WSR - Who Likes Monthly REIT Money?

2023-07-07 07:00:00 ET

Summary

- Whenever I get a dividend check, it’s like getting a paycheck – but without having to work for it.

- Monthly reinvestments minimize market risk, specifically, the risk of reinvesting at peak prices – and opportunities for second-guessing.

- Importantly, some investors are counting on the income to pay bills or cover regular expenses.

This article was published at iREIT® on Alpha on Thursday, July 6, 2023.

I recently wrote articles on SoFi Weekly Income ETF ( TGIF ) and SoFi Weekly Dividend ETF ( WKLY ) – two weekly paying exchange-traded funds, or ETFs, that are yielding in the 3% range.

It was terrific to get feedback from readers regarding the weekly pay model. After reading most of the comments, the consensus is that weekly dividends are not as appealing as monthly dividends.

Another pushback from readers is, of course, the low dividend yield.

I suppose it really comes down to your definition of instant gratification.

Some people like to get paid weekly, some like getting paid monthly, and others are content getting paid quarterly.

Well, as you know, you're reading this article because you clicked the title:

Who Likes Monthly REIT Dividends?

We selected a few of our favorites below...

Realty Income: 5.1% Dividend Yield

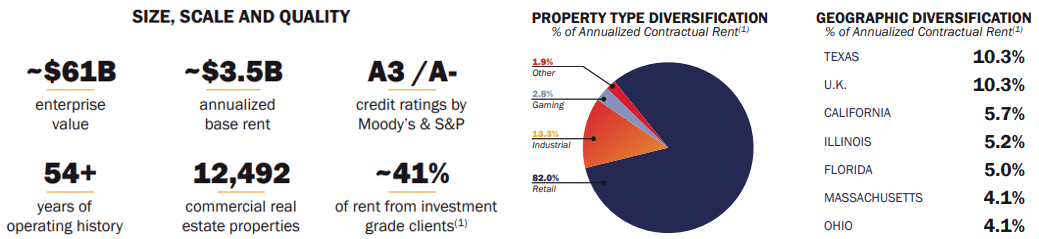

Realty Income Corporation ( O ) is a triple-net real estate investment trust (“REIT”) that specializes in free-standing, net-lease retail properties but also invests in industrial and gaming properties. As a percentage of their annualized rent, retail properties make up 82.0%, industrial makes up 13.3%, while gaming properties make up 2.8%.

In total, Realty Income’s portfolio consists of 12,492 properties located in all 50 U.S. states, the United Kingdom, Spain, and Italy. Their properties cover approximately 246.7 million square feet, serve 1,259 tenants that operate across 84 separate industries, have an occupancy rate of 99.0%, and a weighted average remaining lease term of approximately 9.4 years.

{kind=link}

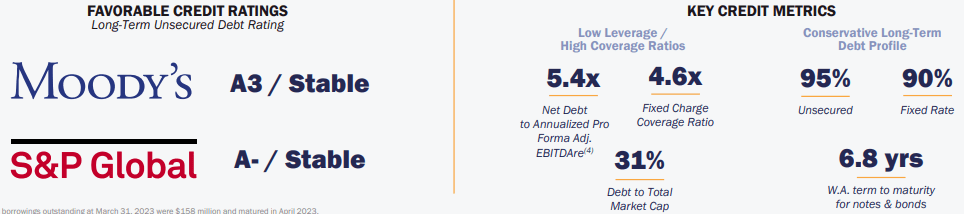

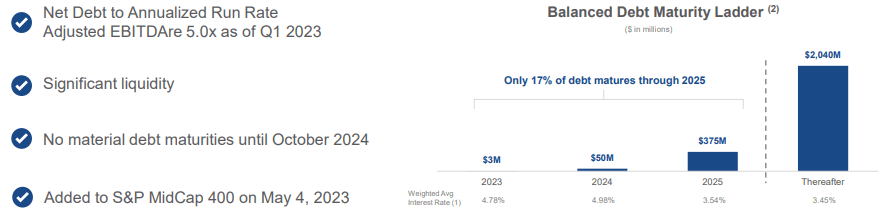

Realty Income is investment-grade with an A- credit rating and has strong debt metrics. They have a net debt to annualized pro forma adjusted EBITDAre of 5.4x, a fixed charge coverage ratio of 4.6x, and a long-term debt to capital ratio of 41.21%.

Their debt is 90% fixed rate, 95% unsecured, and has a weighted average term to maturity of 6.8 years. Additionally, as of the end of the first quarter, Realty Income had $3.1 billion of liquidity.

{kind=link}

Realty Income is probably best known for their monthly dividend, which has been paid and increased for 29 consecutive years. They have declared 634 monthly dividends and raised the dividend for 102 consecutive quarters and have a compound annual dividend growth rate of 4.4% since 1994. Their dividend track record has put them in an elite class as one of the few Dividend Aristocrats within the REIT space.

O - IR

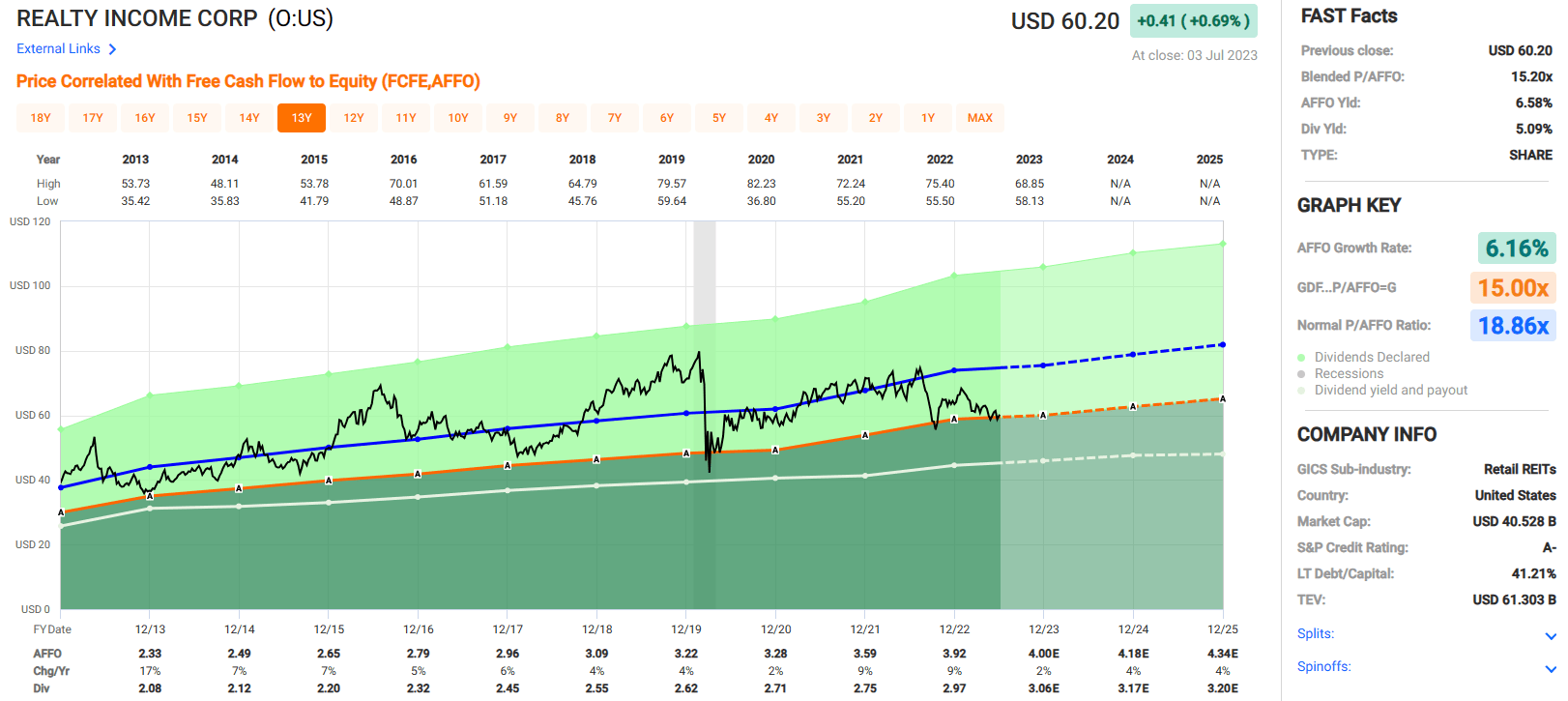

In addition to the excellent dividend track record, Realty Income has delivered positive adjusted funds from operations (“AFFO”) growth in 26 out of the last 27 years and has delivered an average annual AFFO growth rate of 6.16% since 2013.

Currently they pay a 5.09% dividend yield that is well covered with an AFFO payout ratio of 75.69%. The stock trades at a P/AFFO of 15.20x, which compares favorably to their normal AFFO multiple of 18.86x.

At iREIT®, we rate Realty Income stock a BUY.

{kind=link}

STAG Industrial : 4.0% Dividend Yield

STAG Industrial, Inc. (STAG) is an industrial REIT that owns distribution and light manufacturing buildings that are primarily single-tenant properties. Their portfolio consists of 561 properties located in 41 states that cover approximately 111.6 million square feet.

As of the end of 2022, STAGs properties were approximately 98.5% leased and had a weighted average lease term of 4.7 years. They have a diverse mix of tenants with no single tenant making up more than approximately 3.0% of their annualized base rent (“ABR”) and no singe industry making up more than 10.9% of their ABR.

STAG differentiates its investment strategy by focusing on middle market industrial properties that don’t garner the same attention from institutional investors or larger REITs. With this approach they are able to compete with local investors in fragmented markets where they have a competitive advantage due to their size, scale, and access to capital markets.

{kind=link}

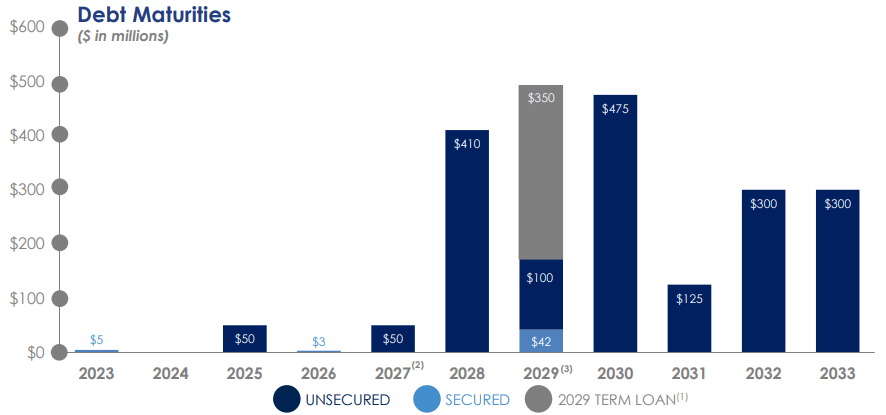

STAG has a Baa3 credit rating from Moody’s and solid debt metrics with a net debt to adjusted EBITDAre of 5.0x, a long-term debt to capital of 39.49%, and a fixed charge coverage ratio of 4.7x. Their debt has a weighted average interest rate of 3.39%, and 99.7% of it is unsecured. STAG has no significant debt maturities until October 2024 and has $783.9 million in total liquidity.

{kind=link}

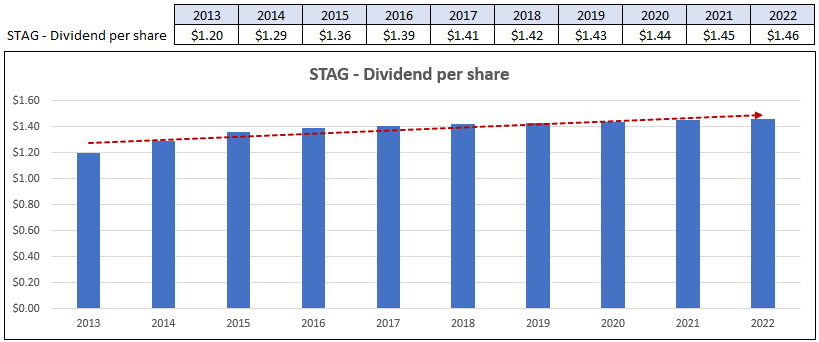

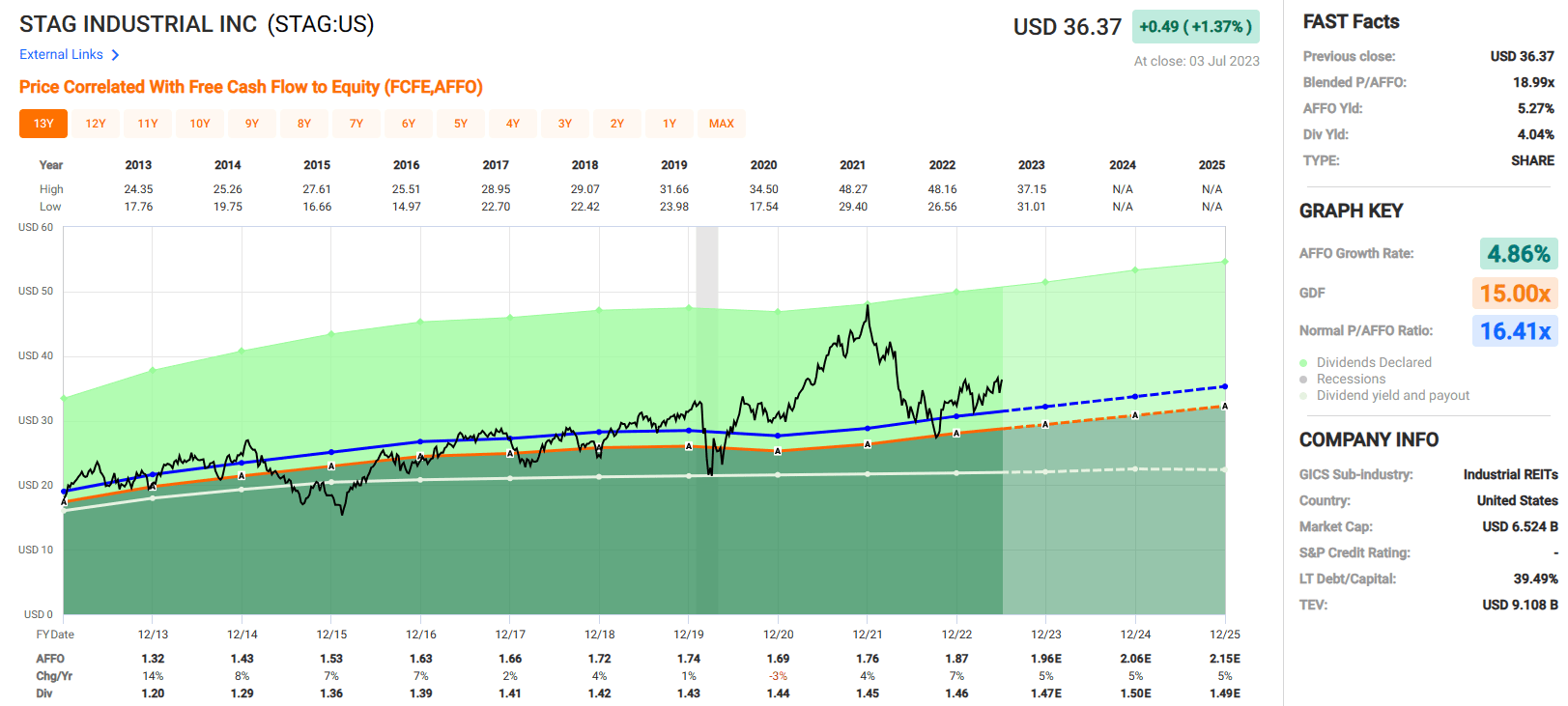

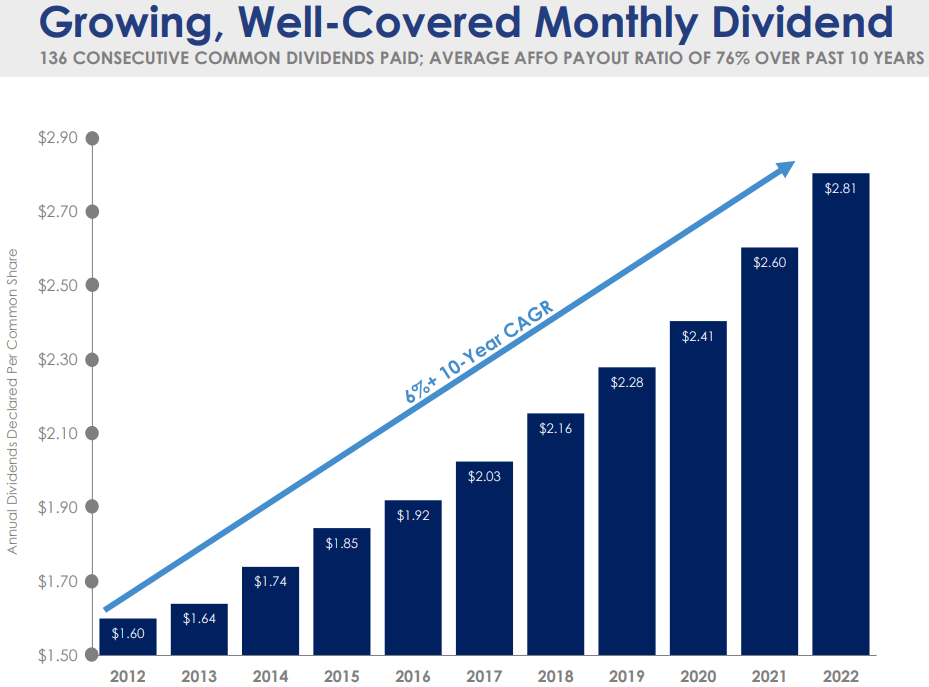

STAG has raised its dividend each year since 2013 and has an average dividend growth rate of 3.22% over the last 10 years. In recent years, the dividend growth rate has slowed with an increase of under 1.00% since 2019, but they currently pay a higher yield than most other REITs in the industrial sector, which as a group averages a dividend yield of approximately 3.0%.

{kind=link}

STAG pays monthly dividends and currently offers a 4.04% dividend yield that is well covered with an AFFO payout ratio of 78.08%.

Since 2013 STAG has delivered an average AFFO growth rate of 4.86%, and analysts expect AFFO growth of 5% in 2023, 2024, and 2025.

Currently, STAG stock is trading at a P/AFFO of 18.99x, which is a premium compared to their normal AFFO multiple of 16.41x. At iREIT®, we rate STAG a HOLD.

{kind=link}

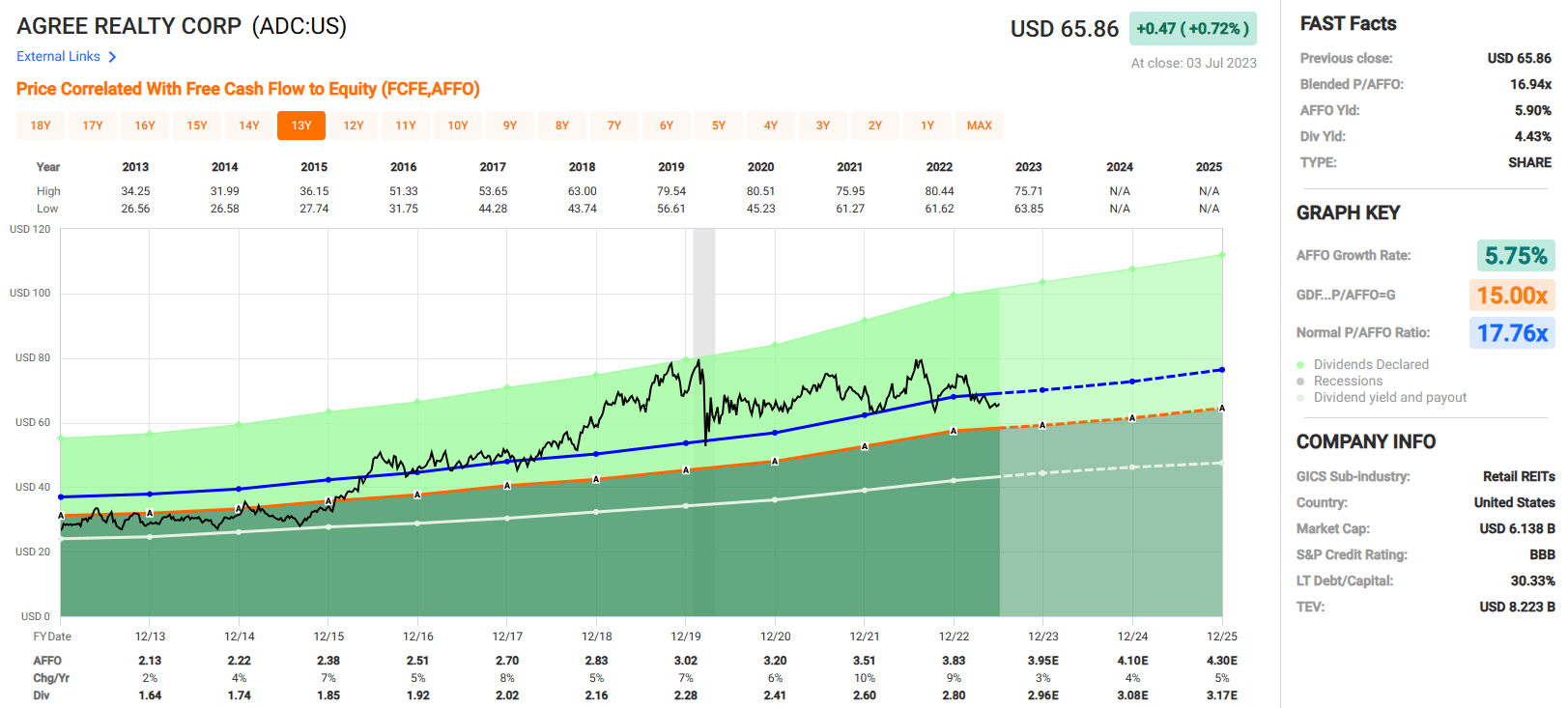

Agree Realty: 4.4% Dividend Yield

Agree Realty Corporation ( ADC ) is a net-lease REIT that specializes in free-standing retail properties that are resistant to e-commerce. Their portfolio consists of 1,908 properties that are located in 48 states and cover roughly 40.0 million square feet. Their properties are approximately 99.7% leased and have a weighted average lease term of around 8.8 years.

The majority of their properties are leased to national tenants and 68.0% of their ABR is generated from tenants, or their parent company, with an investment grade credit rating. ADC has a strong tenant roster with well-established names that make up their top tenants.

As a percentage of their ABR, their top 5 tenants are Walmart, Dollar General, Tractor Supply, Best Buy, and Kroger. By retail sector, their top 5 categories include grocery stores, home improvement, Tire & Auto service, dollar stores, and convenience stores.

{kind=link}

ADC is investment grade with a BBB credit rating from S&P and has strong debt metrics including a net debt to EBITDA of 4.5x, a fixed charge coverage ratio of 5.1x, and a long-term debt to capital ratio of 30.33%. Additionally, ADC has $1.2 billion of total liquidity and no significant debt maturities until 2028.

{kind=link}

Agree Realty started paying monthly dividend in 2021. Prior to the change, ADC paid 107 consecutive quarterly dividends between 1994 and 2020 and has paid 29 consecutive monthly dividends since that time. Over the last 10 years ADC has had a compound annual dividend growth rate of 6% and just recently increased the dividend by 7.2% in 2022.

{kind=link}

Agree Realty pays a 4.43% dividend yield that is well covered with an AFFO payout ratio of 73.24% and is currently trading at a P/AFFO of 16.94x, which is a discount compared to their normal AFFO multiple of 17.76x.

ADC has been very consistent in its earnings with positive AFFO growth in each year since 2013. Over that time period they have had an average AFFO growth rate of 5.75% and analysts expect AFFO growth of 3% in 2023 and 4% in 2024.

At iREIT®, we rate Agree Realty a BUY.

{kind=link}

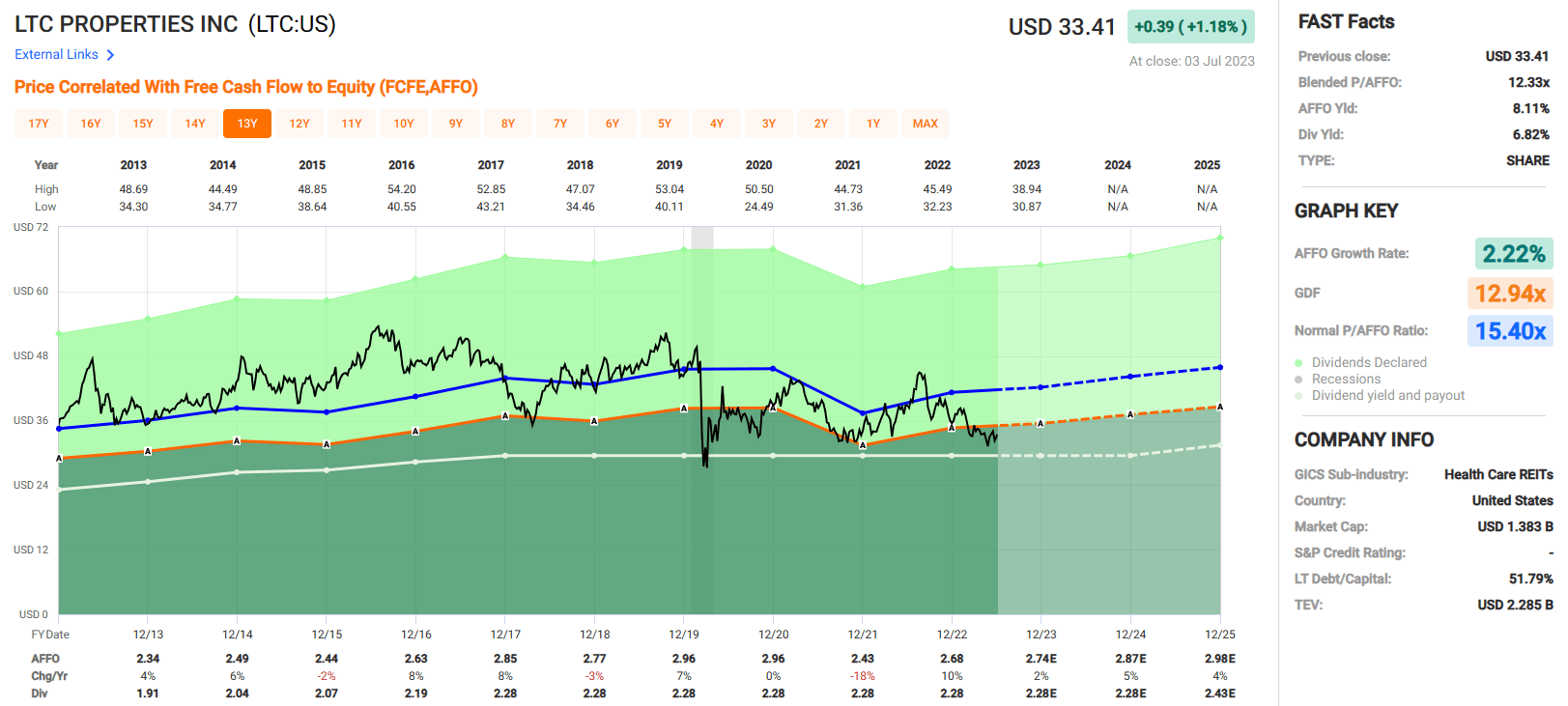

LTC Properties: 6.8% Dividend Yield

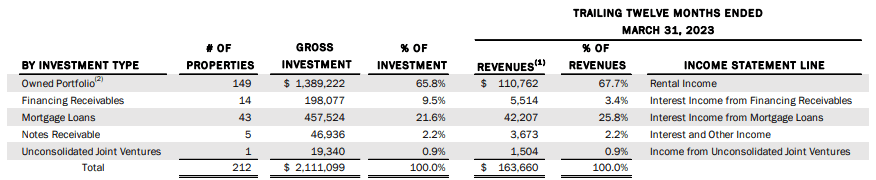

LTC Properties, Inc. ( LTC ) is a REIT in the healthcare sector that invests in senior housing and skilled nursing facilities through triple net sale-leasebacks, mortgage loans, construction financing and structured financing including bridge and mezzanine loans and preferred equity.

LTC's properties consist of 98 assisted living facilities, 50 skilled nursing homes and 1 behavioral health care hospital which together contribute 67.7% of LTC’s annual revenues.

In addition to the rental income they receive from their owned properties, LTC also generates revenues through interest income from the financing they provide. 25.8% of their annual revenues is derived from interest income from mortgage loans, while financing receivables and notes receivables contribute 3.4% and 2.2% respectively.

{kind=link}

LTC has solid debt metrics with a debt to adjusted EBITDAre of 5.8x, a long-term debt to capital ratio of 51.79%, a fixed charge coverage ratio of 3.6x, and a debt to enterprise value ratio of 40.6% as of the end of the first quarter.

They have plenty of liquidity with $5.5 million in cash and cash equivalents, $135.9 million available to them under their revolving credit facility, and $128.8 million available under their at-the-market ((ATM)) offerings.

LTC - IR

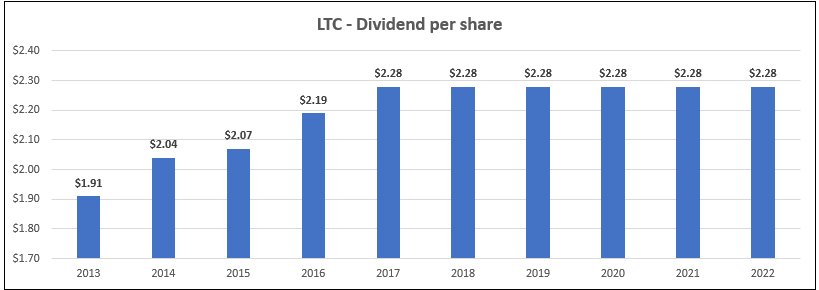

LTC pays monthly dividends and have raised or maintained their dividend since 2008. Over the past 15 years, they have generated an average dividend growth rate of 2.87%, but that has slowed in recent years, with the last dividend increase in 2017. It is worth noting, however, that they did not cut their dividend during the great recession or during the covid pandemic.

{kind=link}

LTC has had modest earnings growth rates, with an average AFFO growth rate of 2.22% since 2013. Analysts expect AFFO growth of 2% in 2023 and then 5% and 4% in the years 2024 and 2025, respectively. LTC pays a 6.82% dividend yield that is covered with an AFFO payout ratio of 85.10% and currently trades at a P/AFFO of 12.33x, which is well below their normal AFFO multiple of 15.4x.

At iREIT®, we rate LTC a BUY.

{kind=link}

Gladstone Land: 3.4% Dividend Yield

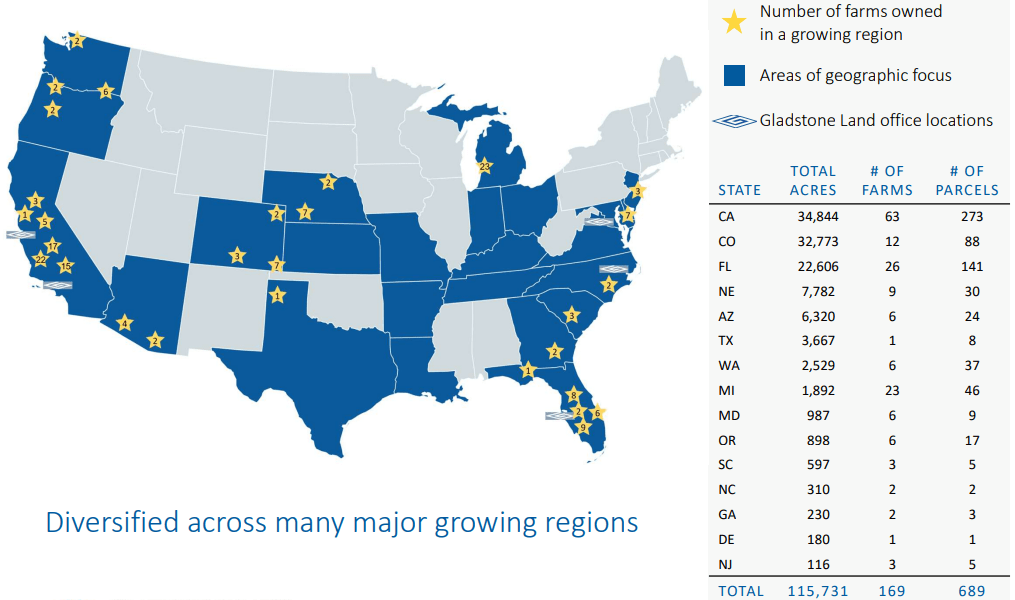

Gladstone Land Corporation ( LAND ) is an externally managed agricultural REIT that owns a portfolio of farms that are primarily leased on a triple-net basis. Their portfolio is made up of 169 farms that are located in 15 states and encompass 115,731 acres of land.

LAND’s farms are leased to 88 different tenants and produce over 60 different types of crops including lettuce, beans, raspberries, sweet corn, tomatoes, almonds, avocados, and strawberries. Their properties have a weighted average remaining lease term of 6.5 years and have a 100% occupancy rate.

LAND targets properties that have an adequate water supply, are in regions with long growing seasons, and markets with a strong farming presence and that have an abundance of strong operators.

{kind=link}

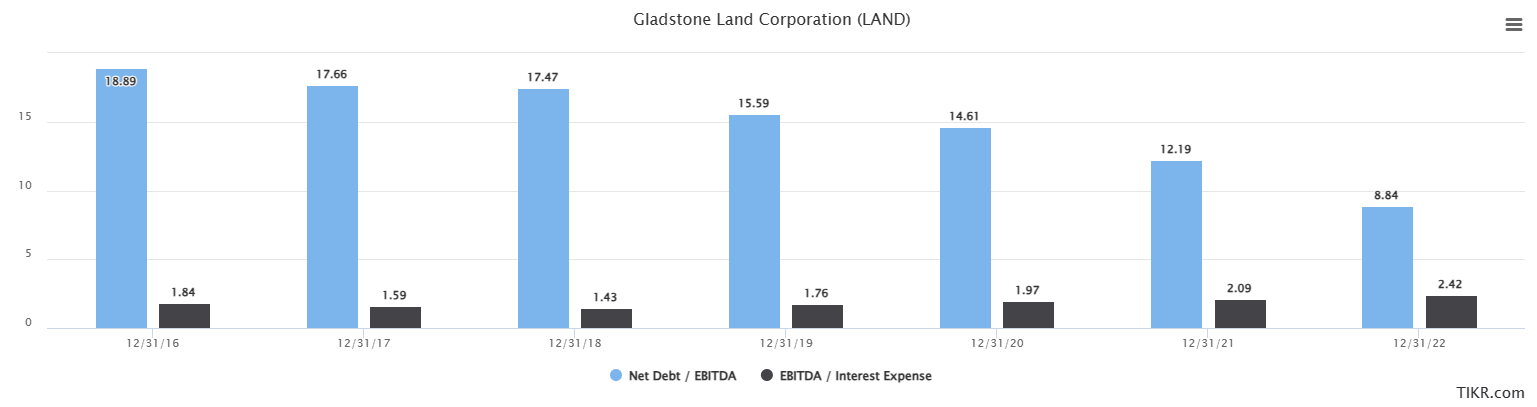

LAND has a net debt to EBITDA of 8.84x and an interest coverage ratio of 2.42x. While these metrics show a higher level of debt than many of the REITs in our coverage, LAND has been improving both metrics over the last several years and has operated with much higher debt levels in the past, so I’m not overly concerned.

{kind=link}

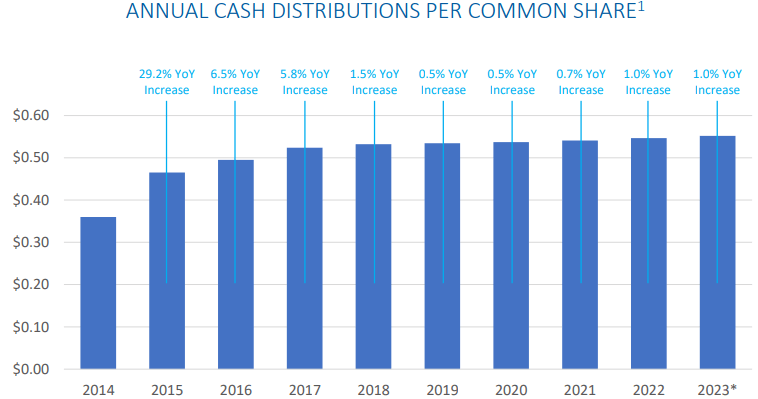

LAND pays monthly dividends and has made 123 consecutive monthly distributions since their public listing in 2013. Additionally, they have increased the dividend 30 times over the past 33 quarters and have delivered a compound annual dividend growth rate of 5.35% over the last 8 years.

While they have a solid dividend growth rate, much of that occurred in 2015, when the dividend was increased by 29.2%. Since 2019, they have raised their dividend by 1% or less.

{kind=link}

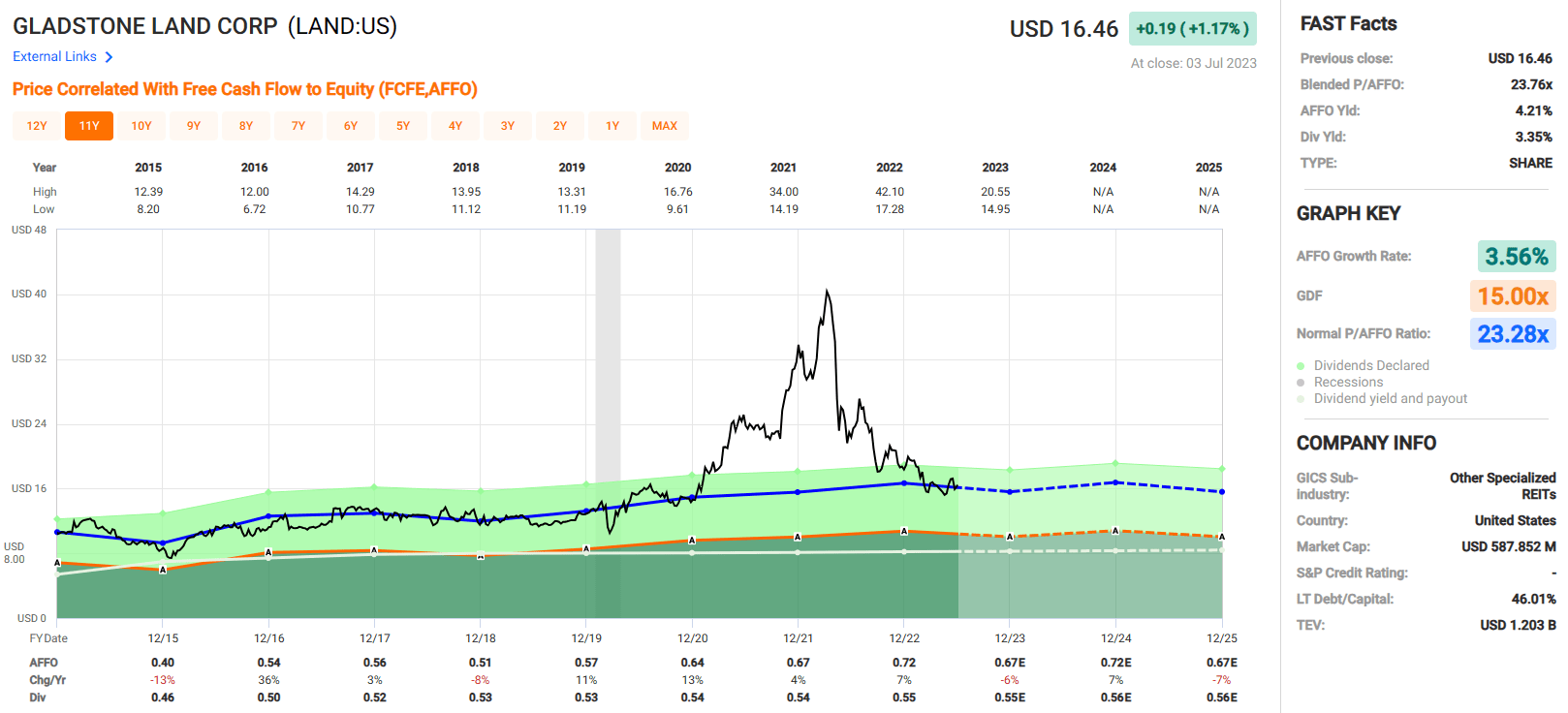

LAND has delivered an average AFFO growth rate of 3.56% since 2015. Analysts expect AFFO to fall by 6% in 2023, increase by 7% in 2024, and then fall by 7% in 2025. They currently pay a 3.35% dividend yield that is well covered with an AFFO payout ratio of 76.30% and are trading at a P/AFFO of 23.76x, which is in line with their normal AFFO multiple of 23.28x.

At iREIT®, we rate LAND a Spec BUY.

{kind=link}

Whitestone REIT: 4.9% Dividend Yield

Whitestone REIT ( WSR ) is an internally managed REIT that acquires, develops, and operates open-air shopping centers. Their properties contain a mix of retail and service-oriented stores that include grocery, specialty retail, restaurants, financial services, and health & fitness centers.

Their wholly owned real estate portfolio consists of 57 properties located in 3 states that cover approximately 5.1 million leasable square feet. WSR targets properties in high growth and densely populated markets.

Their primary markets are in Austin, Dallas-Fort Worth, Houston, San Antonio, Phoenix, and Chicago. Their properties are largely concentrated in Houston and Phoenix with 14 properties in Houston and 25 properties in the Scottsdale and Phoenix metropolitan areas.

{kind=link}

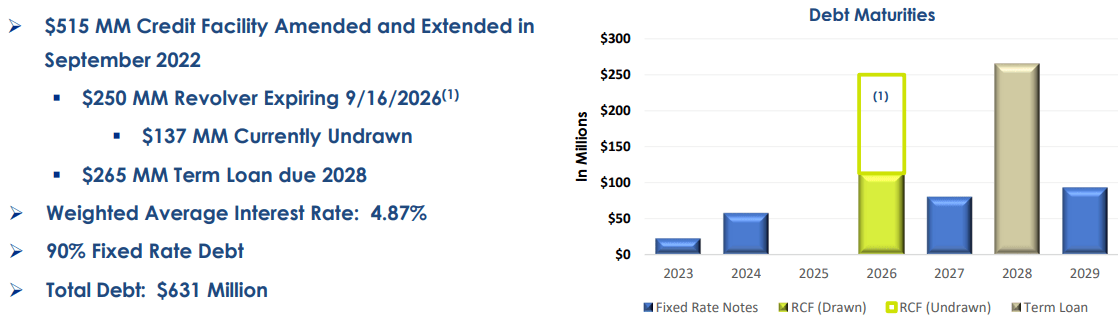

Whitestone REIT has a debt to pro forma EBITDAre of 7.8x, an interest coverage ratio of 2.91x, and a long-term debt to capital ratio of 58.21%. They have $631 million in total debt that carries a weighted average interest rate of 4.87% and is 90% fixed rate. Additionally, they have a well-staggered debt maturity schedule with minimal debt maturities in 2023.

{kind=link}

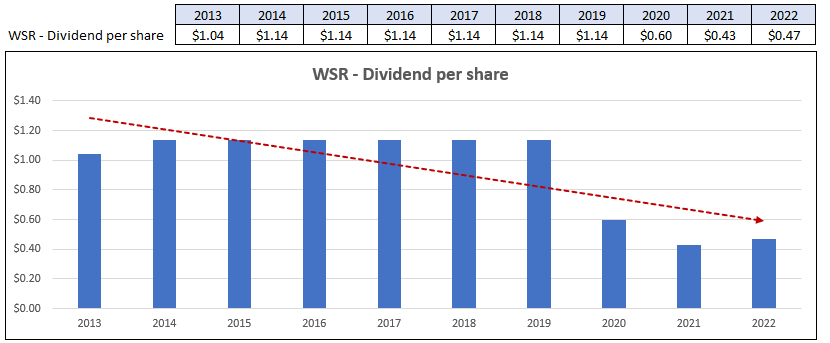

WSR pays a monthly dividend with an annual yield of 4.91%. They maintained their dividend at $1.14 per share from 2014 through 2019, but then cut the dividend by -47.37% in 2020 and then cut the dividend again in 2021 by -28.75%. On a positive note, they increased their dividend by 9.36% in 2022 to $0.47 per share and currently have an AFFO payout ratio of just 55.99%.

{kind=link}

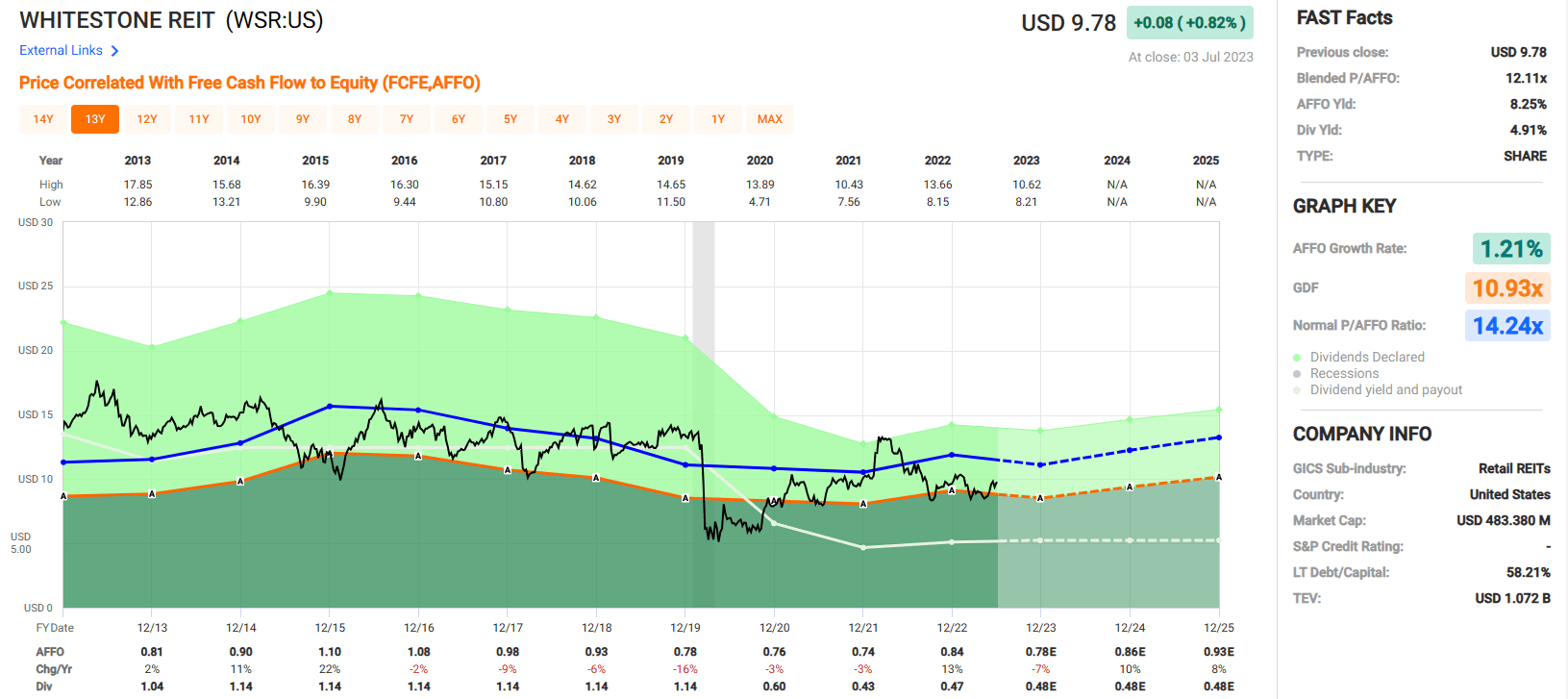

WSR has had an average AFFO growth rate of 1.21% since 2013. Their AFFO per share fell each year from 2016 to 2021 but they delivered positive AFFO growth of 13% in 2022. Analysts expect AFFO to fall by 7% in 2023 but then to increase by 10% in 2024 and 8% in 2025. Currently WSR is trading at a P/AFFO of 12.11x, which compares favorably to their normal AFFO multiple of 14.24x.

At iREIT®, we rate Whitestone REIT a Spec BUY.

{kind=link}

Insist on a Steady Paycheck

Whenever I get a dividend check, it’s like getting a paycheck – but without having to work for it.

There are a few advantages too:

Convenience: one dividend per quarter vs. one every 30 days

Minimizes Market Risk : monthly reinvestments minimize market risk, specifically, the risk of reinvesting at peak prices – and opportunities for second-guessing.

Dollar Cost Averaging : reinvesting dividends monthly enhances the opportunity.

Easy for Selling : You don’t need to wonder if you should wait months for the next dividend to be paid.

Fixed Income : some investors are counting on the income to pay bills or cover regular expenses.

As always, I look forward to your feedback and I look forward to your comments and/or feedback.

Happy SWAN Investing!

PS: Here are a few REITs we would like to see paying monthly :

- Arbor Realty ( ABR )

- Armada Hoffler ( AHH )

- Blackstone Mortgage ( BXMT )

- Highwoods Properties ( HIW )

- Ladder Capital ( LADR )

- NNN REIT ( NNN )

- Alpine Net Lease ( PINE )

- Sachem Capital ( SACH )

- UMH Properties ( UMH )

- VICI Properties ( VICI )

- W.P. Carey ( WPC ).

For further details see:

Who Likes Monthly REIT Money?