DXCM - Why DexCom May Be Up To 40% Undervalued

2023-09-12 08:00:00 ET

Summary

- DexCom is a leading healthcare stock that has seen significant growth, with shares returning close to 1,400% in the past decade.

- DXCM stock has faced resistance and is currently 37% below its all-time high, partly due to competition from weight loss pills.

- DexCom's business model focuses on continuous glucose monitoring systems for individuals with diabetes, and it has a rapidly expanding addressable market.

Introduction

It's time to talk about DexCom ( DXCM ) , a healthcare stock I have never discussed before. This San Diego-based giant is one of the best-performing healthcare stocks of the past two decades.

Over the past ten years alone, DXCM shares have returned close to 1,400%, beating its healthcare peers and the S&P 500 (SP500) by a mind-blowing margin.

Now, DXCM has run into resistance. The stock ran too hot after the pandemic and is now roughly 37% below its all-time high.

Like most of its peers, DXCM stock is also being pressured by the emergence of weight loss pills.

As diabetes is one of the health risks that come with obesity (the list below shows health risks according to the CDC ), DexCom is one of the victims on the stock market.

- All causes of death (mortality).

- High blood pressure (hypertension).

- High LDL cholesterol, low HDL cholesterol, or high levels of triglycerides (dyslipidemia).

- Type 2 diabetes.

- Coronary heart disease.

- Stroke.

- Gallbladder disease.

- Osteoarthritis (a breakdown of cartilage and bone within a joint).

- Sleep apnea and breathing problems.

The good news for DexCom is that weight loss pills do not pressure demand for its products and services. If anything, it's a complementary product.

In this, I'll walk you through the DexCom business model, its opportunities, the weight loss pills, and why we can assume that DXCM shares are roughly 40% to 50% undervalued.

So, let's dive into it!

The Diabetes Giant

With a market cap of more than $40 billion, DexCom is a leading medical device company focused on designing, developing, and commercializing continuous glucose monitoring ("CGM") systems for individuals with diabetes and healthcare providers.

With FDA approvals for its products dating back to 2006, DexCom has been a leader in this field ever since.

Its latest product is the DexCom G7, which got FDA approval in 2022.

According to the company, the G7 maintains the essential features of the G6, such as fingerstick elimination, continuous glucose readings, and data sharing, and offers improved wearability with a smaller profile and faster sensor warm-up, making it a powerful tool for diabetes management.

{kind=link}

The company also has a service called DexCom Share, which enables remote monitoring of glucose levels through a mobile app, allowing up to five designated individuals to receive real-time glucose data and alerts wirelessly. This system enhances care coordination and support for individuals with diabetes.

It also has DexCom One, a system launched in Europe that includes a sensor, transmitter, and display device that eliminates the need for frequent fingerstick blood glucose testing. It's suitable for individuals aged two years and older.

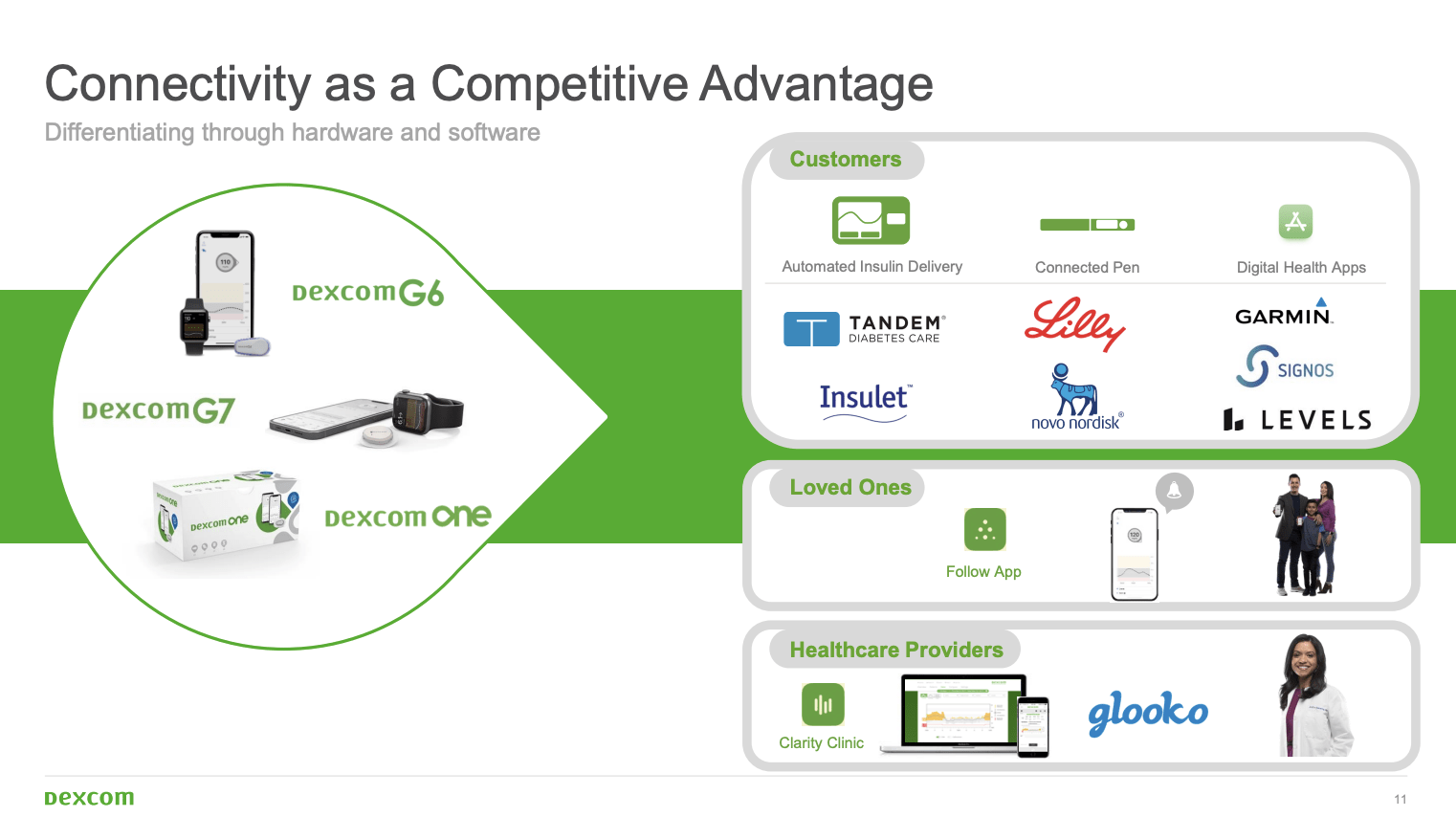

As the overview above also shows, DexCom has entered into collaborations with various partners, including Eli Lilly ( LLY ), Insulet, Novo Nordisk, Tandem Diabetes, and The Ypsomed Group, to integrate CGM technology with insulin delivery systems. These collaborations aim to improve diabetes management and outcomes.

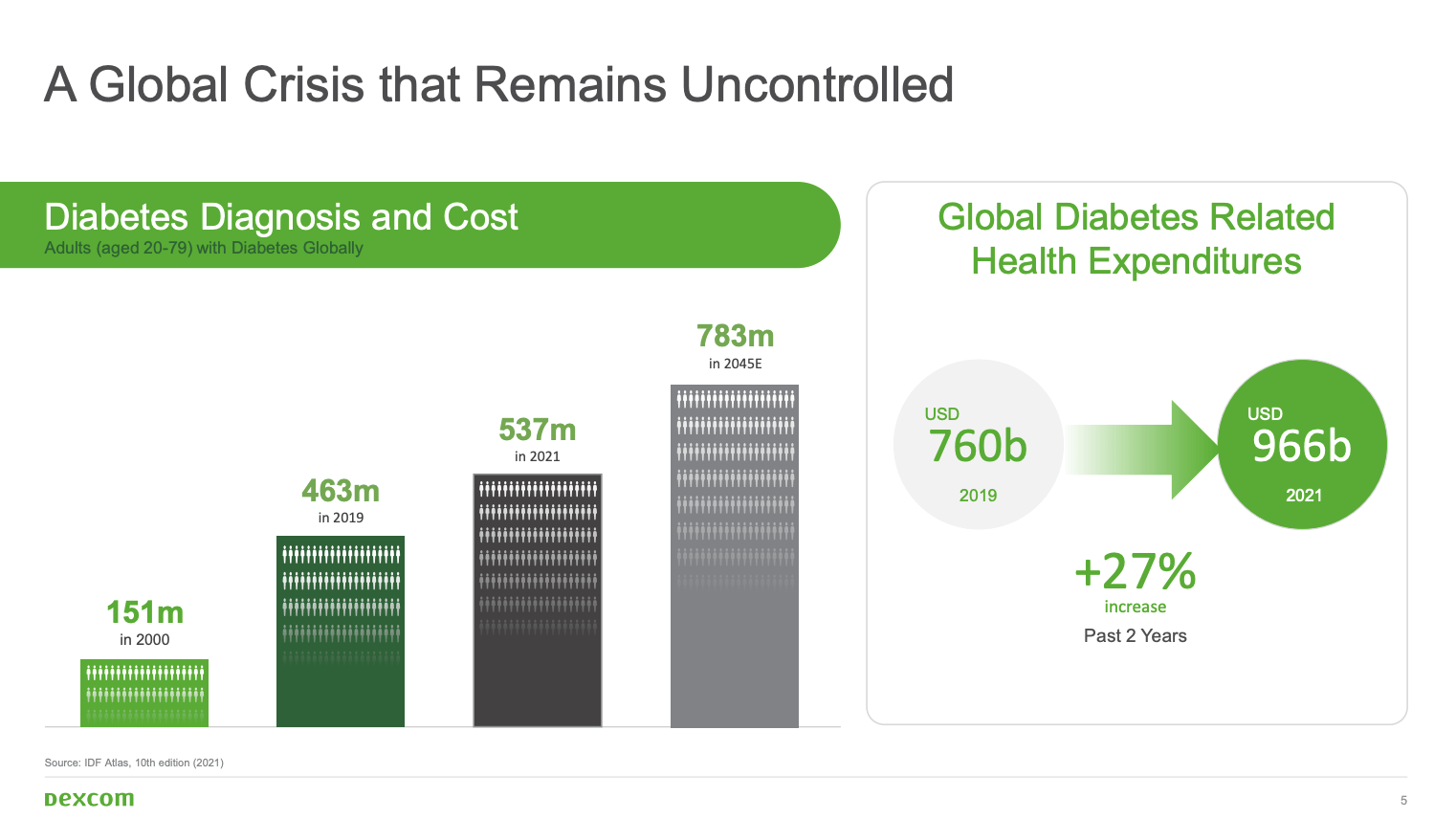

Unfortunately for global health (but very fortunate for DXCM), the company has a rapidly expanding addressable market, with the number of people with diabetes projected to increase significantly.

In 2021, an estimated 537 million adults worldwide had diabetes, with this number expected to reach 783 million by 2045.

{kind=link}

In the United States, diabetes is a major health concern, with over 37 million people affected. The economic burden of diabetes is also significant, with direct and indirect costs totaling billions of dollars.

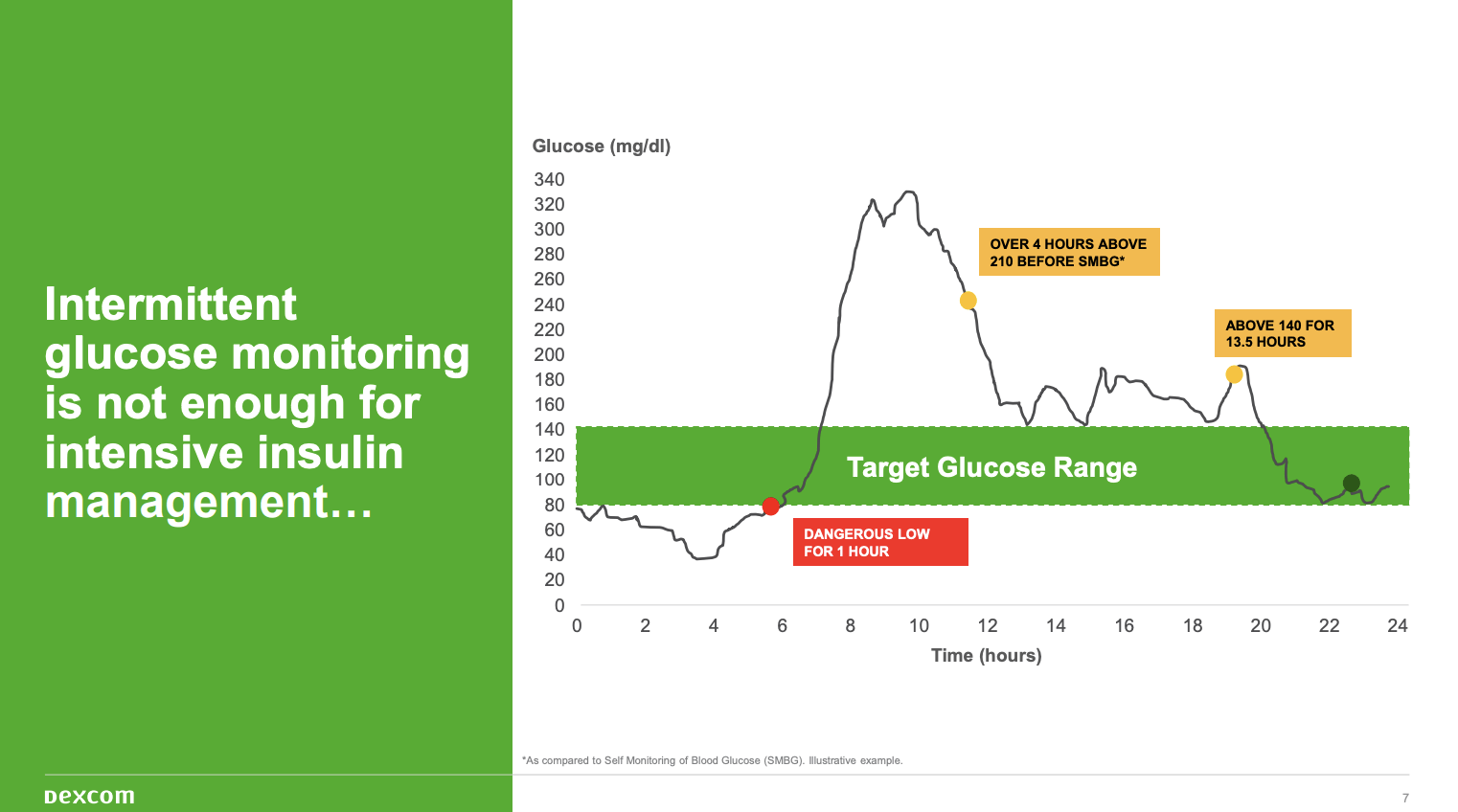

In light of this pandemic, the need for advanced glucose monitoring systems is rising. According to the company, traditional single-point fingerstick devices have limitations, including providing limited information, inconvenience, difficulty of use, and pain.

These devices offer only discrete measurements at specific times, making it challenging to manage blood glucose fluctuations effectively.

The overview below visualizes this.

{kind=link}

DexCom's CGM systems address these limitations by providing continuous and real-time glucose data.

In order to expand its footprint even further, the company is dedicated to continual improvement. Future endeavors include enhanced product performance, intelligent insulin administration, networked platforms with open architecture, and the application of predictive modeling and machine learning for patient insights.

{kind=link}

So far, so good.

One of the issues I have with DexCom is that it relies on a single theme . Looking at ResMed ( RMD ), which relies on demand for breathing support machines and services, we see how dangerous that can be ( I'm bullish on ResMed after its decline).

The good news is that DexCom is holding up quite well despite competing in an industry with some well-diversified giants like Abbott ( ABT ):

The market for glucose monitoring devices is intensely competitive , subject to rapid change and significantly affected by new product introductions and other market activities of industry participants. In selling our current CGM systems, we compete directly with the Diabetes Care division of Abbott Laboratories; Medtronic plc’s Diabetes Group; Roche Diabetes Care, a division of Roche Diagnostics; privately-held LifeScan, Inc.; and Ascensia Diabetes Care , each of which manufactures and markets products for the single-point finger stick device market. Collectively, these companies currently account for the majority of the worldwide sales of self-monitored glucose testing systems . - DexCom 2022 10-K (emphasis added).

Despite these risks, DexCom has found an edge and is poised to generate strong future growth, but more on that in a bit.

It also helps that the company sees no risks related to the weight loss pill.

Weight Loss Pills

During the recent Wells Fargo Securities Healthcare Conference, the company discussed the impact of GLP-1 therapies (weight loss pills) on Continuous Glucose Monitoring).

The company noted that third-party data from Optum's pharmacy base indicated that the prescription of GLP-1 therapies led to an increase in CGM prescriptions.

This suggests that GLP-1 and CGM complement each other rather than being alternatives!

Physicians prefer patients to use CGM to monitor the impact of GLP-1 therapy, which emphasizes the synergy between understanding the body and the therapeutic impact of the drug.

Especially in the early stages of GLP-1, this is key.

As a result, CGM utilization has been on the rise alongside GLP-1 therapy.

DexCom mentioned that a survey showed that 80% of physicians believe CGM is essential to retain benefits from GLP-1 therapy.

The trend is observed across different patient populations, including those transitioning from intensive insulin to basal insulin and non-insulin users. Patients' continuous use of CGM has remained steady over time, indicating its importance in diabetes management.

Where's The Value?

During the aforementioned conference, the company made clear that it anticipates a full year of G7 utilization, enhanced user experience, and DexCom ONE's launch on the G7 form factor in 2024, creating strong competition.

Additionally, the introduction of a non-insulin product targeting type 2 diabetes patients not on insulin presents an opportunity to expand DexCom's reach further.

These factors, combined with DexCom's strategic focus, contribute to a positive outlook for the coming year.

During its 2Q23 earnings call , the company revised its full-year 2023 revenue guidance, raising it to a range of $3.50 to $3.55 billion, which represents a growth rate of 20% to 22% for the year.

With regard to macroeconomic inflation headwinds, DexCom acknowledged pricing headwinds in the current year, with expectations of a gradual reduction in pricing pressures compared to the previous year.

Operating margins are expected to improve with the scaling of the business, higher gross margins, and ongoing optimization efforts. DexCom is on track to meet its long-term margin targets as it progresses toward 65% gross margins in the future.

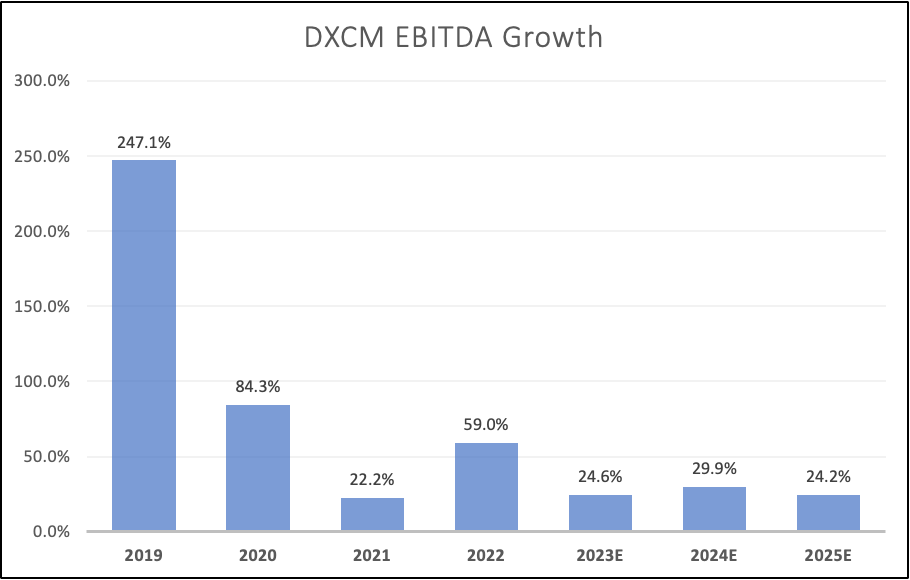

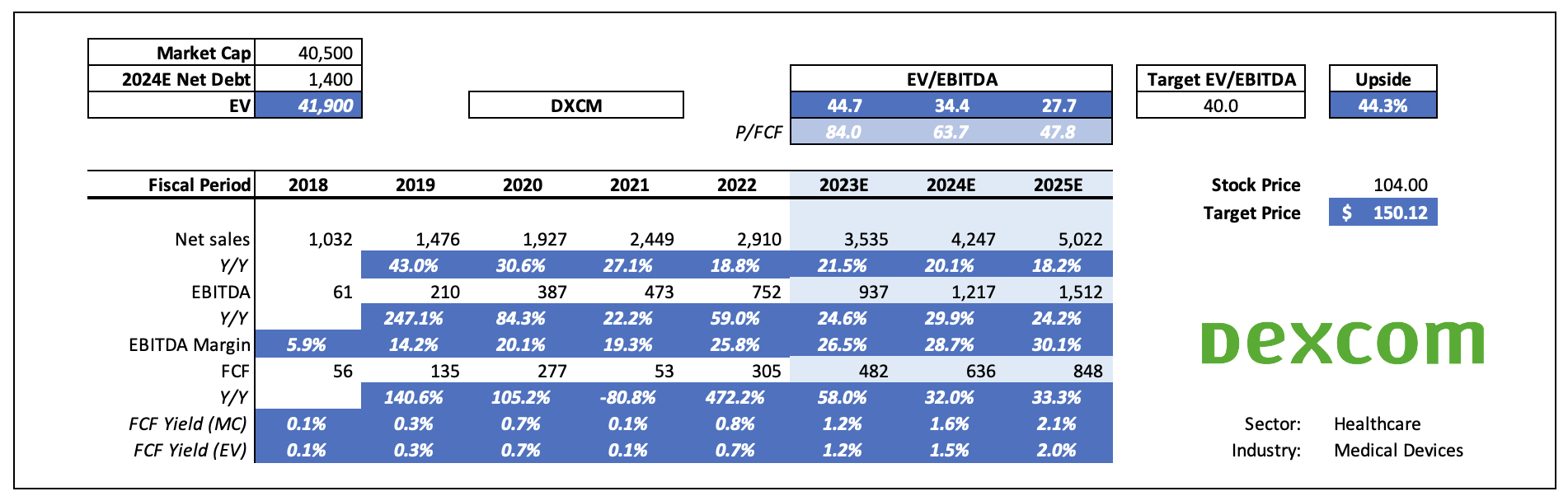

Looking at analyst expectations, the company is not expected to see slower growth in the years ahead. We can assume close to 25% annual EBITDA growth. This is based on close to 20% annual revenue growth and an expected EBITDA margin surge from roughly 14% in 2019 to potentially more than 30% in 2025E.

Leo Nelissen (Based on analyst estimates)

{kind=link}

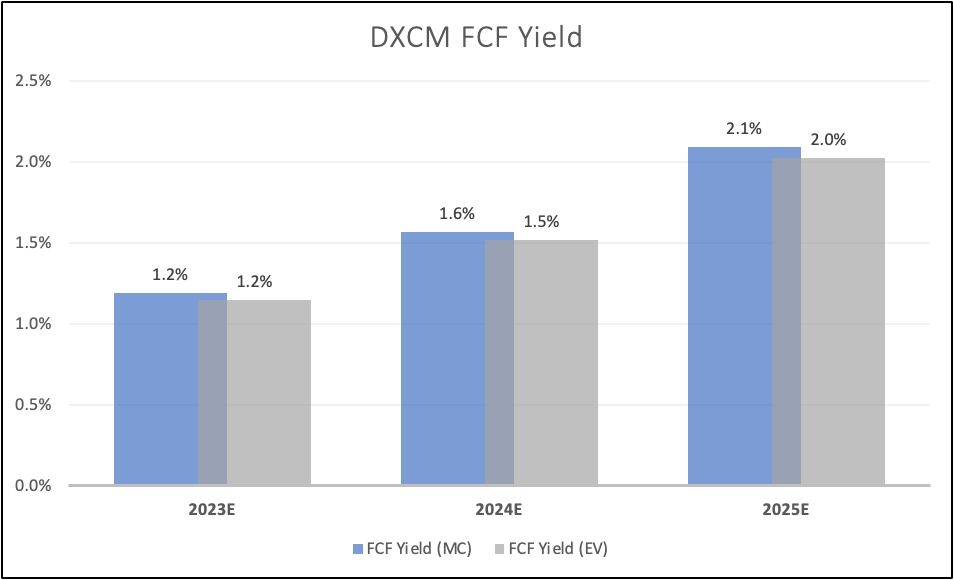

The free cash flow yield is still low. Even in 2025, the company is unlikely to generate much more than 2.1% of its market cap in free cash flow. However, this is normal for a business in the growth stage of DXCM.

It does not pay a dividend and has no focus on buybacks. The company mainly cares about its balance sheet . This year, the company is expected to end up with $1.8 billion in net debt, which is roughly 2.0x expected EBITDA. That number is expected to fall to $1.1 billion in 2025, less than 0.8x expected EBITDA. This indicates a very solid balance sheet.

Leo Nelissen (Based on analyst estimates)

{kind=link}

With regard to the company's valuation, it is trading at 44.7x 2023E EBITDA. Due to high EBITDA growth expectations, that number is expected to drop to 28x EBITDA in 2025.

Leo Nelissen (Based on analyst estimates)

{kind=link}

Now, the question is, what multiple is appropriate? Before 2022, the company used to trade above 80x EBITDA. These times are gone. Average growth rates are now much lower, yet still very high.

If we cut the multiple in half (40x), the company gets a fair value of $150 per share, which is 44% above the current price. If the company maintains >20% annual EBITDA growth in the foreseeable future, that is a more than reasonable assumption.

The current consensus price target is $147.

I expect DXCM to outperform the market on a long-term basis.

However, I would not go overweight. Despite diversification plans, DXCM is highly dependent on CGM. Any major disruption could hurt its stock price.

Takeaway

DexCom, Inc. is a healthcare stock with an impressive track record despite recent challenges in the market. As a leader in continuous glucose monitoring systems, DexCom has a strong foothold in an expanding market driven by a strong uptrend in diabetes cases.

Moreover, the emergence of weight loss pills does not pose a threat but rather complements its products.

DexCom's dedication to innovation, collaborations, and expanding its product portfolio positions it for future growth. The company's positive outlook, as indicated by its revenue guidance and strategic focus, is encouraging for investors.

It is important to note that DexCom's reliance on CGM technology makes it vulnerable to potential disruptions. However, its fair value estimate suggests upside potential, making DXCM an attractive long-term investment.

For further details see:

Why DexCom May Be Up To 40% Undervalued