YACAF - Whitehaven Coal: Missed The Coal Rally? No Worries

2023-12-29 10:12:19 ET

Summary

- Whitehaven Coal is acquiring met coal mines, positioning itself as one of Australia's largest met coal producers by 2024.

- The company benefits from structural secular tailwinds, including supply and demand imbalances in the coal market and increasing demand for energy security and transitions.

- With a low P/E ratio of 2.5x and a strong net cash balance of A$2.45 billion, Whitehaven Coal presents value for investors.

- WHC ‘s clean balance sheet, high-quality management and generous dividend distributions make Whitehaven Coal a shareholder-friendly company.

- Whitehaven Coal is one of Australia’s largest high CV seaborne thermal coal producers, owning more than 6 coal mine assets located in New South Wales and Queensland.

Introduction

Coal has been a hot topic among investors lately. We have seen Coal Stocks like Alpha Metallurgical Resources ( AMR ) rallying 100% in 2023. Missed the boat? No worries, I have found one interesting value coal stock in Australia, which is named Whitehaven Coal (WHITF)

What if I tell you that the company has an FCF and earnings yield of 53% and 43% respectively, while having a 10% dividend yield. Does it really make sense? If the stock were to be listed in the US, I am sure that market participants would assign a high valuation multiple to it.

Nevertheless, Whitehaven is now trading unreasonably low valuations (2.5x PE) in Australia. It has the potential to outperform the market in the long term, I rate WHC as a “Strong Buy”. Without further overdue, let’s dive deep into the business.

Business Overview

{kind=link}

Business Overview (WHC 2023 Investors Presentation)

To those unfamiliar with the company, Whitehaven Coal is an Australian Coal Miner that mines and produces both Thermal Coal and Metallurgical Coal (Met Coal), both used in energy generation and steel production respectively.

Currently, WHC operates six coal mines in Australia, spreading across the Gunnedah Basin in Newcastle, New South Wales (Vickery, Narrabri & Tarragona Mines) and Bowin Basin in Queensland (Winchester South). Coal produced in these mines are then processed to clean out impurities. Subsequently, they are railed to the port of Newcastle or ports in Queensland and shipped across Asian countries.

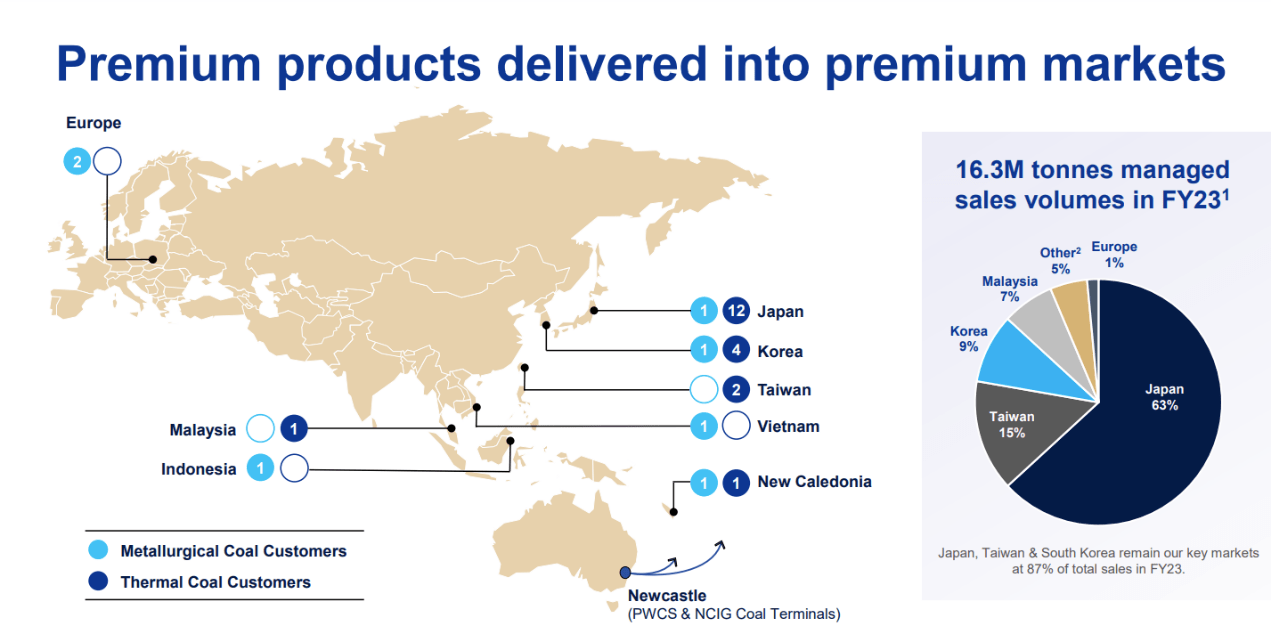

Coal exported by Whitehaven are either sold to European or Asian regions, including Japan, Taiwan, South Korea, and Malaysia. Nevertheless, compared to its competitors like Yancoal (YACAF), Whitehaven is less susceptible to geopolitical tensions between Australia and China as most coal is exported to ex-China Asian regions.

Leadership in production of High CV Thermal Coal

{kind=link}

High-CV Thermal Coal (WHC 2023 Investors Presentation)

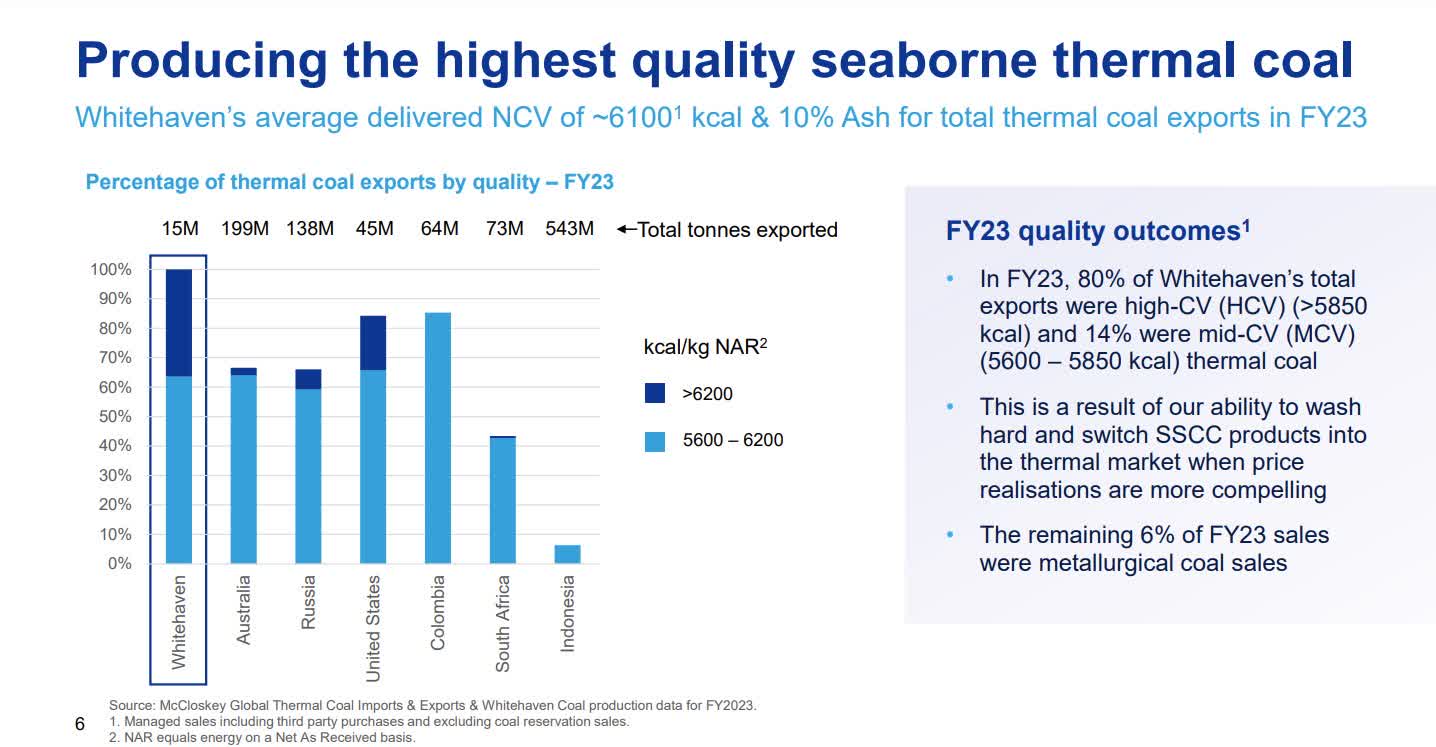

One significant competitive advantage that Whitehaven Coal differentiates itself from its Australian counterparts is the high-quality seaborne thermal coal that it produces and exports.

Prior to the acquisition of coal mines from BHP, more than 80% of coal exported from WHC was high-CV coal, while 14% of them were mid-CV coal. The remaining 6% were metallurgical coal.

To put things into perspective, thermal coal could be classified into several classes based on its quality, carbon energy content, and moisture level. Hard thermal coal includes high-calorific coal (HCV Coal) or Mid-calorific coal (MCV Coal). High CV Coal tends to produce more energy more efficiently with less ash and carbon dioxide, which makes it more compelling and environmentally friendly for customers.

{kind=link}

Coal Feed Rate (WHC 2023 Investors Presentation)

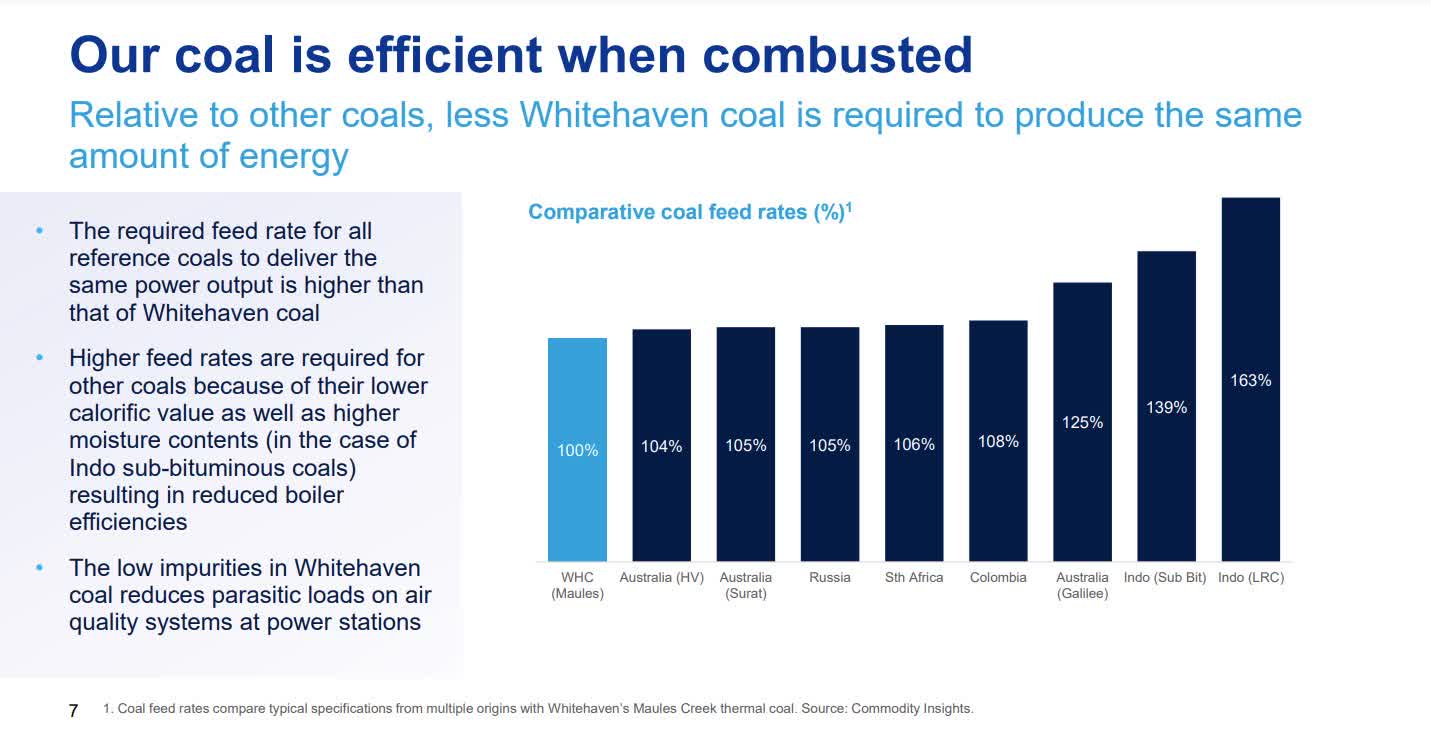

As we can see, high CV thermal coal (Bituminous Coal) produced by WHC has lower moisture level and higher calorific value, this warrants higher energy conversion rates and lower impurities levels for its thermal coal than its sub-bituminous counterparts.

The Coal feed rates of WHC (100%) remains marginally lower than its Australian average (104%), which implies less coal is needed to deliver the same power output for power stations. Furthermore, high CV coal produced by Whitehaven has an average 27% fewer carbon emissions than its Asian coal producers.

Going forward, I expect Whitehaven to retain its dominant and industry leading position in the Coal Mining Sector in Australia given its production leadership in High CV Coal. Furthermore, tighter environmental regulations warrant higher entry barriers for new coal miners to enter the Australian coal industry. This creates an economic moat around Whitehaven.

Thermal Coal is not fading for the coming decade

I acknowledge there have always been concerns and controversies regarding the long-term viability of coal as most people are engrossed with renewable energy and carbon transitions to Net Zero. Thermal Coal, on the other hand, as a non-renewable source of energy with relatively high emissions, would eventually be phased out for the coming decade under the ESG movement.

While such an argument looks convincing at first glance, this doesn’t really hold water, in fact, in my opinion.

{kind=link}

Coal Demand Forecast (WHC 2023 Investors Presentation)

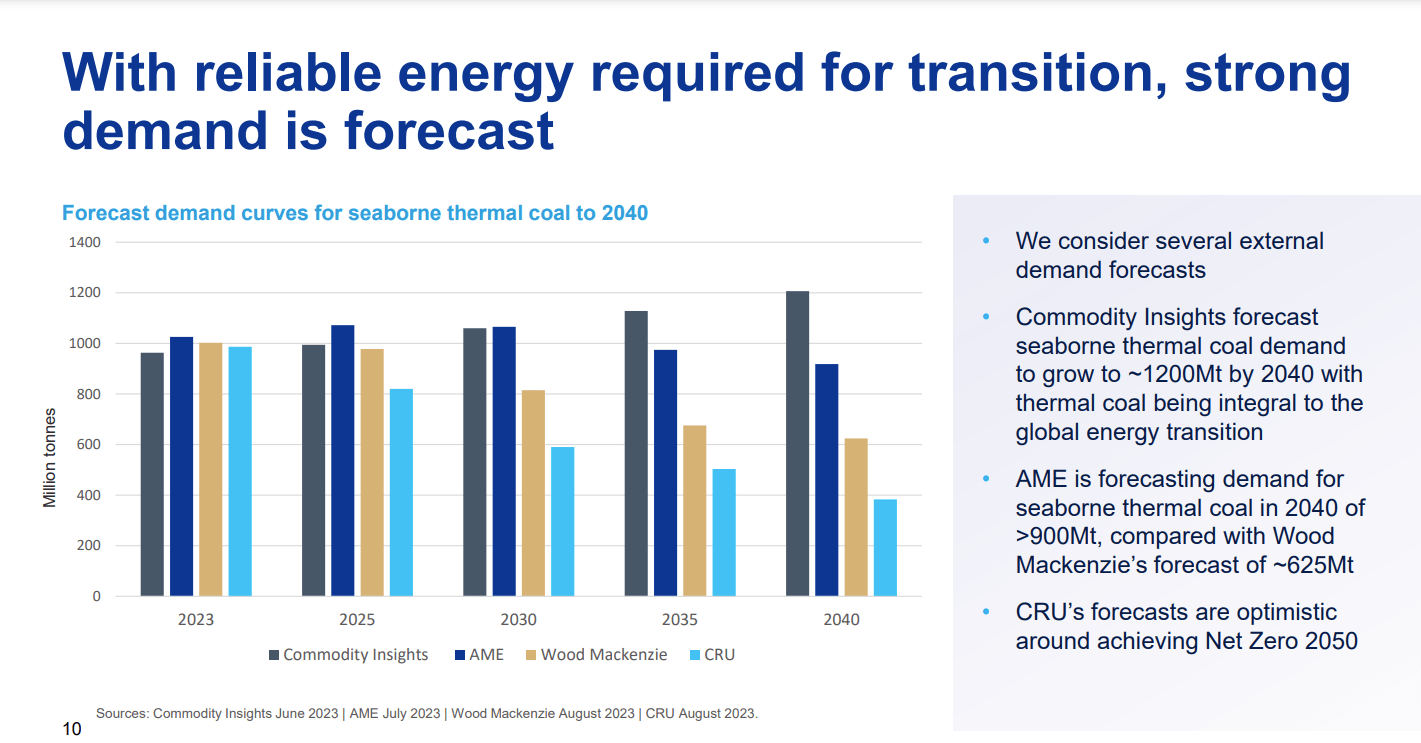

According to Whitehaven, seaborne thermal coal demand is expected to elevate from 900 million tons annually in 2023 to more than 1200 million tons annually in 2030 despite calls for ESG energy transitions. Structurally, there has always been prevailing demand for thermal coal, especially from emerging markets like China, India, and Malaysia for energy production, due to its low costs and high energy conversion and output rates.

Based on S&P Global , India is expected to increase thermal coal imports to 186 million mt in 2024 and 193 million mt in 2025, up from 150 million mt this year due to its growing electricity demand and falling coal inventories.

{kind=link}

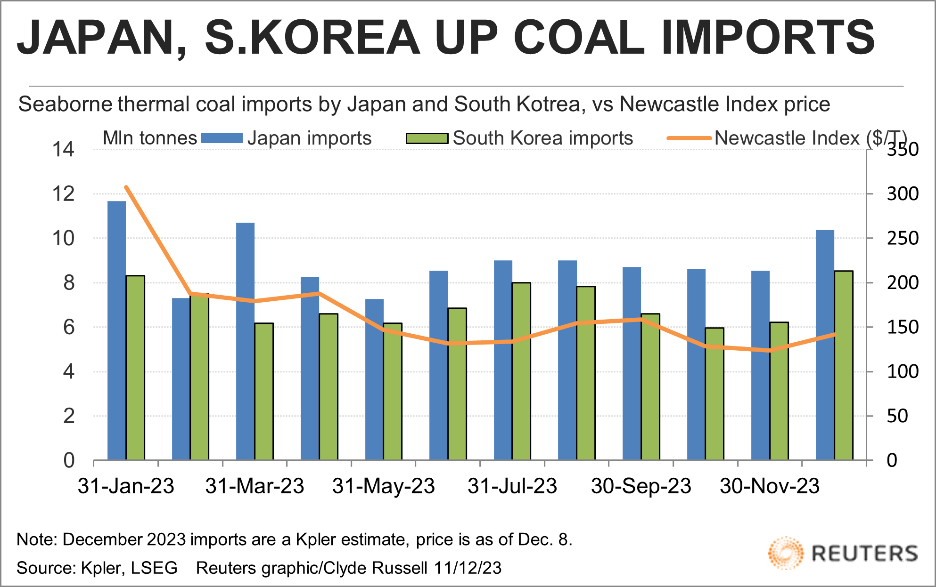

Japan & Korea Coal Demand (Reuters)

Meanwhile, according to Reuters , Japan and South Korea, the 3rd and 4th largest global thermal coal importers respectively, have shown no signs of abandonment for thermal coal in 2023, which has seen robust demand for high CV coal. I think this trend will benefit Whitehaven, who has been shipping 63% of its coal volume to Japan and 9% to Korea respectively.

Japan has imported an estimated 10.37 million metric tons of seaborne thermal coal in December, whereas South Korea's imports of seaborne thermal coal are forecast to reach 8.59 million metric tons in December, the highest since July 2021, and up 13.8% from 7.55 million in December last year.

{kind=link}

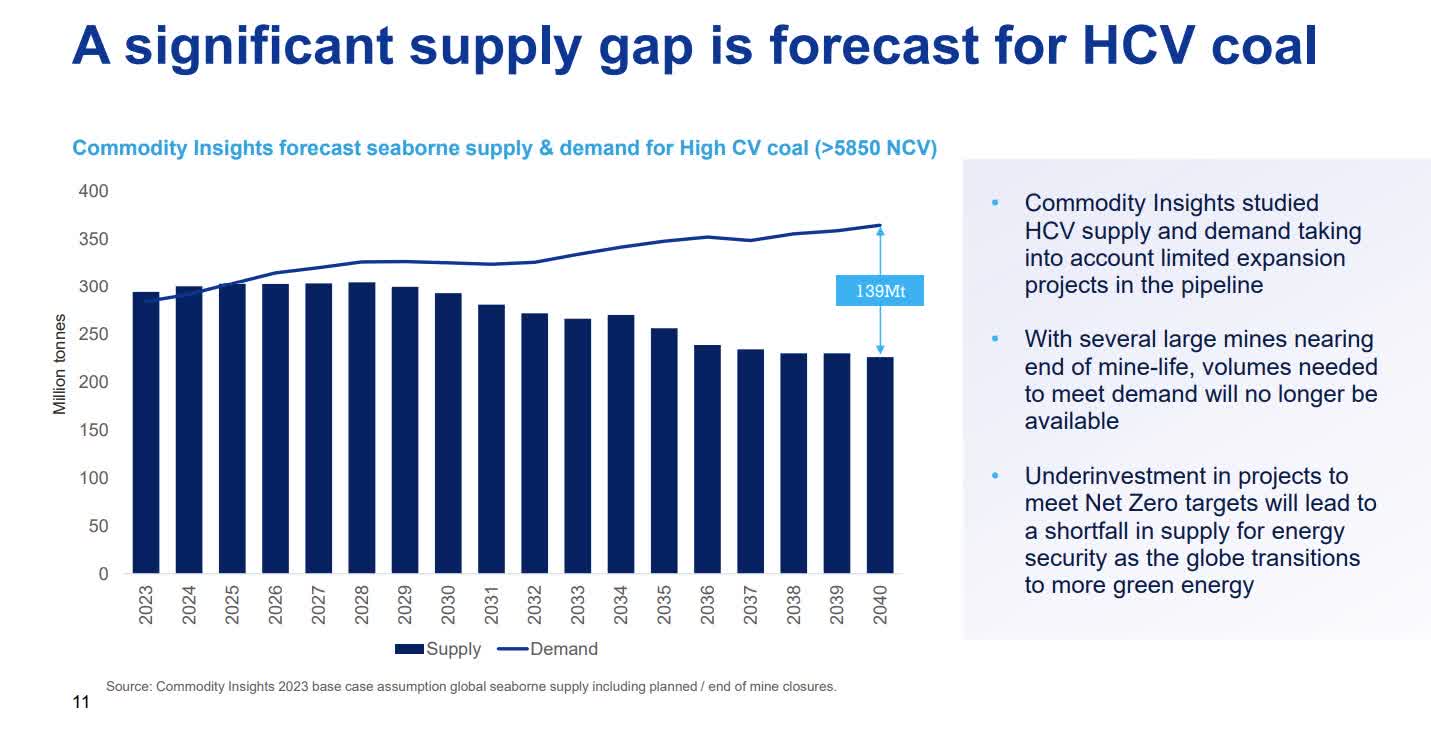

Coal Demand-Supply Imbalances (WHC 2023 Investors Presentation)

Going forward, with greater supply and demand imbalances expected, thanks to the expected closure of large coal mines as they approach the end of their mine-life and tighter entry barriers for new miners, I think this shall result in secular supply reduction and support HCV Coal Price over the long-run. Whitehaven remains well-positioned to take full advantage of this imbalance predicament.

Acquisition of Coal Mines from BMA: Pivots to become the largest Australian Met Coal producer

{kind=link}

Daunia & Blackwater Coal Mines (WHC 2023 Investors Presentation)

The management team of Whitehaven has long envisioned to transition itself from a thermal coal producer to a metallurgical coal producer.

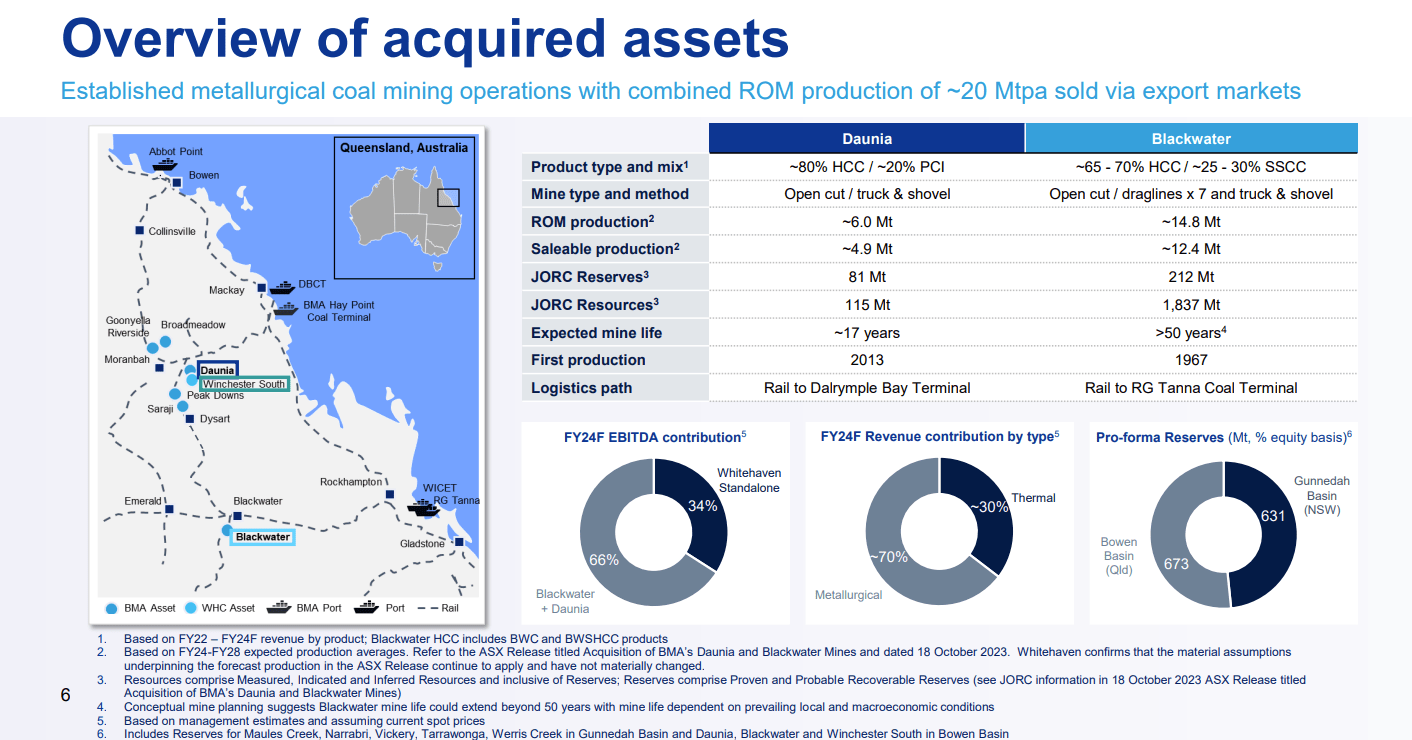

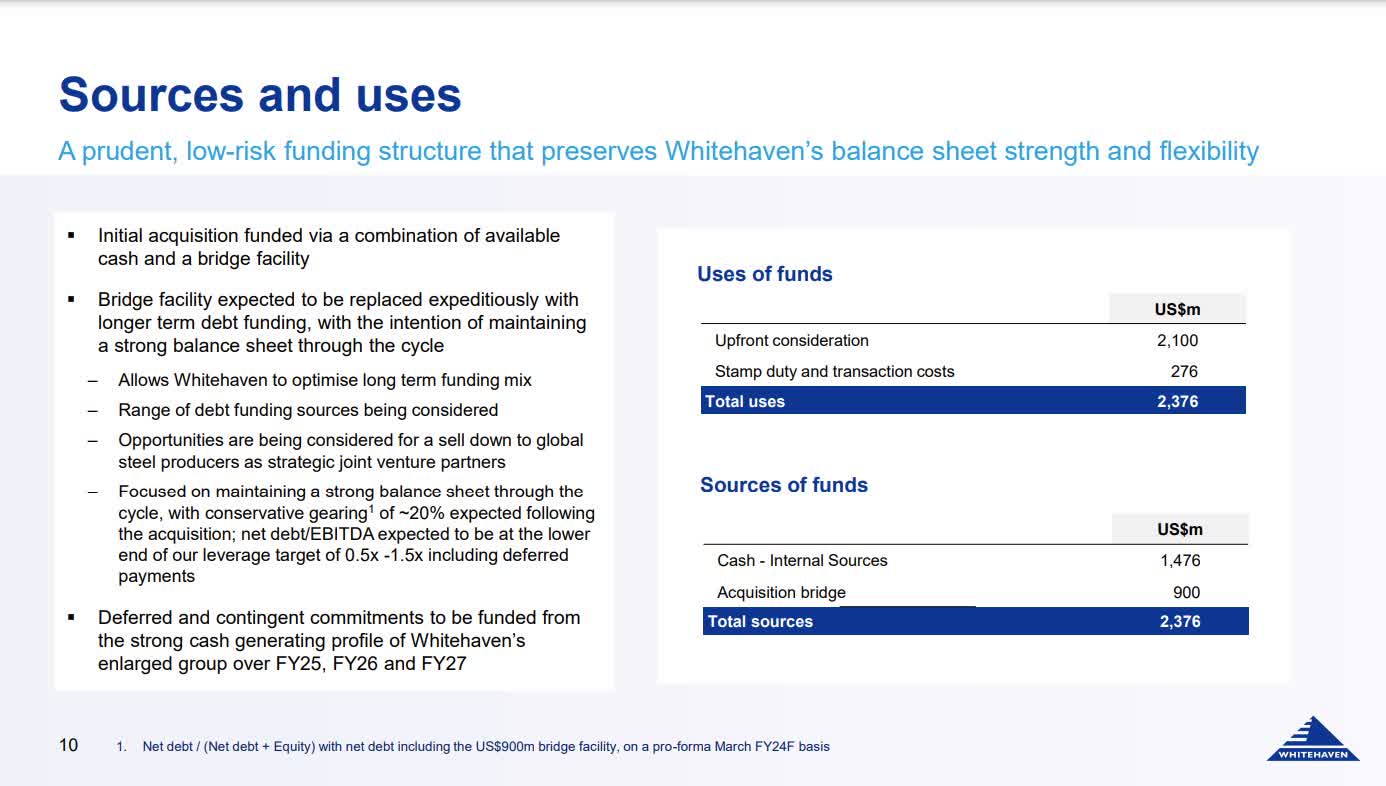

The management took advantage of the acquisition deal to purchase 2 coal mines (Daunia and Blackwater mine) based Bowen Basin in Queensland from BMA (a joint venture between BHP and Mitsubishi) for an estimated $3.2 billion, which would be settled in $2.1 billion of upfront cash and $1.1 billion of periodic payments from 2024-26.

The great news for Whitehaven shareholders is that no new shares would be issued to finance the deal. The whole amount would be settled via cash in hand ($2.3 billion) and a $900 million credit facility (Debt).

The acquisition valuation also makes much sense in my opinion, which trades at an implied transaction multiple of EV/EBIDTA just 2.5x, slightly below the industrial average multiple of 2.7x. Furthermore, management team is expected to bring in an incremental 70% increase in EPS after the deal, which makes great sense for striking the deal in my opinion.

Personally, I think that it’s a short-term pain, but a long-term gain story for Whitehaven shareholders, here’s my thesis.

Enhanced Production Capacity

{kind=link}

ROM 2024 (WHC 2023 Investors Presentation)

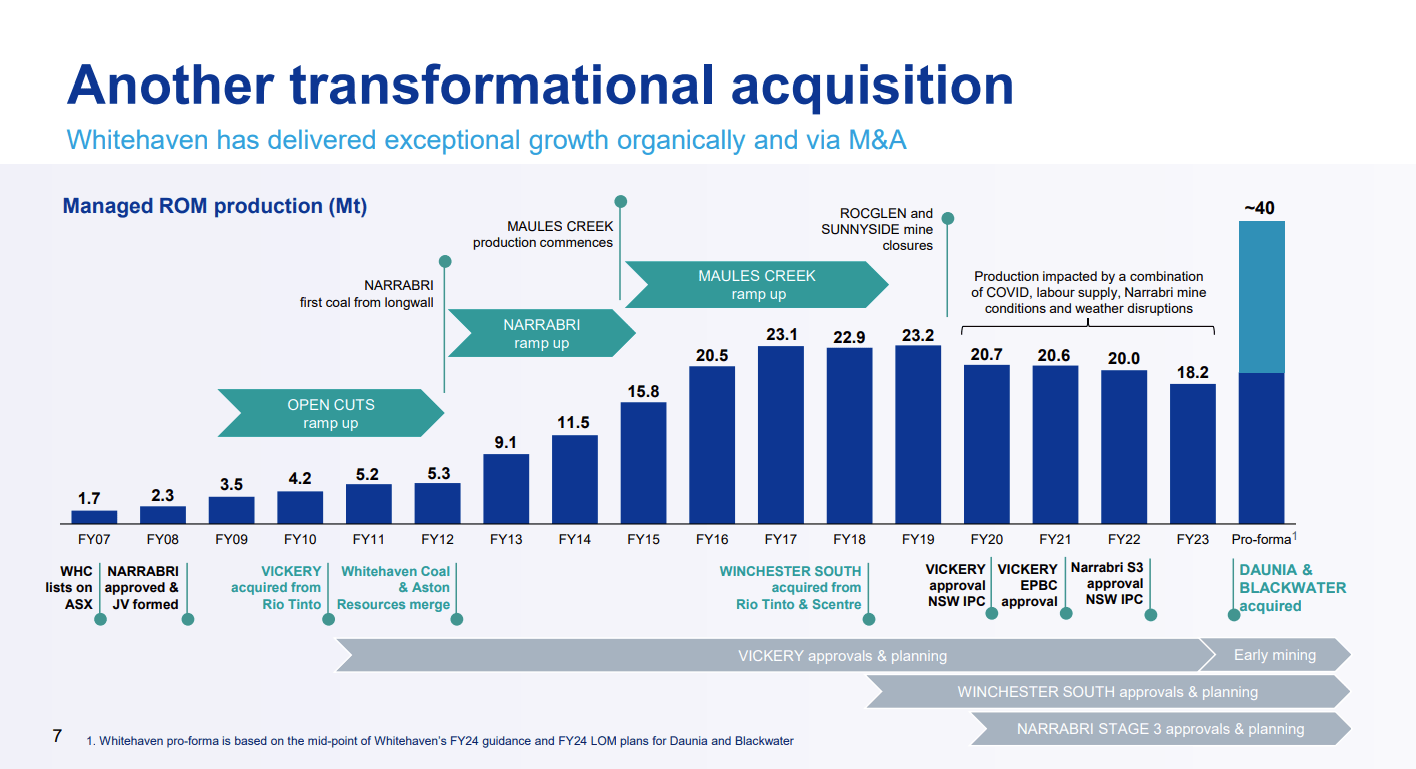

As of 2023, Whitehaven has a Run-of-Mine ((ROM)) production volume of 18.2Mt per annum, which dwarfs significantly in terms of production volume comparing to its competitors like YanCoal (50 Mt) and BHP ( 70 Mt per annum)

Acquiring the Daunia and Blackwater Mine from BMA would more than double the Whitehaven’s projected ROM to 40Mt per annum, which allows it to surpass its competitors like Anglo American and Mitsubishi, ranking 3 rd in Australia domestically behind BHP and Yan Coal in terms of production volume.

These mines produce high-quality seabound met coal, including Hard Coke Coal ((HCC)) and SCC (Semi-hard Coke Coal), diversifying Whitehaven’s operations away from its traditional thermal coal business. The management team is expecting the Blackwater and Daunia mine to have an estimated mining life of 50 years and 20 years, respectively.

With expanding production facilities, I think Whitehaven could easily double its salable production capacity from 17 Mtpa to >32 Mtpa in 2024, thus bringing in more revenue and cash flow to the firm in the future.

Diversified business operations

{kind=link}

Coal Sales Mix (WHC 2023 Investors Presentation)

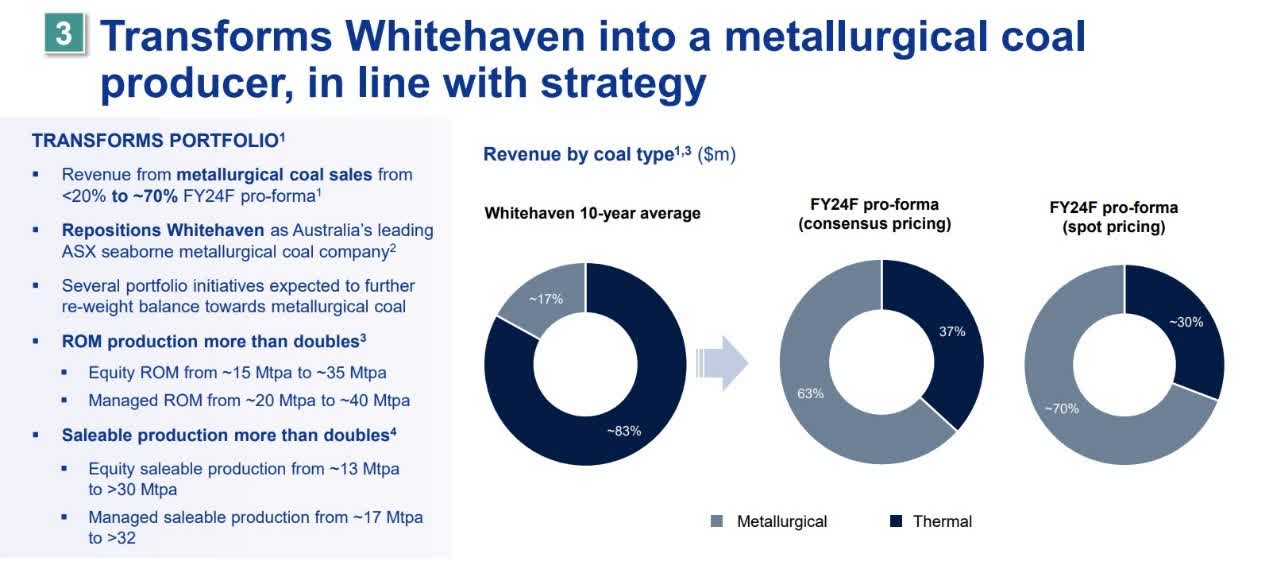

By acquiring two coal mines from BMA would significantly expand Whitehaven’s footprint in the Met Coal sector. Before the acquisition, the sales mix between thermal and met coal is 83% and 17%, respectively.

Taking over two met coal mines would transform how Whitehaven generates revenue over the long run. 63% of revenue is expected to come from Met Coal, while the remaining 37% of revenue would come from traditional high CV thermal coal in 2024, effectively making Whitehaven a met coal producer.

This would be great news to Whitehaven’s shareholders for several reasons. First, Steel is a critical component of economic development. Met Coal is used for steel making in furnaces, and steel is a significant input for infrastructure development and renewable energy.

This would allow Whitehaven to gain business exposure to the vibrant infrastructure development in developing Asia, particularly in ASEAN and India going forward. Second, Met Coal tends to be sold at a higher price than thermal coal. This would probably advance Whitehaven’s gross margin and profitability going forward.

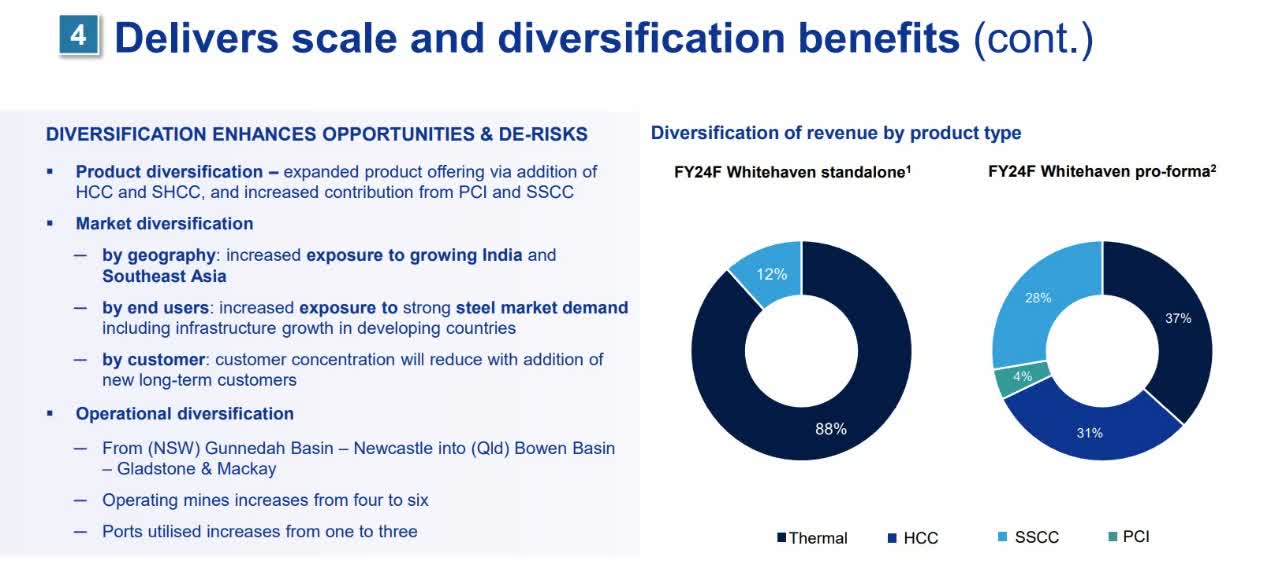

{kind=link}

Product diversification (WHC 2023 Investors Presentation)

The 2 coal mines in Daunia and Blackwater is expected to play a pivotal role in supplying High Quality Met Coal like HCC and SCC (Semi-hard Coke Coal) to Asian countries in the coming few decades, which opens a huge addressable market for WHC to exploit in the future.

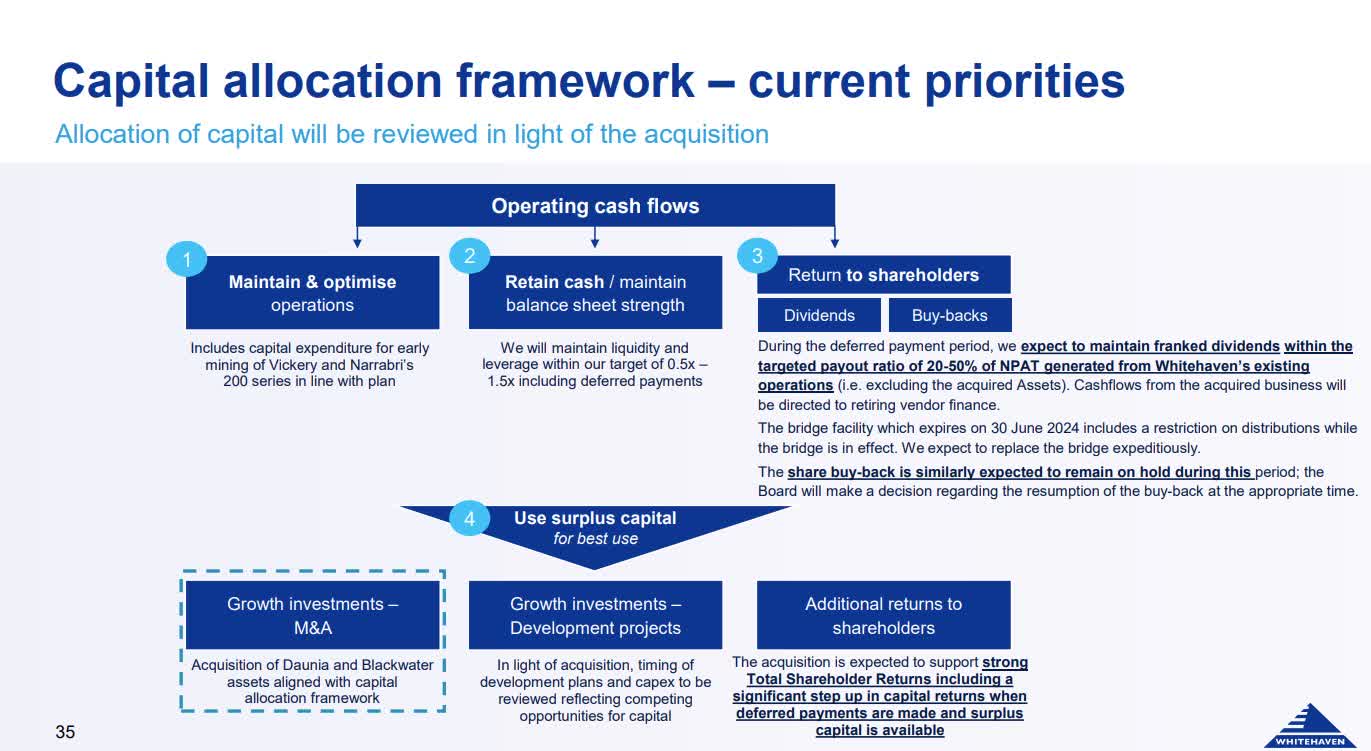

Short-term pain: Share buybacks cuts

Before acquiring 2 coal mines, the management team is committed to returning at least 20-50% of Net Profit After Tax (NPAT) in the form of share buybacks and dividend distributions.

Ever since the management team announced share buybacks in early 2022, the outstanding share count has fallen from slightly over 1 billion in early 2022 to only 836.6 million shares as of December 2023. This implies a 16% reduction in share count in the space of just two years, which is quite astonishing. Purchasing shares at PE levels of (2-2.5x), when they are undervalued warrants gains from existing shareholders.

{kind=link}

Capital Allocation Decisions (WHC 2023 Investors Presentation)

Nevertheless, thanks to the acquisition deal of 2 new coal mines, the share buyback program will be suspended until further notice when deferred payments are settled and surplus cash is available .

As a result of that, one of Whitehaven’s largest shareholders – Bell Rock Capital Management, a London-based hedge fund with 11% ownership interest before its divestment, has halved its ownership position and sold down $260m worth of shares to voice out its opposition against the coal mine acquisition plan as this would undermine capital return programs.

Despite the divestment campaigns from hedge funds, I would argue long-term v alue investors to ignore the short-term buzzes and focus on the greater picture. Analysts at Citi argued that the purchase would push earnings per share for Whitehaven up by 93 per cent in 2025.

With greater production in Met Coal and large sales volume, I think this deal would enhance Whitehaven’s cash flow generating abilities and profitability as higher margin met coal could be sold to Asian customers upon the acquisition of 2 met coal mines. I expect share buyback programs to resume in 2025-26 once the company generates more significant FCF.

Financial Analysis

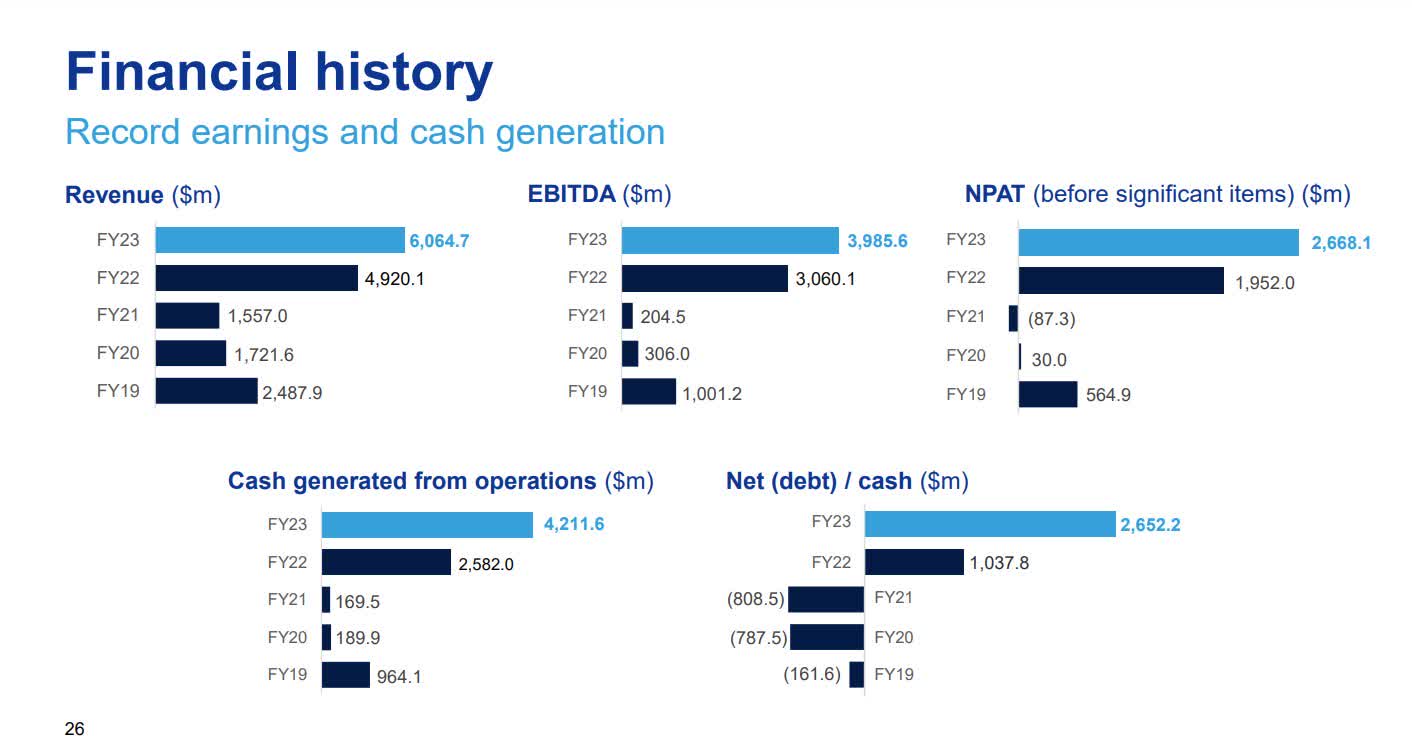

1. Strong Revenue and Margins

{kind=link}

Financial Analysis (WHC 2023 Investors Presentation)

Overall, FY 2023 has been a remarkable year for Whitehaven Coal. Revenue reached A $6.06 billion ($ 4.13 billion) in 2023, up 23% compared to A$4.92 billion in 2022. This was primarily driven by an increase in coal price, which has seen WHC’s overall realized coal price reaching A$445/ton in 2023, up 37% compared to A$325/ton in 2022. Overall, Whitehaven’s top-line and bottom-line growth hinges on the movements of coal prices.

A s for EBIDTA, EBITDA reached historical highs, which peaked at A$3.986 billion in FY23, up 30% YoY compared to A $3.060 billion in FY22. EBITDA margins remained at 65.7%, similar to YanCoal (65%).

Net Profit after Tax (NPAT) reached A$2.668 billion, up 37% from A $1.952 billion. Net margins remained at around 44%.

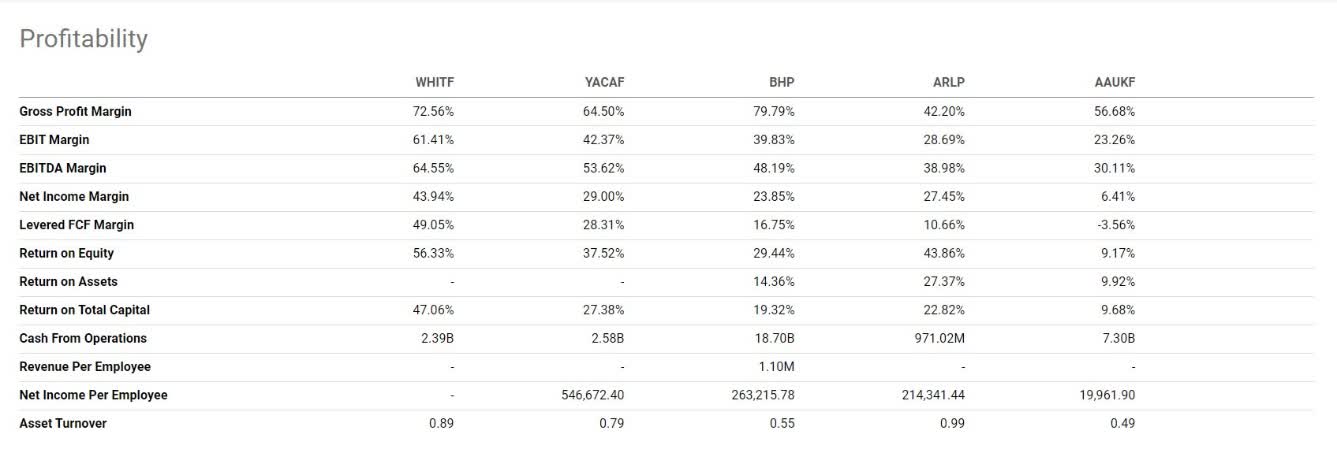

{kind=link}

Profitability Comparisons (Seeking Alpha)

I have compared how Whitehaven performed against its competitors like YanCoal Australia, BHP Group ( BHP ), Anglo American Plc and Alliance Resources Partners in terms of profitability. As shown, Whitehaven is the most profitable coal business of all.

WHC recorded a Gross margin and Net Margin of 72.56% and 43.94% respectively, which remains overwhelmingly higher than YanCoal Australia (64.5% & 29%) and BHP Group (79.8% and 23.9%) respectively.

As a value investor, I prefer owning businesses that have the most robust profitability and highest margins business, which could generate impressive returns on invested capital (47%).

2. Clean Balance Sheet

Another thing I like about Whitehaven is its clean balance sheet. As of Sep 2023, Whitehaven has a healthy net cash position of around $2.45 billion, generating around $269 million of cash from operating activities.

Nevertheless, acquiring the two aforementioned coal mines is expected to deplete around $1.47 billion for cash upfront payments. Therefore, I forecast WHC’s net cash balance to shrink to around $300-400 million in 2024. The management team has also taken out a $900 million acquisition bridge facility to finance the deal, which would eventually be replaced by long-term debt.

{kind=link}

Source of Funding (WHC 2023 Investors Presentation)

Despite the debt borrowings, the management team remains committed to maintaining a solid balance sheet, which sets a conservative gearing ratio of 20% and a leverage (Debt/EBITDA) target of 0.5x -1.5x.

Given the management team’s historical track record of delivering shareholders-friendly policies through continuous share buybacks and dividend distributions, I am confident the management team would keep its promise and maintain a low-leveraged balance sheet going forward.

Financial Valuation: Deeply Undervalued

{kind=link}

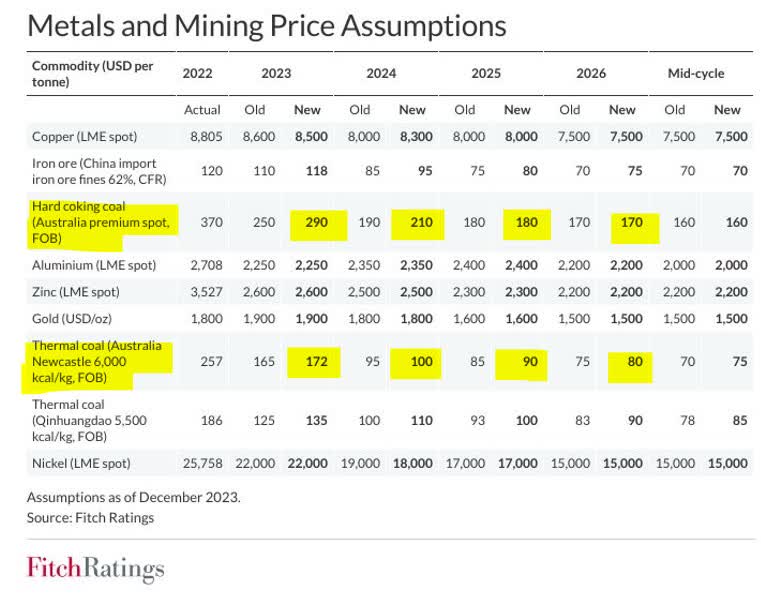

Coal Price Forecast (Fitch Ratings)

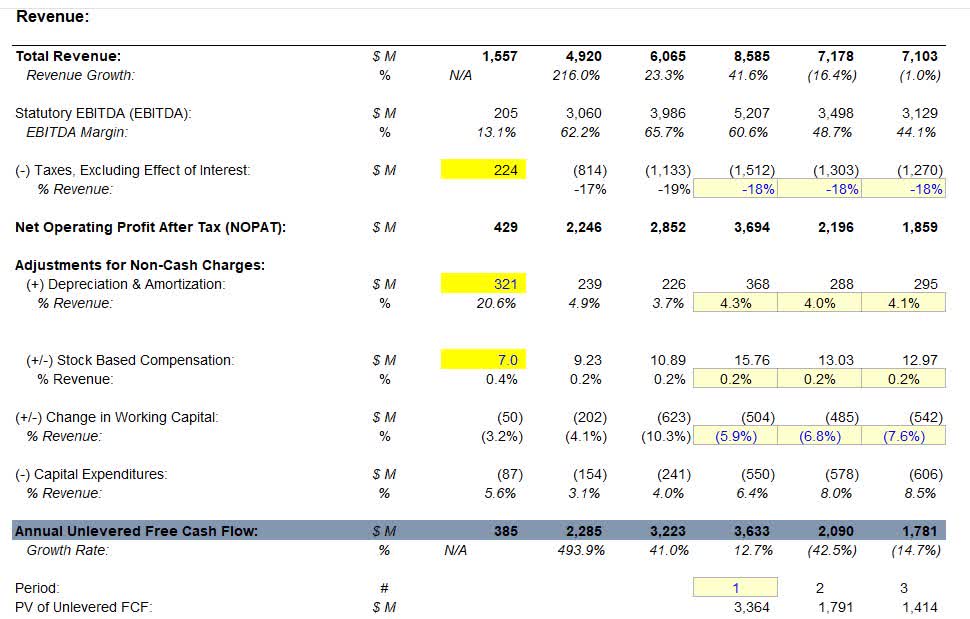

Let’s use a DCF to value Whitehaven Coal. So, I am trying to keep my assumptions conservative and in line with management's forward guidance.

{kind=link}

WHC Assumptions (KL Research)

The following are my assumptions:

First, thermal coal price will decline from $300/t in 1H 2023 to $90/t in 2026 based on estimates from Fitch Rating

Second, Met coal price will drop from $250/ton in 1H 2023 and stabilize at $170-180/ton in 2026 based on estimates from Fitch Rating .

Third, I assume that Whitehaven’s Run of Mine ((ROM)) coal production will double to around 40-44mt per annum in 2024-26 based on management’s guidance upon acquiring the Blackwater and Daunia Coal Mine from BHP.

Fourth, I anticipate that met coal (60%) will take up a more significant role in Whitehaven’s sales mix based on management guidance and will eventually go up to 70% due to increased demand for met coal in steelmaking for infrastructure and industrial development in Asia.

Fifth, I forecast the USD to weaken while the AUD will strengthen as the FED pivots to cut rates as early as Q2 2024.

{kind=link}

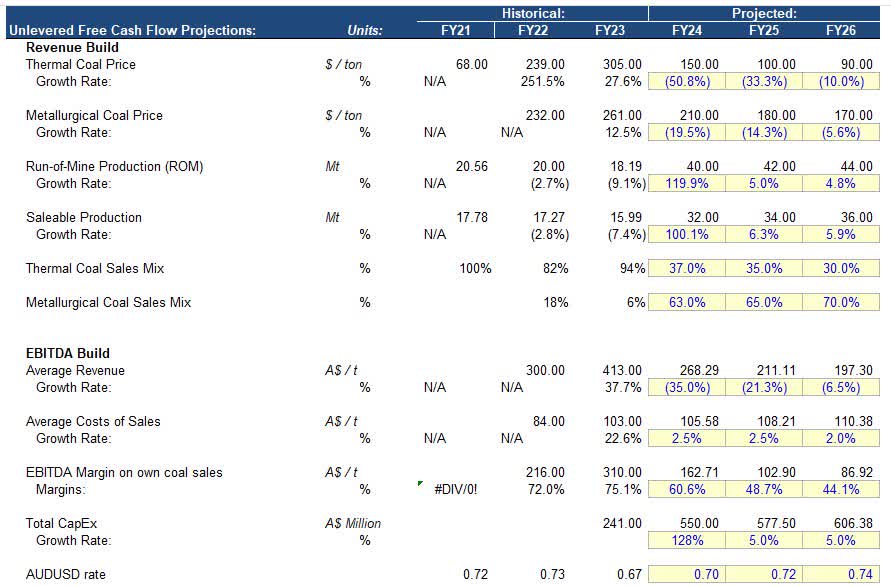

Financial Model (KL Research)

That being said, I expected Whitehaven’s revenue to peak at around A$8.59 billion in 2024 and gradually decline to A $7.1 billion in 2026, warranting the decline in thermal and met coal prices.

EBITDA is expected to reach A$5 billion next year and gradually decelerate to A$3 billion thanks to inflationary pressures and margin contractions.

By deducting taxes, stock-based compensation, changes in NWC, and Capex, which is expected to reach A $550 million based on management guidance. FCF for Whitehaven should be around A$ 3.6 billion, A$2 billion and A$1.8 billion for 2024-26, respectively.

WHC Intrinsic Value (KL Research)

I have applied an 8% discount rate and a 1.1x EV/EBIDTA multiple, which is super conservative in my opinion. This should give WHC an enterprise value ((EV)) of around A $8 billion. Adding back its A $2.45 billion of cash and A $1 billion of debt used to finance the purchase of 2 aforementioned mines.

I think that the intrinsic value of WHC should be around A $10.86, implying a potential 45% upside .

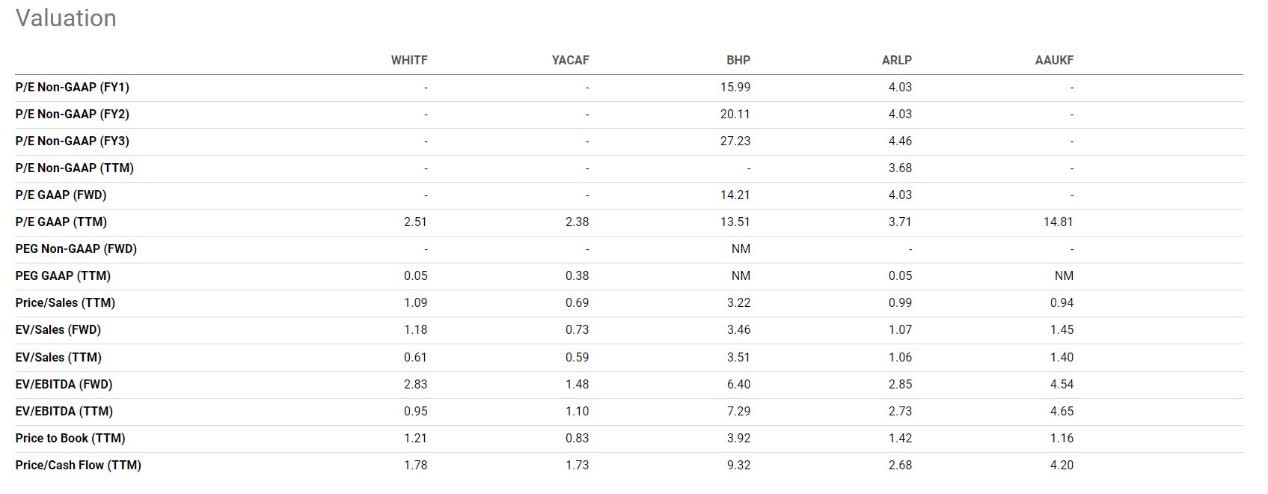

Multiples Valuation: Dirt Cheap

{kind=link}

Valuations Comparisons (Seeking Alpha)

To compare with its competitors like YanCoal and BNP, Whitehaven is now trading at a deep discount, with its P/E ratio now trading at nearly 2.5x earnings, which remains well below its competitors like BHP Group and Anglo American of around 13-14 x. Perhaps WHC is a typical Ben Graham-style cigar-butt-style Deep Value play.

In addition, its P/Cash Flow ratio sits at a whopping 1.78x, which doesn’t make much sense. This gives WHC an FCF yield of 53% and an earnings yield of 43%.

With a dividend yield ranging around 9-10%, investors and Mr Market are profoundly discounting the upside potential of this stock, and the stocks look extremely undervalued, which provides a golden buying opportunity for investors seeking to gain some exposure to deep value play.

Potential Risks

Despite its solid financials and underappreciated valuation, there are still some underlying risks behind the business that are worth considering before you invest.

1. Plummeting Coal Prices

Based on analysts' estimates, Thermal Coal and Met Coal prices are expected to decline. Against this backdrop, Whitehaven Coal’s revenue and margins would inevitably be hampered going forward.

While I acknowledge this poses a material risk to the firm, I think such pessimism has already been priced in at current price levels. My financial model has already factored in the worst possibilities for the business. The current price offers long-term value investors a decent margin of safety ((MOS)) .

Conclusion

Upon researching the company’s fundamentals, I think that Whitehaven Coal is a Deep Value play for long-term value investors that will benefit from the acquisition of 2 coal mines, which creates synergies and expands WHC’s footprint in the Met Coal Market to benefit from the growing manufacturing and infrastructure development in Asia.

I also love that the company's management has a long-term strategic vision with integrity and returns substantial capital back to shareholders.

At an FCF and earnings yield of 53% and 43% respectively, and a dividend yield of 10%. If WHC were to be listed in the US, its valuations and share price would have already skyrocketed. For value investors, time to broaden your horizons and search for value outside of the US!

For further details see:

Whitehaven Coal: Missed The Coal Rally? No Worries