DB - Why Credit Suisse Is Dangerous To All Banks

2023-03-31 09:00:00 ET

Summary

- You need to pay close attention to what occurred during the recent Credit Suisse write-downs.

- The Swiss regulator opened a can of worms, and its decisions will have major implications for the global banks, especially for the larger ones that have a lot of AT1.

- You need to review the extent of AT1 in your bank's capital structure.

We just wanted to express our opinions regarding Credit Suisse's (CS) AT1 write-down because we think it will negatively affect major international banks.

The CS story had been progressing quite quickly. The bank released its 2022 annual report on March 14, and it noted that it had found a significant flaw in its reporting practices that raised the possibility of misstatement risks. The chairman of the Saudi National Bank, which was a significant shareholder in CS prior to the agreement with UBS, disclaimed any further increases in the bank's stake the following day. The share price of the bank has dropped once more as a result, and the U.S. Treasury Department has reportedly begun examining the financial sector's exposure to CS.

Thereafter, at least four sizable banks reportedly restricted trades with CS, according to media reports from Friday. The French bank BNP Paribas informed clients that it will no longer accept requests to take over their derivative contracts when Credit Suisse is the counterparty, according to news from Bloomberg. On Sunday, March 1, UBS announced plans to acquire Credit Suisse.

The Swiss financial regulator, FINMA, instructed Credit Suisse to write down all of the bank's AT1 instruments ($17.5B), while equity shareholders received their payouts from the deal with UBS. This decision clearly contradicts the global banking supervision rules, which were created after the GFC and were supposed to avoid major banking crises.

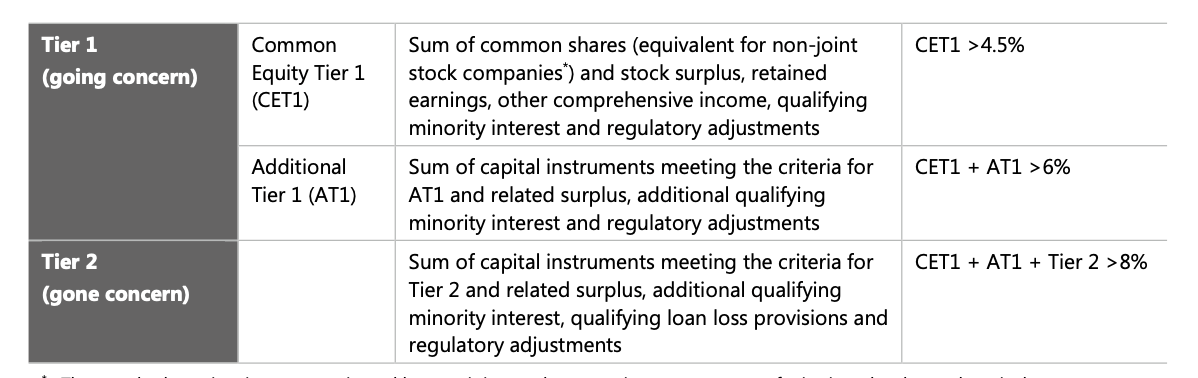

According to the Basel rules, a bank's total available regulatory capital is the sum of these two elements - Tier 1 capital, comprising Common Equity Tier 1 capital (CET1) and Additional Tier 1 capital (AT1), and Tier 2 capital.

{kind=link}

The Basel framework clearly says that CET1 absorbs losses immediately when they occur, and only after that AT1 capital is converted into equities.

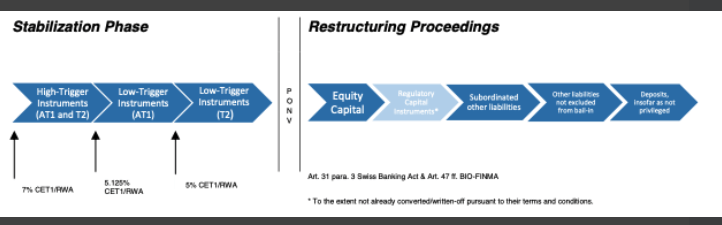

The picture below is from the FINMA's website and shows that the Swiss financial regulator follows the Basel rules as a bank's equity capital should be written down first.

{kind=link}

The FINMA tried to defend its decision, saying that the CS AT1's bond prospectus stated a wipe-out was a risk if certain conditions were met. However, as some legal experts pointed out, one of the conditions has not been met. The government support was a liquidity injection, not a capital injection, which was required to treat the deal between UBS and CS as a viability event. As reported throughout this week, several law agencies are already preparing legal action against the FINMA.

The FINMA's decision seems to have shocked not only bond investors, but UK and EU regulators as well. On March 20, The Single Resolution Board, the European Banking Authority and ECB Banking Supervision published the following press-release:

The resolution framework implementing in the European Union the reforms recommended by the Financial Stability Board after the Great Financial Crisis has established, among others, the order according to which shareholders and creditors of a troubled bank should bear losses.

In particular, common equity instruments are the first ones to absorb losses, and only after their full use would Additional Tier One be required to be written down. This approach has been consistently applied in past cases and will continue to guide the actions of the SRB and ECB banking supervision in crisis interventions.

On the same day, the Bank of England made the following statement:

The UK's bank resolution framework has a clear statutory order in which shareholders and creditors would bear losses in a resolution or insolvency scenario. This was the approach used for the recent resolution of SVB UK, in which all of SVB UK's Additional Tier 1 (AT1) and T2 instruments were written down in full and the whole of the firm's equity was transferred for a nominal sum of £1.

AT1 instruments rank ahead of CET1 and behind T2 in the hierarchy. Holders of such instruments should expect to be exposed to losses in resolution or insolvency in the order of their positions in this hierarchy.

There are various rumors about why the FINMA decided to wipe out CS's AT1 but made payments to the bank's equity holders. One of them says that the Swiss government wanted to keep a good relationship with the Saudi National Bank, which was a top shareholder of Credit Suisse before the deal with UBS. We can't comment on these rumors, and, anyway, the reasons for FINMA's actions are not important now. The Swiss regulator opened a can of worms, and its decisions will have major implications for the global banks, especially for the larger ones that have a lot of AT1 instruments in their capital structure.

First, the holders of AT1 instruments will certainly reassess the risks of ownership. Last Friday, the yield on Deutsche Bank's (DB) AT1 reached a whopping 24%.

Second, FINMA's decision will lead to a spike in the global bank's funding costs, not just for AT1s but for senior debt as well. Even a mild deposit outflow would likely cause liquidity issues when a bank's AT1 is trading at 24%.

Third, the FINMA's decisions suggest that global regulators can easily alter laws and regulations when it comes to dealing with a struggling bank. Imagine a situation where a regulator decided not to write down both equity and senior debt but rather introduce a 5%-10% haircut on deposits. That was extremely unlikely before the FINMA's decision, but now the probability of this event has increased sharply.

Conclusion

At the end of the day, we're speaking of protecting your hard-earned money. Therefore, it behooves you to engage in due diligence regarding the banks which currently house your money. You have a responsibility to yourself and your family to make sure you money resides in only the safest of institutions.

In our methodology, we clearly exclude banks with complex capital instruments such as AT1, and we would like, once again to urge you, to be wary of banks with these risky instruments. You can review the detail of our methodology here so you can apply it in your due diligence of your own bank .

Housekeeping Matters

This article, as well as Saferbankingresearch.com , was a combination of efforts between Avi Gilburt and Renaissance Research, which has been covering U.S., European, LatAm, and CEEMEA banking stocks for more than 15 years.

For those interested, Saferbankingresearch.com covers banks in the US, and has recently begun expansion into European banks, and will continue its expansion later this year into Canadian banks.

If you would like notifications as to when my new articles are published, please hit the button at the bottom of the page to "Follow" me.

For further details see:

Why Credit Suisse Is Dangerous To All Banks