FREE - Whole Earth Brands: Due For A Price Rise

2023-04-19 17:11:21 ET

Summary

- Sweetener manufacturer Whole Earth Brands' share price is trading near all-time lows, which does not appear commensurate with its fundamentals, even considering its present challenges.

- In the next quarters, revenues can continue inching up and it can swing back into profits too. Over the longer term, it can gain from the growing sugar substitute market.

- Just to be doubly sure though, I'm maintaining the Hold rating until its next results in May.

My first article about the sweetener manufacturer Whole Earth Brands (FREE) in October last year was titled "Whole Earth Brands: The Messy Middle". This alluded to the situation it continues to find itself in. Before it made acquisitions from 2020 onwards, the company was doing fine and going by the potential of the sugar substitutes market, it can do so in the future as well. But right now, it is adjusting to the impact of acquisitions on its business. If we add high inflation from last year, rising interest rates and a recessionary environment to the mix, there truly can be a glorious mess on its hands.

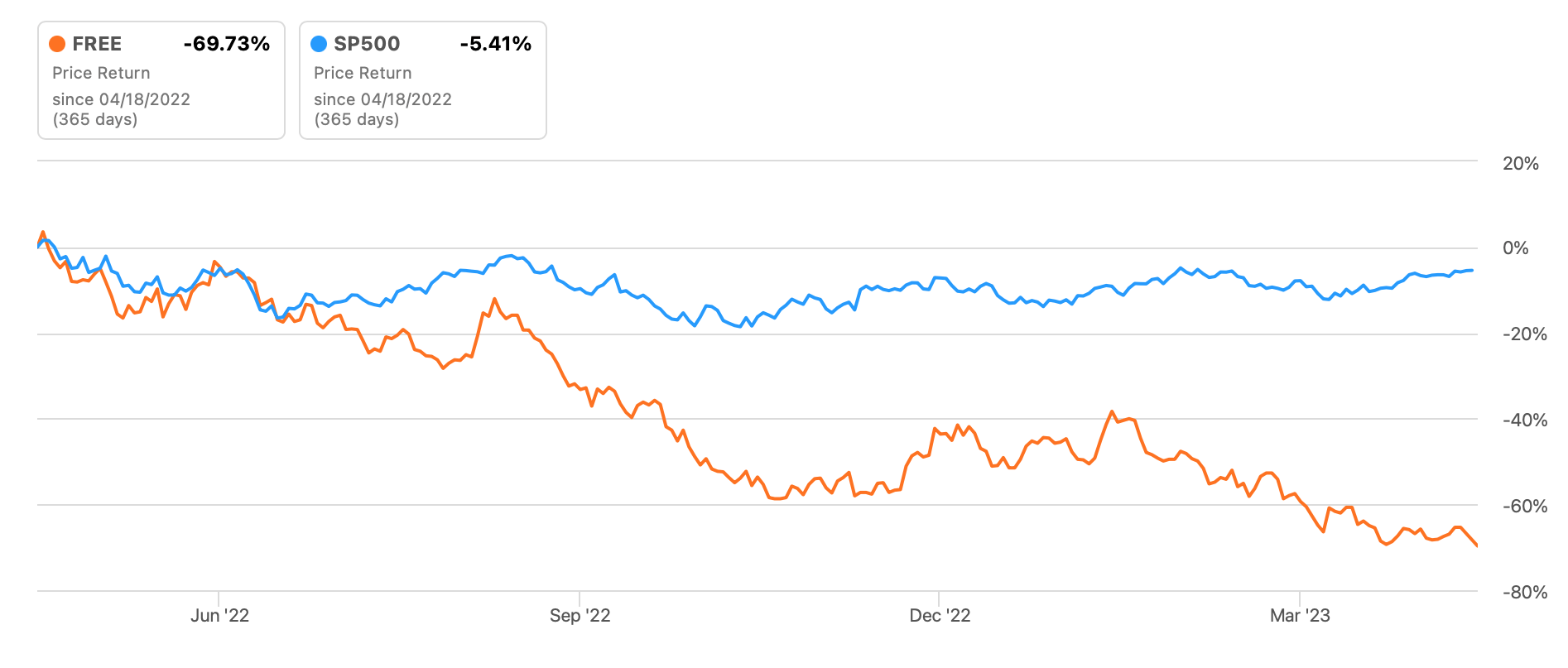

Investors are rightly cautious about it. The stock has fallen by 45% year-to-date and by 70% over the past year. But here is the rub. It is now trading at near all-time lows. Admittedly, it has a short trading history, since just 2020, but even then the extent of price decline is hard to miss.

{kind=link}

Quick recap

Some correction was due even in January this year when I next wrote about it . This was because the price had run ahead of what the fundamentals indicated. To do a quick recap, growth was expected to soften, though largely because of the high base effect from acquisitions. Margins were weakening, operating income had halved and the company had reported a net loss in the third quarter of 2022 (Q3 2022). But, the price instead of falling, had strengthened, leading to a clearly unsustainable 157x price-to-earnings (P/E) ratio.

It was obvious that the only way was down for the stock. And no sooner than the markets got a bit hesitant that it started falling. Adding fuel to the fire were its final quarter and full year 2022 results , which will be discussed in some detail here. Based on these, the outlook for 2023, and the present market multiples, I figure out here if the stock might just have overcorrected now.

Slowing growth, operating loss

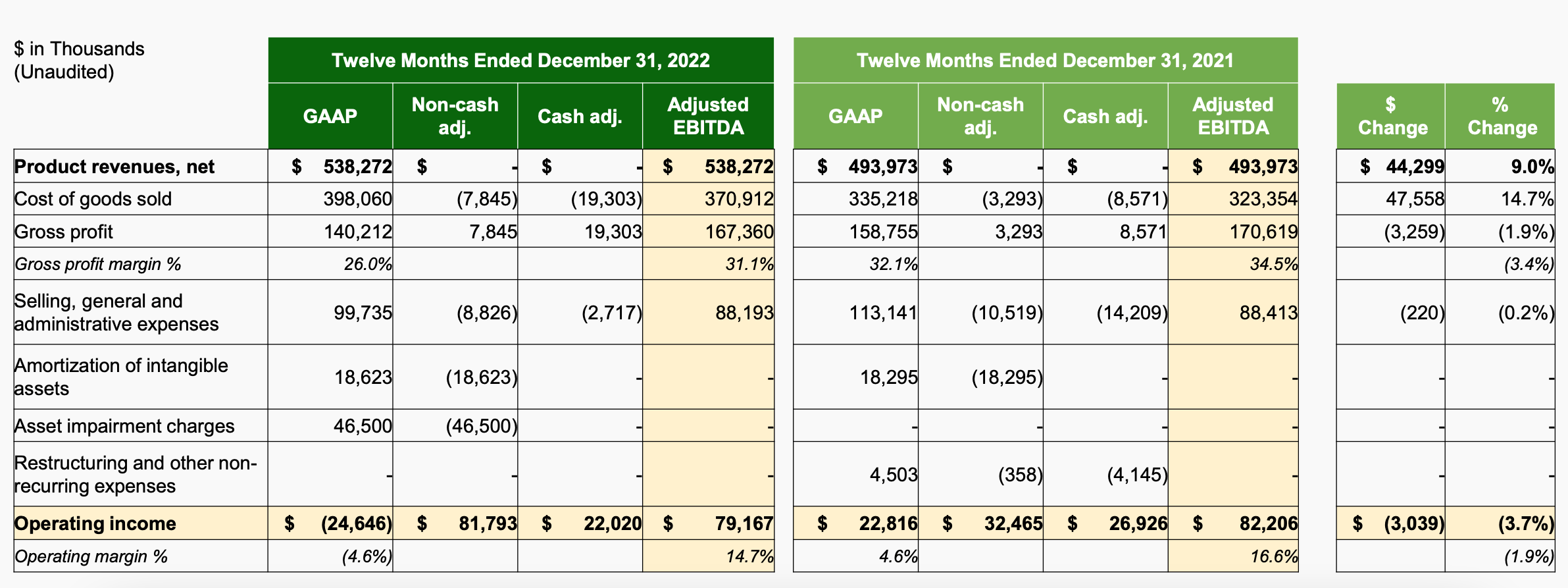

After rising by 10.6% in the first nine months of 2022 (9M 2022), revenue growth was slated to slow down. And that has happened. Full-year 2022 growth came in at 9%, in line with the company's projection of an 8-10% increase. The high base effect from acquisitions continued to play a part in slowing the pace of its increase in the second half of 2022. Growth in Q4 2022 slowed down to 4.7% year-on-year (YoY), from the already muted 4.9% in Q3. A strong dollar was also detrimental to revenue rise at market exchange rates. At constant currency, FREE's revenues grew by a faster 11.6%.

The silver lining here though is that the decline is not down only to a genuine demand slowdown. Even then, however, the company's challenges are visible. Whole Earth Brands' earnings have disappointed as well, with gross profit margin down to 26% in 2022 from 32.1% in 2021, on account of cost inflation as well as its supply chain reinvention projects and impairment charges. It has also fallen into an operating loss and reported a net loss.

Key Financials (Source: Whole Earth Brands)

{kind=link}

Liquidity and debt look alright

In the past, I expressed concern about its interest coverage ratio, in an environment of rising interest rates and the company's own growing debt. And indeed, FREE's interest expense rose by over 24% during the year to USD 30.6 million, along with a rise in its debt by 9.5%. With no operating income to speak of the interest coverage ratio does not apply anymore.

Though I am somewhat comforted by its liquidity position. Its current ratio of 3.7x is very healthy, as is its quick ratio of 1.2x. At 0.4x, its cash ratio is less than ideal, but then it is a more conservative measure of liquidity. And finally, its debt ratio at 0.5x is not too bad either, especially considering the increase in debt levels this year.

Further, its operating loss is down to an impairment charge of USD 46.5 million in Q4 2022. Until 9M 2022, it was profitable at the operating level. Assuming that this charge is a one-off, the company can well be back in profits when it reports its first-quarter results in May. And that means interest coverage going forward.

Muted outlook

However, in total I would not get my hopes up too much, going by its forecasts for 2023. The company expects revenue growth of 2-5%, which is slower than that seen in 2022. It also expects a decline in adjusted EBITDA to USD $76-$78 million from USD 79 million in 2022. FREE does say "The outlook is provided in the context of greater than usual volatility as a result of current geo-political events, the ongoing COVID-19 pandemic, the current inflationary environment and foreign currency exchange rate fluctuations.".

In other words, it acknowledges the challenges that haunted the consumer market in 2022. I do believe that recessionary conditions can impact demand as well, though a less strong dollar and a come-off in inflation can all serve to balance it out. Also, a lower adjusted EBITDA might not be the biggest consideration, if it starts clocking profits again. But that remains to be seen, based on how all the influencing factors play out over the rest of the year.

What the market multiples say

So in sum, we have a company whose performance was affected in 2022 and is not looking at a particularly positive 2023 either. At the same time, the market multiples suggest that its price has overcorrected. Its price-to-sales (P/S) is at a minuscule 0.2x compared to 1.2x for the consumer staples sector. Even if we consider the enterprise value-to-EBITDA (EV/EBITDA) because of its growing debt, the ratio is 12.3x compared to 13.6x for the sector. In fact, the difference is even sharper if we consider the forward EV/EBITDA figure, which is at 7x compared to 12.3x for consumer staples.

What next?

Based on the multiples it would appear that the stock can rise from here. Already at near multi-year-lows, there is really no basis for it to decline further. Sure, its revenue growth can be slow in 2023, but at the same time, it is not as if it is seeing declining revenues. Moreover, it can become profitable again. Its liquidity and debt position look fine too. And I have not even touched upon the potential of the sweetener market yet.

Obesity is an increasing global problem, as are other sugar-related health conditions. There is much potential for the sugar substitute market to grow, therefore. Whole Earth Brands has a market leadership position in multiple markets, which bodes well for it. Its present challenges are real, but they are not commensurate with the extent of the price decline. Just to be doubly sure, I would wait until its first-quarter results next month. I will maintain my Hold rating until then.

For further details see:

Whole Earth Brands: Due For A Price Rise