AZUL - Why Azul Stock Is Flying Higher

2023-03-06 22:18:00 ET

Summary

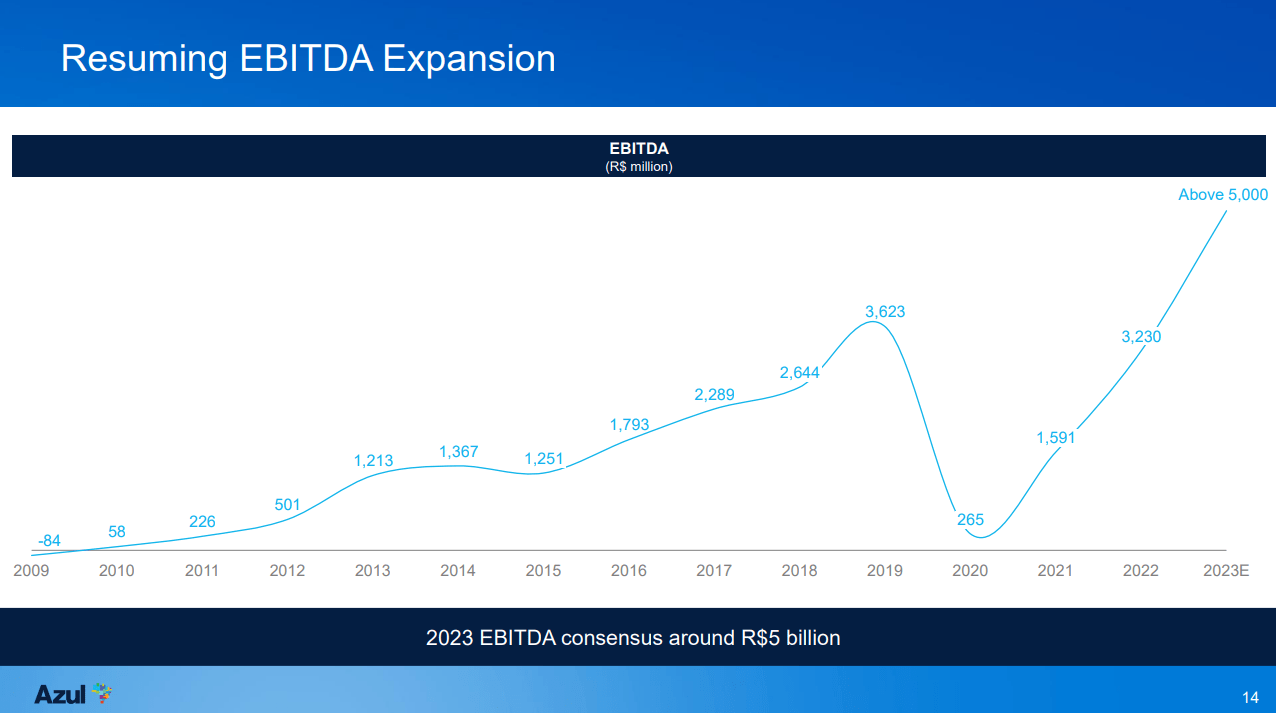

- Azul remains bullish on the future with >55% EBITDA growth targeted for 2023.

- Agreement on lease restructuring was a must for Azul, not a luxury as the company turns its business around and aims to improve its capital structure.

- Azul strategy and focus are impressive, its stock performance not so much.

- Despite the strong forecast and significant deleveraging, I won't upgrade Azul stock.

In a previous report , I discussed the third quarter results for Azul (NYSE: AZUL ) and while I do like how management is transforming the business, its bad luck has been that it's active on the Brazilian market that suffered some challenges as the Brazilian Real came under pressure.

Azul Stock Loses in Sell-Off

Seeking Alpha

The way management approaches the business and aligned it for a post-pandemic world is impressive. However, even after today’s 40% surge the stock is still trading 17.4% lower compared to the last time I covered Azul. So, all with all great company but the stock performance is not so great and that is the way it has been for a while now.

Azul Reports Strong EBITDA for 2022

{kind=link}

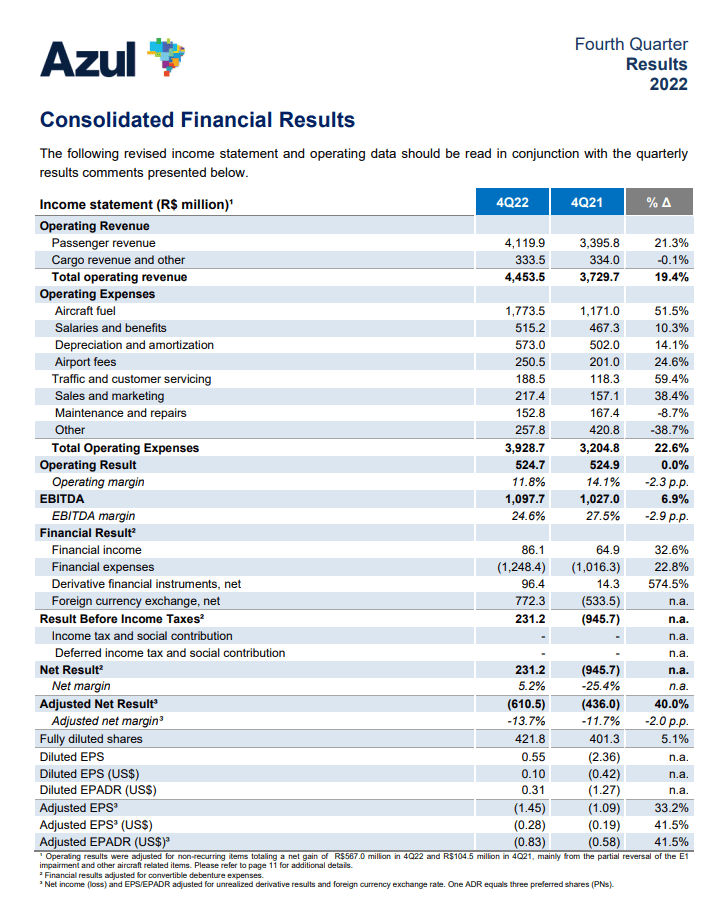

During the fourth quarter, we saw revenue increase by 19.4%. This was driven by 10% higher revenues and 10% higher capacity offset by lower cargo revenues. Costs, however, rose more than the 9% higher number in departures and 10% higher capacity. Obviously, the 51.5% higher fuel costs played a significant role but we also saw airport fees increasing by a combination of higher block hours, more international routing and inflation.

So, overall we see higher international costs feathering into the cost picture as well as higher departure numbers. The company also had a tailwind from foreign currency exchange. Its adjusted results, however, were worse than last year driven by higher oil prices, inflation and volume costs and the adjustment of a fleet impairment reversal.

{kind=link}

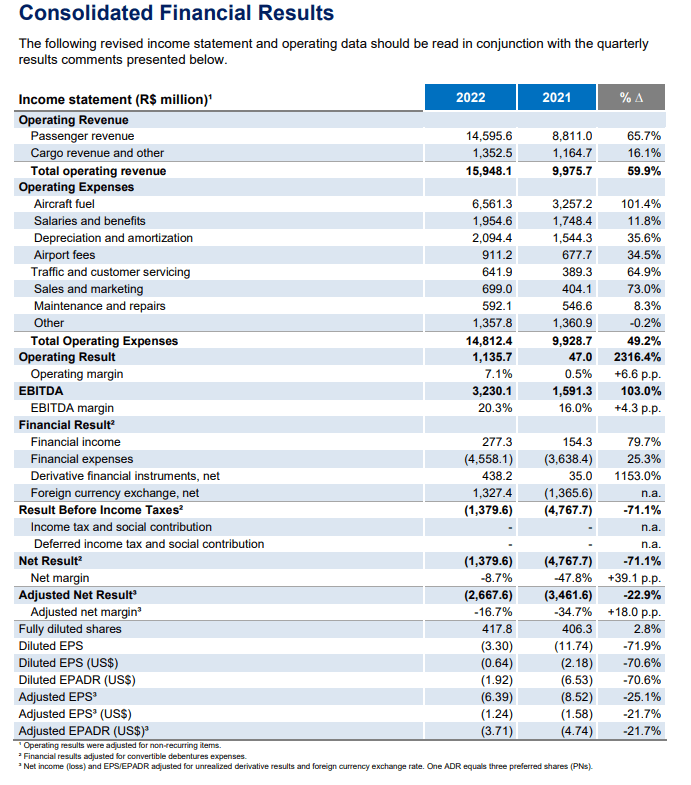

Year-over-year revenues grew by 60%, which was 26%, driven by higher capacity and 40% higher fares. Aircraft fuel cost unsurprisingly doubled due to higher fuel consumption and higher fuel prices. The positive is that despite inflation, we saw top line growth in excess of growth in operating expenses resulting in EBITDA margin expansion. Maybe somewhat off putting is that a significant portion of improvement in year-over-year EBIT was driven by forex results. However, the net results were significantly better as are the adjusted net results.

Azul Posts Significant Deleveraging

{kind=link}

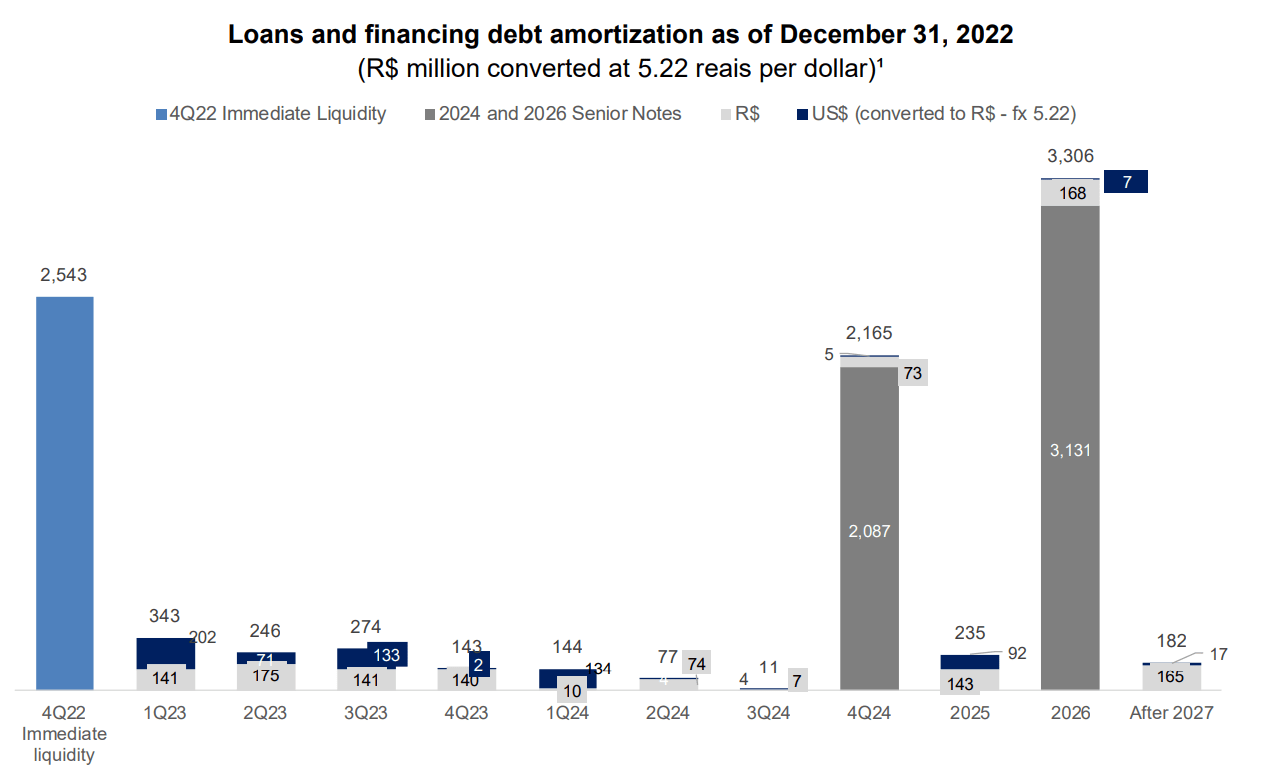

Azul posted significant year-over-year improvement in net debt to EBITDA. The cash pile decline by 35.6% to 3,381 million Brazilian Real and its gross debt decreased 5.3%. Overall, its net debt increased by 3.7% to 18,434.1 million Brazilian Real. However, EBITDA more or less doubled year-over-year leading to the net debt to EBITDA dropping from 11.2x to 5.7x.

Immediate liquidity by the end of the quarter stood at 2,543 Brazilian Real which consists of cash and equivalents and receivables. With that, the Brazilian airline can cover its debt requirements through Q3 2024 two times. After that in Q4 2024 and the entirety of 2026 we see higher debt repayments.

Why Did Azul Stock Surge?

{kind=link}

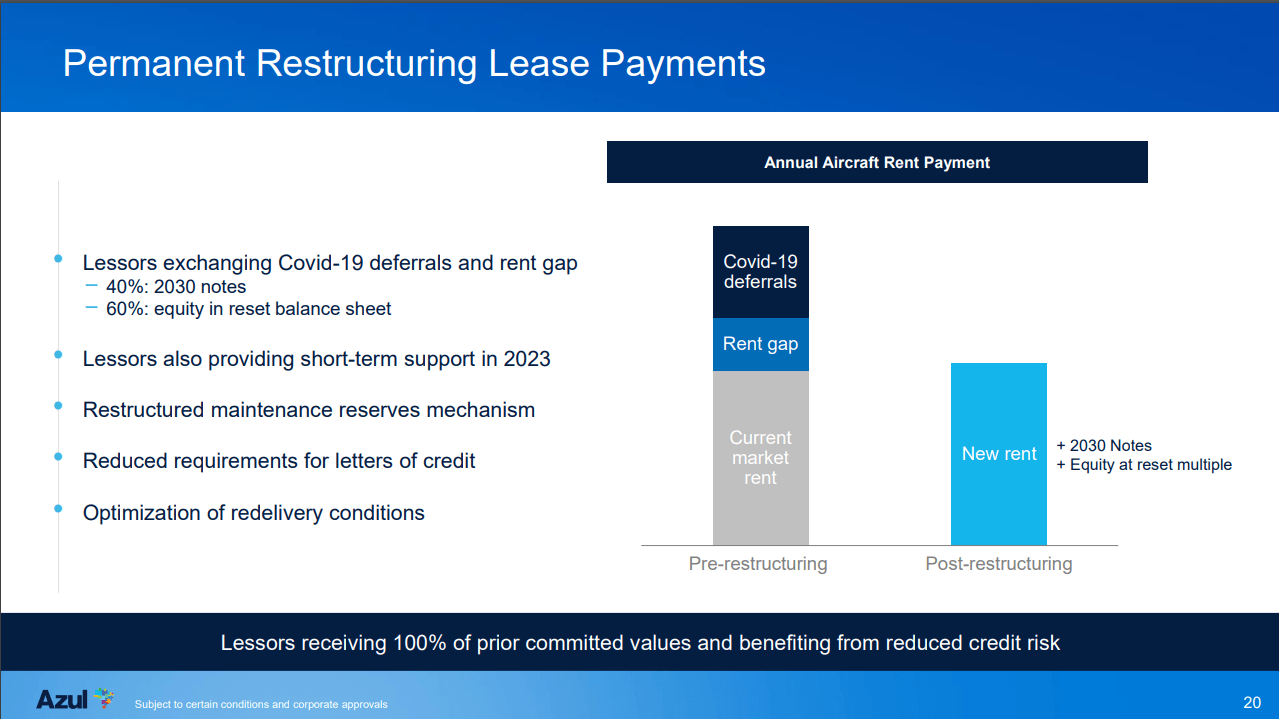

Shares of Azul surged for two reasons. The first one is that for 2023, the airline expects another year of strong EBITDA performance, which should further improve the net debt to EBITDA. Moreover, Azul successfully restructured lease plans. Basically, COVID-19 deferrals and the gap between current market rates and contractual lease rates has been converted into a combination of debt and equity. This debt-to-equity conversion will reduce debt and improve the debt-to-equity metric that should make Azul more attractive. Next to that, the restructuring also will aid the cash flows which will help the company reduce its net debt position and its leverage. Similarly, capital expenditures with jet makers has been reset basically granting Azul additional discounts. The fact that OEMs and lessors are taking these steps and feel confident in either granting credit or swapping debt to equity shows that there's a lot of confidence in Azul’s business and that in turn also boosts stock price as we saw today.

What Is The Azul Deal With Lessors?

{kind=link}

Azul’s gross debt consists of 79% of lease related debt. Azul reached agreements with lessors to either swap to notes or to equity for 90% of the its lease obligations. Azul has yet to work those numbers through in their debt calculations. I don’t believe that an agreement covering 90% means that we will see 90% of the lease debt evaporate, but we should significant tailwinds to the debt requirements and the cash flow. So, it is a positive spiral all-in-all.

Conclusion: Azul Strategy Is Promising, Risk Reduced

My view on Azul remains more or less unchanged. We see that the company is performing well on making its fleet more efficient and push down unit costs. Wall Street continues to have a target representing 73% upside. The reality, however, once again is that results show a strong vision from management beaten up by inflation and high fuel prices leading to decline in share prices and nervously surrounding President Lula’s policy can continue to weigh on the Brazilian stock market including Azul stock.

While management did provide some light on what the lease restructuring will mean for the business, we currently do not have sufficient insight to use that to warrant a Buy rating. While the business environment remains strong and Azul will increase flying significantly this year on lower expected fuel prices, the uncertainty for Brazil and the lack of detail from the debt-to-equity agreement with airplane lessors make me hesitant to upgrade the stock. The way I see it, if it were not for the turnaround at Azul and the accompanying restructuring of leases there would have been a significant solvency risk for Azul that would ultimately lead to lessors pulling aircraft from the fleet and Azul being a smaller airline with high debt. So, that was not a manageable position. That position has now significantly improved, but I wouldn’t feel comfortable putting a Buy rating.

For further details see:

Why Azul Stock Is Flying Higher