FRFHF - Why Brookfield And Peers Followed Apollo Into Insurance And What's In It For You

Summary

- Apollo has developed a new model to combine insurance and investing. It is based on structuring retirement liabilities and overperforming in investment-grade fixed income.

- For Apollo, insurance has become a strategy centerpiece. The company has delivered ~20% CAGR since focusing on insurance.

- The strategy still seems underappreciated by the market and Apollo appears trading at a significant discount to its fair value.

- Major peers including Brookfield, Blackstone, KKR, Ares, and Carlyle are replicating elements of Apollo's strategy.

- Brookfield is following Apollo very closely and allows investing in the strategy on either an asset-light (via BAM) or asset-heavy (via BN) basis.

We will start with an ultralaconic recap of the first installment of this series. Please read "How Brookfield and peers make money..." if something in the following section is not clear to you. Building on this recap, I hope to make the insurance strategy of alternative asset managers accessible for all readers at the cost of some oversimplification.

A primer on alt asset managers

- Alternative ("Alt") assets are everything other than public-traded stocks, bonds, and cash instruments. The most popular alternative asset is private equity followed by real estate, private credit, natural resources, infrastructure, renewables, and some others. Since alt assets do not trade publicly, they are illiquid and may take years to sell.

- Alt managers source funds mostly from institutional clients with long investment horizons such as pension plans, college endowments, sovereign funds, and so on. Clients' contributions are organized in so-called private funds that differ by vintage and strategy. Alt managers handle simultaneously tens of private funds with a typical lifetime of 7-10 years during which clients' monies remain locked. When a fund winds up, clients receive back their contributions with profits. Since alt managers have to consolidate private funds in their statements, their GAAP reports are difficult to understand.

- Recently, alt managers have started attracting funds from high-net-worth and mass-affluent individuals as well (the so-called retail channel). Despite certain hiccups, it is considered a promising channel for growth.

- Some alt managers invest their own significant funds along with clients to achieve alignment of interests and are called asset-heavy. Others try to invest as little as legally possible and are called asset-light.

- The biggest alt managers include 6 companies (that I call the "Big Six") but 7 stocks: Blackstone ( BX ), Brookfield Corporation ( BN ), Brookfield Asset Management ( BAM ), Apollo ( APO ), KKR ( KKR ), Carlyle ( CG ), Ares ( ARES ). Each of the Big Six has its unique strategy and several of them have beaten the market over the long term. All of them are more volatile than the market and currently several of them are trading at a high dividend yield.

- Alt managers charge clients fees. For asset-light managers, these fees dwarf all other sources of revenue. Asset-heavy managers can count on returns on their capital as well, but fees are still the most reliable and valuable part of their business. Fee-related earnings (FRE) is the most important line item of an alt manager's income.

- The clients agree to pay fees since normally (but not always) the returns they receive AFTER FEES are higher than they can achieve otherwise. Alt manager's performance track record is a valuable intangible asset that is highly cherished.

- Fees can be divided into management fees charged as a percentage of clients' funds (similar to mutual funds but higher) and performance fees. Smaller advice and transaction fees charged on a per-event basis are usually grouped with management fees. Management fees are stable and predictable as they are being charged quarterly while a private fund exists. Some performance fees are assessed periodically as well but can be zero if investment targets are not reached. The best-known performance fee is the so-called carried interest ("carry") that represents a slice of investment gain/income received by an alt manager only when a fund is wound up provided its investment performance is above a certain hurdle rate.

- Since fees are dependent on assets under management ("AUM"), AUM is the single most important metric for all asset managers. When we talk about industry growth, we mean growth in AUM. The total of alt AUM today is estimated at $13T with 40% of them in private equity. The Big Six forecast growth in AUM at ~16-20% over the next five years or so.

Berkshire's business model

Warren Buffett popularized a close connection between insurance and investments. Most of my readers must have read Buffett's annual letters explaining it but I will repeat his mantra in short.

Insurers receive premiums before paying claims which allows them to generate "float" - cash that is reserved for paying future claims but that can be invested meanwhile. As long as a property and casualty ("P&C") insurer is growing and generates underwriting profits (i.e. its premiums are greater than the sum of its claims and expenses), its float grows as well. For our ever-profitable and ever-growing insurer, today's float is a liability that will NEVER be paid (because it will only grow) and thus it can be used for long-term investments such as buying stocks or acquiring businesses.

As far as I know, nobody before Buffett formulated this principle so openly. Most of the real-world insurers are less confident in their underwriting profitability and/or their growth and invest their float mostly or only in reliable bonds.

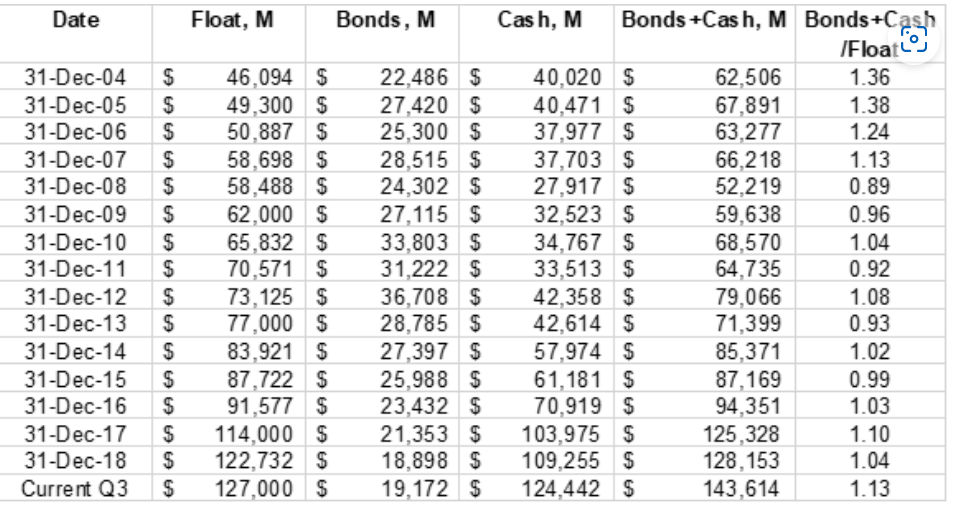

In his insurance operations, Buffett is also more conservative than in his verbal statements. Below is a table from one of my old articles about Berkshire Hathaway ( BRK.A )( BRK.B ) that shows that the sum of cash and bonds on its balance sheet usually exceeds its float. However, in 2008, when stocks were particularly attractive due to the Financial Crisis, Buffett used the float to fund aggressive equity investments. On a smaller scale, he did it also in 2009, 2011, 2013, and 2015.

{kind=link}

For Berkshire, insurance always means P&C operation (not counting some life reinsurance). This is not by chance. P&C insurance has short-duration contracts (typically one year and even less for some cases) and at the end of the contract term, a conservative carrier knows its underwriting results fairly well. Thus both underwriting profits and float are available in cash and can be invested, at least partially, in stocks or acquisitions.

On the contrary, contracts for life insurers have long duration and profits are accounting-driven and accounting itself is arcane. Actual cash is unambiguously generated only at the end of the long-term contract. This makes life insurance unattractive for a capital allocator like Buffett.

Berkshire's model, however, has a major weakness - it needs Buffett to make it work at least during the growth period. Markel ( MKL ), Alleghany (Y), and Fairfax ( FFH:CA ) have tried to replicate it with limited success. Both Markel and Fairfax made significant investment mistakes at a certain point. Alleghany has avoided it but was too cautious to generate strong returns and recently was acquired by Berkshire.

Hedge funds and insurance

Some hedgies tried to exploit insurance differently. For reasons that will become clear shortly, we will spend a couple of paragraphs on it.

The two well-known examples involve famous hedgies Daniel Loeb and David Einhorn. Both set up affiliated/controlled public reinsurance companies in the Caribbean that paid investment management fees to their hedge funds. As long as one trusts publicly announced plans, these reinsurers were supposed to benefit from the hedgies' investment acumen and offshore taxation.

In reality, hedge funds were the only beneficiaries. Hedgies viewed reinsurers' float as a permanent capital to manage and an endless source of fees. Under this lens, reinsurance underwriting was secondary and overall performance was mediocre, to put it mildly. Investors in these public reinsurers have not fared well while hedge funds pocketed hundreds of millions in fees.

Athene and Apollo

Apollo co-founded insurer Athene right after the Financial Crisis and became its major and controlling shareholder. James Belardi, a long-time insurance executive who is still Athene's CEO, was another co-founder. Athene's design was based on fundamentals that Belardi had learned for 20 years of his previous insurance career.

The timing of Apollo's entry into the insurance industry was not accidental. After the Financial Crisis, banks became tightly regulated and had to limit their lending activities. The need to borrow money, meanwhile, kept growing in line with the economy. This mismatch had created a profitable niche to exploit and Apollo made a decision to become a non-bank lender. Back then, very few, besides Apollo, figured out the long-term consequences of the Dodd-Frank Act and similar regulations.

At that time, Apollo was an asset-light alt manager without the wherewithal to fund any loans. The answer was to lend other people's money and Athene's float was supposed to become one (but not the only one) source of funding. The beginning was rather modest - Athene had still to generate float and Apollo had still to optimize its lending skills.

While the concept itself was rather creative, its implementation required even more creativity. However, James Belardi had done it before for his previous employer.

Banks fund their loans with customers' deposits. Insurance companies, in principle, can fund loans with underwriting liabilities aka float. But not all floats are created equal. Buffett needs P&C short-duration float to fund equity investments for the reasons I already explained. On the contrary, Apollo needed long-duration liabilities to benefit from the illiquid long-term nature of private credit. Of all insurance companies, life insurers have the longest-duration float and so Athene was destined to become a life insurer.

This solution had another important benefit: a typical assets-to-equity ratio for life insurers is something like 10:1. Since Apollo's fees are based on AUM, it provided a simple way to generate a lot of fees on a rather small equity investment.

All this was more or less obvious. But the critical step in Athene's design was a strict limitation on products it would underwrite. Oversimplifying a bit, Athene would specialize only in annuities.

The simplest type of annuity is a fixed annuity when a customer gives an insurance company a certain amount of money with an exact knowledge of how much and for how long she will receive back from it at a future date. This type of annuity is quite similar to a long-term bank CD (or a set of CDs to account for multiple contributions and/or payouts). There are other types of annuities with fixed-indexed annuities being especially popular. Some annuities also include elements of mortality risks. However, by using derivatives, reinsurance, and hedging, a life insurance company can reduce a more complicated annuity to a simple fixed annuity. If it is not possible, Athene is not interested to underwrite the product. Nor it is interested in other insurance products such as P&C, medical insurance, long-term care, variable annuities, and so on.

In this regard, Athene is an insurance company that closely resembles a bank with funding from annuity liabilities in place of CDs. As long as Athene's return on investments is greater than annuity funding costs plus operating expenses, it generates spread-related earnings ("SRE").

Since annuities are primarily for (future) retirees, Athene has become a specialist retirement company and that is how it positions itself. Due to population aging, retirement funding will remain a growing industry for years to come.

Athene acquires annuities via several channels. First, from individuals through different intermediaries. Secondly, by reinsuring annuity liabilities generated by other insurers. Thirdly, by acquiring closed blocks of already existing annuities from other insurers. Fourthly, by agreeing to provide defined-benefit pensions to employees of third parties (it is also called a group annuity or a pension risk transfer). And finally, by agreeing to take deposits from institutions (something like corporate CDs with either fixed or floating rates) - the so-called funding agreements that are not related to annuities but are similar in structure.

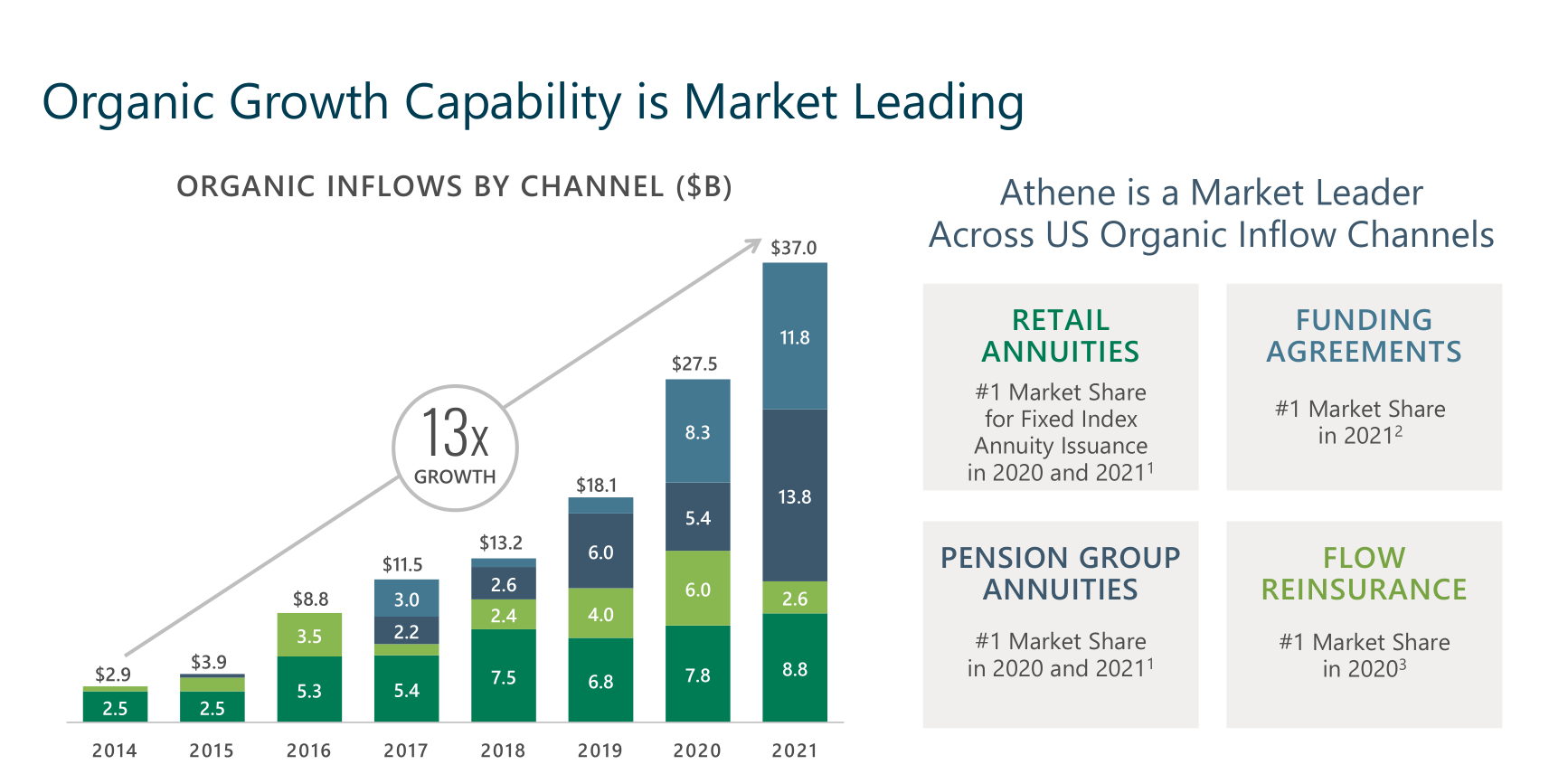

Below is a slide from recent Athene's presentation to illustrate how it works in practice. The slide shows only impressive organic growth without occasional big acquisitions of closed blocks.

{kind=link}

Despite all the efforts in design and successful implementation, Athene as a public company had never traded well. Many investors (including truly yours) considered Athene a means to create AUM for Apollo's fees and nothing else. It is not particularly surprising once one is familiar with hedgies' insurance experiments.

In mid-2021, Apollo and Athene agreed to merge and it became a total surprise for me. Only after this announcement, I started looking at Athene seriously. Under the merger lens, it became clear that Athene was much more than a supplier of AUM to Apollo.

Since the merger (it closed on Jan 1, 2022), previously asset-light Apollo has become asset-heavy. What was Apollo's motivation for merging with Athene?

One of famous Apollo's tenets is "purchase price matters". This was the case with Athene because it was trading poorly. The purchase was done by issuing additional shares of Apollo at around P/E~6.

But the low price was a requirement, not the motivation. The real reason was achieving the full alignment of interests between both sides. It is clearly advantageous for the insurance side because the investment side, handled by Apollo, will be paying closer attention to Athene's SRE in addition to FRE. However, it is less obvious that Apollo will also benefit from Athene's capital generation. Before the merger, asset-light Apollo was paying out practically all earnings in the form of dividends. Athene generates capital beyond its growth needs and this capital can be and has already been used for long-term investment opportunities beyond immediate SRE generation.

The world according to yield

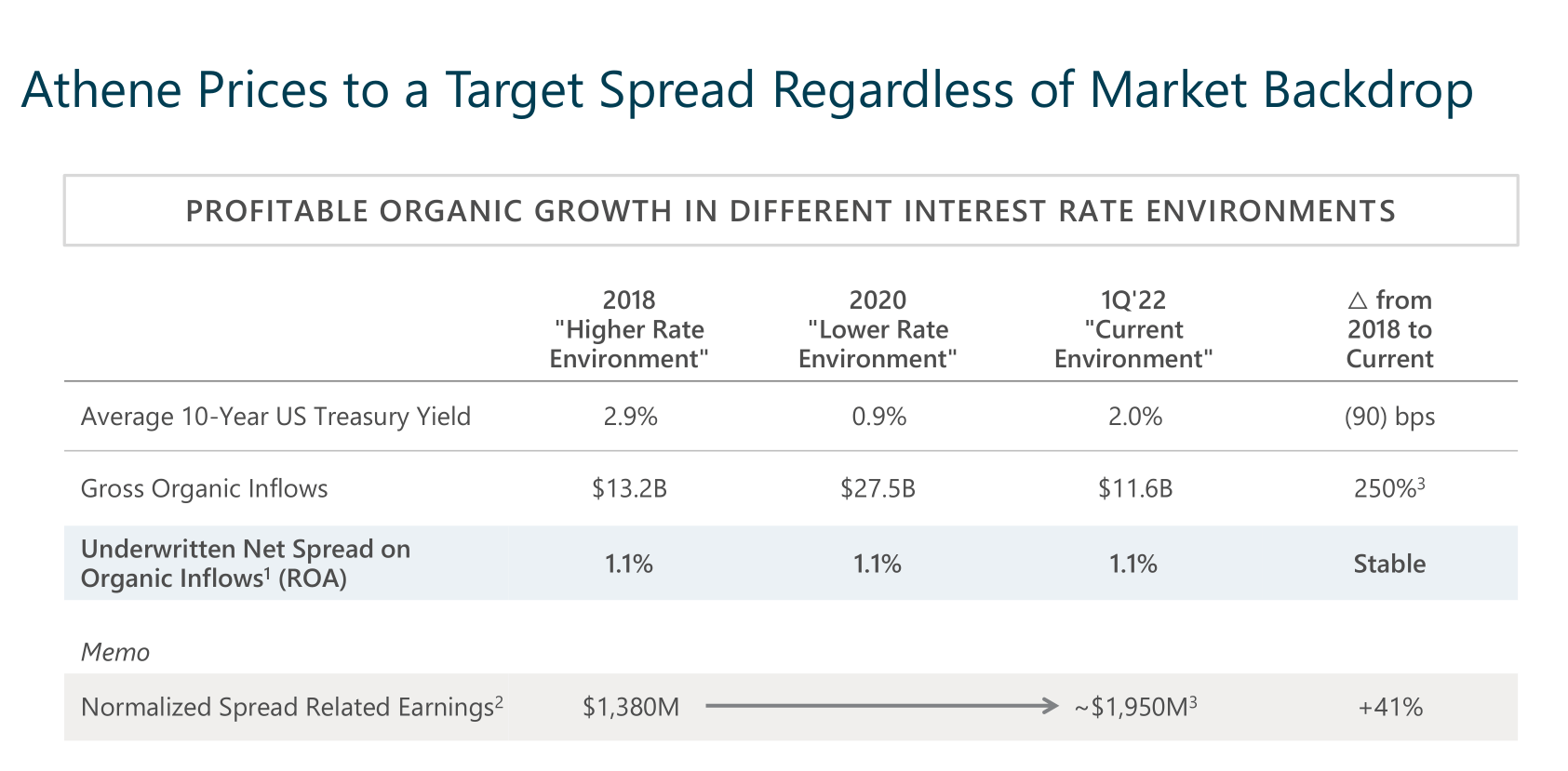

So far, we have described the liability side of Athene. But what is on its asset side managed by one of Apollo's investment groups? Before we proceed, please take a look at Athene's stable spread generated:

{kind=link}

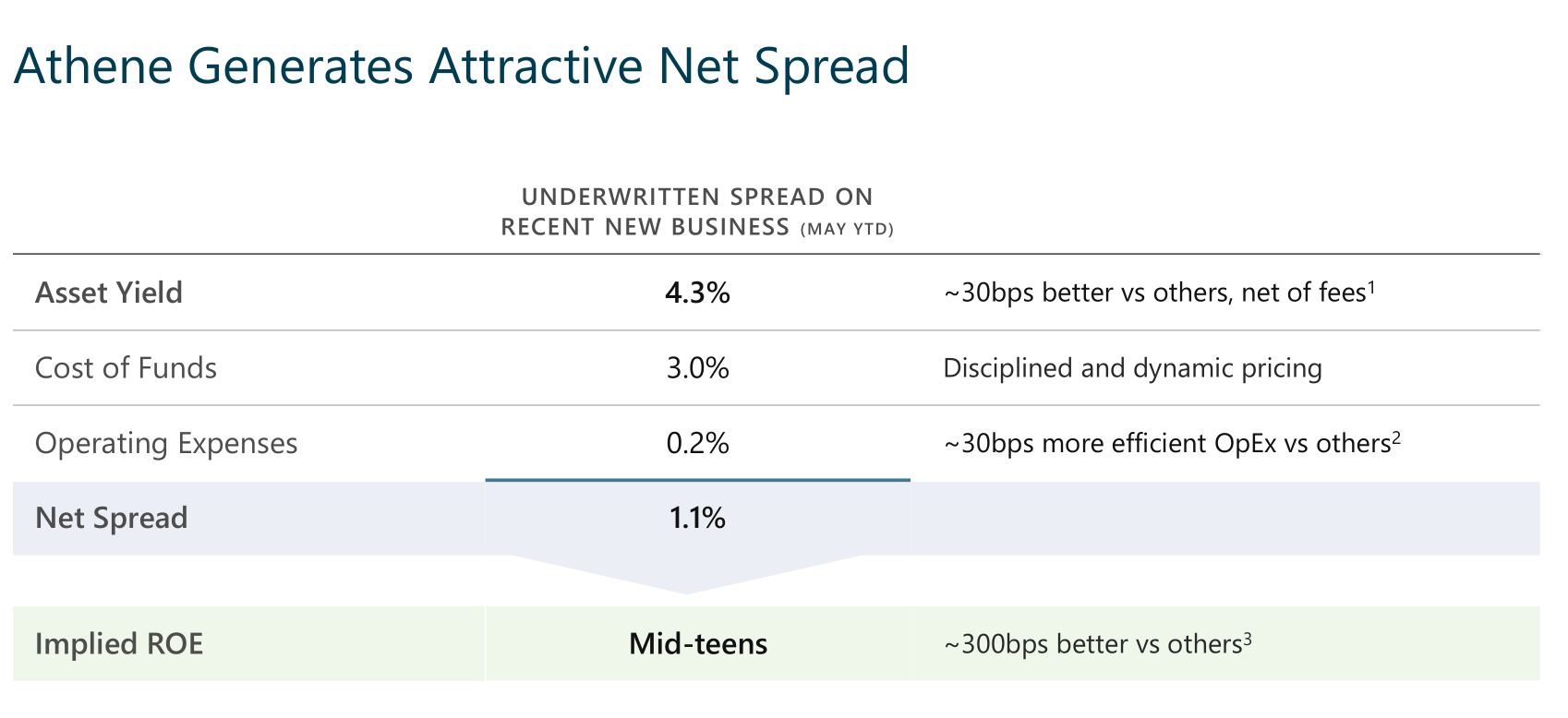

And the following slide explains how this spread is achieved:

{kind=link}

So, besides thoroughly structuring its liabilities, Athene also incurs lower operating expenses (which is not surprising for a narrow-focused and scaled-up specialist) and achieves better investment results AFTER APOLLO'S FEES! This overperformance may seem small at only 0.3% but Athene's assets are ~11 times higher than its equity and it allows to generate ROE several points higher than its competitors!

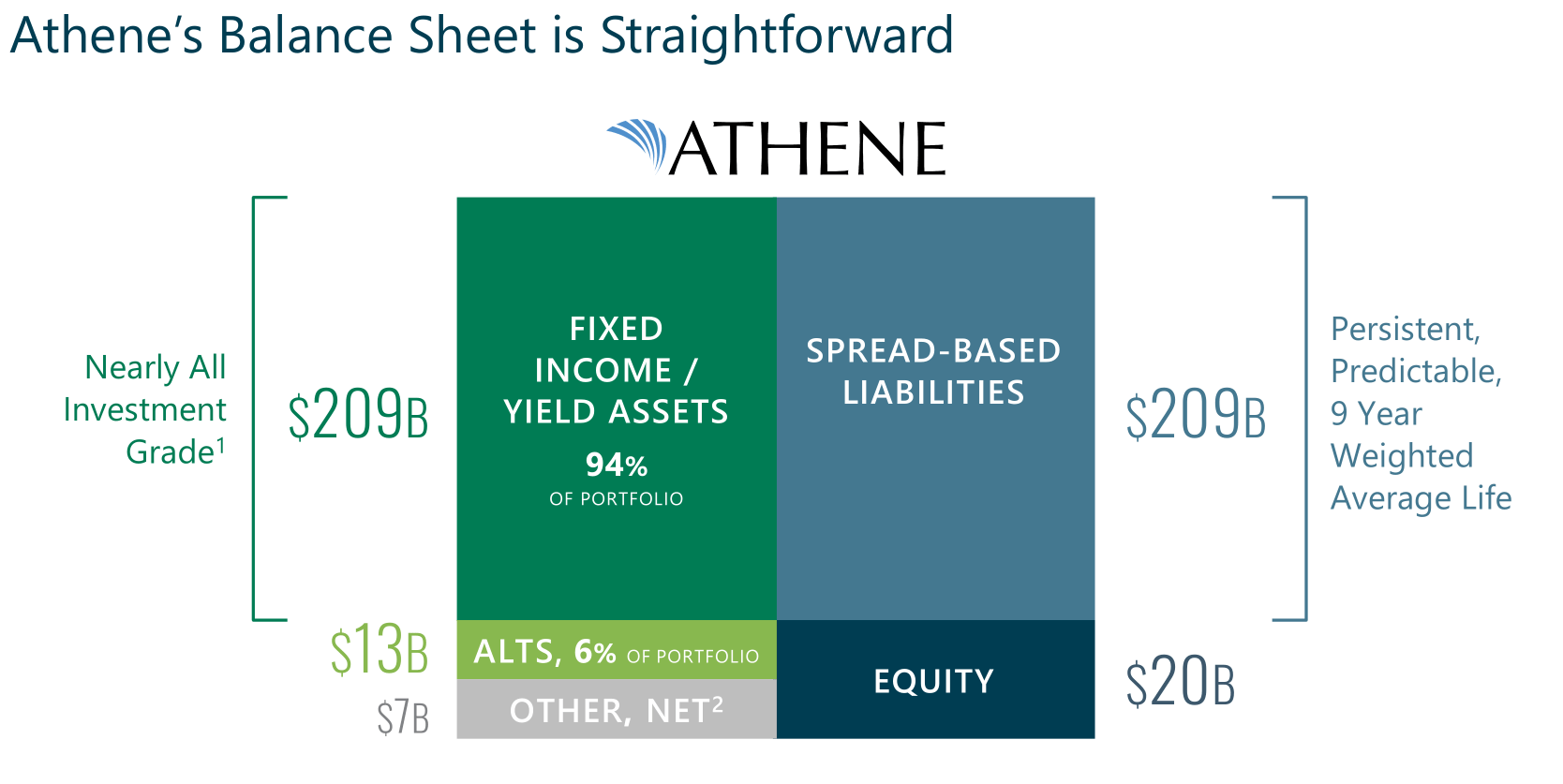

To understand the reason for this overperformance, let us take a look at Athene's balance sheet first:

{kind=link}

There are two components of "secret sauce" here. First, part of Athene's equity (but not float!) is invested in various equity-like alts across Apollo's strategies. They generate annual returns of about 11% on average which contributes to investment outperformance.

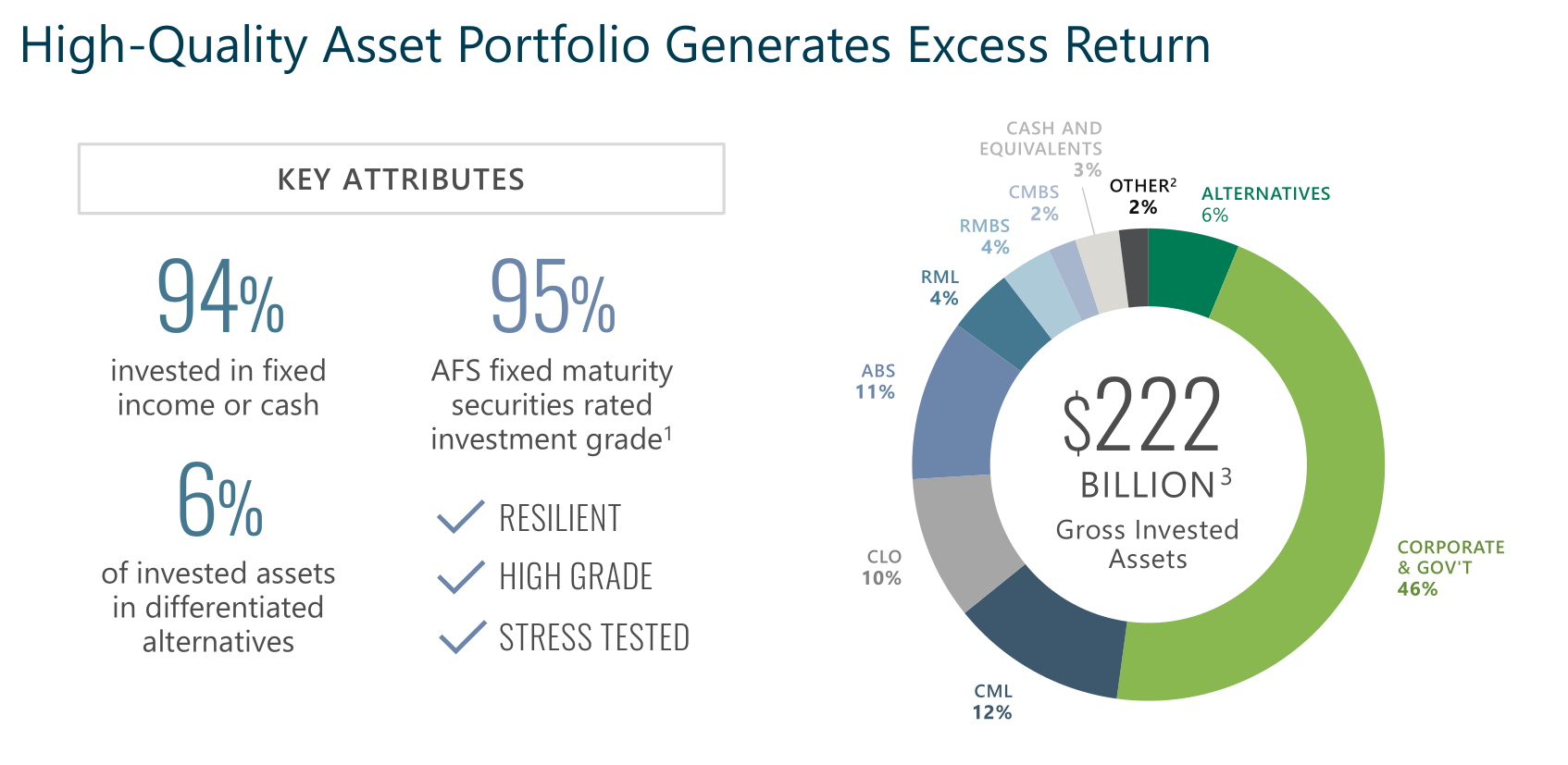

Let us turn now turn our attention to 94% of Athene's assets in fixed-income. Roughly half of it is in corporate and government bonds not different from other life insurers. But the other half consists of investment-grade securities originated mostly by Apollo itself.

{kind=link}

To originate debt, Apollo has 13 internal independent underwriting groups (and is in the process of acquiring the 14th one from Credit Suisse) that are specialized in lending to a vertical the group knows in detail. For example, one group may specialize in senior secured lending to mid-market companies, another in commercial mortgages, and so on. Apollo is always on the prowl to start, hire, or acquire new groups in different geographies to cover more and more lending niches. These groups are successfully competing against banks and surprisingly often cooperate with them. Per Apollo's estimate, only about 20% of US lending today is originated by banks. To make our discussion more down-to-earth, I will bring a simple business case that I have been slightly involved in.

My friend is selling his medical office in New York which he does not need anymore. The property has certain issues but eventually, he found a buyer who agreed on the price. The buyer wants to start a cosmetics business in the office but she is a relative newcomer to the US and does not have a credit record that would allow her to obtain a bank mortgage. However, she offered to pay my friend 2/3 of the purchase price in cash plus a 5-year 7% seller-financed interest-only mortgage with a balloon payment at the end. My friend does not need cash now and is agreeable to this structure.

If the deal closes my friend will originate a mortgage that banks do not want. Do you consider this mortgage risky? It seems rather safe to me because of the claim seniority, collateral quality, and low loan-to-value ratio. In my friend's portfolio, this loan can become a bond replacement, paying a higher yield without higher risks. If everything goes well, my friend will pocket additional money without any hassle. If something goes wrong, he will have to foreclose on the property but it should be a very profitable hassle.

There are 3 differences between my friend and Apollo's underwriting groups: the scale, the flow, and the securitization. Apollo's groups can set up a flow of sizable deals in different verticals and then securitize them making the end product truly investment grade but with a higher yield (I am hopeful my readers are familiar with securitization - it will take me too long to explain it here). Similar to my friend's case, the underlying loans are fairly illiquid but that is acceptable for entities with high-duration liabilities like Athene.

Several conditions are important for this type of activity: the claims should be senior; the loans are often tailor-made rather than standard; documentation control is essential for downside protection and favorable covenants; and the loans should be funded rather quickly to make it convenient for the borrower.

Before the Apollo-Athene venture, private credit implied primarily either distressed debt or junior speculative debt. Working with Athene, Apollo has become a specialist in high-grade debt, unique among alt managers. The ability to generate investment-grade debt (though illiquid in many cases) has led to two important consequences. First, Apollo's high-grade products are fit not only for Athene but for other insurance companies and pension funds as well. Secondly, Apollo has become capable of offering holistic and complicated capital solutions to big companies across the credit spectrum - from equity to investment-grade debt with everything in between. Some of these deals have already been spectacularly successful like financing and makeover of Hertz, for example.

Apollo defines its objective in private credit as delivering better returns per unit of risk. Risk in this case is measurable as either back-looking historical credit losses (Athene's credit losses are very low, lower than those of its peers in life insurance) or forward-looking debt metrics. As long as Apollo-originated products are attractive in this regard, they end up on either Athene's balance sheet (generating both FRE and SRE), in Apollo's private funds (generating FRE), or on third-parties balance sheets (generating transactional and sometimes, management fees as well).

Quick Apollo's evaluation

I spent time on Apollo/Athene because it helps to understand the combination of alt managers and insurance in general. But once one understands how Athene works, it is natural to crudely check whether its value is properly reflected in Apollo's stock price.

On the Q3 earnings call, APO forecasted ~$2.35 and ~$4.00 per share for FRE and SRE respectively for the full 2022. The rest of Apollo consists of carry and returns on its capital outside of Athene's balance sheet (Principal Income and Interest or PII in Apollo's lingo). PII is much smaller than FRE or SRE and fluctuates wildly. But I noticed that it is always bigger than combined parent costs and interest expenses. For simplicity, we can conservatively discard all three of them together. The company also forecasted an 18% tax rate, which translates into $1.93 after-tax FRE and $3.28 after-tax SRE. Using 25 and 15 multiples respectively, we come up with a ~$97 estimate of APO's value vs its current price of ~$67. Alternatively, APO is currently trading at a P/E ratio of 67/(1.93+3.28)~13 with expected growth of something like 15% or higher.

I will avoid specific discussions about multiples here, please consider it as nothing more than a ballpark estimate. Combined Apollo will report its first full-year numbers shortly. It will be interesting to see its Q4 buybacks and the dividend increase from Q1.

Risks and attractions of Apollo's model

The main attraction of Apollo-Athene's model is an expansion of alt managers' addressable market. Now alt managers can deal with all kinds of debt and the demand for higher-yielding investment-grade debt should land new clients and additional fees.

It does not necessarily require having an insurer on the alt manager's balance sheet. Until 2022, Apollo had exercised this strategy holding a significant stake in Athene but without merging with it. Upon the merger, Apollo got access to SRE and Athene's capital. But Athene, like most life insurers, has a high ratio of assets to equity and small investment or underwriting mistakes can lead to big negative consequences. This risk is always with life insurers and will never go away. It may be further exacerbated since Apollo-generated investment-grade assets are relatively new compared with well-known traditional bonds.

So far, nothing foretells that these assets are riskier than bonds, quite on the contrary. Athene's credit losses have been lower than those of its peers. Certainly, Apollo has full confidence in this strategy as well, otherwise, the merger would have never happened. Athene regularly stress-tests its portfolio trying to simulate the environment of the Financial Crisis or even worse and publishes the results on its website. Nothing portends any trouble. But still, the only way to avoid the insurance risk is to keep the insurer separate from the alt manager.

The Big Six follow each other rather closely and clone the best ideas. All of them have recognized the opportunity of working with affiliated insurers but some preferred to stay asset-light. Some investments in insurers were still necessary even for Blackstone - the most staunch asset-light manager. Alternatively, asset-heavy managers decided to replicate Apollo-Athene's strategy in full. To illustrate it, we will focus on Brookfield's approach.

Brookfield and Oaktree

In 2018, I read a transcript of Bruce Flatt's interview in which he predicted that quite shortly Brookfield would have hundreds of billions of AUM in credit funds. It sounded unbelievable as at that time, Brookfield barely participated in private credit. Still, Bruce Flatt was correct. In 2019, Brookfield acquired a majority stake in famous credit specialist Oaktree which was the first step in entering insurance.

In 2020, Brookfield formed Brookfield Reinsurance ( BNRE ) as its new entity to conduct insurance operations which started quarterly reporting in 2021. Initially, these operations were at a small scale until in May 2022, Brookfield acquired American National Group, a public insurer, for about ~$5B. This acquisition was another necessary step as Brookfield now has a capable underwriting group with various insurance licenses in all 50 states and an ability to grow its insurance business organically. But the key prize was ~$30B in insurance float that Brookfield was about to invest more profitably.

Brookfield has also made several smaller acquisitions in the insurance industry including a ~20% stake in American Equity Life ( AEL ). Altogether, Brookfield currently has about ~$40B in insurance assets and this is just the beginning. Surely, the company is on the hunt for new acquisitions in the industry.

In terms of strategy, Brookfield appears to replicate Apollo with a strong emphasis on retirement and annuities. The expectations are rather high and Brookfield is currently estimating the value of its insurance operations at exactly two times its book value. While there is some ground for optimism regarding Brookfield's insurance operations, in my opinion, this estimate is not sustainable.

If a mature insurer produces an ROE of 10%, it is trading close to its book value. To trade at 2 times its book value, an insurer needs to achieve a 20% ROE. Can Brookfield Reinsurance reach this number? It seems unlikely in the long run as even Athene has not done it (Athene has produced a superior ROE of 15-17% over many years). However, it may be possible for Brookfield to reach close to 20% ROE in 2023 alone due to a favorable increase in interest rates.

Overall, I would not overestimate initial Brookfield's success in insurance as the company still has many wrinkles to iron out. We will start with Oaktree as the main credit tool in Brookfield's arsenal.

Historically, Oaktree has been a distressed debt specialist. Its most successful deals involved buying deeply discounted junk debt of companies that were either in bankruptcy or close to it. Later this debt would be either successfully converted into equity of the restructured company or sold at a higher price. This is not what is required for insurance operations. I do not have the slightest doubt in Oaktree's credit capabilities but as we have seen in Apollo's example, investment-grade skills have to be honed and built one step at a time.

The second problem is that though Brookfield owns a majority of Oaktree's shares (64%), it does not control the company. Oaktree has an archaic structure and is controlled by its partners with Howard Marks and Bruce Karsh being the main actors. It has a very important implication: Oaktree's FRE margins are way smaller than Brookfield's (approximately 30%+ vs 50%+) and Brookfield cannot change it no matter how many shares it controls. In other words, FRE generated by insurance assets are expected to be smaller than in the case of Apollo (Apollo's FRE margins are comparable with Brookfield's).

I believe this is the main reason why the management of BNRE float is advised by Brookfield and sub-advised by Oaktree. It implies some agreement between Brookfield and Oaktree regarding the splitting of management fees but we do not know anything about it.

Inside its real estate, infrastructure, and renewables businesses, Brookfield has opportunities to originate debt similar to how Apollo is doing it. As of today, however, we do not know much about these originating groups, their structure, and their scale. In my opinion, it should take several years to achieve palpable progress in this direction.

Finally, some things are not clear on the liability side of Brookfield's insurance operations. American National is a diversified insurer. While annuities are an important part of its business it also underwrites P&C and medical risks. This is a direct contradiction to Athene's playbook. Brookfield emphasized many times that it is primarily interested in retirement float but did not specify its plans regarding other types of float on its balance sheet.

On the positive side, Brookfield offers an opportunity in insurance that Apollo cannot match. Since December, investors can buy Brookfield either as asset-heavy BN or asset-light BAM. BAM is different from all other asset-light managers because it enjoys all the benefits of alignment of interests without the costs of it incurred by BN. By buying BAM, investors can benefit from the growth of insurance float on BN's balance sheet without any exposure to insurance risks as BAM is not invested in insurance at all.

Conclusion

It is time to answer the question in the title: what's in it for you?

Apollo and Athene came up with a new business model for combining investments and insurance. This model may or may not become as profitable as Berkshire's. It has taken many years for Berkshire to make its model widely accepted.

In the world of alt managers, everything is happening more quickly. The remaining five of the Big Six are developing their recipes to combine insurance and investments partially following Apollo's blueprints. Only time will tell who will succeed the most.

But only for Apollo, insurance is the centerpiece of its strategy. At the end of 2011, a couple of years after starting its experiment with Athene, APO was trading at ~$15. It means that over 11 years, APO has delivered ~15% of CAGR solely from stock appreciation. If we add significant dividends, the total CAGR is closer to 20% annually. Is it a sign that the model works or a consequence of declining interest rates?

In my opinion, Apollo's model is quite attractive and still underappreciated by the market. In terms of insurance and investment-grade debt, Apollo is far ahead of the rest of the pack and if you are comfortable with insurance risks, buying APO may be a good step. Alternatively, you can consider asset-light managers such as BAM to benefit from the model but insulate yourself from these risks.

For further details see:

Why Brookfield And Peers Followed Apollo Into Insurance And What's In It For You