CPRT - Who Is The King Of Junk? Copart Vs. IAA

Summary

- The totaled auto auction industry is a lucrative market with many tailwinds.

- 80% of the market is split between Copart and IAA, making it a Duopoly.

- The companies differentiate each other in their strategy and execution over the last years.

Investing in the right stocks can be a challenging task. One industry many people aren't familiar with is the totaled auto auction industry. Two prominent players in the market are Copart ( CPRT ) and IAA ( IAA ), who dominate the market. This article will compare these two companies' business models, financials, and market performance to help you decide which one might fit your investment portfolio. By the way, the title is a reference to the book 'From Junk to Gold' by Copart's Founder Willis Johnson.

A lucrative industry

The auto auction industry is a dirty industry that Peter Lynch would love. Every time a car gets into an accident and the insurance has to deal with it, they calculate: Is it more lucrative to repair the car or scrap it for parts? This is where Auction companies like Copart and IAA come into play. The damaged vehicles get transported to the Scrapyard of the Company and then auctioned off to the best bid. The market is expected to grow steadily as the US car fleet keeps expanding. I talked more intensively about the advantages of the industry in my recent article about Copart .

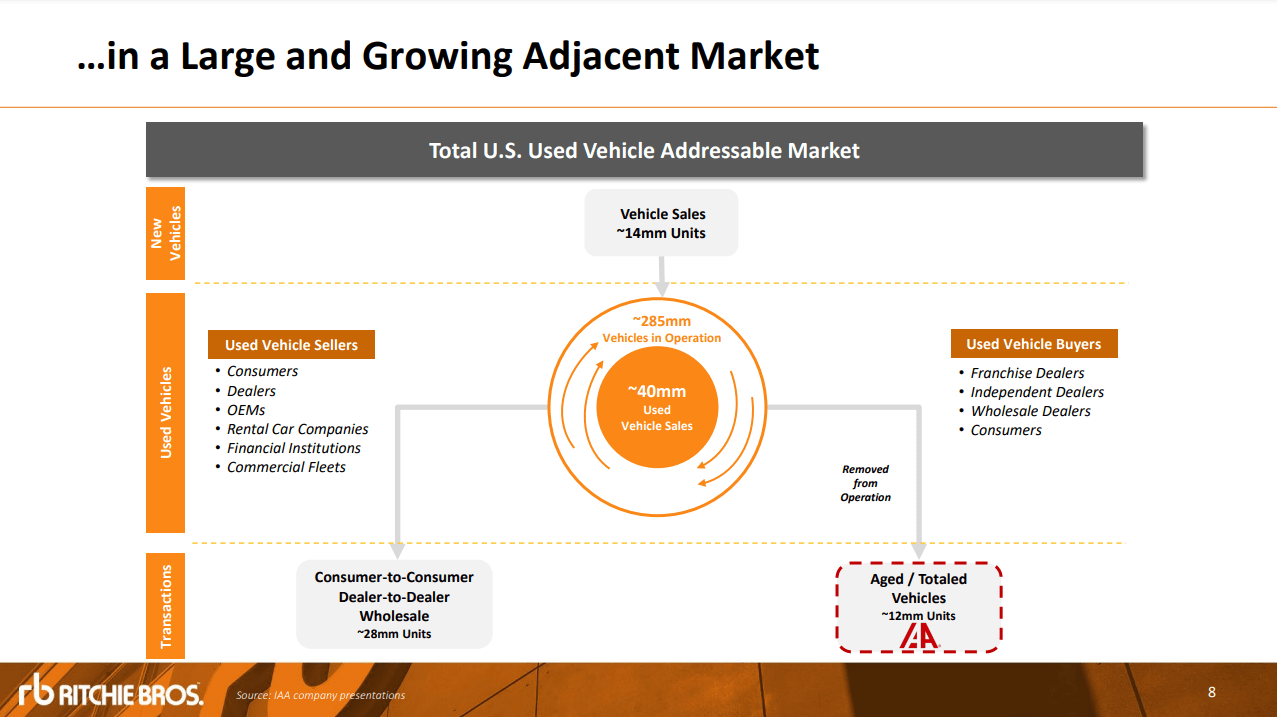

As we can see in this illustration from IAA and Ritchie Bros (RBA), we'll get to Richtie Bros later, the total vehicles in operation in the US is estimated at around 285 million vehicles with 14 million new sales a year and 12 million vehicles at the end of their lifecycle. This means the market should grow by 2 million cars a year. That being said, the total loss ratio (percentage of damaged vehicles that are totaled versus repaired) keeps increasing and the fleet is aging, providing additional headwinds.

US Used Vehicle Addressable market (RBA IAA Merger Presentation)

{kind=link}

A duopoly

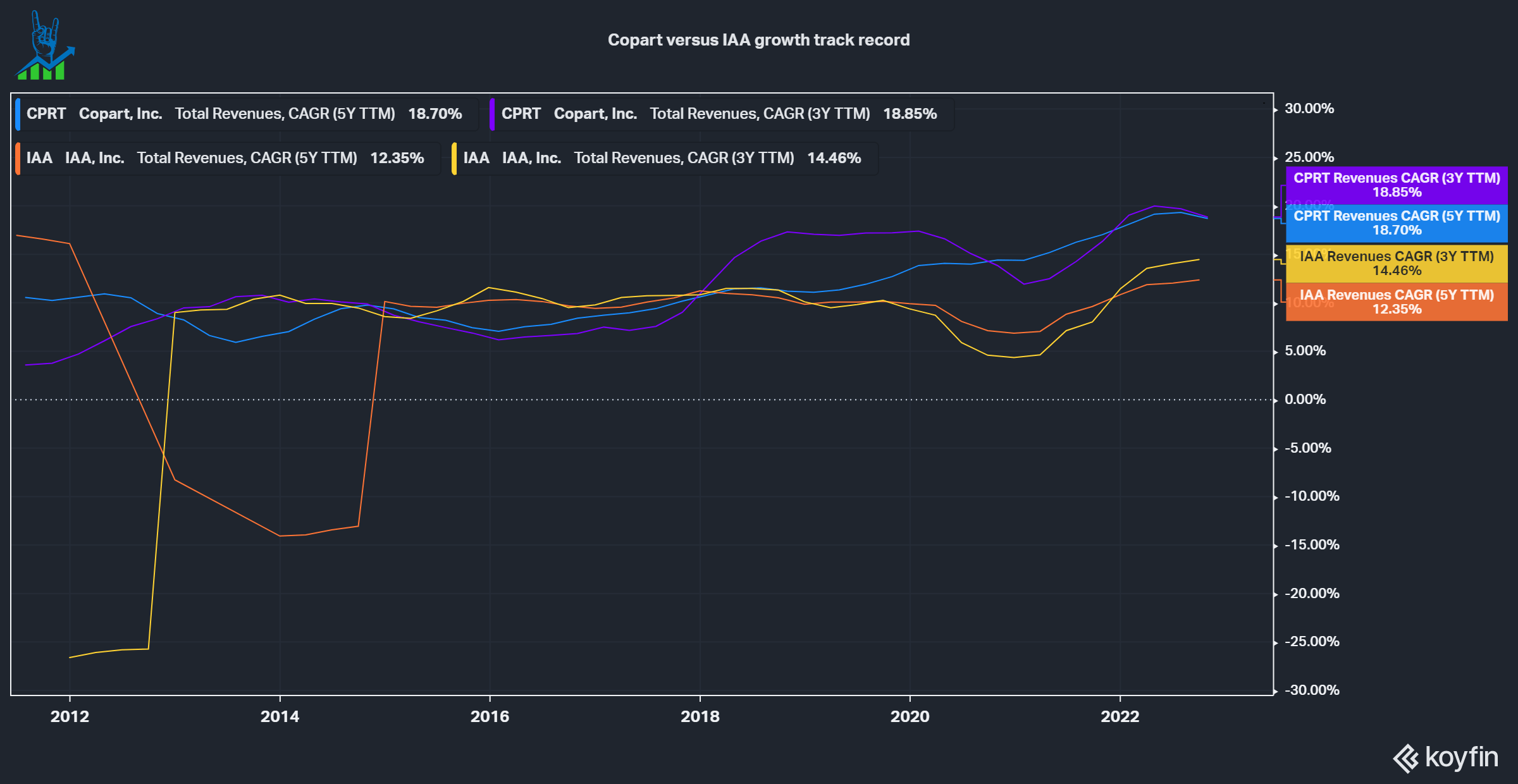

Copart has been operating for 40 years in the industry and IAA was spun off from KAR Auction Services (KAR) in 2018. In the spin-off filing, KAR stated that IAA and Copart represent around 80% of the NA market ( page 9 ). This makes the market a duopoly with two dominant players and many smaller players without significant market share. The revenue trends over the last years indicate that Copart is taking market share. Over the last decade, we see that Copart's growth was much more stable and generally higher. This is further supported by a claim from Ancora Holdings, a wealth management firm with a 2% stake in IAA, that wrote an open letter to the IAA board in March 2022. The firm points out that IAA keeps losing market share because:

One of IAA’s largest insurance customers has been shifting vehicle supply to Copart since the third quarter of 2019. We have heard this issue was due to the service levels IAA provided during Hurricane Harvey, during which the Company was not able to meet the supply needs of this particular customer.

This brings us to a significant differentiation, the balance sheet of both companies.

CPRT vs IAA growth history (Koyfin)

{kind=link}

Two very different balance sheets

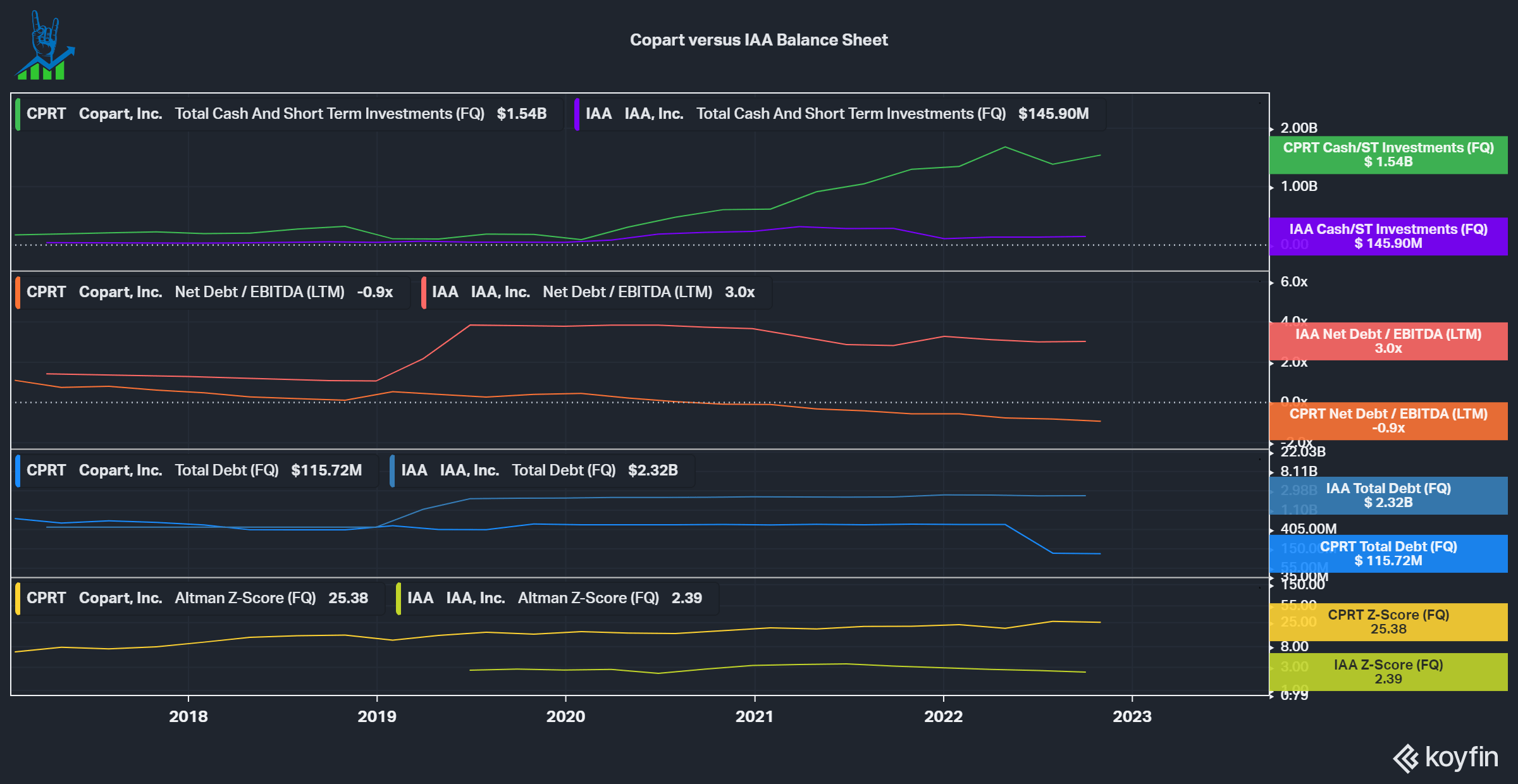

Below you can see a comparison of the balance sheets for both companies. We can see a very different approach here. Copart has a fortress balance sheet with $1.54 billion in cash versus just $115 million. A few quarters ago, the Company decided to pay down around $400 million of its debt due to the interest rate environment. IAA is the polar opposite, with a leverage of 3 times EBITDA. This is also represented in the Altman Z-Score (the higher the score, the better), a metric showing the financial health of a company and the risk of bankruptcy.

Copart justifies this amount of net cash because it says that they want to be in a position where it can always promise its customers to be able to serve them, especially in difficult situations like natural disasters. In the last segment, we heard that Ancora Holdings pinpoints IAA's loss of market share to the service levels IAA provided during Hurricane Harvey, during which the Company was not able to meet the supply needs of this particular customer . Trust is one of the essential things in most industries, but especially in this industry. Insurance companies want to know that they can trust their partner and Copart is taking all steps to ensure this. In Q4 earnings, Copart noted that they keep on doing more services for the insurance companies, increasing their relationships and with that moat:

In some -- to give you specific examples, we have many fewer insurance company employees who are day-to-day visiting our yards to do their work and we've instead virtualized much of that workflow for them, doing it on their behalf and conveying that information digitally so that they can process those vehicles without coming to [ see us ] first hand.

Jeffrey Liaw, Copart Q4 22 earnings call

CPRT vs IAA Balance Sheet (Koyfin)

{kind=link}

A high-margin business, at least for Copart

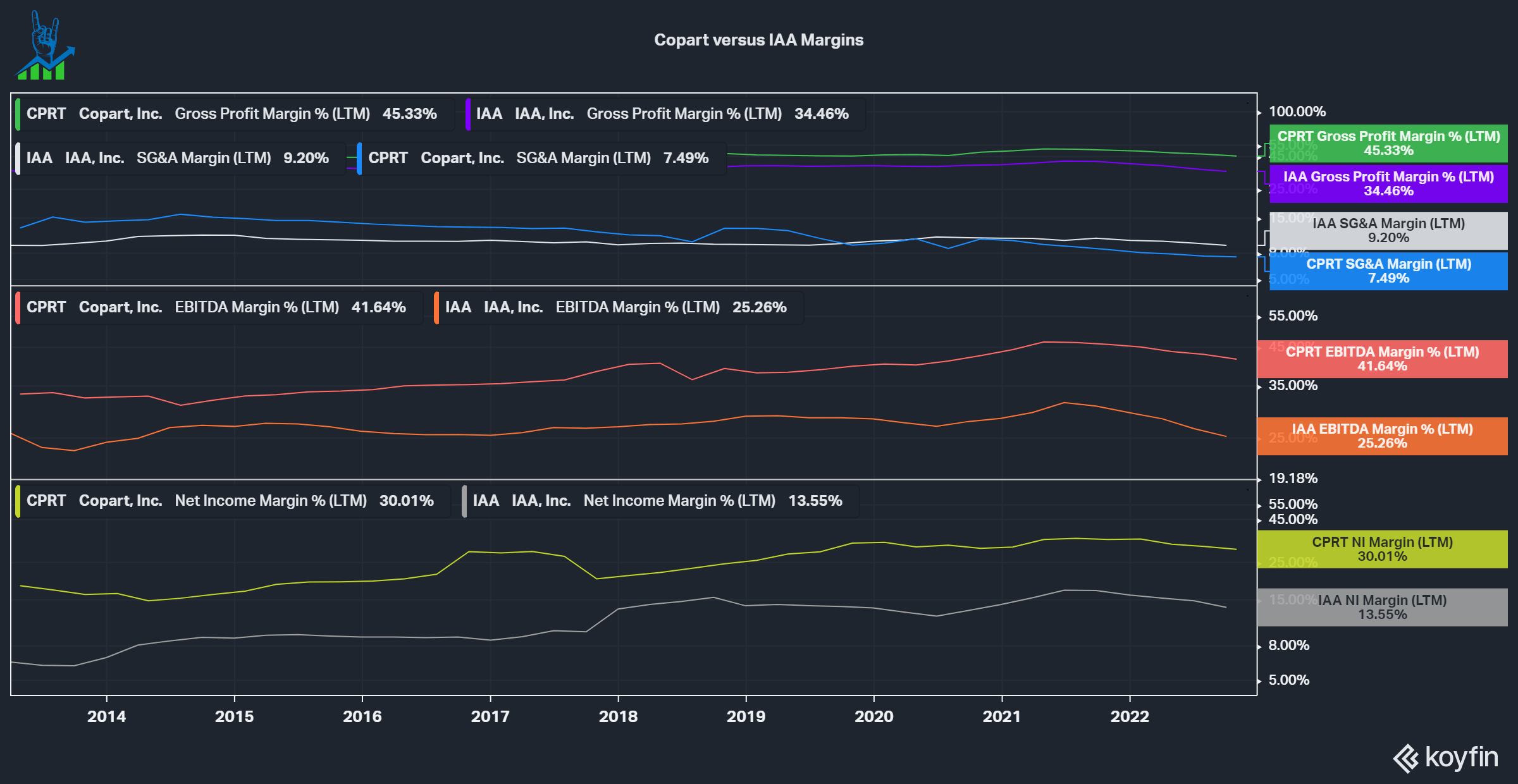

Below you can see a comparison of the margins both companies have. We can see that Copart has higher margins across the board and can keep increasing the bottom line, while IAA is stagnating. This is in part due to Copart' focus on the long term. While IAA leases many of its yards, Copart owns most of its scrapyards and has done so in many cases for decades. Scrapyards often are local monopolies because municipalities don't allow new yards to be built. After all, they are dirty and not what you want in your city. This gives these yards a large moat and owning them increases Copart's moat significantly. Over the last five years since IAA was spun off, Copart spent $2.17 billion on CapEx, while IAA just spent $476 million.

{kind=link}

IAA's merger with Ritchie Bros

Last year, Ritchie Bros proposed a merger with IAA. Since then, the deal has had a lot of drama around it, with several large holders of both companies publicly announcing to vote against the deal. Since then, the deal has been revised and could now go through. A large part of the discussion about the deal is the lack of clear synergies. Ritchie Bros want to diversify their business model, which is split between Construction, Commercial Transportation and Other auctions, while IAA has 100% Vehicle end markets. The more significant issue I see is that Ritchie has very little business with insurance companies, while most of IAA's business is with insurance companies. I believe this deal will benefit Copart the most because I could imagine it distracts IAA, who are already losing market share.

Pro Forma business (IAA RBA merger presentation)

{kind=link}

And the winner is...

Let's take a look at valuations. We can see that Copart trades at a significant premium to IAA in PE and EBITDA multiples but is actually cheaper on an FCF yield (although Copart still is expensive at a 2.4% FCF yield). I believe the premium is justified due to Copart's superior business, management and market share gains. Copart has teens growth rates priced into it, but I think that Copart will be able to achieve this by continued strong execution with a long-term focus. I recently started a position in Copart at $60 and am looking to increase my position if we see some weakness in the stock.

CPRT vs IAA Valuation (Koyfin)

{kind=link}

For further details see:

Who Is The King Of Junk? Copart Vs. IAA