BIZD - Why Ares Capital Is Likely To Underperform The BDC Sector

2023-12-26 23:38:26 ET

Summary

- I missed 1.48% of alpha creation in my last article on Ares Capital when I had downgraded it to a hold. Yet, I still downgrade ARCC to a 'Strong Sell':

- The chances of a rate reduction by the Federal Reserve are increasing, which could benefit the BDC sector, particularly BDCs with greater cyclical exposure.

- Ares Capital is not well-positioned to benefit from easing rates due to its defensive orientation and predominantly floating investment yields.

- The relative performance outlook of ARCC vs the BDC sector via the VanEck BDC Income ETF confirms the fundamental view.

- Overall, I have a strong relative bearish view on ARCC vs BIZD primarily and also the S&P 500. This is not a strong bearish view of the absolute return prospects of ARCC.

Thesis Review

In my last article on Ares Capital ( ARCC ), I proposed a 'Neutral/Hold' rating for the stock due to a host of headwinds that were emerging at that time. Now, I am changing my stance to a 'Strong Sell' as I believe the relative bear case is more compelling. To be clear, this bearish view is on Ares Capital's alpha generation potential vs the S&P 500 ( SPY ) ( SPX ) and also the broader BDC sector that may be represented by the VanEck BDC Income ETF ( BIZD ). This is not necessarily a bearish view of the absolute return potential of Ares Capital.

Before getting into the new thesis, as always I review my performance since the last article; Since July 31, 2023, Ares Capital has generated a total shareholder return of +5.84% vs the S&P 500's +4.38%. This translates to an alpha creation of +1.46%. Therefore it seems my earlier downgrade from a ' buy ' to a 'neutral/hold' was too early.

Here is why I am still bearish on Ares Capital now:

- The chances of an easing in the rates are increasing

- Ares Capital is not the best beneficiary of easing rates

- Relative performance outlook of ARCC vs the BDC sector confirms the fundamental view

The chances of an easing in the rates are increasing

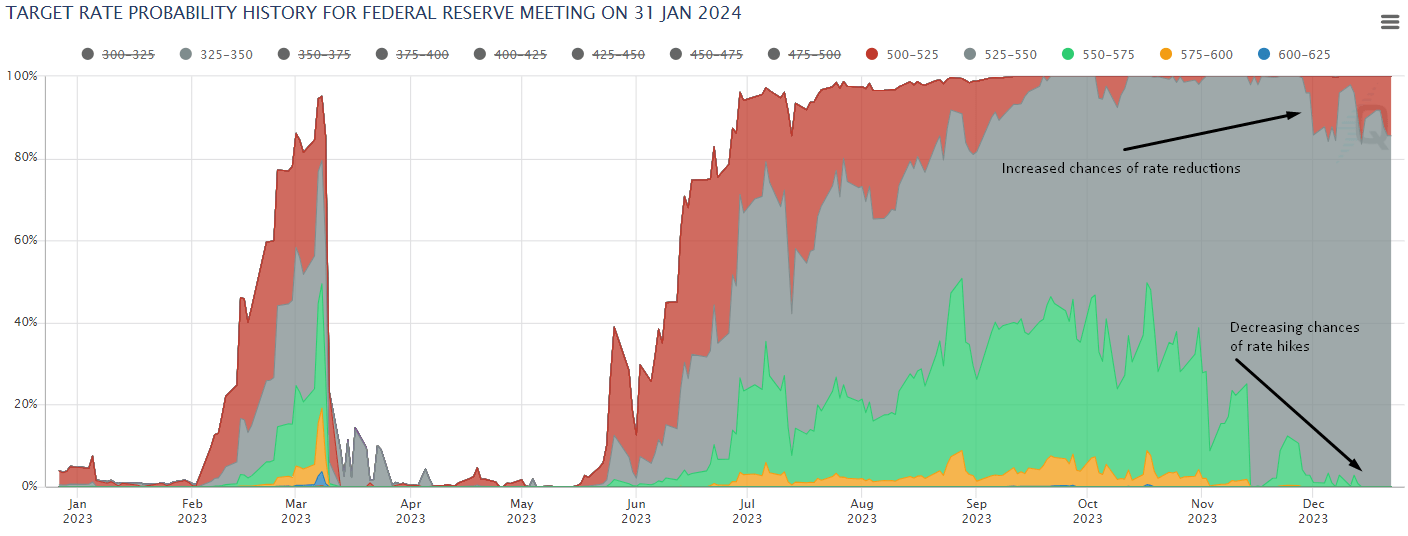

Federal Reserve Target Rate Probabilities (CME FedWatch Tool)

{kind=link}

As can be seen in this annotated graphic of the CME FedWatch Tool's target rate probabilities, the chances of a rate reduction to the 500-525bps level have increased in December 2023 to stand at a modest 14.47% from virtually 0% in the months prior. This increased likelihood of a dovish view on rates has come at the expense of a reduced likelihood of a rate hike; the chances of a 550-575bps rate level has reduced to 0%. This is a dramatic fall from 40%+ levels in October 2023.

A fall in rates is a sectoral tailwind as this reduces the pressure on portfolio companies and triggers waves of new borrowing and hence new investment opportunities. Indeed, this is what Fitch Ratings' industry research suggests as well:

[BDC] deal activity is expected to improve in 2024, and several BDC managers have pointed to improving pipelines...

The benefit of rate reductions is most felt by companies in cyclical industries, benefiting the BDCs with greater exposure to more volatile sectors.

Ares Capital is not the best beneficiary of easing rates

The company's management team has often described Ares Capital as a defensively-oriented BDC:

And when you think about our portfolio, which I think is more defensively positioned and as we always mentioned, less oriented towards cyclical companies...

- CEO Robert DeVeer in the Q3 FY23 earnings call

Q3 FY23's data provides numbers to support this narrative; 51% of Ares Capital's $820 million backlog and pipeline is comprised of the Consumer Services, Consumer Staples, Distribution & Retail sectors - all defensive, less-cyclical categories.

Moreover, the majority (69%) of Ares Capital's investment mix is on floating rate terms:

Floating Rate Investment Mix (Company Filings, Author's Analysis)

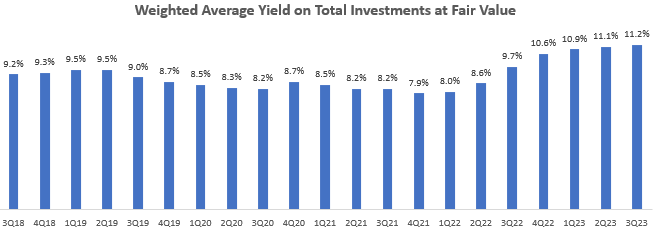

I anticipate this to lead to a drag on investment yields from the current levels of 11.2%:

Weighted Average Yield on Total Investments at Fair Value (Company Filings, Author's Analysis)

{kind=link}

So far in 2023, Ares Capital's net investment income margins have been held back by low investment activity and deal flow but offset by higher rates. In 2024, I believe these drivers will switch around; investment activity is expected to rebound but lower yields may hinder a material rebound in net investment income margins:

Net Investment Income Margin (Company Filings, Author's Analysis)

Relative performance outlook vs the BDC sector confirms the fundamental view

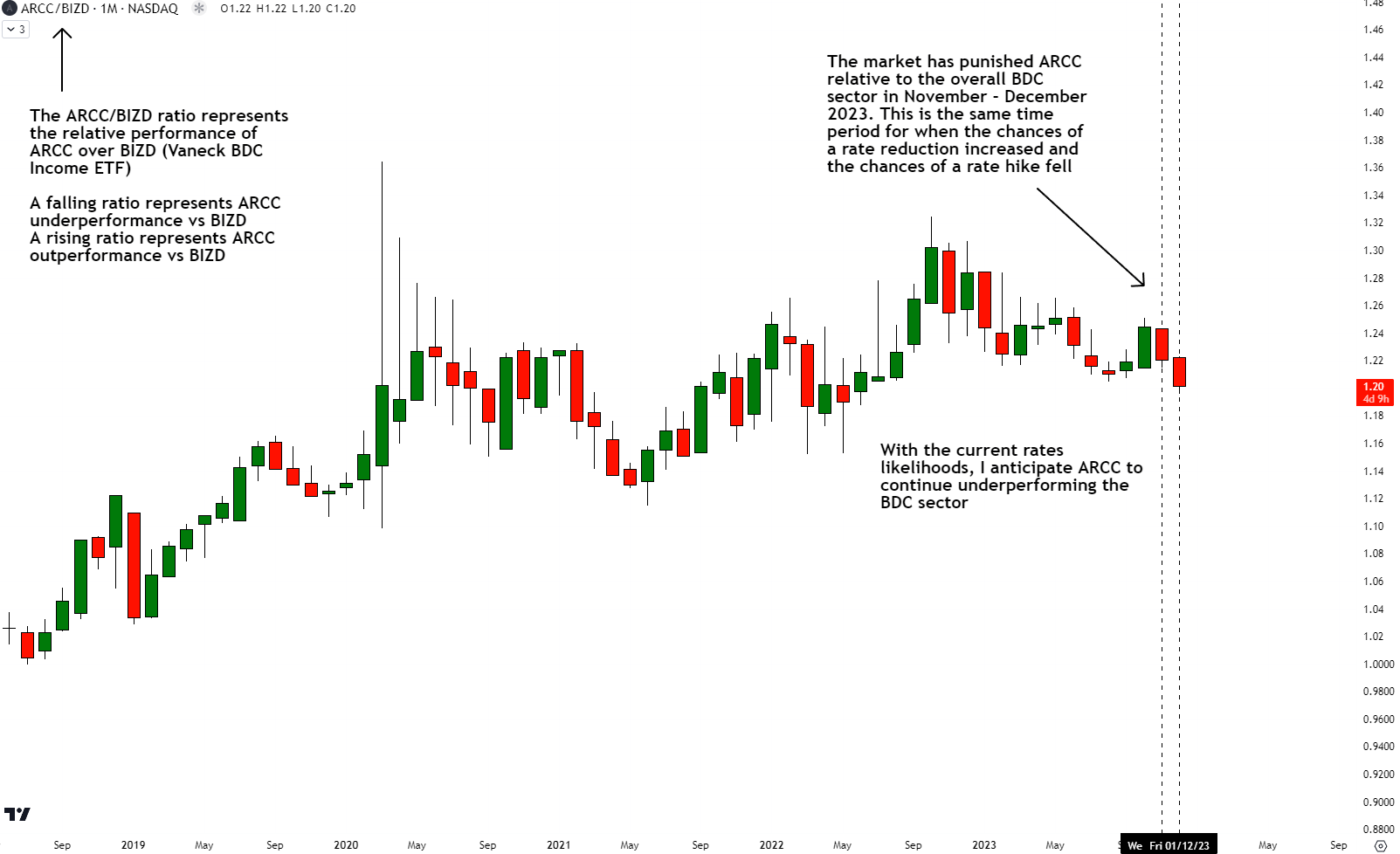

A look at the relative ratio of ARCC/BIZD reveals to us the performance of ARCC vs the Vaneck BDC Income ETF:

Relative Performance of ARCC vs BIZD (TradingView, Author's Analysis)

{kind=link}

I note that ARCC has underperformed the BDC sector in November and December 2023; precisely when the chances of the Fed's target rate reduction increased at the expense of the chances of a rate hike. Thus, market sentiment seems to be responding in line with the fundamental thesis that is based on the implications of the current target rate probabilities. This gives me confidence that we have identified the critical stock driver.

I anticipate ARCC to continue underperforming the BDC sector so long as the chances of easing rates do not deteriorate.

Key Risk and Monitorable

My relative underperformance thesis on Ares Capital is highly dependent on the market's Fed's target rate probabilities. The performance of the BDC also seems to be responding in line with this driver. Hence, this is a key monitorable.

On the company side of things, Ares Capital can improve its positioning in an easing rates environment if it increases the mix of cyclical companies in its portfolios or if it manages to lock in higher rates for its investments. Although I believe this is unlikely to happen as it would be contrary to Ares Capital's DNA, I keep tabs on all these key metrics disclosed by the company to identify thesis-relevant changes in a timely way.

Takeaway

The BDC sector is set for an activity rebound, driven by the increased likelihood of a target rate reduction by the Federal Reserve. This bodes particularly well for BDCs with more volatile and cyclical portfolios as the financing pressure is eased most for these investee companies.

Ares Capital, however, is a defensively oriented BDC with minimal cyclical exposure in its portfolio and predominantly floating investment yields. This highlights a disadvantage to Ares Capital relative to other BDCs.

The relative performance outlook of Ares Capital against the broader BDC sector as represented by the Vaneck BDC Income ETF supports the fundamental view.

Hence, I rate Ares Capital a 'Strong Sell' as I believe it is very likely to underperform the broader BDC sector - which is the more confident view - and also the S&P 500. I wish to emphasize that this view is based on my outlook for relative performance (i.e. alpha). I do not have a similarly strong bearish view on the absolute performance prospects of ARCC.

I also understand that this is quite a controversial view as Ares Capital is ardently held by many income-seeking investors. However, I am comfortable being the contrarian here as I have gained confidence in my ability to go against the herd when the situation demands it, as evidenced by successful 'Strong Sell' outlooks on British American Tobacco ( BTI ) ( BTAFF ) and Cronos Group ( CRON ).

How to interpret Hunting Alpha's ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher-than-usual confidence

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in line with the S&P 500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis, with higher-than-usual confidence

For further details see:

Why Ares Capital Is Likely To Underperform The BDC Sector