FREE - Whole Earth Brands: Trading Below Initial Acquisition Offer Price (Rating Upgrade)

2023-10-02 22:45:38 ET

Summary

- Whole Earth Brands' share price has fallen below the acquisition offer price it received from Sababa Holdings.

- Despite the company reporting weak results for H1 2023 and the likelihood that 2023 can be a sluggish year, there's still an upside to the initial price offer.

- Its profit situation is expected to improve next year, in fact, its operating profits already look better and its market multiples are competitive too. So it's one to consider anyway.

Since I last wrote about the sweetener manufacturer Whole Earth Brands ( FREE ) in July this year, its share price is down by 10%. This is a curious phenomenon, considering that it has now fallen below USD 4 to USD 3.6, the acquisition offer price it received from Sababa Holdings.

{kind=link}

There have been no further developments on the potential deal since, except for the release of its second quarter (Q2 2023) results. With it still being a potential buyout candidate, the question then is, are the results poor enough to justify the fall in price or has the price fallen below fair valuation?

Weak results

Whole Earth Brands undoubtedly reported poor results for the first half of the year (H1 2023), with revenue increasing at just 0.5% year-on-year (YoY). This is partly due to a base effect, with 13.7% growth in H1 2022 as revenues for the sweetener Wholesome were added during the quarter after its acquisition in 2021. As a result Q1 2023 growth was a muted 1.4%.

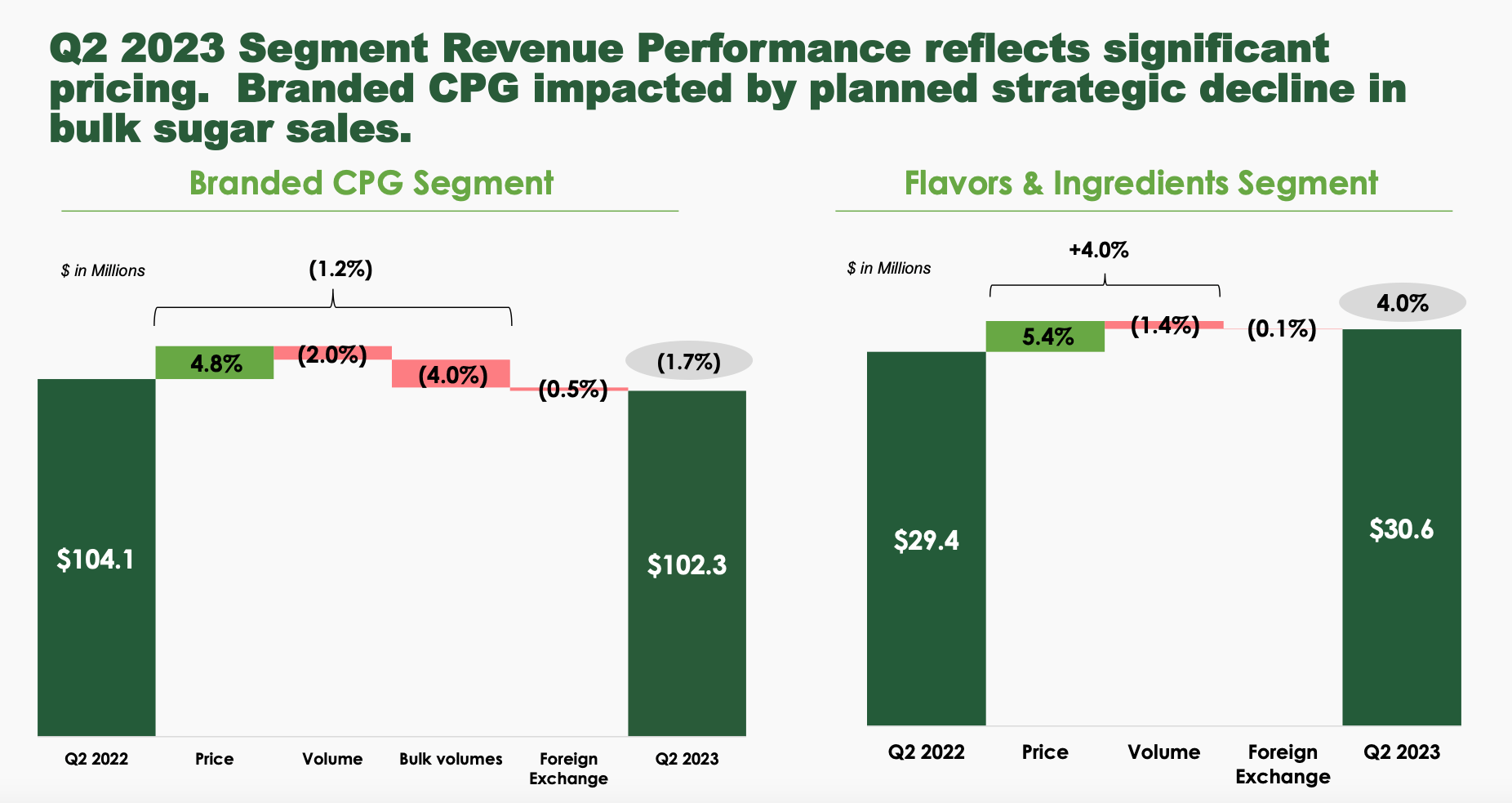

Further, in Q2 2023, a strategic decision to reduce bulk sales of Wholesome sugar, resulting in a 0.5% decline in the quarter’s revenues (see chart below). If it weren’t for this, the constant currency revenue for the CPG segment, of which it is part, would have risen by 2.8% instead of declining by 1.2%.

{kind=link}

Revenue projections at risk

Despite the weak figures, the company maintains revenue growth projections of 2-5%. I believe, however, that there are now risks that it won’t be able to meet its targets, though. Here’s why.

First, in H1 2023, the sales figures are already lower than targeted. However, if the drop in bulk revenues is added back, H1 2023 revenues now rise by 2.6%, which is in the target range for the full year.

But there are two points to consider here. One, we don’t know if the company will or won’t continue with the bulk sales management in the next quarters. If it does, we can well expect a revenue softening in the coming quarters as well. Also, Whole Earth Brands reported weak Q2 2023 sales despite the fact that the high base effect of Q1 2023 had actually worn off in the quarter.

Even if the company is able to show the same absolute revenue increase it did in Q1 2023 instead of the decline in Q2 2023 for the rest of the year, it will report a full-year growth of 0.9%. However, if the remainder quarters grow by where Q2 2023 would have been with bulk sales added back, the full-year growth be 3.2%. On average we should just about expect 2% growth.

Adjusted EBITDA margins

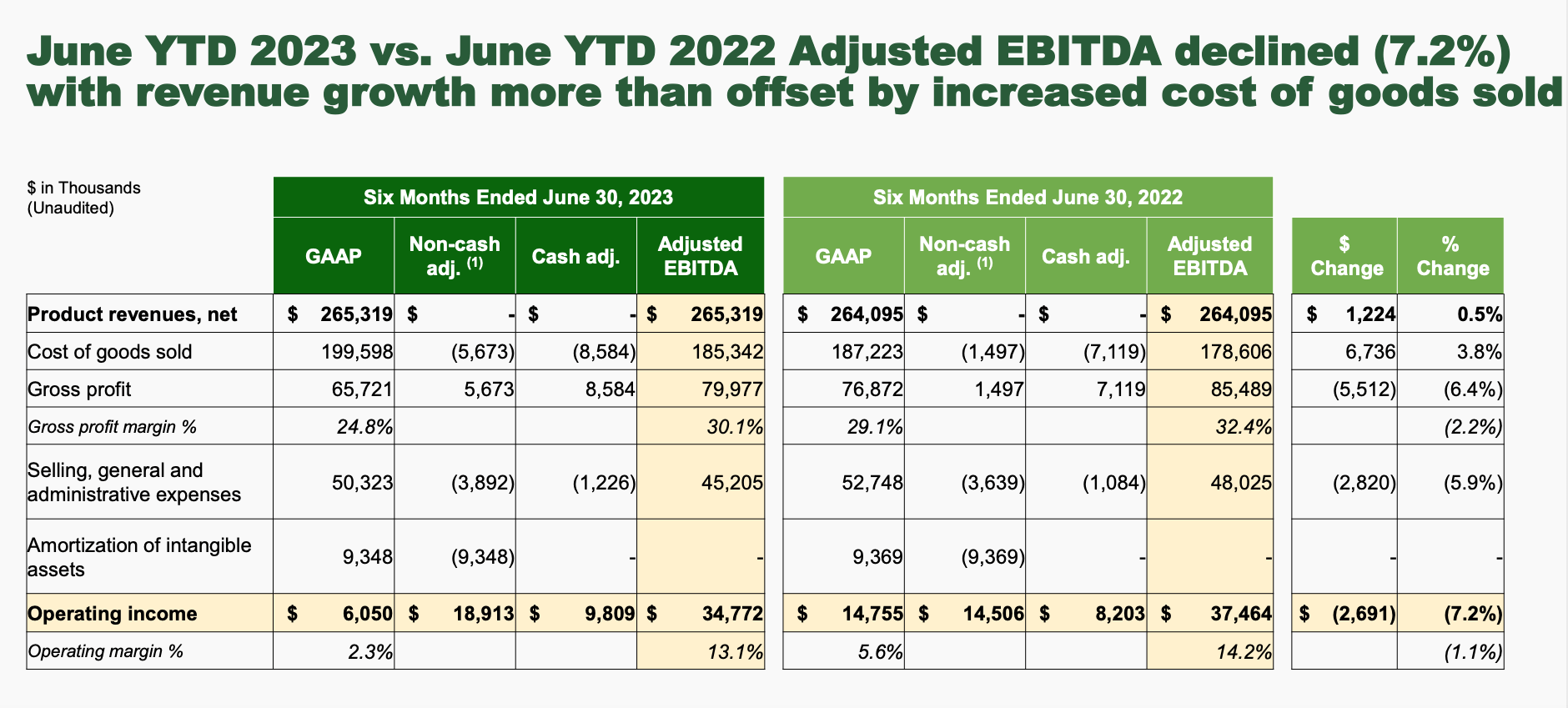

Next, let’s look at its adjusted EBITDA (A-EBITDA) figures. These came in at USD 34.8 million in H1 2023, a 7.2% decline from last year. The corresponding margin declined by over a percentage point to 13.1% (H1 2022: 14.2%).

{kind=link}

The company expects the full-year number to come in the range of USD 76-78 million. At the current rate, it appears that the company might fall behind on its A-EBITDA projections as well. In this case, however, there is a chance that it might just make the target, considering that it mentions severance expenses and cost inflation have eaten into profits.

Assuming the severance costs were a one-time expense and considering that cost inflation is expected to come off even more over the next months, profits could inch up.

Impact on FREE’s valuations

The key question, though is, what do the projections mean for FREE’s market multiples, especially keeping in mind that they could affect its valuations. When I last checked, the enterprise valuation was at USD 594 million. My own valuation, based on 2023 revenue growth expectations of 2% puts it at USD 549 million now, which is actually lesser.

As per forward revenues

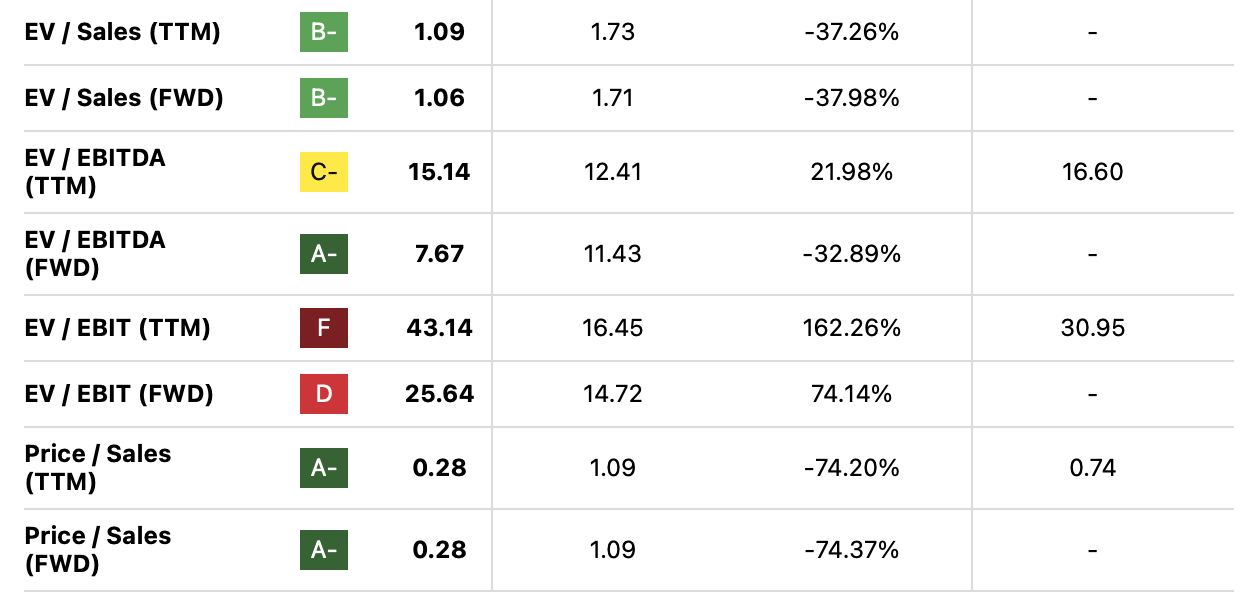

However, with the forward EV/Sales having risen for the consumer staples sector from 1.64x at the time I last checked to 1.71x now, the potential fair valuation for FREE’s share price is now at USD 12.7 compared to the USD 12 earlier. In other words, despite its weak performance, there’s actually an upward push to its valuation from this perspective.

{kind=link}

As per forward EBITDA

Next, let’s look at it from the EV/EBITDA perspective. Assuming that it comes in at the midpoint of the expected range of USD 76-78 million, the forward EV is at a higher USD 591 million. However, in this case, the forward EV/EBITDA for the consumer staples sector has actually declined from 11.9x earlier to 11.4x right now. It still implies an increase in valuation for FREE, but the share price indicated is smaller at USD 10.3.

Of course, there are arguments at the other end as well. The company’s not growing, and even if growth does happen, it will be slower than that for the consumer staples sector and its EBITDA growth is slower too .

But the fact remains that even now the company’s valuations indicate that the acquisition price can actually be much higher than the USD 4 on the table first offered, even if not as high as indicated with a comparison with the sector.

What next?

Based on the latest valuations and the fact that FREE is now trading below the offer price, it actually looks like a speculative buy. There’s only one risk, of the deal falling through, which means that investors can get stuck with an underperforming stock.

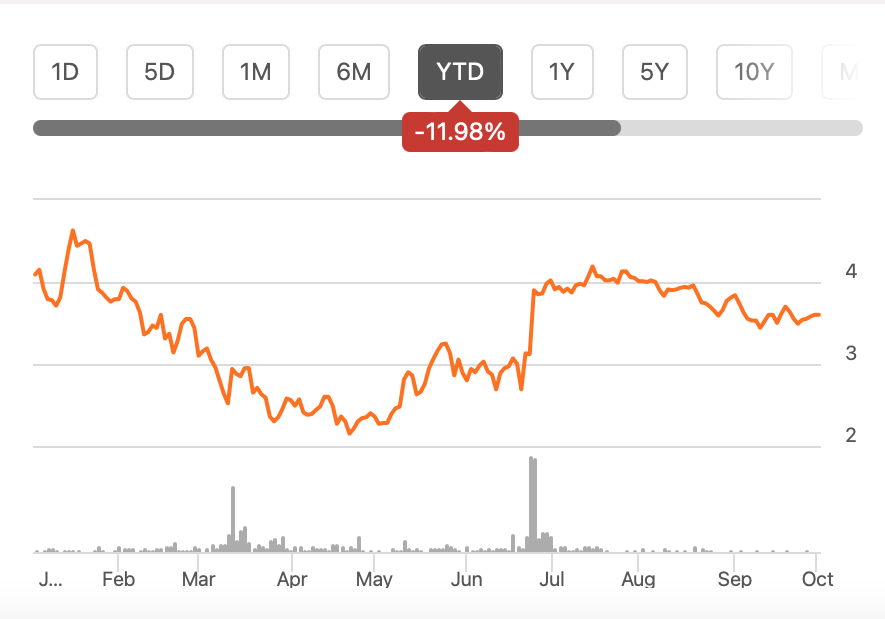

But I would like to point out that with a forward price-to-sales ratio of 0.28x, way below the 1.09x for the consumer staples sector, there’s still a case for some price rise. Especially since it has now reported operating profits for the past two quarters, and analysts expect it to turn EPS positive in 2024 as well. In the meantime, its price is down by 12% year-to-date.

I’m upgrading FREE to a Buy, largely based on the likelihood of it being sold at a higher price, but also because I see a lesser downside to it in the medium term even if it doesn’t.

For further details see:

Whole Earth Brands: Trading Below Initial Acquisition Offer Price (Rating Upgrade)