BRSP - Who's Scooping Up These High-Yielding Mortgage REITs?

2023-07-06 07:00:00 ET

Summary

- I’m a fan of commercial mREITs that are differentiated from their riskier residential cousins, because of their lower leverage and significant floating rate exposure that benefits from rising rates.

- I like owning around 10% in commercial mREITs (within my REIT portfolio); however, I’m increasing that to ~20% given the attractive opportunity I see unfolding right now.

- Where do these landlords get funds to refinance these debt maturities?

- You guessed it: Commercial mREITs.

This article was published at iREIT® on Alpha on Tuesday, July 4, 2023.

I must say, I’m feeling the love for high-yielding mortgage real estate investment trusts, or mREITs.

I’m talking about yields from 9% to 12%.

Now, before you call me names, I want to first let you know that I’m not talking about residential mREITs like Annaly Capital Management, Inc. ( NLY ) or Cherry Hill Mortgage Investment Corporation ( CHMI ), both chronic dividend cutters that have returned an average of 2% per year in a decade.

(See my recent article on NLY and CHMI .)

I don’t recommend investing in any of these more toxic residential mREITs that have been nothing but value destroyers, regardless of your skillset in the REIT sector.

However, I’m a fan of commercial mREITs that are differentiated from their riskier residential cousins, because of their lower leverage and significant floating rate exposure that benefits from rising rates.

Typically, I like owning around 10% in commercial mREITs (within my REIT portfolio), however, I’m increasing that to ~20% given the attractive opportunity set unfolding right now.

One primary catalyst supporting my REIT blueprint is the fact that banks are not doing much real estate lending. Unless you’re a professional like a dentist or doctor (who owns real estate), most banks are not making CRE Loans these days.

So, who’s going to service the regional and community banks that hold 31.5% of all commercial real estate mortgages (20% of total assets)?

The Mortgage Bankers Association released a survey estimating the maturity profile of all commercial and multifamily mortgages, including those held by banks and non-bank lenders.

They calculate $728 billion (16% of total loans) will mature in 2023, with another $659 billion (15%) maturing in 2024. Hotels/motels have the largest share of their loans maturing in 2023 (34%), followed by office (25%). Multifamily has the smallest share of outstanding mortgages maturing in 2023 (9%).

The greatest risk lies in loans originated over the past several years at peak valuations, especially if they have shorter maturities.

About 56% of all outstanding CMBS was issued from 2019 to 2023 YTD, consisting of less than 1% for the 2023 vintage, 14% for the 2022 vintage, 21% for the 2021 vintage, 7% for the 2020 vintage, and 13% for the 2019 vintage.

Where do these landlords get funds to refinance these debt maturities?

You Guessed it : Commercial mREITs.

iREIT®

BXMT: Yielding 12.1%

Blackstone Mortgage Trust, Inc. ( BXMT ) is externally managed by Blackstone Inc. ( BX ) and is a mortgage real estate investment trust that specializes in loan origination of senior, floating rate mortgage loans backed by commercial real estate in North America, Australia, and Europe.

While BXMT’s primary focus is on floating rate senior loans, they may also acquire and originate subordinate and fixed rate loans.

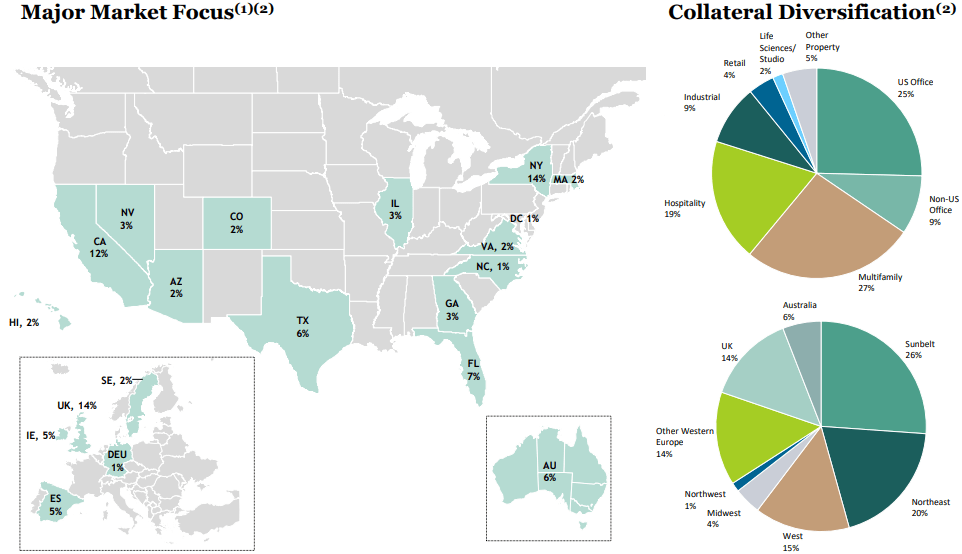

BXMT has a $26.7 billion senior loan portfolio that consists of 199 loans with a weighted average origination loan-to-value of 64% . BXMT is well diversified by region and by the property type serving as collateral. 26% of their loan exposure comes from the U.S. Sunbelt region, 20% comes from the U.S. Northeast region, and 15% comes from the Western region of the U.S. Internationally, 14% of their loan exposure comes from the U.K., 14% comes from Western Europe, and 6% comes from Australia.

BXMT’s largest asset class is office properties that makes up 34% of their loan exposure (both U.S. and non-U.S. properties), followed by multifamily which makes up 27%, hospitality which makes up 19%, industrial which makes up 9%, and retail properties which makes up 4% of their loan exposure.

{kind=link}

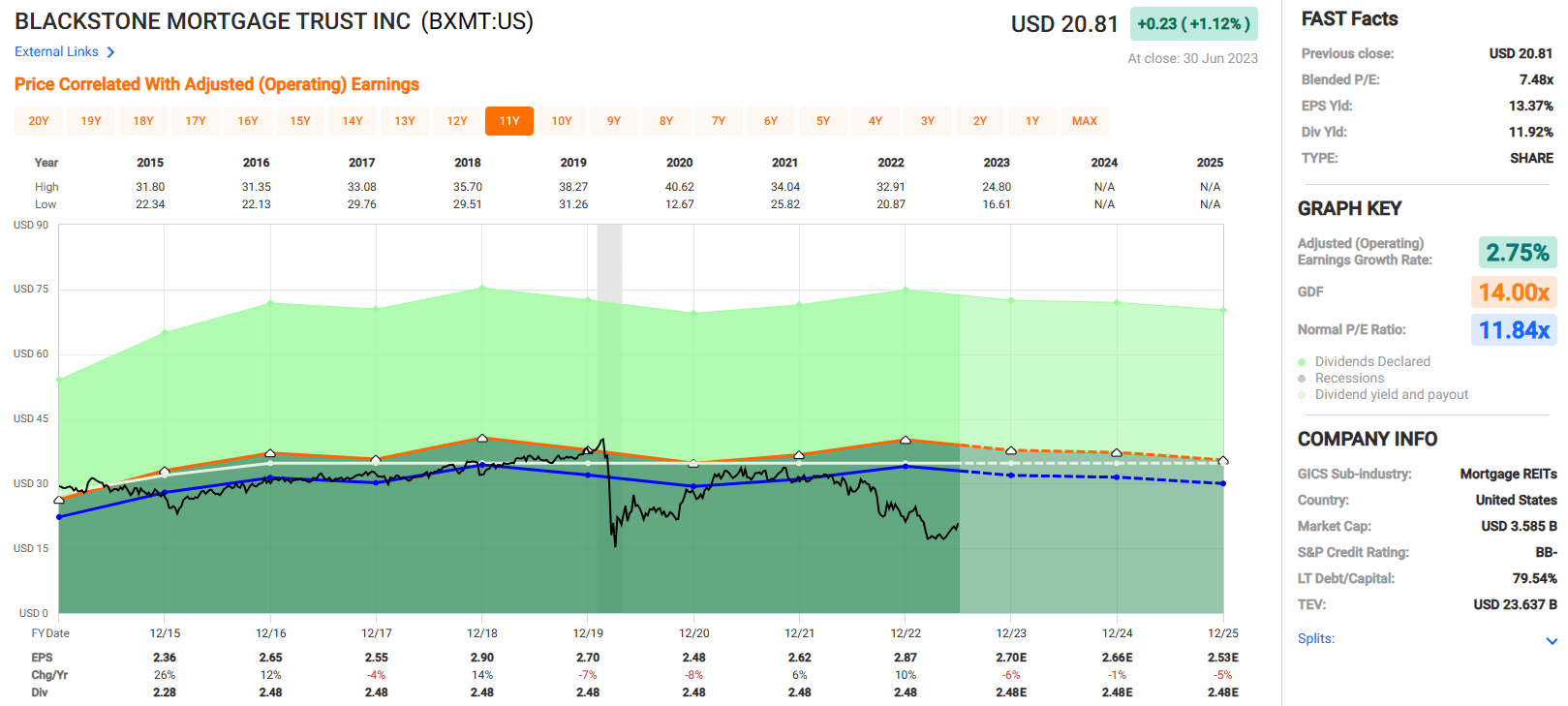

BXMT paid a first quarter dividend of $0.62 compared to their first quarter distributable earnings of $0.79 per share, which put their dividend payout ratio at 78.4%.

BXMT has been very consistent with its distributions with a dividend of $0.62 paid for 31 consecutive quarters, and currently the current dividend yield is 12.1%.

BXMT’s stock has fallen almost 27% over the last year, putting the mortgage REIT on sale with a P/E of 7.48x vs. their normal P/E ratio of 11.84x.

At iREIT®, we rate BXMT stock a BUY and assign it a tier 1 rating.

{kind=link}

STWD: Yielding 10.0%

Starwood Property Trust, Inc. ( STWD ) is an externally managed mREIT that specializes in originating, acquiring, and managing mortgage loans and other types of real estate investments in the U.S., Europe, and Australia.

STWD conducts its operations through 4 business segments that include Commercial and Residential Lending, Infrastructure Lending, Real Estate Property, and Real Estate Investing and Servicing.

Through their Commercial and Residential Lending segment they originate and manage first mortgage loans for commercial properties, non-agency residential mortgages, mezzanine loans, subordinate mortgages, residential mortgage-backed securities (“RMBS”), commercial mortgage-backed securities (“CMBS”), and preferred equity.

Through their Infrastructure Lending segment they originate, acquire and manage debt instruments related to infrastructure projects.

Their Real Estate Property segment invests in equity interest in multifamily and net-lease commercial properties that are held for investment, and their Real Estate Investing and Servicing segment focuses on investing in businesses that acquires CMBS and businesses that originate conduit loans that are securitized and sold to third parties.

{kind=link}

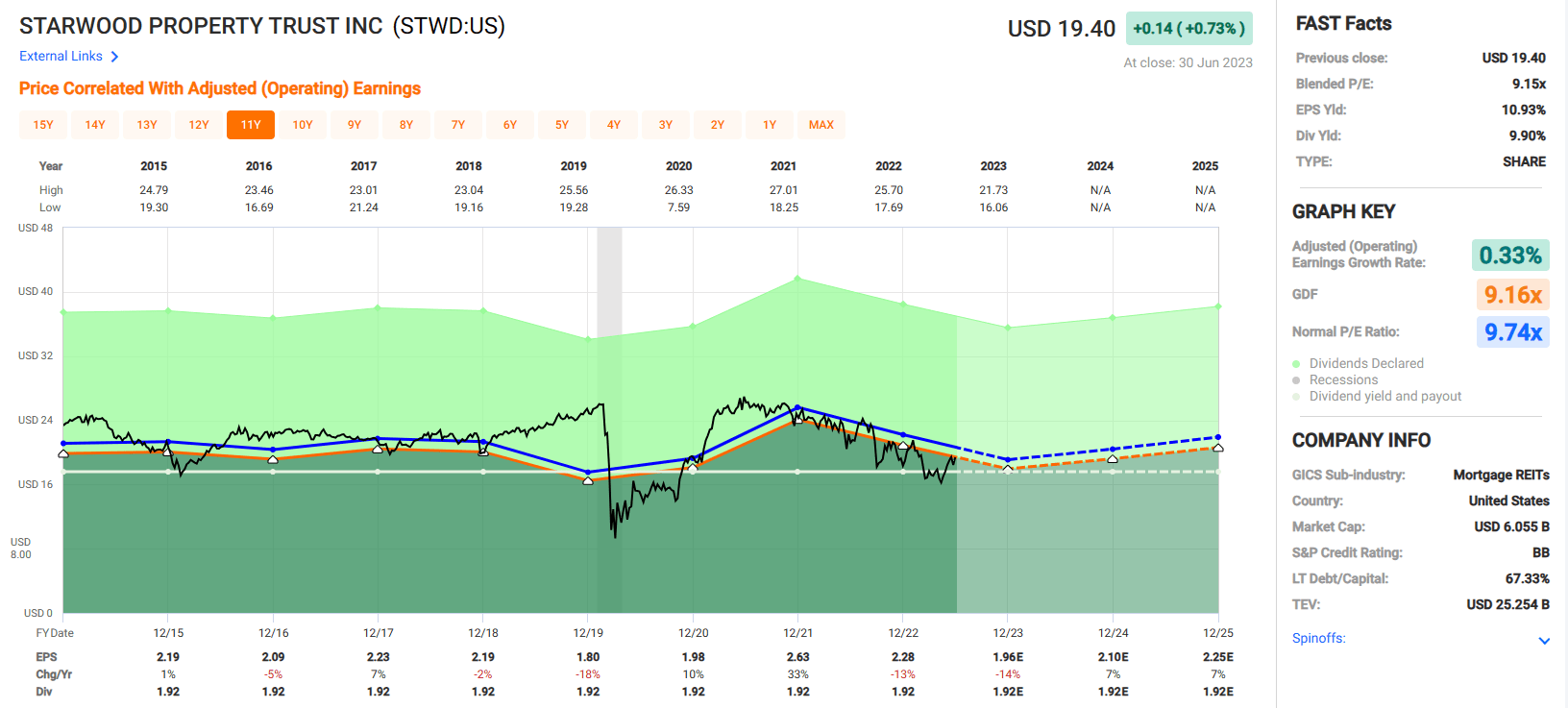

For the first quarter, STWD reported distributable earnings of $0.49 per share and paid a first quarter dividend of $0.48, for a dividend payout ratio of 98% .

Since 2014, STWD has paid an annual dividend of $1.92 per share and currently pays a 10.0% dividend yield.

Analysts expect adjusted operating earnings to fall by 14% in 2023 but then increase by 7% in both 2024 and 2025. Currently the stock trades at a P/E of 9.15x, which is a slight discount to their normal P/E ratio of 9.74x.

At iREIT®, we rate STWD stock a BUY and assign it a tier 1 rating.

{kind=link}

LADR: Yielding 8.6%

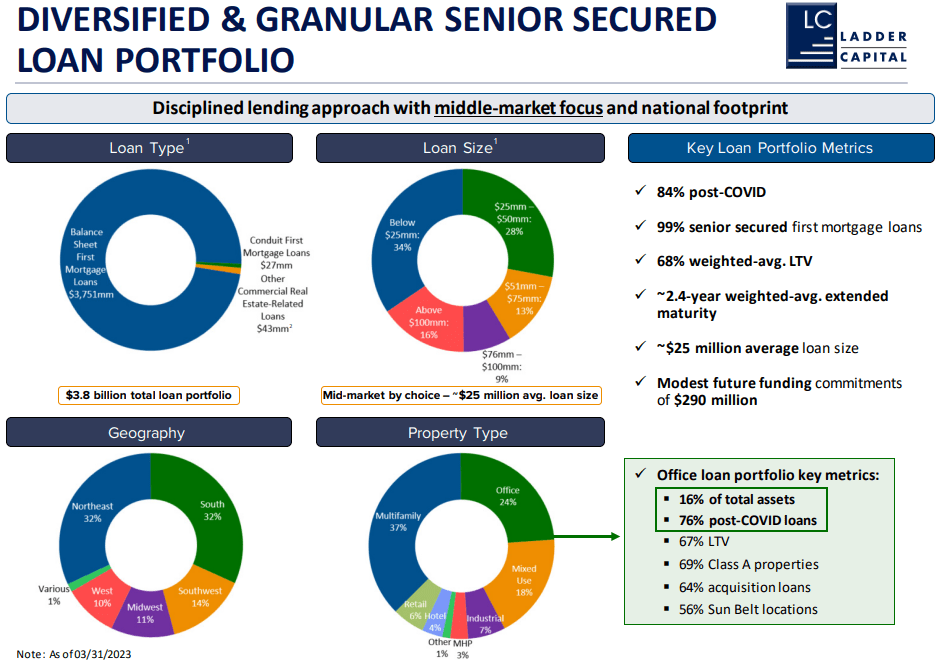

Ladder Capital Corp ( LADR ) is an internally managed mREIT that specializes in originating senior first mortgage fixed and variable rate loans that are secured by commercial real estate.

They generate interest income and rental income through their businesses which includes balance sheet lending, securities investments, conduit lending, and real estate investments. As part of their lending operations, LADR originates first mortgage conduit loans on stabilized properties that are securitized into CMBS and sold to third parties.

Additionally, they own and operate net-lease commercial properties and invest in investment grade securities that are secured by first mortgage loans.

LADR has a $3.8 billion loan portfolio that primarily consists of balance sheet first mortgage loans and to a much lesser extent conduit and other commercial real estate loans. 99% of their loan portfolio consists of senior secured first mortgage loans with a weighted average LTV of 68% and an average loan size of $25 million.

{kind=link}

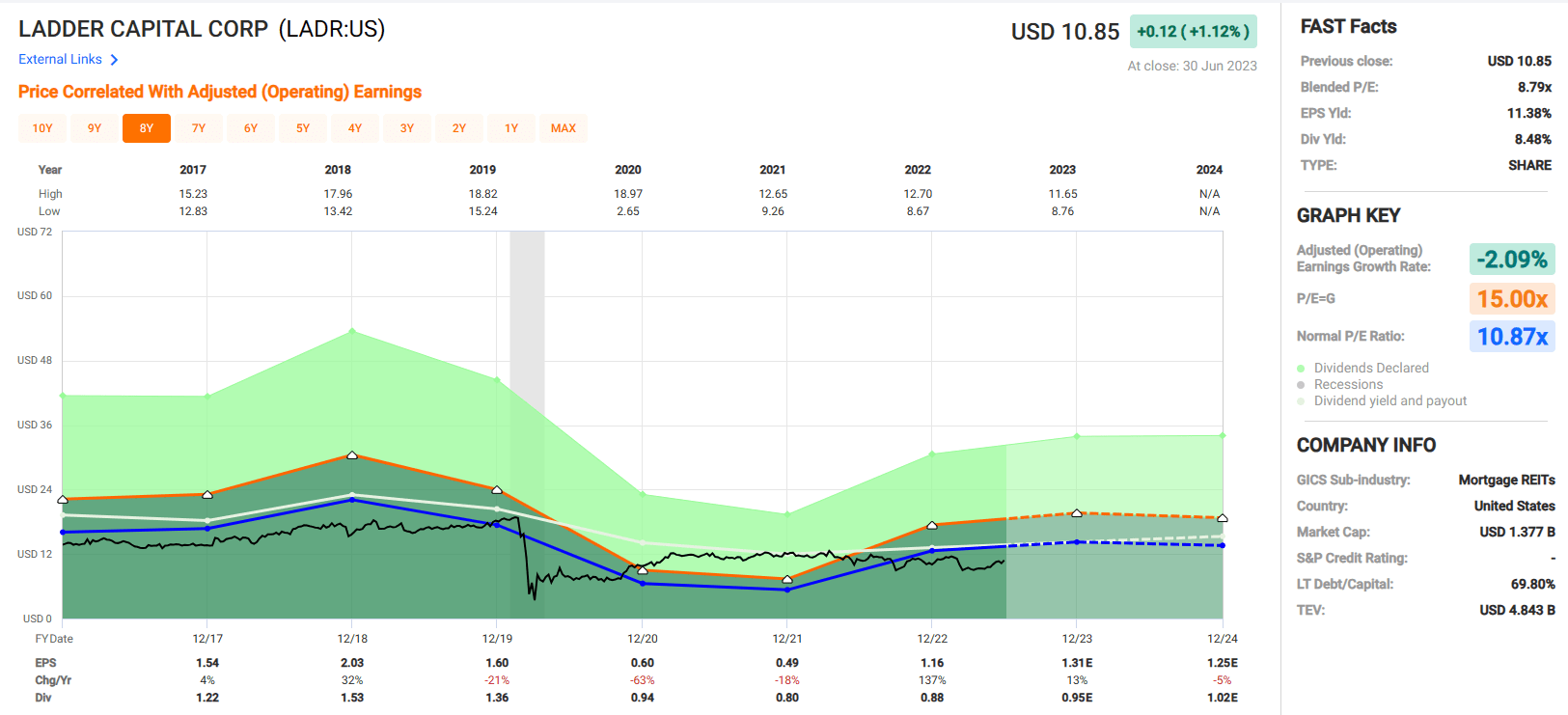

LADR reported $0.38 in distributable earnings per share for the first quarter and paid a $0.23 quarterly dividend, for a dividend payout ratio of just 60.5% when based on distributable earnings.

Their adjusted operating earnings fell each year from 2019 to 2021 but increased by 137% in 2022.

Analysts expect earnings to increase by 13% in 2023 and then fall by 5% in 2024. Currently, LADR pays a 8.48% dividend yield and trades at a P/E of 8.79x, which compares favorably to their normal P/E ratio of 10.87x.

At iREIT®, we rate Ladder Capital stock a BUY and assign it a tier 1 rating.

{kind=link}

BRSP: Yielding 12.0%

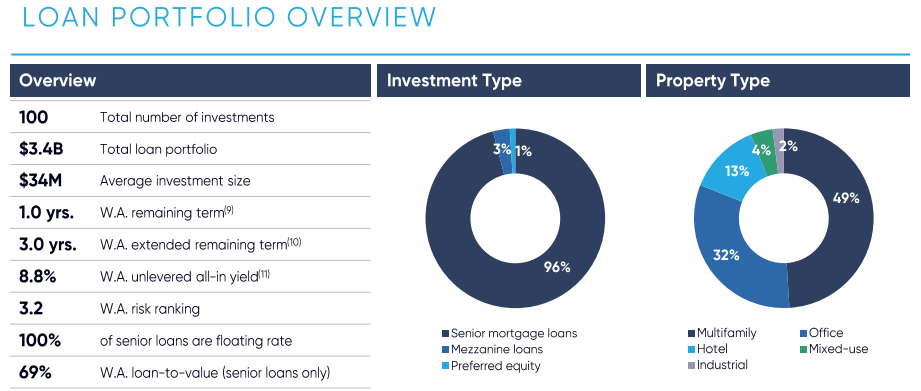

BrightSpire Capital, Inc. ( BRSP ) is an internally managed mREIT that originates and manages a portfolio of commercial real estate debt investments and invests in net-leased real estate properties that are primarily located in the U.S.

BRSP’s debt investments mainly consist of senior mortgage loans but may also include mezzanine loans and preferred equity investments. BRSP’s primary business is originating and acquiring senior loans that are collateralized by commercial real estate assets.

Their senior loans are issued to developers and owners of commercial properties to provide mortgage financing and may be issued at fixed or floating rates. In addition to their investments in debt instruments, BRSP also selectively invests in commercial real estate that is leased to tenants on a long-term, net-lease basis where the tenants are responsible for the property operating expenses.

BRSP’s has a $3.4 billion loan portfolio that consists of 100 investments with an average investment size of $34 million and a weighted average loan-to-value of 69% for their senior loans.

{kind=link}

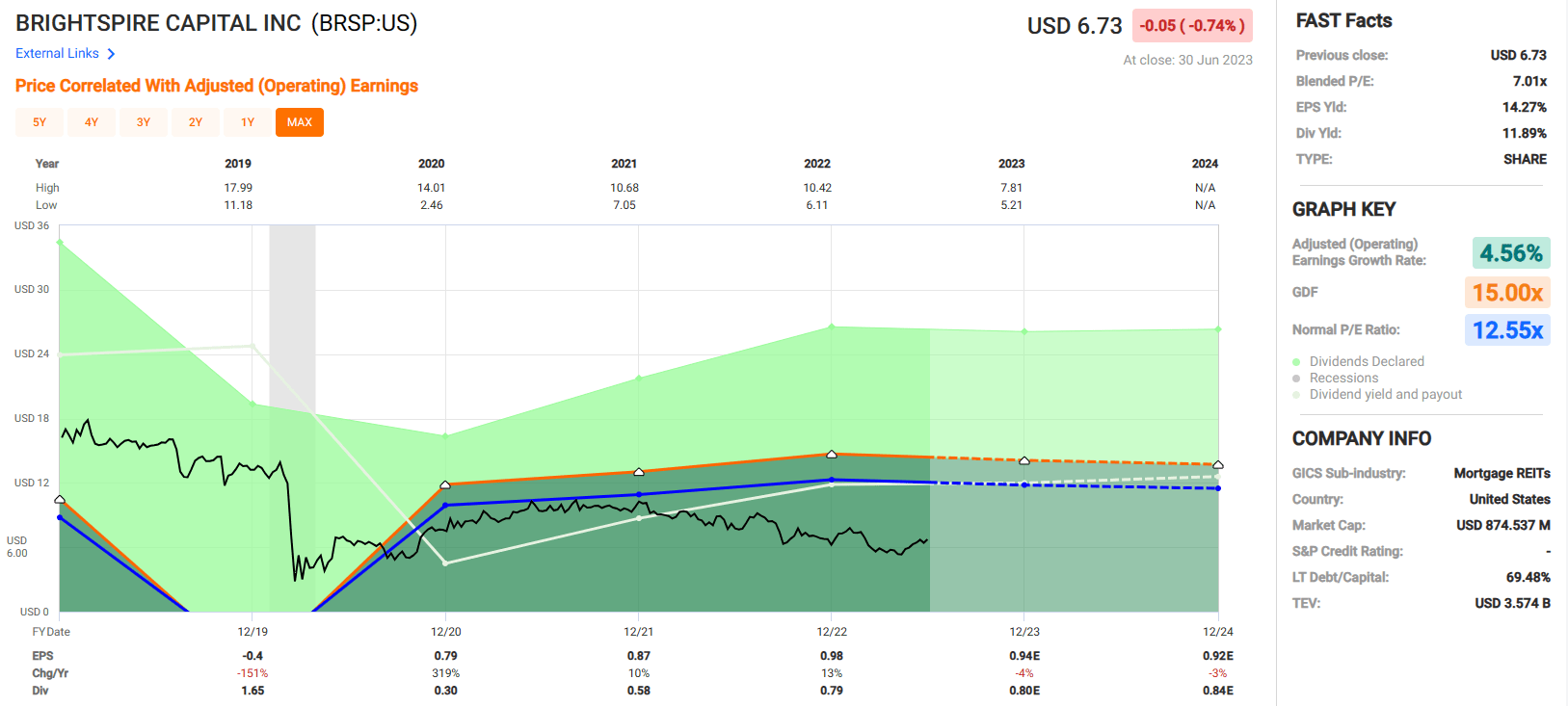

For the first quarter BRSP reported adjusted distributable earnings of $0.27 per share and paid a $0.20 dividend for a dividend payout ratio of 74%.

In 2020, BRSP cut its dividend by 81.82%, from $1.65 to $0.30 per share, but then increased the dividend for the next two years. In 2021, BRSP increased their dividend by 93.33%, and in 2022 they increased it by 36.21%.

Currently, BRSP pays a 12.0% dividend yield and trades at a P/E ratio of 7.01x, which is a significant discount to their normal P/E ratio of 12.55x.

At iREIT®, we rate BrightSpire stock a BUY and assign it a tier 1 rating.

{kind=link}

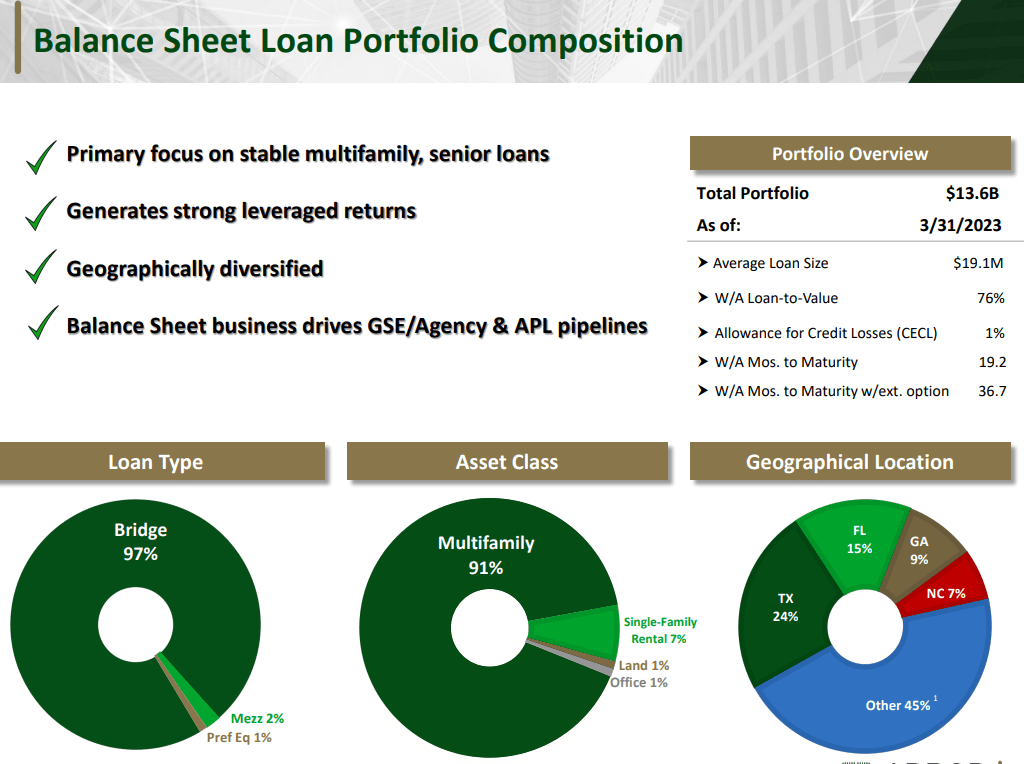

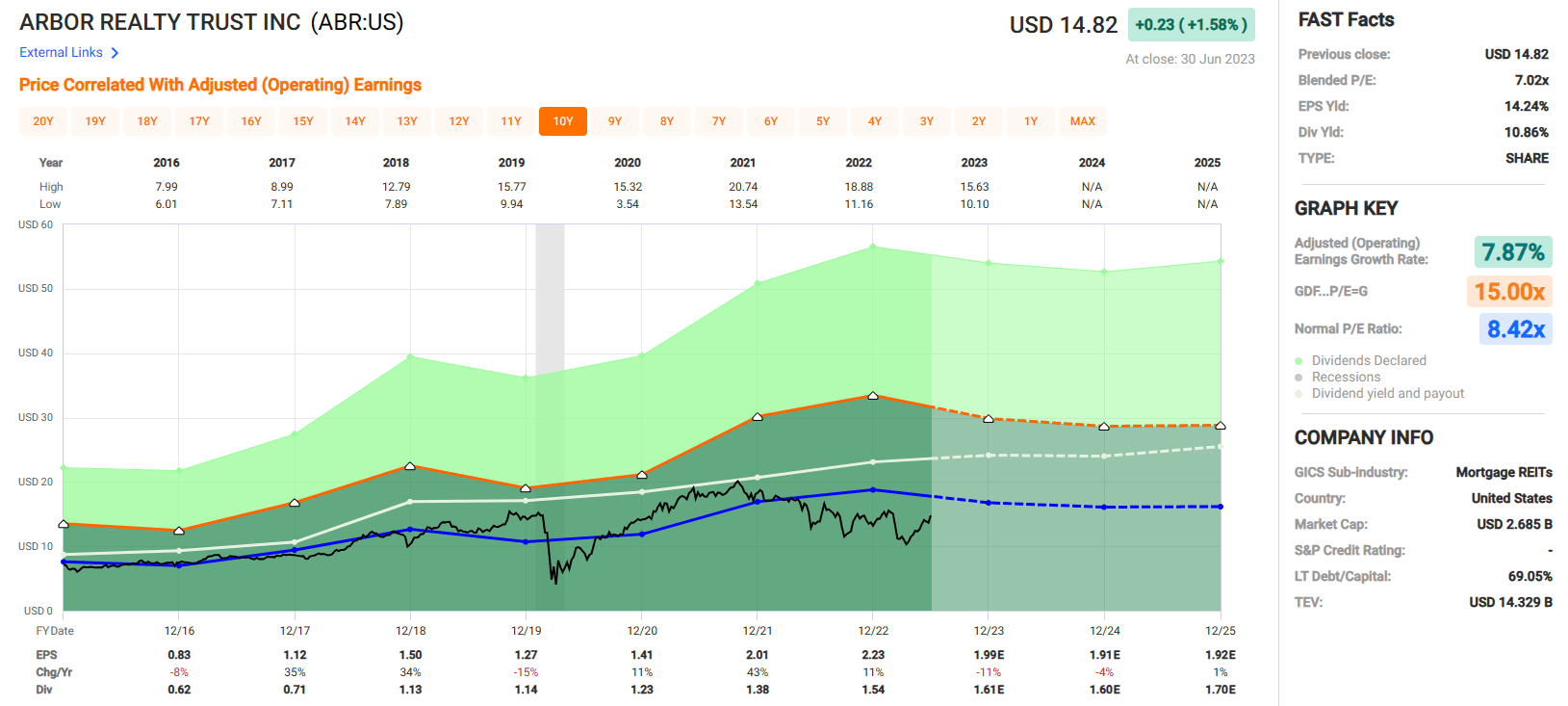

ABR: Yielding 11.3%

Arbor Realty Trust, Inc. ( ABR ) is an internally managed multifamily-focused mREIT that originates loans through their Structured Business and Agency Business. Through their Structured Business they invest in a portfolio of structured finance assets that primarily consist of bridge loans, but also includes mezzanine loans and preferred equity.

Through their Agency Business, ABR originates, sells, and services multifamily finance products through government-sponsored enterprises (“GSEs”) such as Fannie Mae and Freddie Mac and also sells loans through the conduit markets.

Additionally, through their Agency Business, Arbor Realty originates private label loans which are then pooled and securitized into CMBS and sold to third-parties.

While ABR securitizes and sells many of their loans, they retain the servicing rights on almost all of the loans they originate through their Agency Business. Arbor Realty has a $13.6 billion balance sheet loan portfolio with an average loan size of $19.1 million and a weighted average LTV of 76%.

{kind=link}

ABR reported distributable earnings of $0.62 per share in the first quarter of 2023, which is $0.20 more than their first quarter dividend for a payout ratio of approximately 68%.

ABR has delivered 11 consecutive years of dividend growth and has increased the dividend in 11 out of the last 13 quarters.

Since 2016, ABR has had an average adjusted operating earnings growth rate of 7.87% and an average dividend growth rate of 16.16%. Currently they pay a 11.3% dividend yield and are trading at a P/E of 7.02x, which is a discount to their normal P/E ratio of 8.42x.

At iREIT®, we rate Arbor Realty Trust stock a Spec BUY and assign it a tier 2 rating.

{kind=link}

The Anchor & Buoy Approach

As I mentioned earlier, I like owning commercial mREITs because it’s a terrific way to gain access to commercial real estate debt that generates income and attractive total returns (unlike preferreds that don’t benefit from price appreciation).

Given where we are in this cycle, that includes a wave of debt maturities, these mREITs are perfectly positioned to capitalize on refinancing landlords (more demand) who are in need of bridge funding.

Given the fact that mREITs aren’t under the same scrutiny as banks, these skilled mREITs will be able to capture market share and generate attractive risk-adjusted returns.

Market Capitalization (in millions)

iREIT®

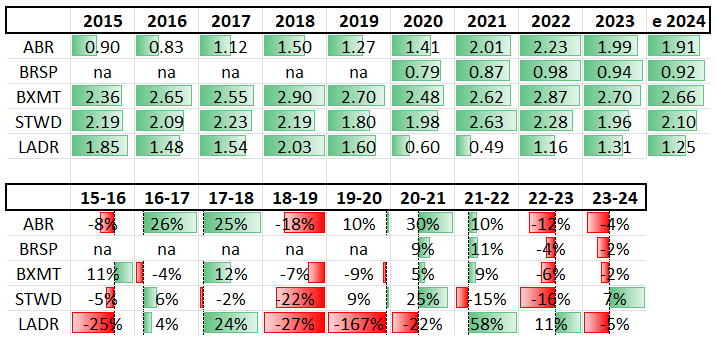

Historical and Forecasted (2024) EPS

{kind=link}

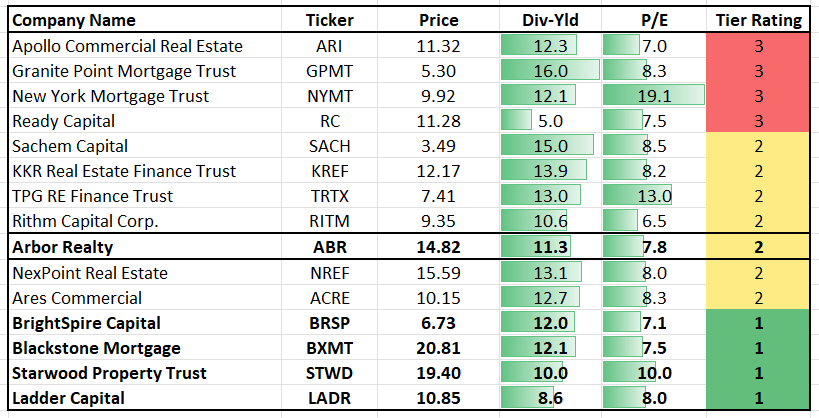

Commercial mREIT Coverage Spectrum

{kind=link}

As always, thank you for reading, and I look forward to your comments below.

For further details see:

Who's Scooping Up These High-Yielding Mortgage REITs?