FANG - Why Diamondback Energy Will Be The Next Permian M&A Target

2023-10-26 14:19:53 ET

Summary

- After considerable M&A in the oil patch, the universe of potential targets within the publicly traded tier-1 Permian operators has dramatically shrunk.

- I predict Diamondback Energy will be the next large publicly-traded M&A target among the big pure-play Permian producers.

- And ConocoPhillips could likely to be the acquirer. COP has reportedly shown interest in CrownRock but will likely avoid over-paying in a bidding war.

- A possible COP/FANG merger would create a Permian powerhouse with more than 1.3 million acres in the play with production of an estimated 1.2 million boe/d.

- EOG Resources has a net cash position of $615 million (i.e. no debt) which means it's ideally positioned for superior dividends and share buybacks.

I predict that Diamondback Energy ( FANG ) will be the next publicly traded tier-1 M&A target in the Permian and that ConocoPhillips ( COP ) will be the likely acquirer. While Reuters reported this morning that COP is readying a bid for CrownRock - a privately held Permian producer - reports have been swirling that Devon Energy ( DVN ), Marathon Oil ( MRO ), and Continental Resources are also interested in purchasing CrownRock. That being the case, I doubt COP will get into a bidding war for CrownRock and will, instead go after Diamondback. Today, I'll explain why.

Investment Thesis

You already know that the oil patch has seen a plethora of big deals since the pandemic hit in 2020 - and even before then with Occidental Petroleum's ( OXY ) purchase of Anadarko. ConocoPhillips was an early mover with its well-timed purchases of Concho Resources and Shell's Permian assets during the pandemic downcycle. Chevron ( CVX ) also was a down-cycle mover and scooped up Noble Energy and PDC Energy, two companies whose primary assets were in the DJ Basin. Exxon ( XOM ) was late to the party, but recently bought Pioneer Resources in a relatively expensive transaction (see Chevron Buys Low, Exxon Buys High ). And just this week, of course, Chevron agreed to buy Hess ( HES ), but primarily for its crown jewel: Its 30% working interest in the prolific Guyana discovery (see CEO John Hess Sells 90-Year Old Hess Corporation To Chevron ).

WSJ

As shown in the graphic above, this flurry of M&A activity leaves only a few top-tier public Permian producers left, and I list them in the table below according to enterprise value ("EV") per Seeking Alpha:

| Market Cap |

| Net debt |

| Occidental Petroleum ((OXY)) |

| $56.0 Billion |

| $20.2 Billion |

| EOG Resources ( EOG ) |

| $75.5 Billion |

| ($615 Million) |

| Devon Energy |

| $30.7 Billion |

| $6.4 Billion |

| Diamondback Energy |

| $29.5 Billion |

| $6.7 Billion |

As you can see, both OXY and EOG would be very large transactions - significantly bigger than either of the recent deals for Pioneer and Hess ((HES)), which only Exxon and Chevron had the ability to engineer.

That leaves Devon and Diamondback, of which FANG is clearly the superior Permian play. And that's the reason COP - already a large-scale tier-1 producer in the Permian - will likely be the buyer.

For long-term energy investors, EOG's pristine balance sheet - which is actually, net cash positive - bodes very well for investors in terms of dividends and share buybacks. That's especially the case given the current relatively strong O&G commodity price environment.

The Midland Basin

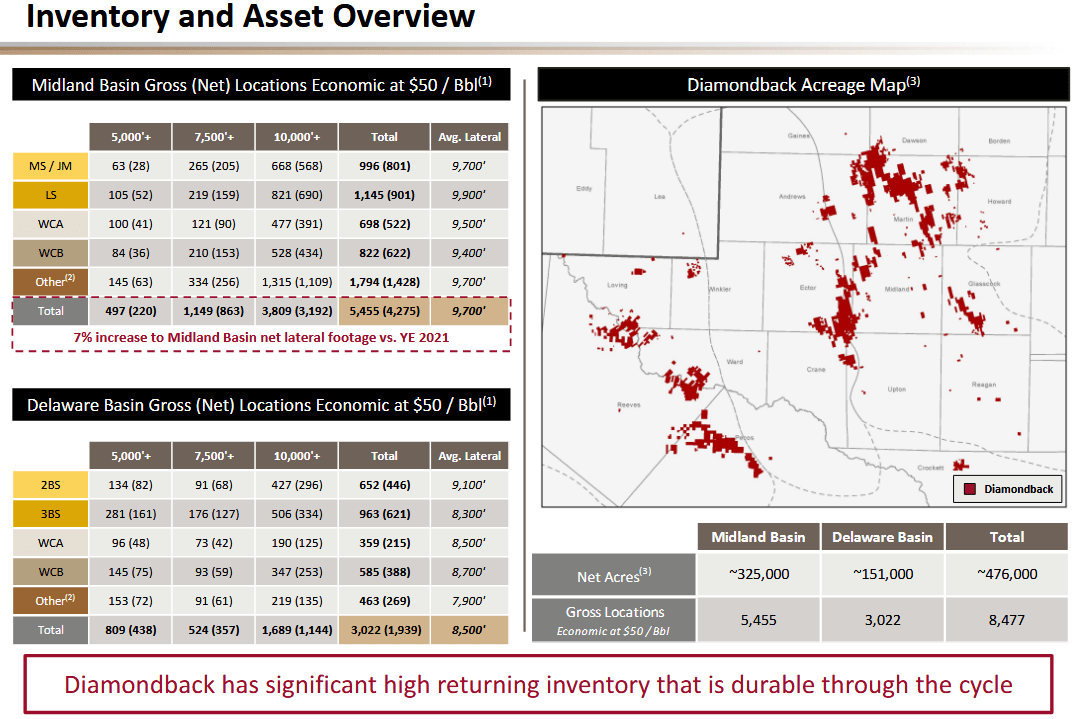

The following graphic, taken from a recent Diamondback presentation , shows the company's footprint in the Permian. FANG has large leaseholds in both the Midland and Delaware Basins:

{kind=link}

As you can see, FANG has a huge inventory of long-lateral drilling locations: 5,400+ in the Midland Basin and 3,000-plus in the Delaware Basin.

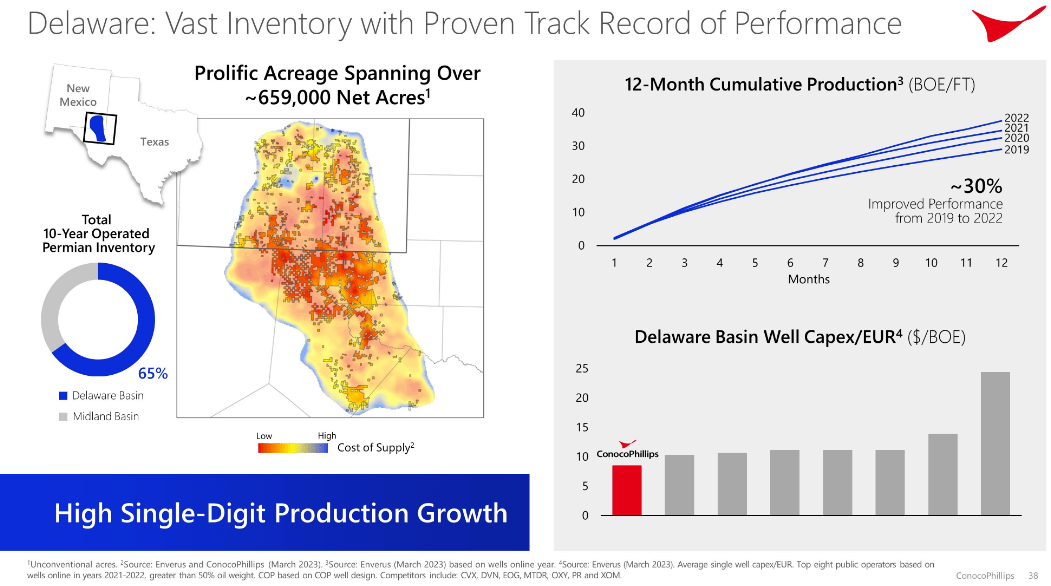

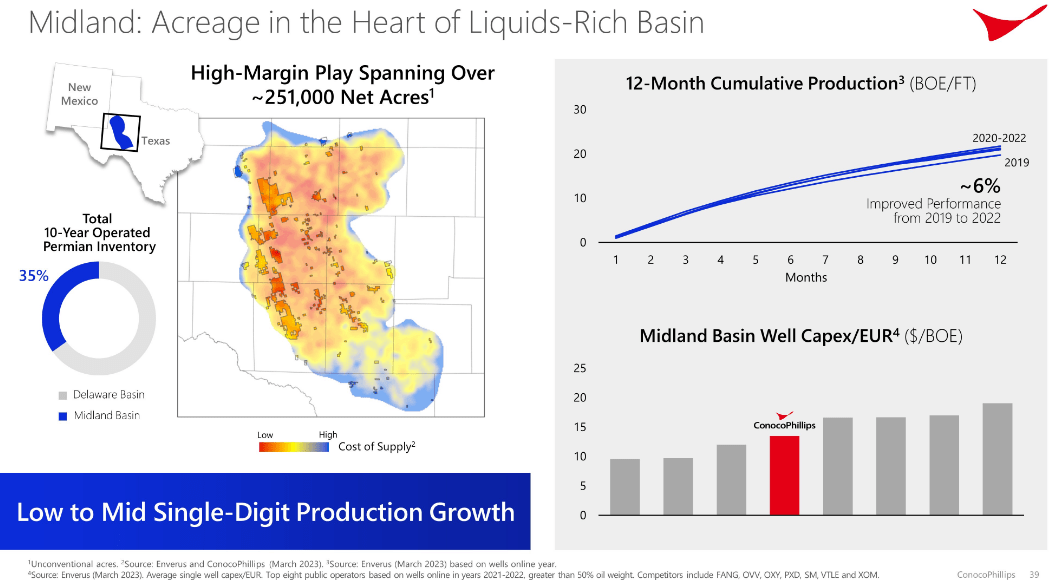

COP, as a result of its M&A activity, also has large and excellent positions in the Permian, as shown from these two slides taken from an April presentation :

{kind=link}

{kind=link}

Together, the two companies would be a Permian powerhouse, with over 1.3 million acres and production, as of Q2:

COP: 709,000 boe/d .

FANG: 449,900 boe/d .

Combined: 1,158,900 boe/d.

Such a combination would vault COP ahead of the Exxon+Pioneer combination in terms of No. 1 Permian production, with more than double OXY's Q2 Permian production of 582,000 boe/d .

The combined companies would also significantly extend the life span of COP's already huge Permian inventory - out to as long as three, or perhaps even four, decades.

Considerations

However, Diamondback would be a large fish for COP to swallow. Note COP's previous two deals, for Concho and Shell's assets, were both under $10 billion ($9.7 billion and $9.2 billion, respectively). However, the free cash flow from these deals is exactly why COP is now big enough to tackle FANG.

COP's current market cap is $144.2 billion, with net debt of $9.6 billion, or an EV about 4.2x that of FANG. So such a deal is definitely doable. And the fact that FANG generates strong free cash flow ($547 million in Q2) and is a very disciplined operator adds to its M&A attractiveness.

Meantime, FANG shareholders would get a much more diversified production profile because COP has significant (and growing ...) exposure to global LNG prices as well as strong Brent-based production in Alaska (see COP Pivots To LNG ).

Risks To The Thesis

I never advise investors to invest on the basis of takeover potential. In this case, the suggested deal could obviously not come to fruition for a variety of reasons, primarily that someone else could make an offer for FANG or that COP could decide to go through with an offer for CrownRock or some other company. In addition, the relatively high interest rate environment means such a deal - like most deals of late - would likely be an all-stock transaction. That being the case, COP CEO Ryan Lance might not want to take on what would be a relatively large and dilutive all-stock transaction.

Summary and Conclusion

Energy investors have likely not seen the end of M&A in the oil patch. However, the number of publicly traded tier-1 Permian operators has shrunk dramatically over the past few years. FANG remains a standout - and if the company does not merge with EOG, it will get squeezed by the bigger players and will likely be the next big tier-1 company to be taken out. COP, with its overlapping footprint in both the Midland and Delaware Basins, would be the most likely acquirer in my opinion.

I'll end with a six-month stock price chart of FANG, which has risen sharply on the combination of improved O&G prices as well as implied takeover potential:

However, note the recent drop in FANG's share price after Chevron announced its decision to buy HES (as did OXY). The thought there being both Exxon and Chevron now have their hands full, taking the two biggest companies out of further M&A transactions (at least for the short term). The biggest company left is obviously ConocoPhillips. And, as I wrote previously on Seeking Alpha, the only rationale for COP CEO Ryan Lance not to reward shareholders with much (much...) higher dividends over the past year or two is because he was keeping his powder dry to make another big acquisition. FANG certainly fits the bill. Yet for FANG shareholders, and like the recent PXD and HES transactions, I doubt COP would make a bid for much more than a 10% premium above where FANG is currently trading.

For further details see:

Why Diamondback Energy Will Be The Next Permian M&A Target