SRC - Who's Ready For A Santa Claus REIT Rally?

2023-12-12 07:00:00 ET

Summary

- REIT stock prices have been struggling, but I believe a REIT rally is on the horizon.

- Some experts speculate that the Santa Claus rally has already happened.

- In this article, I will reveal three of my largest positions and why I own them.

Who’s ready for the REIT rally?

I know I am – so much so that I don’t care who rolls their eyes at me. “There he goes again,” I can practically hear some groan.

Admittedly, it’s been a rough ride with real estate investment trust, or REIT, stock prices for a while. As I noted in last year’s exclusive Investing Group piece “REIT Roadmap 2023”:

“Real estate – including… REITs – has had a dreadful year in 2022…”

U.S. Sector 1-Year Performance - 14th December 2022 - Simply Wall St

“For starters, you can see that real estate declined 22.11% between January 1 and December 14. That’s the first strike against it.

“Admittedly, some categories did worse than real estate:

- Tech, down 25.23%

- Consumer discretionary, down 34.13%

- Telecom, down 38.67%.

“… But seven out of the 11 categories did better, making for a very poor ranking. So that’s strike No. 2.

“And as for strike No. 3? Well, the larger U.S. market was down “just” 18.14%, making it nearly 4% better than real estate’s showing.

“As for REITs specifically, here’s a chart of the Vanguard Real Estate Fund ( VNQ ), which can serve as a basic REIT index.”

Yahoo Finance

“As of December 21, it was down 26.73% year-to-date. Which makes it an even worse performer than the larger real estate category. And I doubt the last few days of 2022 can change that.”

Nor did the first 11 months of 2023. But I think that’s officially changing.

Some Don’t Expect a Lot for Christmas

Everyone’s been wondering about the Santa Claus rally, and understandably so. ‘Tis the season, after all.

Traditionally speaking, the markets tend to rise 1%-2% over the last five trading days of the old year and the first two trading days of the new one. So investors tend to get excited about it come December.

But some, including the well-respected Morningstar, are speculating that Santa Claus already did his duty. It wrote on December 1 :

“Hope you were good – as the Santa Claus rally came early this year. In our November market outlook, we noted that stocks were trading at a deep discount to fair value. But even we were shocked at how fast and how far stocks surged in November. The Morningstar U.S. Market Index rose 9.4%, one of its best November gains in history.

“Historically, December is a stronger-than-average month for stocks, but this year, the rally started after the November Federal Reserve meeting. Traders interpreted commentary by Federal Reserve Chair Jerome Powell that the Fed had reached the end of this monetary tightening cycle.”

Morningstar also noted how “Growth stocks were the best-performing category in November, rising 11.59%, whereas core and value rose 7.96% and 7.26%, respectively.” It’s therefore recommending investors “to move back to an underweighting in growth stocks,” especially tech.

On the other end of the spectrum, it writes, is the communications category, which has regained “its title as the most undervalued following a rally in real estate.”

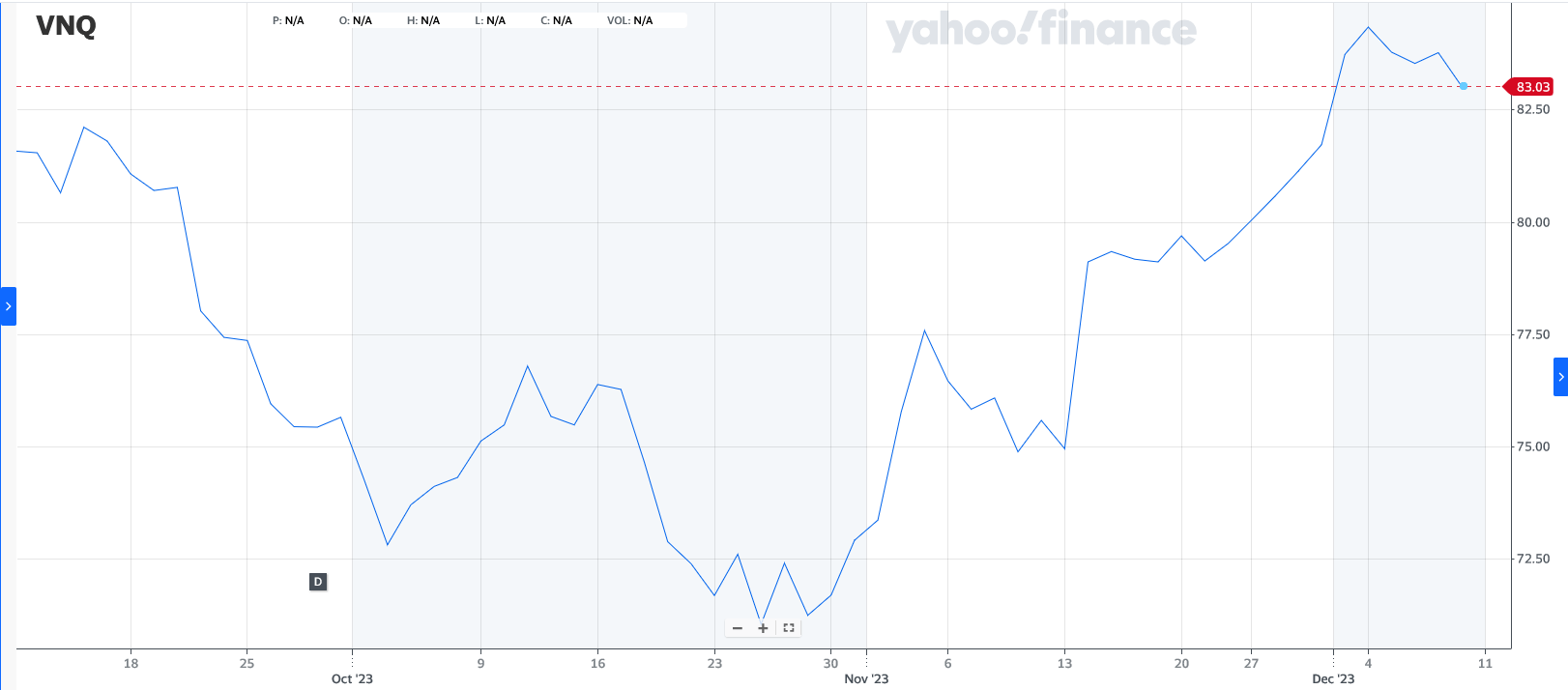

That real estate rally has been noteworthy, as you can see in this three-month chart of the Vanguard Real Estate Index Fund ETF Shares ( VNQ ), which can be used as a REIT proxy index considering how much of the sector it holds.

{kind=link}

Obviously, it’s up.

But I think it’s got a lot more to go.

Here Comes the REIT Rally. Here Comes the REIT Rally Right Down REIT Rally Lane

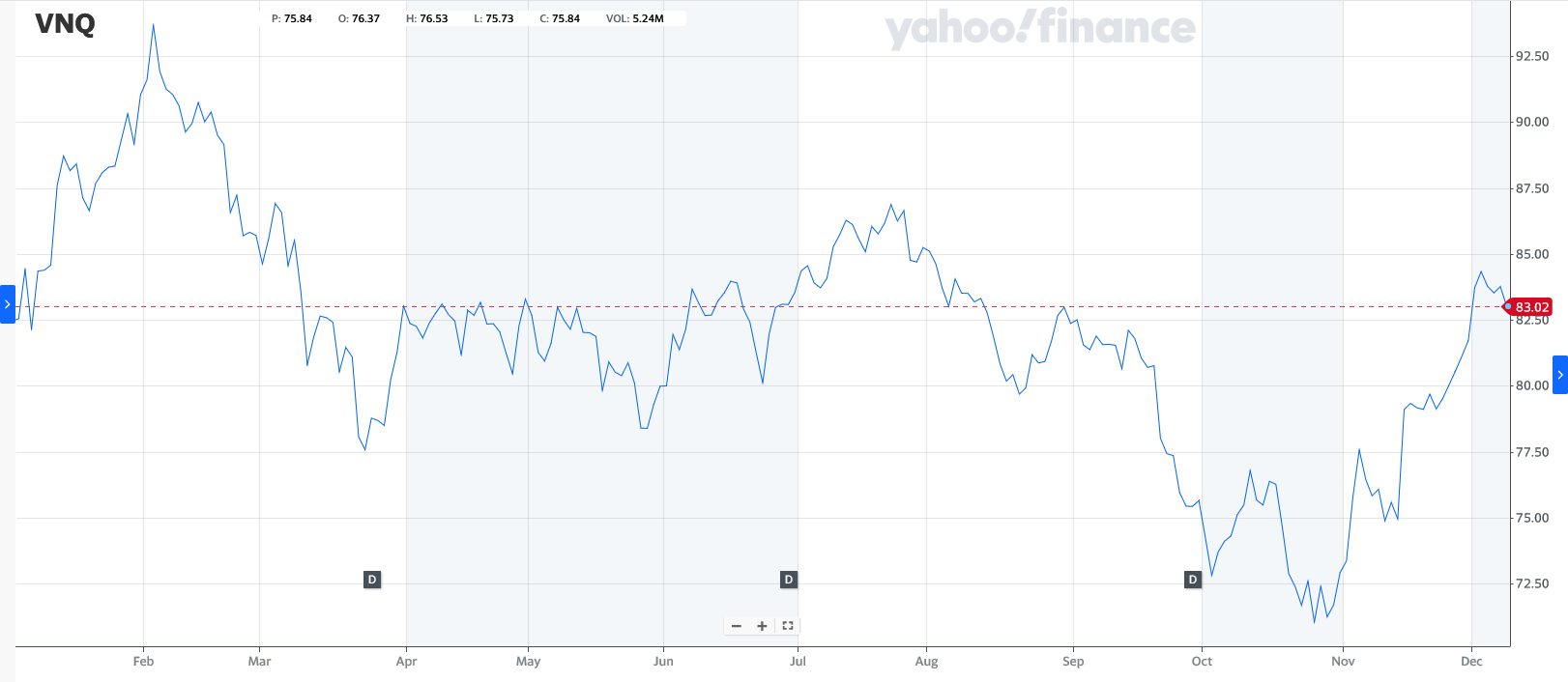

For evidence of this theory, consider this year-to-date chart (as of mid-day December 8):

{kind=link}

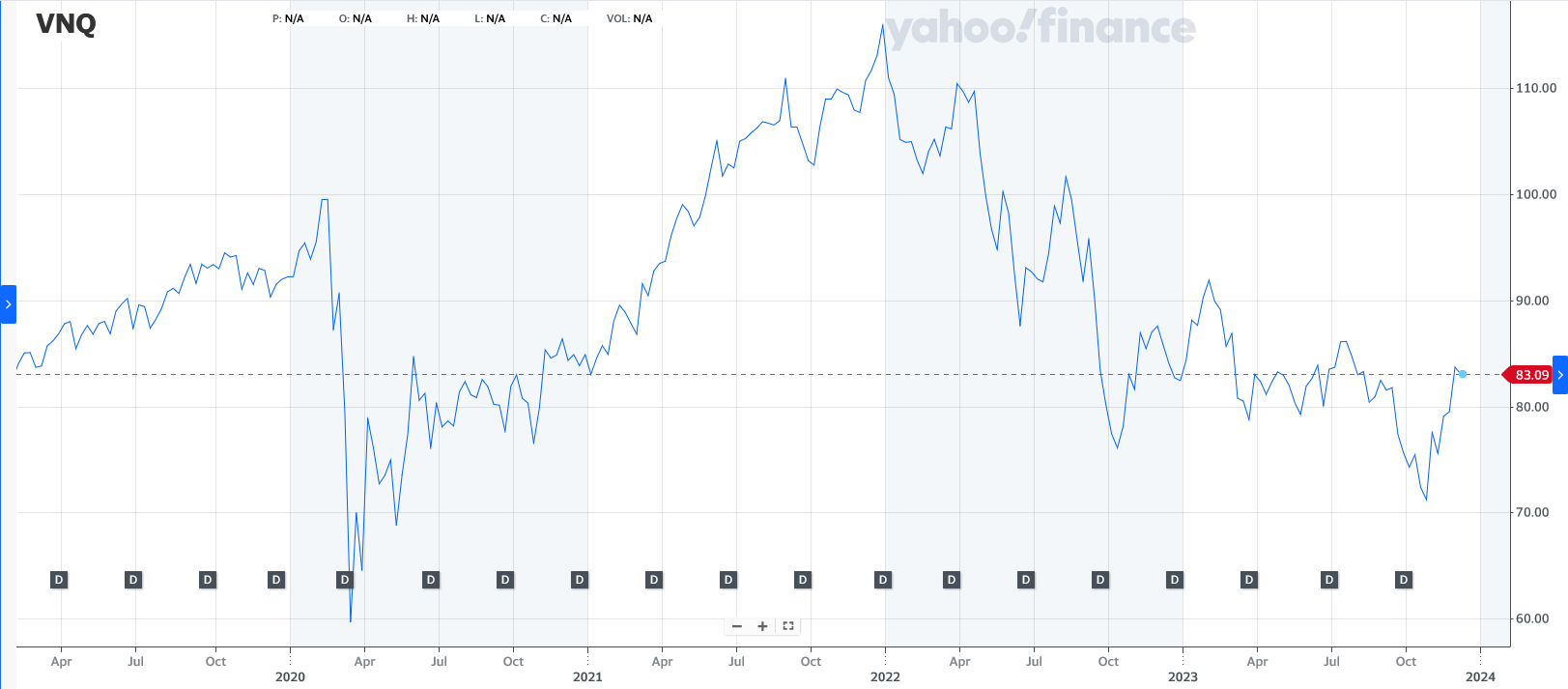

And how about this five-year picture:

{kind=link}

Together, they paint a compelling picture, right?

This is especially true if you do your research into individual stocks.

As I already stated, VNQ is a compilation, holding a significant list of large-cap REITs alongside many of their mid- and small-cap competitors.

So, its price is lifted by those that are doing well and lowered by those that aren’t.

That’s the whole point of an ETF: to provide a diverse and balanced investment vehicle.

Obviously, the intent is for it to go up, but it’s going to go up less than its best holdings.

In VNQ’s case, it also provided dividends.

It’s not a bad setup.

But it simply cannot compare to good, old-fashioned research into individual REITs.

When you’re holding the right ones, you get to enjoy an amazing combination of dividends and share price movement that adds up – a lot – over time.

Can those share prices slump sometimes?

Clearly. Yes.

I’d be an idiot if I said otherwise, especially after that introductory segment I wrote.

Moreover, sometimes REITs can slump for a while.

Then again, sometimes they can pop and stay up for years and years and years on end. And when you’re buying into them at such still-undervalued prices…

Well, that just adds to your profit potential in ways I’ve seen materialize over and over again.

All to say that if you really want to see another Santa Claus rally – and one that keeps giving the whole new year through – consider the following REITs I write about. I see them doling out lots of presents from here.

To prove my point, let’s consider three of my top REIT holdings.

Plenty of Power with American Tower

American Tower Corporation ( AMT ) is a cell tower REIT that owns a global portfolio of nearly 225,000 tower sites, including nearly 43,000 properties in the U.S. and Canada and nearly 182,000 properties internationally.

In 2021, the company acquired CoreSite Realty, adding over 20 data centers to the portfolio.

AMT’s non-cancellable customer lease revenue of nearly $62 billion represents around 6x its 2022 property revenue, and this highly disciplined portfolio diversification strategy drives strong organic tenant billings growth.

5G smartphone access has surpassed the 50% mark in North America, which will eventually allow for the majority of network traffic to shift over to 5G networks which is expected to occur in the 2025 time frame.

AMT’s CEO, Tom Bartlett, pointed out on the Q3 2023 earnings call :

“…the average smartphone subscriber in North America utilizes roughly 21 gigabytes of mobile data per month, and this is expected to grow to about 48 gigabytes by 2028.

Of the 21 gigabytes consumed today, the majority or approximately 19 gigabytes are attributed to video streaming, which corresponds to a little over an hour of daily video usage and 360- and 480-pixel videos currently make up around half of that time.”

In Q3 2023, AMT saw solid growth trends driving consolidated property revenue growth of 7% and 9% growth in the data center business. Also, Adjusted EBITDA grew over 10% to $1.8 billion for the quarter, or approximately 11% on an FX neutral basis.

Adjusted funds from operations, or AFFO, per share increased by over 9%, driven by solid cash adjusted EBITDA growth partially offset by an approximately 5% headwind from financing costs.

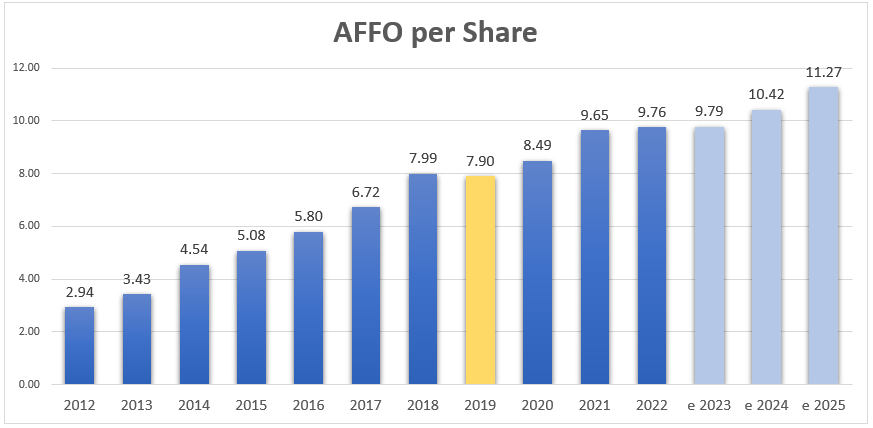

As a result, AMT raised expectations for AFFO by $40 million at the midpoint, or approximately $0.09 on a per share basis, moving the midpoint to $9.79 per share.

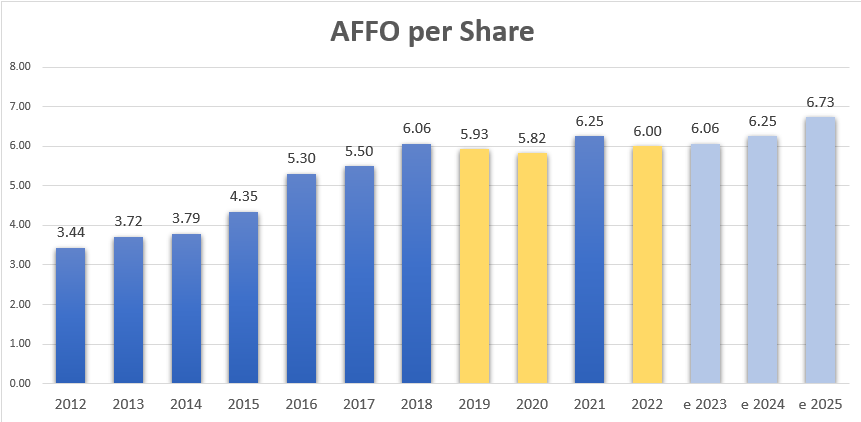

As you can see below, there was only one year in which AMT generated negative growth (2019), and it was just -1.1%.

{kind=link}

This signals a steady hand within AMT’s capital markets team.

Consistent with AMT’s expectation the company plans to distribute around $3 billion in dividends in 2023, which represents a year-over-year growth rate of 10%.

I also want to highlight the fact that AMT reduced its floating rate debt to below 11% and increased liquidity to $9.7 billion, with an average maturity of 6 years. At the end of Q3 2023, net leverage was around 5x and the company is rated BBB- by S&P.

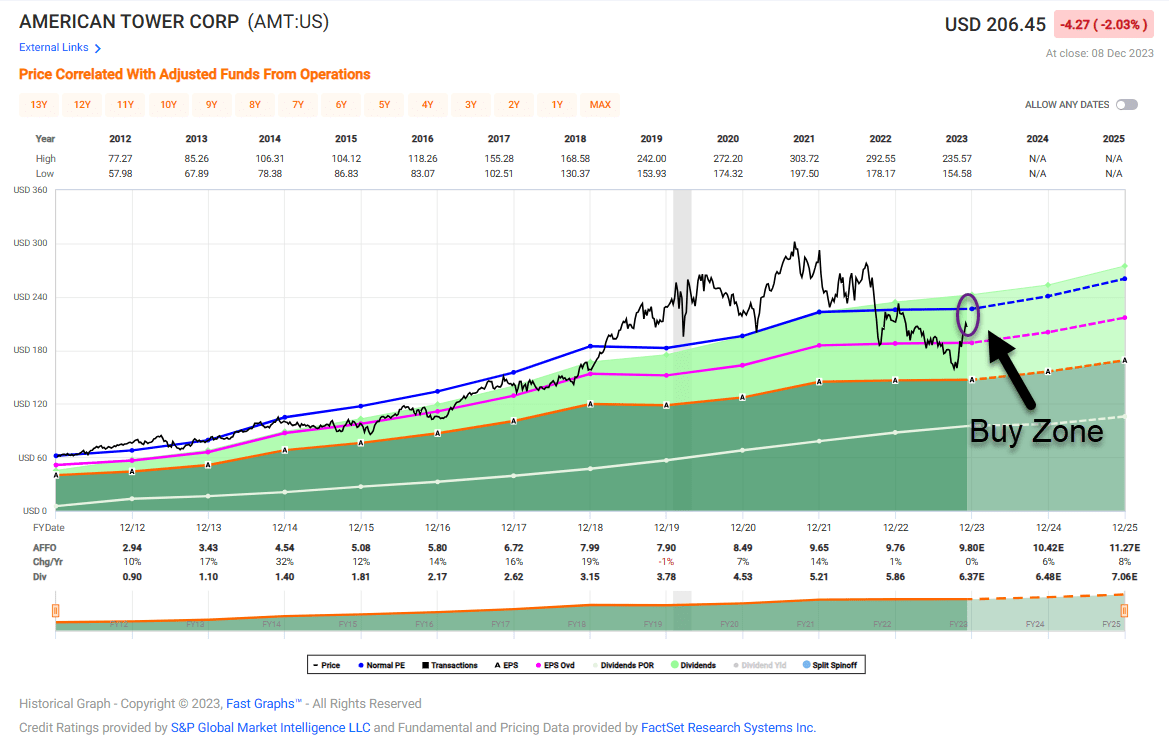

You may recall that I recommended AMT at the end of September and shares have since returned over 16% (versus the S&P 500 (SP500) that has returned 3.4%). AMT shares are now trading at $178.99, with a P/AFFO multiple of 21.0x (compared with the normal P/AFFO of 23.1x).

I have an overweight allocation in AMT, and I plan to hold onto my shares. As seen below, shares are still in our “Buy Zone”:

{kind=link}

I’m still layering-in capital with this REIT, which I consider to be the best cell tower play.

iREIT®

As you may know, Crown Castle Inc. ( CCI ) is in the midst of an activist-led battle as shares have persistently underperformed due to lower ROIC and capital-intensive fiber (small cell) investments. I recognize there’s value to unlock with CCI, but I prefer the much less complicated AMT story.

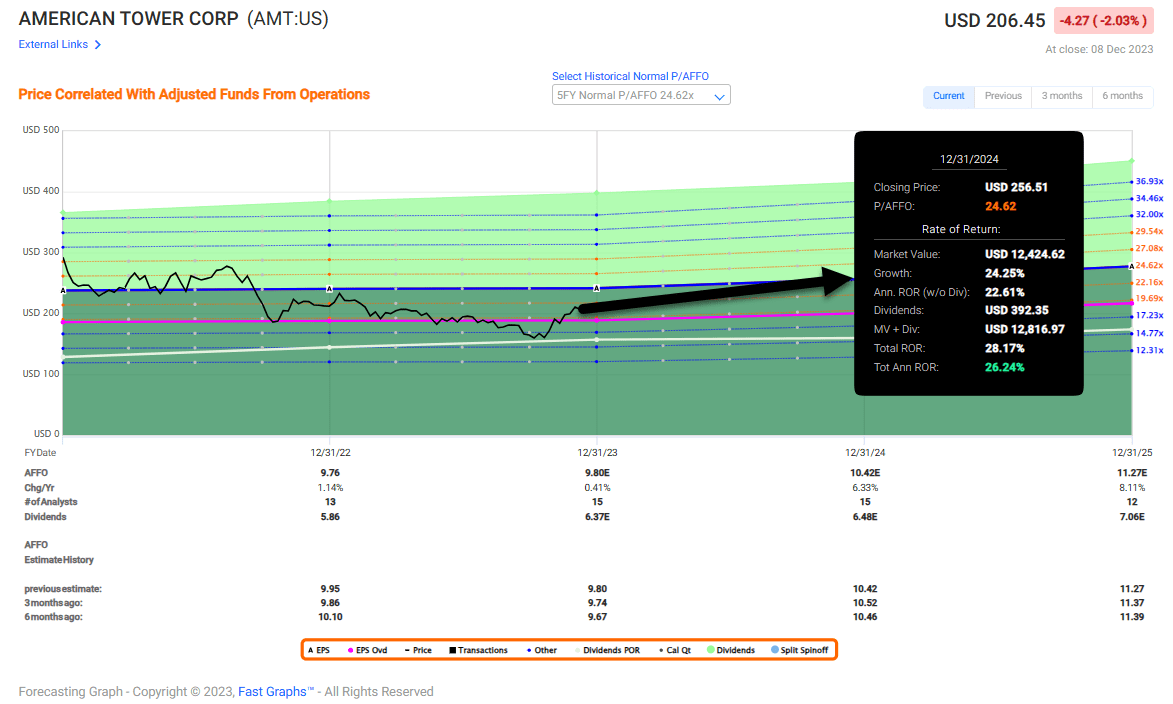

I’m sticking with AMT, and as shown below, we estimate shares could return over 20% annually (on top of the 16% growth over the last few weeks).

{kind=link}

A Data Center Diva

Digital Realty Trust, Inc. ( DLR ) is a data center REIT that owns 310 data centers with over 5,000 global customers with facilities located in 25+ countries and 50+ metros. The REIT has an Enterprise Value of over $55 billion and is the 5 th largest publicly traded U.S. REIT (added to the S&P 500 in 2016).

Over the last decade DLR has put together a string of acquisitions including:

- 2015 : Telx (U.S. Colocation Provider, Interconnection and Cloud Enablement)

- 2016 : European Portfolio Acquisition (8 highly connected carrier-neutral data centers)

- 2017 : DuPont Fabros (North American REIT)

- 2018 : Ascenty (leading Latin America Data Center provider)

- 2020 : Interxion (leading colocation and interconnection provider in Europe)

- 2022 : Teraco (South Africa’s leading colocation and interconnection provider).

Just days ago, DLR announced two new deals:

- DLR and Realty Income Corporation ( O ) formed a JV that will build two data centers in northern Virginia. Realty Income will invest $200 million to acquire an 80% stake in the JV. The build-to-suit facilities are 100% pre-leased to an S&P 100 investment-grade client before construction and are expected to generate a 6.9% initial cash lease yield upon lease commencement in mid-2024.

- DLR and Blackstone ( BX ) are forming a JV to build $7 billion to build 10 data centers in Paris, Frankfurt and northern Virginia over the next 5 to 6 years. Similar to the Realty Income deal I just mentioned, BX will own 80% and DLR will own 20%.

Let’s take a look at DLR’s earnings (AFFO per share) history:

{kind=link}

As you can see, DLR’s earnings history is not as strong as AMT, but the data center REIT has still generated 5.5% CAGR since 2012. Importantly, the company has maintained steady capital markets discipline with consistent access to capital.

DLR Investor Presentation

At the end of Q3 2023, the company had reduced leverage by 0.8 turns of EBITDA (since Q1-23) and increased liquidity to $3-plus billion, including $1 billion of cash. DLR’s leverage fell to 6.3x net debt to EBITDA, down from 6.8x at the end of the Q2 and should achieve its year end goal of 6x.

The company’s weighted average debt maturity is over 4.5 years, with a weighted average interest rate of 2.9%. Less than $1 billion of debt matures in 2024 and beyond, and maturities remain well laddered through 2032.

In Q3 2023 , DLR reported core FFO per share of $1.62, down $0.06 from Q2 2023 due to asset sales and equity raised. Total revenue was up 18% year-over-year and 3% sequentially despite the impact of the more than $2 billion of asset sales completed.

DLR’s full year revenue guidance range was adjusted down by about 1% at the midpoint to a new range of $5.475 billion to $5.525 billion to reflect the impact of lower pass-through oriented tenant utility reimbursements.

You may recall that I recommended DLR back in June 2023 when shares were trading at $106.29. I explained,

“I’m piling back into Digital realty, recognizing that there’s a tremendous opportunity to capitalize on what I consider to be one of the best business models on the planet.”

DLR is my second largest position and I’m +40%.

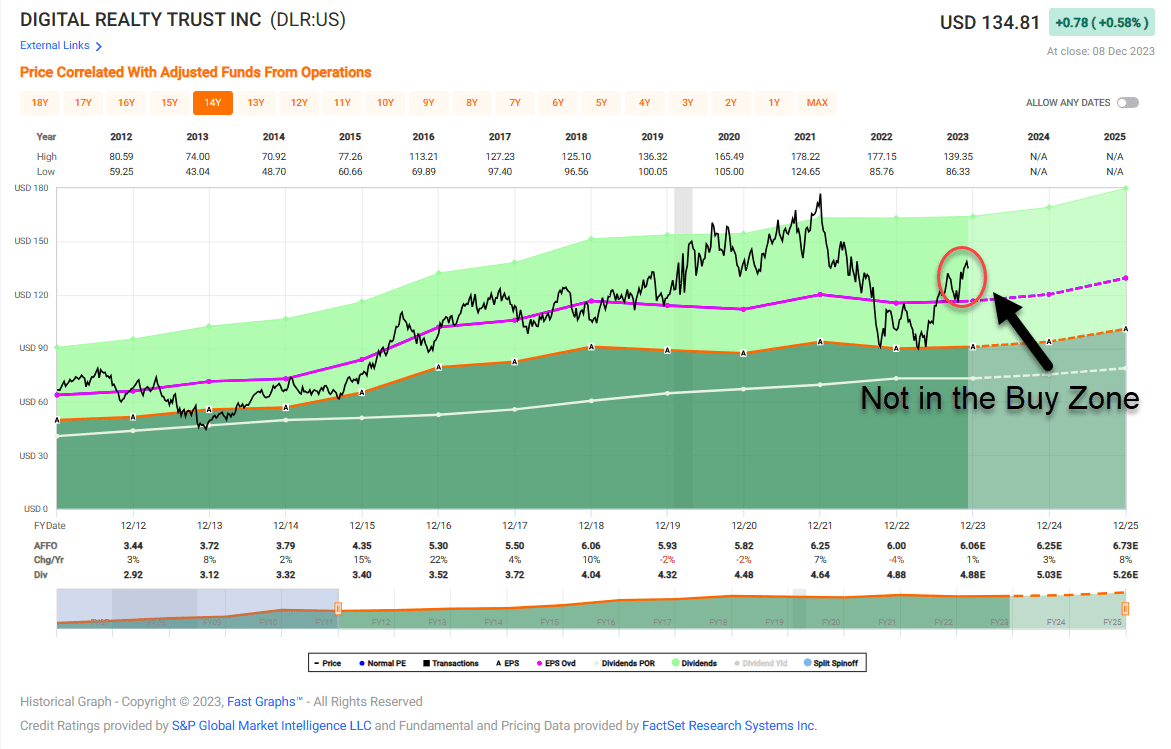

Shares are now trading at $134.81 with a P/AFFO multiple of 22.3x (normal is 19.2x). I consider shares expensive and I would not recommend buying now.

The dividend yield is 3.6% and well-covered with a payout ratio of 80%. Analysts are forecasting growth of 3% in 2024 and 8% in 2025 (when the development pipeline kicks in).

{kind=link}

My Largest Holding

Realty Income Corporation is my largest holding that represents around 10% of my portfolio. I’ve owned shares in the company for over a decade now and I’ve been increasing my stake over the last several months.

Realty Income owns over 13,250 properties (in 50 states, Puerto Rico, Italy, Spain, and the UK) that consists of 1,324 customers that operate in 85 industries.

In late October, the company announced it was acquiring Spirit Realty ( SRC ), which will add another 2,064 properties (in 49 states) to the Realty Income portfolio.

The Spirit transaction is expected to be over 2.5% accretive to Realty Income AFFO per share with expected annual synergies of approximately $50 million, or approximately $30 million excluding stock-based compensation.

Upon closing the deal, Realty Income will become the 4 th largest REIT and 150 th largest company in the S&P 500.

In addition to M&A, I expect Realty Income to continue its dominance (in the net lease sector) by targeting select sale-leaseback clients like the $1.7 billion Encore Boston Harbor transaction that closed in December 2022.

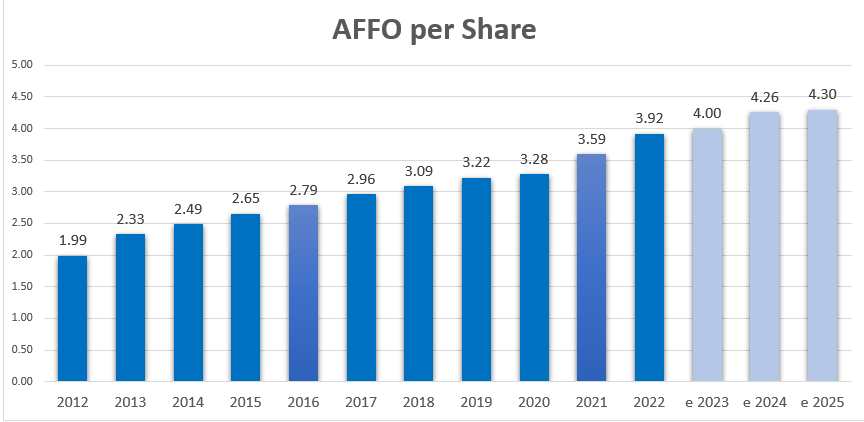

As seen below, Realty Income has a strong history of judicious capital markets discipline:

{kind=link}

As you can see, Realty Income has grown AFFO per share in every year since 2012, and the company has only seen one declining year (of AFFO per share) in its history as a public company (in 2009).

The dividend history is impressive: 29 consecutive years of rising dividends and a member of the S&P 500 Dividend Aristocrats' index.

That’s the mark of blue-chip stock!

In addition to the $9.3 billion Spirit Realty deal I just mentioned, Realty has closed on over $6.8 billion thru Q3-23. And to fuel the growth, the company has maintained strict capital markets discipline with an A3/A- credit rating.

During Q3 2023, net debt to annualized pro forma adjusted EBITDA and fixed charge coverage ratios each fell by 10% to 5.2x and 4.5x, respectively. Combined with cash on hand of $344 million, the net availability on the credit facility of $3.4 billion was $4.5 billion of liquidity.

As a result of a solid Q3 , Realty increased its guidance range : AFFO per share $3.98 to $4.01.

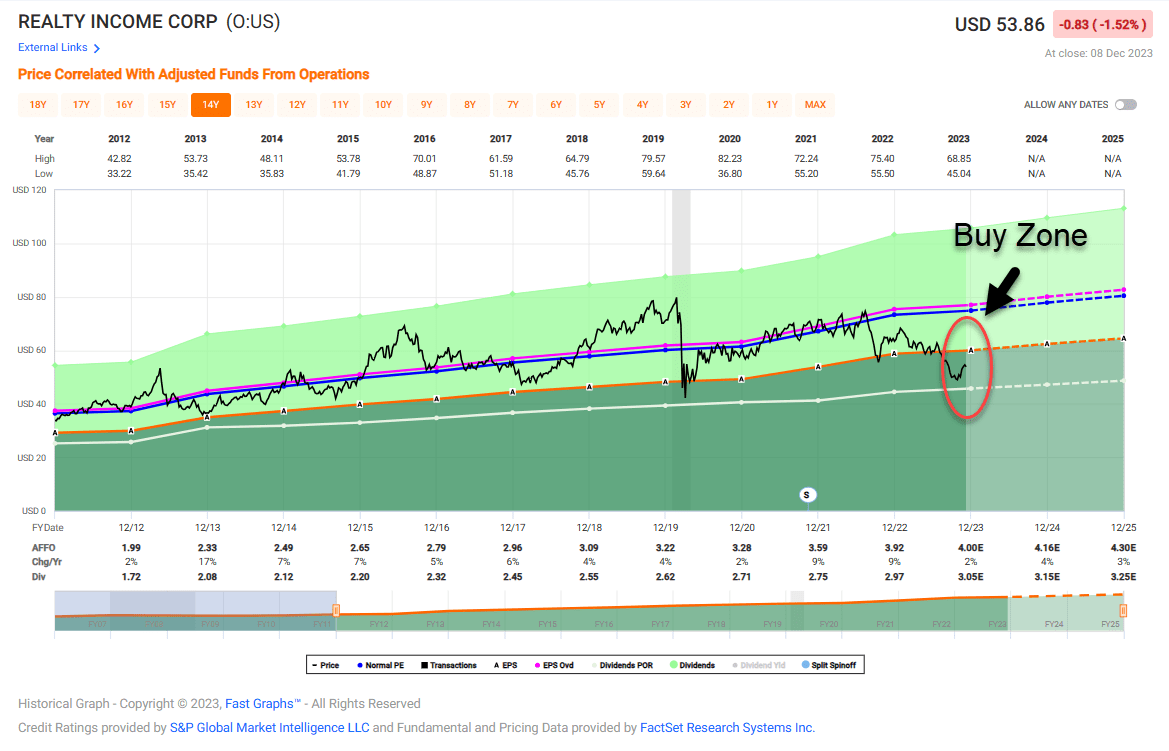

As seen below, Realty Income has traded up by ~15% since the end of October, however, shares remain well within our Buy Zone:

{kind=link}

Currently they’re priced at $53.86 with a P/AFFO multiple of 13.5x (normal is 18.7x). The dividend yield is 5.7% and well-covered (based on a payout ratio of 76%).

Analysts are forecasting growth of 4% in 2024 and 3% in 2025, plenty to support future dividend growth.

The reason that I’ve been quietly adding shares to my position is because of the stability of the business model. I’ve watched the evolution of Realty Income since around 2000 (when I was a net lease developer) and I’ve seen how the “moat” has become wider and wider.

This REIT exemplifies the “margin of safety” principle in which the discounted price builds in a significant buffer. While valuation is always subjective, the 13.5x P/AFFO multiple represents a telling indicator in which this blue chip A-rated REIT is trading at a minimum 25% discount.

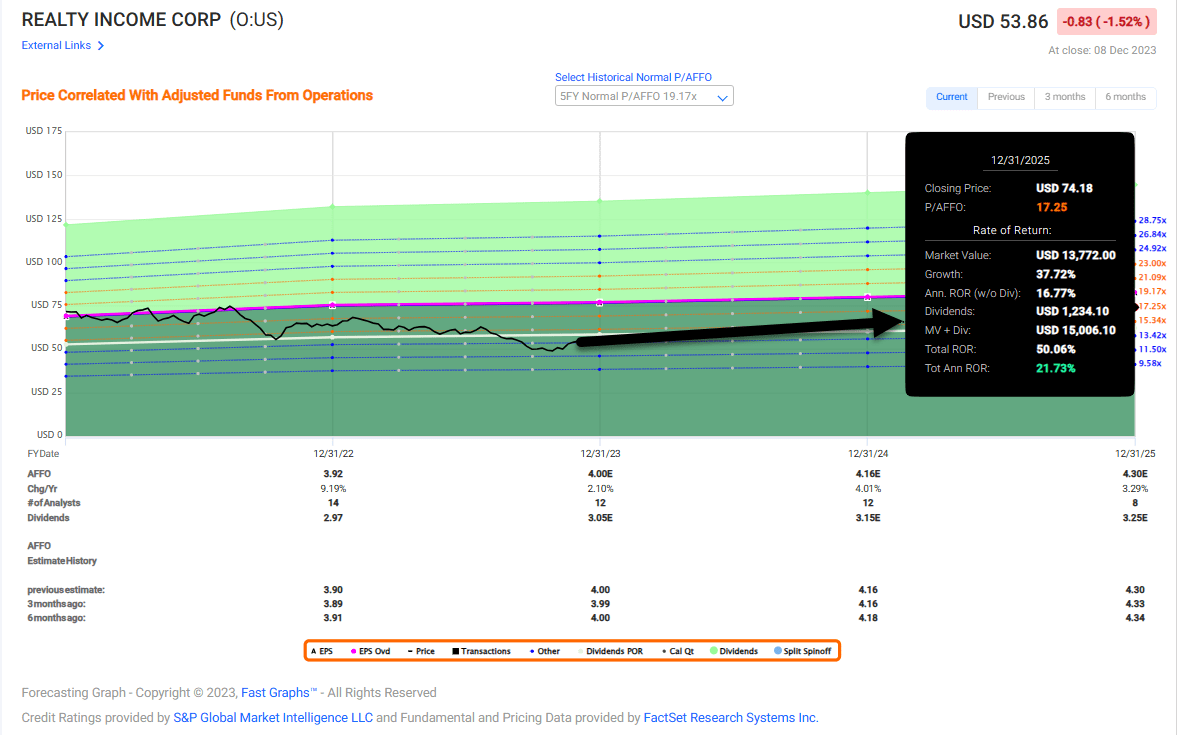

Our most conservative estimates has shares returning 20% in 12 months (that’s the permanent pause scenario):

{kind=link}

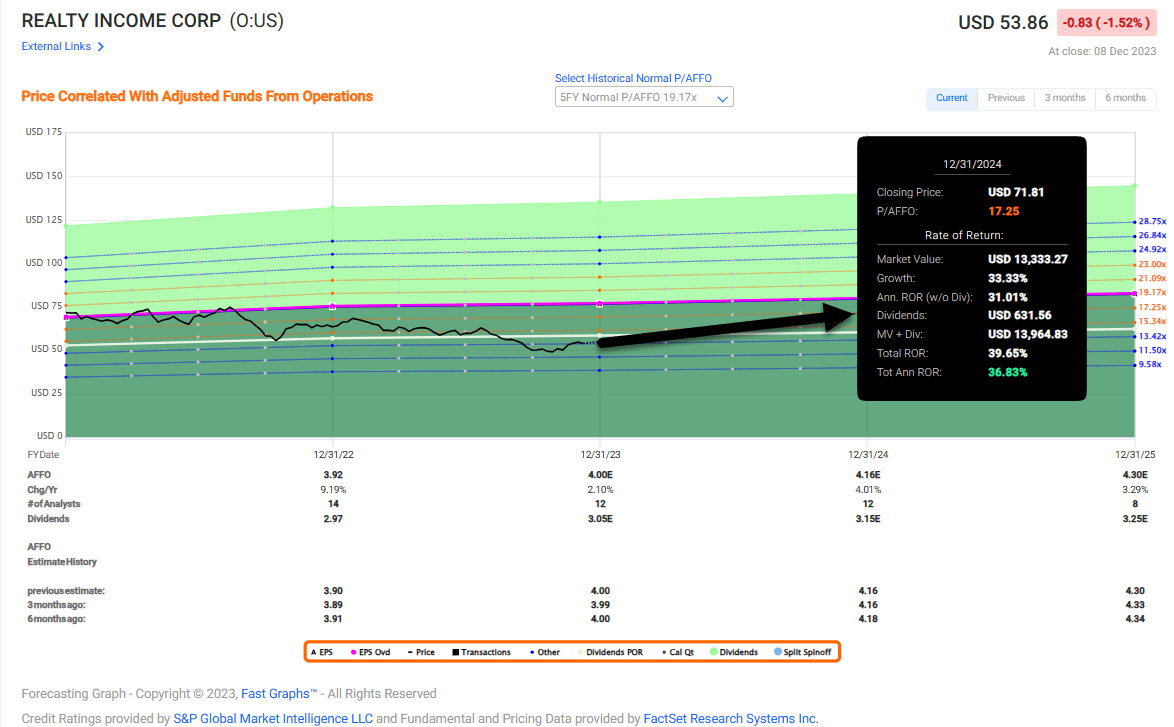

Our most likely scenario is that rates will fall in 2024.

In fact, Morningstar projects a year-end 2023 federal-funds rate of 5.25%, falling to about 2.00% by the end of 2025. That will help drive the 10-year Treasury yield (US10Y) down to 2.50% in 2025 from an average of 4% in 2023.

This could result in Realty Income returning over 35% annualized as shown below:

{kind=link}

Santa Baby!

If Morningstar is right, REITs will rally in 2024.

I like my odds and the picks that I’ve provided here.

While Digital Realty is no longer cheap, I believe there’s more room to run, and I’m perfectly content with my outsized position in this data center giant.

Also, American Tower (another giant) is the best play in towers, and I expect to see the company increase the size of its “moat” and its dividend payout.

Finally, Realty Income is a world-class REIT that I’m happy to own forever.

The competitive advantages are the envy of the REIT sector, and I’m happy that Mr. Market has given me the opportunity to build a sizeable position that can be enjoyed for generations.

Now, let me ask you this question…

Who’s ready for a Santa Claus REIT Rally?

Ho, Ho, Ho…

For further details see:

Who's Ready For A Santa Claus REIT Rally?