WHITF - Whitehaven Coal Is Burring Itself In The Coal Pit

2023-11-03 08:15:00 ET

Summary

- Whitehaven Coal had an exceptional FY23 with a 23% increase in revenue and wider EBITDA margins of 66%.

- Despite the positive performance in FY23, the company is expected to face headwinds in FY24 due to lower coal prices, inflation-related costs, and increased capital requirements.

- The Blackwater acquisition for 2.5x EV/EBITDA may pose financial challenges for Whitehaven in a challenging commodity market.

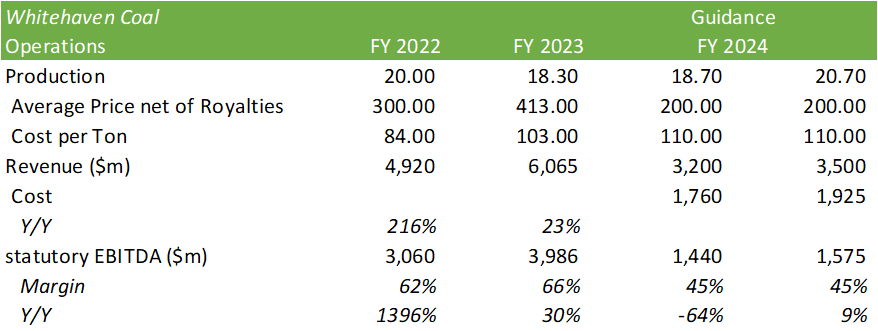

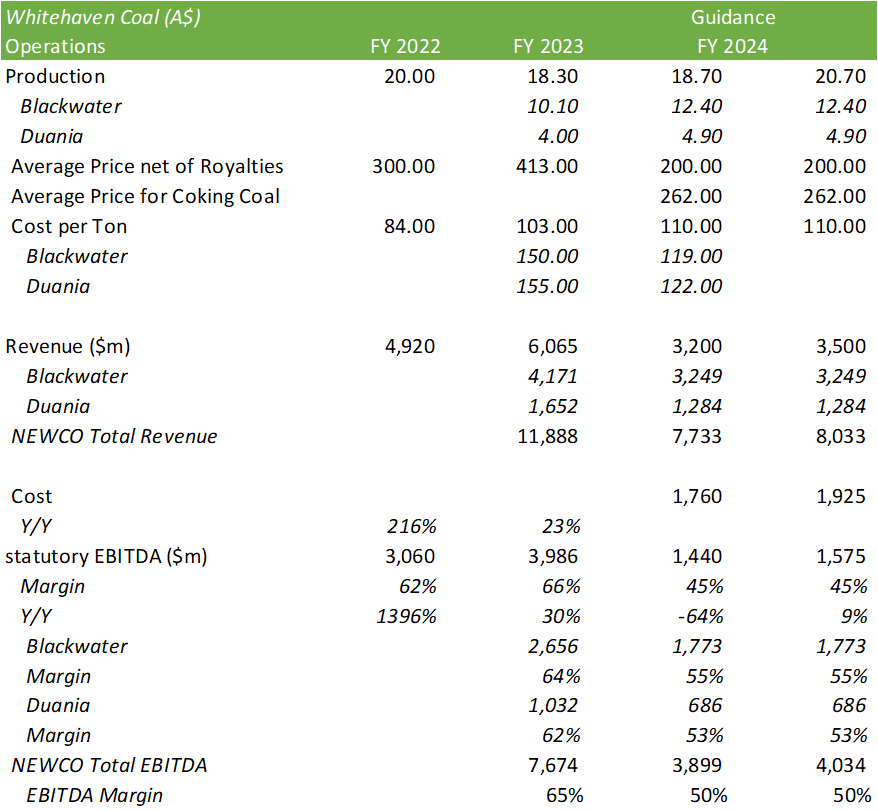

Despite operational challenges as a result of severe weather and inflationary costs, Whitehaven Coal ( WHITF ) experienced an exceptional FY23 with revenue increasing 23% followed by wider EBITDA margins of 66%. This came with exceptional tailwinds in pricing, in which Whitehaven realized an average price of A$445/t coal. As CY23 has progressed and the price for coal has reverted down to a more normalized price, Whitehaven will be faced with challenging comps as the firm invests in the operations of their Vickery mining project. Pre-Blackwater announcement, WHITF shares trade at 0.91x FY23 EV/EBITDA at $4.77/share. Considering the headwinds in pricing for FY24, EBITDA is expected to drop from A$3,986mm to A$1,440mm-A$1,575mm pre-acquisition, based on management's FY24 production guidance. Using a $0.67 USD/AUS conversion, we can come up with a fwd EV/EBITDA multiple range of 2.30x-2.51x. With the recently announced acquisition of the Blackwater and Duania mines, EBITDA can be expected to be closer to A$3,899mm-A$4,034mm with forward multiples adjusting down to 1.42x-1.47x with the expectations of cash and debt financing requirements. The original dividend and buyback policy was to payout 20-50% of net income; however, management has halted the share buyback program as well as the dividend as a result of the Blackwater acquisition terms. Given the current headwinds in coal pricing, capital requirements for mine development, and financing for the Blackwater deal, I provide WHITF a sell recommendation with a price target of $2.85/share at 0.75x EV/EBITDA.

{kind=link}

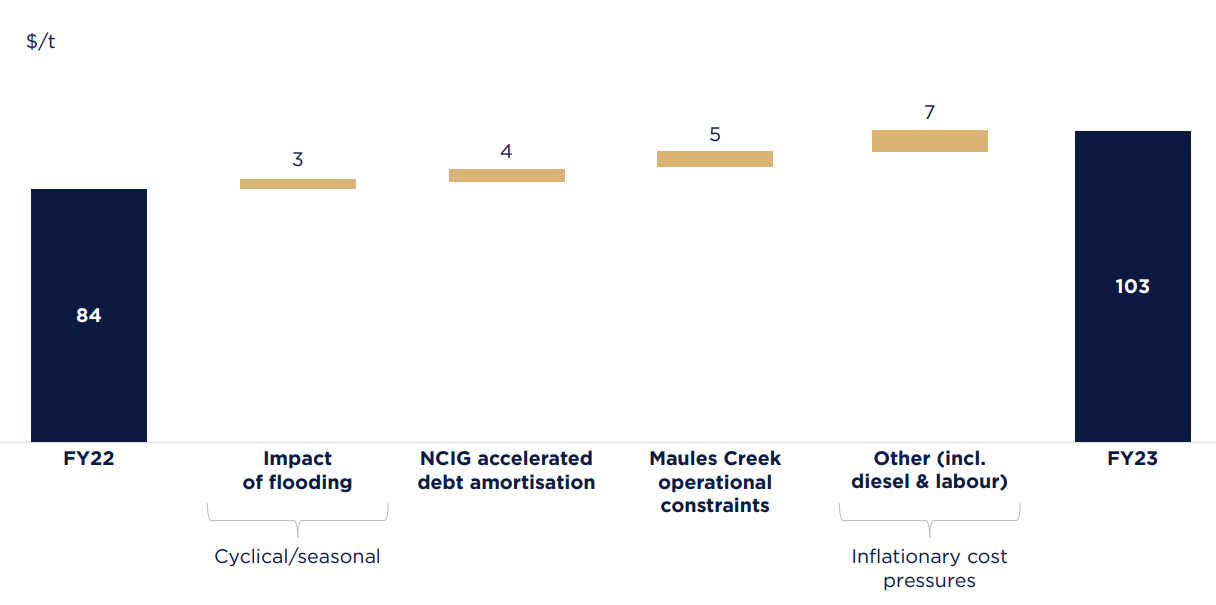

Whitehaven had an exceptional FY23 given the production constraints faced by several factors, including severe weather. Between lower production and inflationary pressures, cost per ton increased by A$19/t to A$103/t. In relation to La Nina, Whitehaven lost 24 days at Maules Creek, 17 days at Tarrawonga, and 36 days for coal haulage to the Gunnedah CHPP during 1h23. Other challenges faced during FY23 included labor shortages and congestion at dumping locations for their Maules Creek operation.

Whitehaven was able to manage their revenue by blending metallurgical coal into their thermal coal blend to realize a higher premium for sales. This resulted in 6% of total sales deriving from metallurgical coal when compared to 18% in FY22. This trend may continue to be necessary as hydrogen is actively being tested to replace coking coal in steel furnaces.

Management did raise an interesting point in that as nuclear energy is more heavily utilized as a fuel source, coal may simultaneously increase in utilization due to the carbon offset in power generation. From a global perspective, this may be a short-term benefit to Whitehaven as new LNG export capacity is being built out across the US Gulf Coast.

{kind=link}

Looking ahead to FY24, despite the massive supply/demand dispersion management laid out in their annual report, it's challenging to see coal returning to the A$445/t (A$413 net of royalties) average selling price, despite their forward guidance.

Corporate Reports

Looking at coal prices today, it appears much of this supply/demand dispersion has tightened, with new supply coming online. According to Trading Economics, coal power demand surged by 9.9% for the month of September, with China increasing coal imports by 27.5%. Considering China's easing of the coal import ban from Australia in January 2023, it doesn't appear to have changed the global market pricing for coal.

{kind=link}

Converting for AUD/USD at $1.58/USD, coal is currently priced at ~A$195.13/t.

Despite the IEA's anticipation of coal-fired power plant decommissioning, it appears that coal has the potential to remain a resilient power source through at least 2030. In total, China consumed 8.6 gigatons of coal in 2022, accounting for 70% of the country's energy mix. As of this writing, China has 100GW of coal capacity being constructed , with an additional 50GW planned. Though China isn't necessarily a primary destination for Whitehaven's coal, it will potentially increase or at the minimum balance out the capacity as coal plants are decommissioned elsewhere .

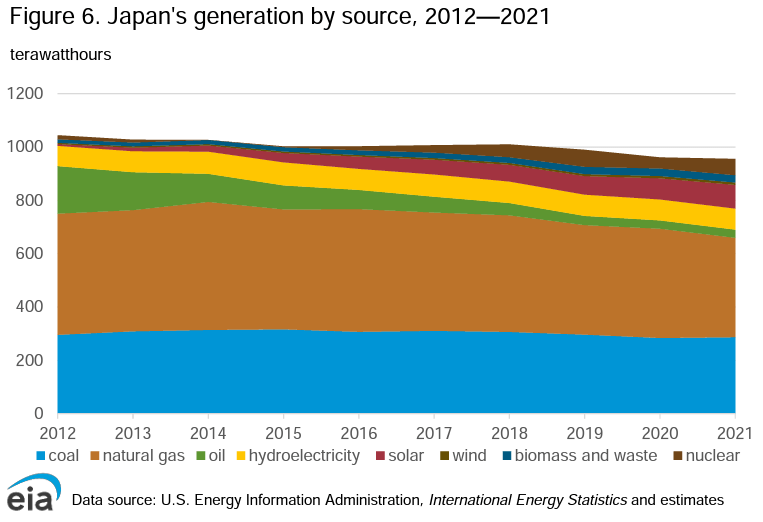

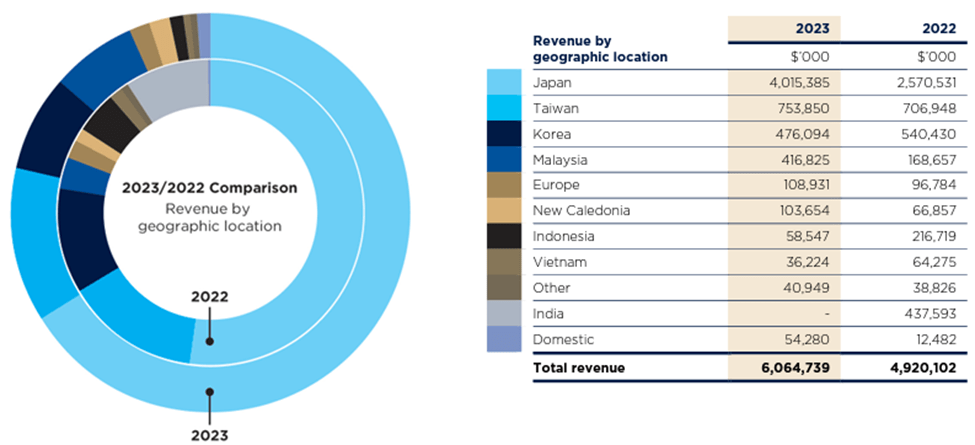

The primary destination for Whitehaven's coal is Japan, South Korea, and Taiwan. Japan alone accounted for 66% of revenue for 2023, a 14% increase from the previous year. Accordingly, the EIA reported that 32% of Japan's power generation in 2021 was attributable to coal, with a mere 3% to nuclear. Natural gas is their largest source of power generation at 42%.

{kind=link}

There is a lot of promise in coal demand coming from India. As India further industrializes, more demand for metallurgical coal for steel production is expected to come. Management has very high expectations for the demand for metallurgical coal to outpace supply in the coming decade.

"Pricing in metallurgical coal markets been strong in 2022 and 2023, and is expected to remain well supported in the near future. In the medium to longer term, growing industrialization and urbanization in India together with South East Asia is expected to underpin robust pricing. India has committed to significant steel capacity expansion, and new manufacturing capacity is being built throughout South East Asia, both of which are translating directly into increased demand growth for seaborne metallurgical coal. China's influence on the seaborne metallurgical coal market has been tempered in the short term due to a slowing economy and a slowdown in major stimulus projects. In the coming decade, metallurgical coal demand is expected to exceed supply due to depletion and closure of current mining operations compounded by the challenges of bringing new supply to market."

- Paul Flynn, Managing Director & CEO

{kind=link}

India has run through some challenges in their coal industry this past year. In an attempt to bolster its domestic coal production, the Indian Coal Ministry announced a ban on coal imports from 2023-2024 . This has led to a severe drop in coal inventories, the fastest rate in two years as electricity demand has outpaced supply.

{kind=link}

Making matters worse, coal-fired power generation increased 33% y/y as utilities faced a 20.4% increase in power demand with a -26.8% decline in hydropower output. Due to the shortage, India elected to extend imports by 8 months to keep power plants operating. Given the drop of revenue deriving from Indian coal imports, Whitehaven should experience a significant increase in volumes shipped to India for FY24.

Overall production declined from the previous year by 9%. Much of this was the result of Maules Creek's -15% y/y decline in production due to localized flooding. The Gunnedah open cut mines lost -15% of annual production due to the La Nina flooding. Some of this loss of production was made up by Narrabri's 9% increase in production from the previous year. As a result of the lower production, coal stocks were drawn down by 0.8Mt, or -36% to meet sales commitments.

{kind=link}

Capital Investments

Whitehaven invested A$150mm for early commencement of mining their Vickery coal deposit in April 2023. Work commenced in the June 2023 quarter to advance the Early-Stage Mining project, with feasibility works still ongoing. As of FY23, Whitehaven has approval from the NSW Independent Planning Commission to operate at upwards of 10Mtpa of metallurgical and thermal coal with onsite processing and rail infrastructure.

Whitehaven is expecting to spend between A$460-570mm in capex for FY24. This spending includes A$220-250mm in development and growth investment. This will primarily reside in the Vickery project, with roughly $180-200mm to be directed.

Financials

With the price per ton of coal significantly suppressed from the previous year, it's challenging to expect Whitehaven to achieve the same operational success in FY24. Given management's production guidance and a baseline assumption for higher production costs and lower price per ton, we can expect a ballpark A$1,440-1,575 in EBITDA generation for FY24. This figure may look significantly different as the price of coal can fluctuate at any given moment based on geopolitical risks; however, this is very much a baseline presumption based on forward estimates.

{kind=link}

Due to the Blackwater acquisition, dividends and share buybacks have been halted until further notice. Net of the dividend and buybacks being placed on hold during the Blackwater mines acquisition, we can set some expectations for the shareholder returns in normal circumstances if the acquisition were not to occur. Their dividend and share buyback policy in place before the acquisition announcement was to pay out 20-50% of net income in the combination of share buybacks and a dividend. Given the assumptions laid out above, we can expect somewhere between A$70mm-A$138mm in net income for dividends and buybacks with the assumption management maxes out at the 50% distribution limit. With these assumptions along with the same payout ratio from FY23 of 24%, we could have expected the dividend to decline to $0.02-$0.04/share with the remaining A$53mm-A$104.50mm to be utilized for share buybacks.

Doing a deeper dive on the Blackwater and Duania acquisition, assuming constant pricing for coking coal at A$262/t as well as assuming management's production and cost forecast, we can insinuate that future value accretion may be realized. Looking back to FY23, consolidation would have reduced the firm's profitability.

{kind=link}

Valuation

There are additional challenges to consider in relation to the recently announced Blackwater acquisition. This deal will cost a total of A$3.2b and will require an additional A$900mm in debt to finance the deal. With the expectation of the upfront costs being A$2.1b with A$900mm financed with debt, we can expect A$1.2b cash to cover the remainder of the cost. This upfront cost is net of A$1.1b in future contingencies that is expected to be paid off through operating cash flow. With these figures, we need to adjust their net debt to -A$487mm, which adjusts their enterprise value to $3,812mm for an EV/EBITDA of 0.75x from the pre-acquisition of 0.91x. With these figures in mind as well as the production headwinds faced in FY24, I give WHITF shares a sell recommendation with a price target of $2.85/share for a multiple of 0.75x EV/EBITDA.

For further details see:

Whitehaven Coal Is Burring Itself In The Coal Pit