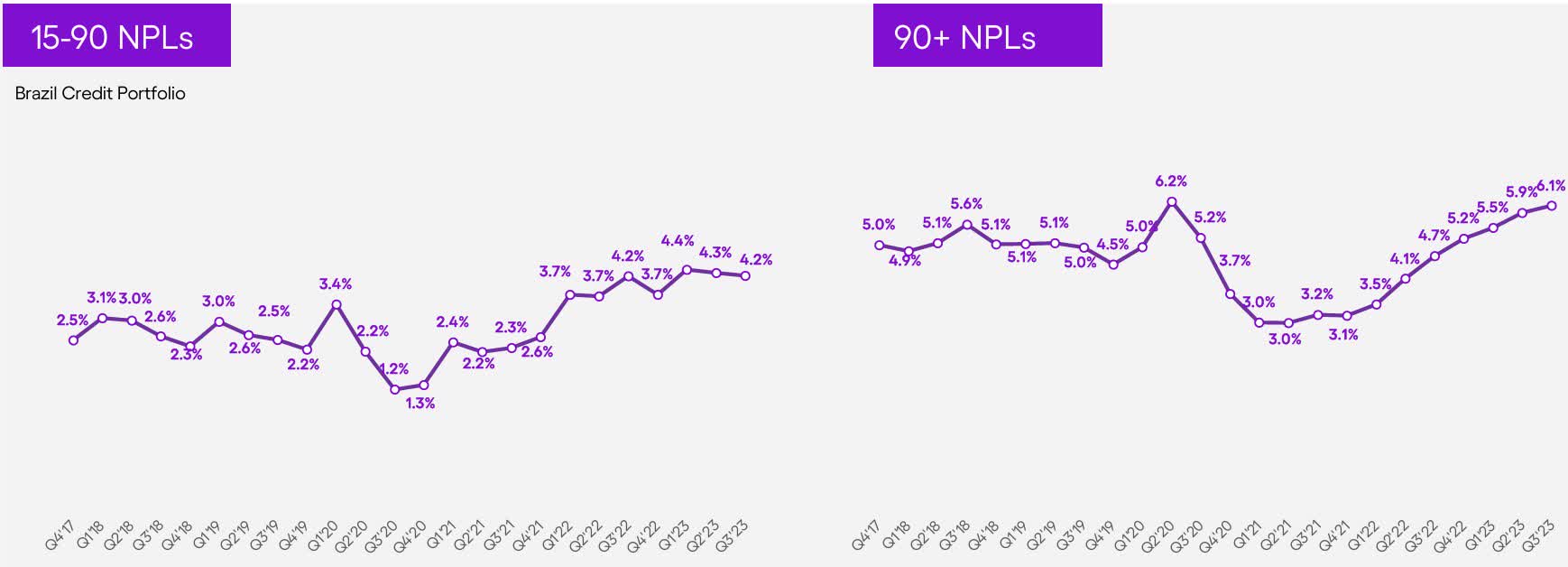

Importantly, Nu generates proprietary data on millions of individual consumers and SMEs. Nu has an internally developed credit engine called NuX which collects more than 11,000 data points per monthly active customer. One such datapoint is how an applicant came to Nubank – the model shows that someone recommended by a well-performing cardholder is likely to be a better credit risk. They use this data to improve underwriting and lower risks. As an example, Nu had a 90-day credit card delinquency rate that is consistently 25-30% better than the competitors.

From its early days, Nubank management has hired former employees of US credit card lender Capital One into risk management roles. Capital One has consistently been good at finding mispriced risk in the card market. It then takes a slow and deliberate approach to raising limits, using payment history to identify “good” credits and grow with the customer - just like Nu!

While investors worry about a recession and its effect on Nu’s credit quality, it is important to remember that Nubank’s credit card business has weathered a period of volatile macro in Brazil, including the 2014-2016 recession. This also likely strengthened Nu’s credit models.

During bad times, bank managements used to have in when and how much provisions to take against the oncoming wave of delinquencies. However, accounting regulations require Nu to take provisions against credit risk up front. So while Nu generates revenue and credit losses from these credit card and personal loan customers over time, the impact of upfront provisioning means that gross profits are artificially depressed especially when growth is high.

Source: Autonomous Research Source: Nu Presentation

{kind=link}

Nu has been growing its share of personal loans. These have a high interest rate but almost no fee income. Due to this, high growth in these loans will have the effect of depressing margins as Nu will have to take all all provisions upfront.

Cross-sell

“So in just a few years we were able to go from a credit card monoliner to achieving leadership positions in the verticals we entered - deposit accounts, personal loans, SMEs, life Insurance and investments - while reaching over one third of the adult population in Brazil. This, to us, represents significant progress in advancing a product diversification and cross-sell strategy.”

- Nu Conference Call

-

Source: Nu Bank Q3 Presentation

{kind=link}

Above we observe three things:

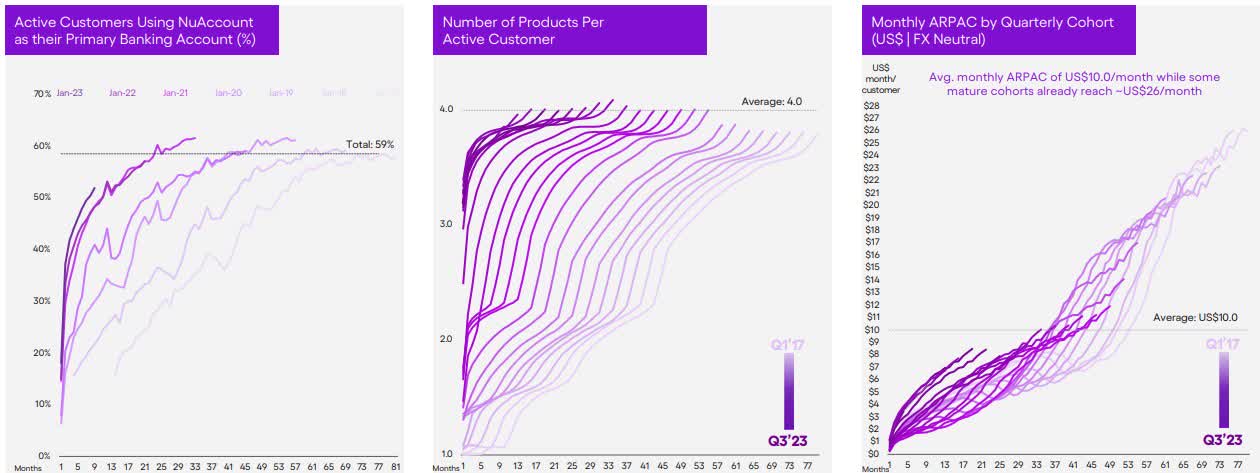

- 59% of active customers use NuAccount which means that Nu Bank is slowly becoming their primary bank.

- With this, Nu is able to sell more products and services to their customers. In 3Q 2023, they had 4.0 products per customer which is one of the best ratios in the world

- More primary customers and more products per customer means that Revenue per user is increasing. In 3Q 2023, this revenue was $10 per customer per month (ARPAC) but some mature cohorts are doing $20+. This metric is very important as we believe that most of Nu’s future growth will come from ARPAC growth. Nu’s competitors in Brazil have ARPAC’s of > $35 per customer per month.

This cross sell flywheel is in full motion and we expect Nu to increase its ARPAC per customer per month to slowly increase to $15 in 2025.

David Velez/Management

David Velez was born in Columbia but his family moved to Costa Rica when he was 9 in order to escape the security situation in the country. After graduating as a valedictorian, David went to Stanford for his engineering degree. Thereafter, he worked with Morgan Stanley and then General Atlantic. During this time, David met Nigel Morris, a co-founder of Capital One and got an opportunity to learn about Capital One’s business model.

After General Atlantic, David then went back to Stanford to complete his MBA. After graduating he started working with Sequoia Capital. He moved to Brazil and was tasked with building Sequoia’s Latin American practice. Over time, David and Sequoia both realized that there was not enough talent or opportunity for a thriving tech ecosystem in Brazil and they abandoned their effort.

David describes his experience in opening a bank account in Brazil,

“When I moved to Sao Paulo for the first time, I had to go to a banking branch and it was the most painful experience I ever had in my entire life. I would describe it as almost going to jail because you have to go to these bulletproof doors, you have to leave your wallet and your cell phone and your bag in a locker outside the branch and go through the bulletproof door and wait 60 minutes and then talk to a branch manager that has a horrible attitude that is always thinking I’m doing you a favor, opening your bank account, and it’s not like, oh, let me really serve you. I had to go to the banking branch maybe 10 times in the course of four months to eventually open a bank account that charged me about $30 per month, an interest rate that was over 400% a year.”

-David Velez, founder Nu Bank

While this experience certainly played a part, I believe David’s conversations with Nigel Morris, the co-founder of Capital One, were more consequential. From Morris he likely learned about Capital One’s business model. He also probably saw Oleg Tinkoff adopting this business model to great success in Russia. He realized that this business model, when applied to the highly consolidated, inefficient and underbanked banking sector in Brazil, could pay significant dividends.

Here is David describing the big lessons studying other technology businesses which helped form Nu Bank’s strategy:

- Consumer obsession

- Building technology in-house

- Superior culture

In 2013, after raising a $2M seed round from Sequoia, David was in business. David’s past experience was as an investor. While he could help set strategy and apply his learnings sitting on the other side of the table from entrepreneurs, he still needed co-founders who could help him execute his vision. Cristina Junqueira, a management engineer from Universidade de São Paulo with an MBA from Kellogg School of Management came on board as a co-founder. Cristina was Brazilian and was working in one of the biggest banks in Brazil, Itaú Unibanco, handling consumer’s loans and credit card business. To build the technology stack, Edward Wible, a Princeton Computer Science grad with an MBA from INSEAD joined as a co-founder.

In August, 2014, they raised a $15M series A round. They launched Nubank’s beta a month later, with the primary value product being a credit card with no annual fees.

Nu came to the market with an IPO in November 2021 and raised $2.6 bn in class A shares. No class B shares were offered. Nu has two classes of shares. The Class A ordinary shares are entitled to one vote per share, whereas the Class B ordinary shares are entitled to 20 votes per share.

Contingent share awards - Nu granted an entity controlled by David Velez a share award where he gets 1% of the firm if the shares, over the next 5 years, are higher than $18.69 per share and another 1% if shares are higher than $35.50 per share. This is somewhat controversial in Brazilian business circles which are not used to seeing such awards. David, for his part, has pledged to donate proceeds from this award to his family’s philanthropic platform. He is also a signatory to the giving pledge.

For its part, Nu Bank is the most ‘international’ of Brazilian financial institutions with talent from all parts of the world working in Brazil. This is unlike other Brazilian companies such as Stone or Pag Seguro. Also unlike the latter institutions, stock is distributed much more widely at Nu Bank.

Bringing it all together with Financials

{kind=link}

The financials are fairly simple,

- Nu has 89 mn clients and makes about $10 mn per client per month. This revenues comes from the interest income on loans as well as fee income from credit cards as well as selling third party products

- Expenses consist of interest expense as well as the expenses related to fee income

- Nu reports its results a little differently from other banks in that it reports its loan loss provisions before gross profit.

- Operating expenses consist of all personal expenses as well as all technology expenses as well as support services to run the business

Nu will grow the number of customers as well as revenue per customer over time. It will do this by cross selling other products and services to its customers. On the other hand, its expenses will decline as a percentage of revenue as more and more products are launched and as these products mature. Over time, we will see the inherent earnings power of the business.

We get a significant acceleration in earnings with an EPS of $0.43 in 2024E and $0.62 in 2025E. At the current share price of $9, this is a P/E of 21x 2024E and 14.5x 2025E. Given growth and quality, we should expect this business to trade at 25x earnings at a minimum; giving a value of $21 in 5 years - more than double from the current stock price or > 15% IRR.

Conclusion

David Vélez found inspiration in Capital One, which had achieved success as a new entrant in the US financial services market in the 1990s and has meticulously executed the same playbook in Latin America. In fact, David went one step further. Instead of building a financial institution that uses technology to serve its clients, David built a technology company that happens to operate in the financial services arena. Nu has a lot of ingredients we look for in a successful investment - a large market opportunity, a profitable business model, and competent management.

Today, Nu is the 6th largest bank in Brazil and expanding just as fast in Mexico and Colombia as it was in Brazil. This is a proven business model and we believe that we are being very conservative in our estimates and that Nu is likely to surprise us to the upside.

| Disclosure: White Falcon has a long position in the shares of NU Holdings. Disclaimer

|

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

White Falcon Capital Q4 2023 Partner's Letter