CAAP - Why Corporacion America Airports Is Still Undervalued

2023-07-19 13:40:36 ET

Summary

- I've been a longtime bull on multinational airport operator Corporacion America Airports S.A. and shares are up sharply over the past two years.

- Despite that, I believe the stock is still materially mispriced.

- I expect shares to trade above their IPO price in the coming months thanks to growing traffic, rising profitability, and a political catalyst.

I've been a long-time bull on Argentina's airport operator Corporación América Airports S.A. ( CAAP ), first starting coverage in October 2020 when the stock was at $2. Since then, we've enjoyed a tremendous recovery as the firm navigated its debt issues and saw airline traffic start to come back. In 2022, the airport operator returned to GAAP profitability .

Shares have now rallied far beyond where they were trading prior to the onset of COVID-19, and some traders might be thinking that it is time to take profits:

In this article, I will offer highlights of the recent developments in CAAP's story and why I remain bullish and expect further stock price appreciation. For a more complete backstory of the company and its strategy, please see my prior articles. Here's what's new with the company in 2023 and my outlook going forward.

Traffic Tops Pre-Pandemic Levels

CAAP operates airports in half a dozen countries spanning Europe and South America. As such, it is a more complicated story than, say, the Mexican airport operators, which have just one or two countries to worry about. With CAAP, while it had traffic recover rapidly in some markets, others lagged considerably. Its home Argentina market, which accounts for half of the firm's total business, was slow to reopen, as that government had stricter COVID-19 regulations than many other countries.

It was impressive that CAAP returned to profitability in the middle of 2022, as it did so while still generating less than 80% of the traffic that it had been obtaining in 2019. However, the global travel recovery story has now made it to Argentina as well.

On Monday, CAAP reported its June 2023 passenger traffic figures. For the first time, the company's traffic topped pre-pandemic levels, with June numbers coming in 2.6% ahead of the same period in 2019. Here's a table of the company's traffic levels versus the same pre-pandemic period:

CAAP traffic versus pre-pandemic figures (Corporate press release)

As recently as February of this year, CAAP's overall traffic was still down double-digits from 2019 levels. We've seen a major upward inflection just over the past quarter, which should bode well going forward. While some other publicly-traded airport operators have started to show a material deceleration in their growth trajectories, it appears CAAP's traffic has plenty more room to increase.

I'd also note that the June figures represent a massive 32% year-over-year jump versus June 2022. It took CAAP longer than the Mexican airport operators to fully recover from the pandemic disruption, but CAAP is now building a strong track record of its own.

And traffic has been a lagging indicator for the company, as opposed to other metrics. Thanks to management's swift cost-cutting during the pandemic, the company now has a much lower operating cost base than it did pre-pandemic. This can be seen in the company's EBITDA margin, which is now more than 1,000 basis points above where it was prior to the onset of the pandemic:

This also translates to GAAP earnings, with CAAP becoming a value stock on a price-to-earnings basis thanks to the surge in net income:

The company's earnings peaked at around 60 cents per share annually prior to 2020. Now, CAAP has already hit $1/share in earnings, and earnings should grow dramatically from the current run rate given that traffic is increasing at a more than 30% annualized pace at the moment.

This isn't just natural recovery from the slowdown, either. Part of what makes CAAP unique is that it invests heavily in growing its airports. Some operators, such as the Mexican airport companies, tend to focus on maximizing near-term free cash flow generation and resulting dividends per share. That's fine and well, I greatly appreciate the dividends from those companies.

By contrast, however, CAAP focuses on airport concessions where there has been underinvestment in an asset, giving it room to reposition the property for significant growth. CAAP just opened a massive new terminal at its flagship Buenos Aires airport this year, which should drive growth for a long time to come. There is a major expansion occurring in Brazil, and the company is also reworking the Florence (Italy) airport so it can receive larger planes, which should expand its reach dramatically.

The structural bull case should be quite apparent. There is a long runway for deploying capital in infrastructure assets with a functional monopoly in their local market. CAAP is a reasonably aggressive operator. It uses leverage of around 3x Net Debt/EBITDA to plow more money back into its concessions earning high rates of return on that invested capital.

The pandemic put this model to the test, with CAAP having a sizable debt load and minimal revenues coming in for a significant period. However, another of the firm's strong points became apparent there. All the firm's operations are held through subsidiaries, with debt tied to airports at a country level rather than the parent company. This insulated CAAP from facing wipeout risk if anyone country's airports became economically untenable. As it turns out, CAAP was able to maintain its concessions as local governments were quite flexible in giving CAAP relief, assistance, and improved terms on concessions to make it through the down period. I mention all this, however, to note that I believe CAAP's leverage policy is prudent and can supercharge returns for investors going forward.

Shares Are Still Surprisingly Cheap

Here's where things get really interesting. Due to the combination of leverage and a skyrocketing level of EBITDA generation, CAAP shares remain incredibly cheap on an EV/EBITDA basis:

The stock has now risen sevenfold from its October 2020 lows. Despite that, shares still trade at a meager 6.5x EV/EBITDA, barely up from where that ratio was either in 2019 or late 2022.

CAAP should generate about $600 million annually in EBITDA at present. The company has about 160 million shares of stock outstanding, so for the company to add one turn on its EV/EBITDA multiple, the stock needs to rally nearly $4/share. To get the stock to 10x EV/EBITDA, shares would need to move up to the high $20s. This isn't assuming any future EBITDA growth either, that's just based on next twelve-month numbers.

Is 10x EV/EBITDA too aggressive a target? I'd argue no. For one thing, CAAP shares IPOed in early 2018 at around 11x EV/EBITDA. I believe the business is in as good a shape as it was then, if not better, and thus a multiple in the same ballpark would be appropriate.

For another thing, the Mexican airport operators have historically tended to trade at EV/EBITDA ratios in the 12-15x range:

Several of the Mexican airport operators also remain undervalued now versus past historical multiples, but that's a topic for another day.

I understand that Argentina should trade at a discount to Mexico for political and economic reasons. That said, half of CAAP's profits come from outside of Argentina, including in markets such as Italy that should earn a much higher multiple. For another thing, CAAP gets paid $57 per international passenger that arrives in Argentina. Regardless of how far the Argentinian Peso devalues, CAAP is paid in dollars on those Argentine tourist arrivals, so the exchange rate holds little import.

Finally, on the political front, when CAAP IPOed in 2018, Argentine assets were at a relative high point with a conservative government in power and investors feeling optimistic. Since then, Argentina returned to socialist rule and the economy has sputtered to a halt amid a debilitating round of inflation. This had a negative effect on most Argentine assets.

However, this seems likely to change; elections are this fall and conservatives have a considerable lead in the polls. Investor sentiment is also improving, with the Global X MSCI Argentina ETF ( ARGT ) hitting new all-time highs this summer. To the extent that there is a remaining political overhang on CAAP stock, I believe it should lift as investors price in a more business-friendly government.

In February 2018, CAAP's IPO debuted with shares selling for $17 a pop . Today, CAAP has more passengers, higher profit margins, and far higher earnings per share than it did at the time of the IPO. On an EV/EBITDA basis in particular, I believe CAAP shares are at an unsustainably low multiple compared to international peers.

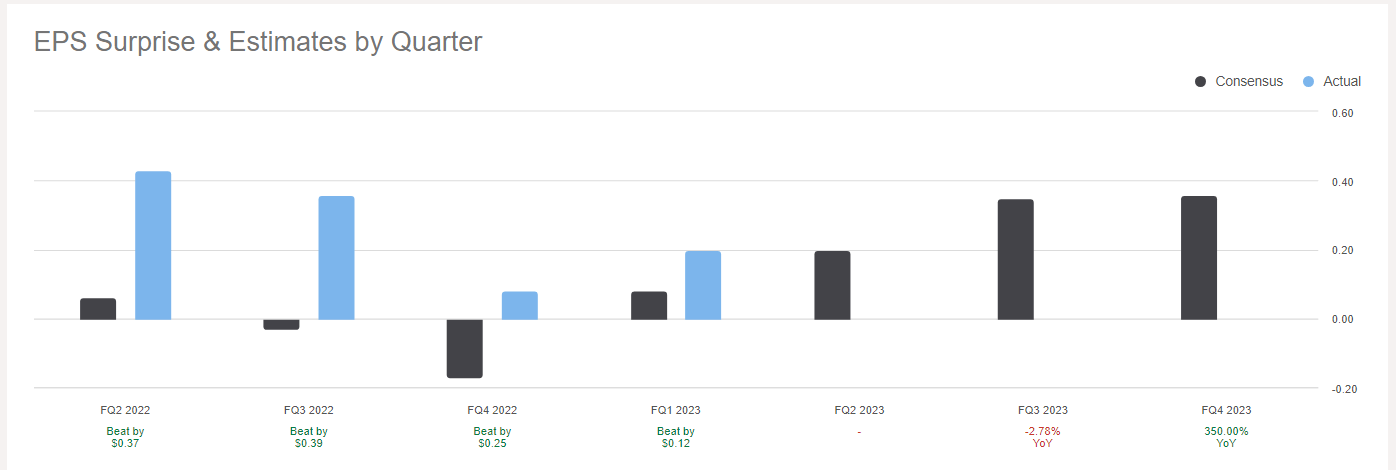

Shares also trade at just 14 times forward earnings and I believe those earnings estimates are too low. CAAP has beaten estimates by a wide margin each of the past four quarters:

CAAP quarterly earnings vs. estimates (Seeking Alpha)

{kind=link}

I think the company will earn approximately $1.50/share over the next twelve months, which would put the stock around 9 times forward earnings. In any case, the valuation is not demanding for a firm that is currently reporting greater than 30% year-over-year traffic growth.

All this to say that purely on the numbers, CAAP looks like a growth stock selling at a value price.

I understand some folks are understandably cautious, with the Corporacion America Airports S.A. share price up 160% over the past year. However, I believe that mostly reflects how badly mispriced shares were. I still see significant upside from here, with the next target being that CAAP should trade above its IPO price ($17) later this year and potentially move into the $20s as the election catalyst plays out and Argentine assets climb.

For further details see:

Why Corporacion America Airports Is Still Undervalued