CI - Why Dividend Growth Investors Should Buy Cigna

2024-01-18 18:05:33 ET

Summary

- Cigna Group should not be overlooked despite its short dividend growth streak, as its business model has proven successful and it benefits from aging demographics and growing demand for healthcare plans.

- The company has shown double-digit growth rates in revenue, net income, and earnings-per-share, and has a safe and growing dividend with a low payout ratio.

- Cigna's most recent financial results have exceeded expectations, and it has raised its guidance for FY2023, indicating continued growth and profitability.

Many dividend growth investors focus on the number of years that a company has raised its dividend, believing a longer streak speaks to the dedication to a growing distribution. This is also taken as a sign that a company is fundamentally strong enough to continuously increase its dividend.

However, ignoring names with shorter dividend growth streaks can mean overlooking high-quality companies that have attractive investment characteristics.

One name I believe investors should value the nature of the business over its short dividend growth streak is The Cigna Group ( CI ).

Company Background

Cigna is one of the largest providers of insurance products and related services. The company offers medical, disability, life, and dental insurance through employer- and government-sponsored coverage plans. Cigna also provides individual coverage as well.

Cigna is composed of two businesses, including Evernorth Health Services, which provides pharmacy services and benefit management, and Cigna Healthcare, which offers commercial and government insurance plans. This segment also includes International Health. In total, the company covers more than 164 million people through its plans. The company is valued at close to $90 billion.

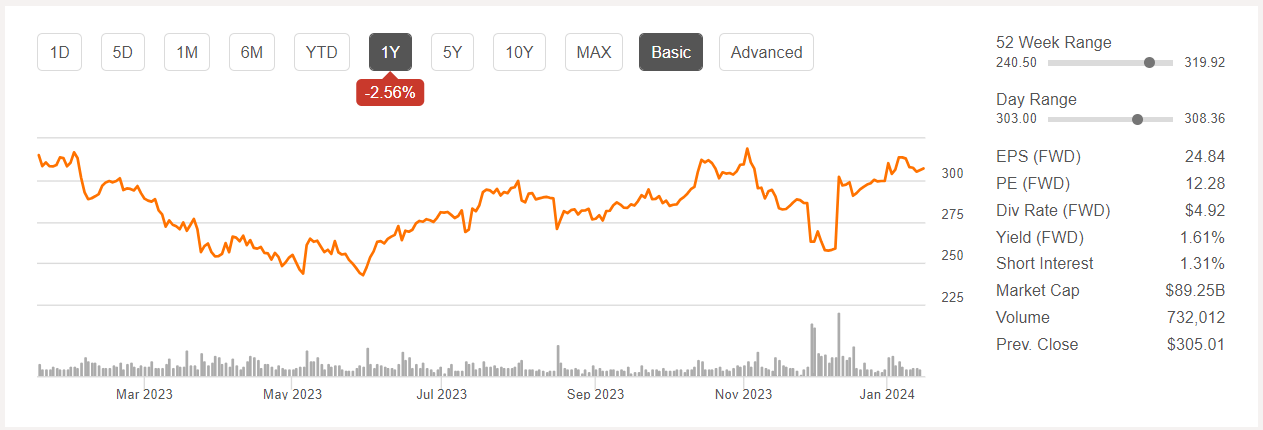

Healthcare has been a difficult place to invest compared to the S&P 500 Index in the last twelve months and Cigna has not escaped unharmed.

Shares of the company are down close to 3% over the last year, but have returned nearly 6% in the last month alone.

{kind=link}

Profit Trends Are Very Encouraging

Though the stock has not changed in value much over the last year, Cigna has a proven track record of growing its profitability at a high clip. The company’s earnings-per-share have a compound annual growth rate ((CAGR)) of 13.1% for the 2013 to 2022 period.

High growth rates have been the norm as the five-year CAGR remains a robust 10.4%. Growth has slowed ever so slightly over the medium-term, but this shows that Cigna’s improvement in its bottom-line has been largely consistent over the years.

These growth rates also do not tell the whole story, as the company has issued 26 million shares of stock over the last decade.

Looking at just net income gives us a clearer picture of the company’s true growth. Cigna’s net income has a CAGR of 16.3% for the 2013 to 2022 period. Even more impressive is that the growth rate is more than 20% when looking at just the last five years.

The increase in share count hides the fact that not only is Cigna continuing to grow at a high rate, but that the growth rate is accelerating.

{kind=link}

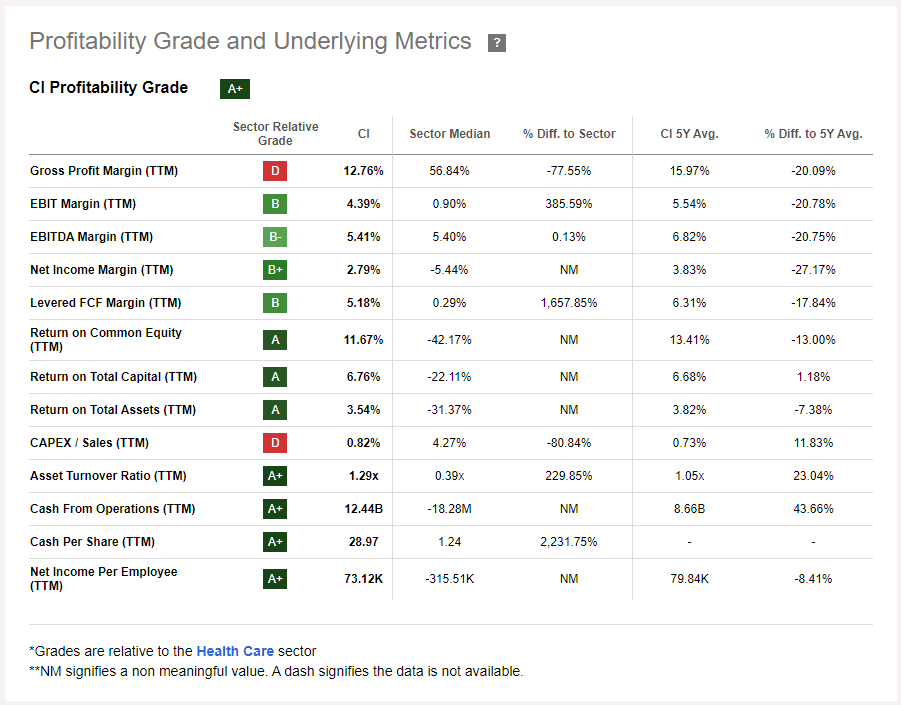

Cigna scores very well on most metrics rated by Seeking Alpha Quant, demonstrating the overall soundness of the business model and its ability to generate profit.

Revenue growth has been outstanding as well, with top-line results improving 30% and 18.7% over the past five and 10 years, respectively.

Recent results provide further evidence of a company flexing its business muscles. Cigna reported third quarter results on November 2 nd , 2023, with results coming in ahead of what the market had anticipated. Revenue grew 8.2% to $49 billion, which was $800 million more than expected, while adjusted earnings-per-share of $6.77 compared to $6.04 in the prior year and was $0.09 above estimates.

Revenue for Evernorth Health Services, the largest contributor to results, grew 8.1% to $38.6 billion, due to strength in its management solutions as well as specialty and care delivery businesses. Revenue for Cigna Healthcare improved 14.2% to $12.8 billion due to gains in customers and increases in rates related to higher medical costs. The medical cost ratio, a measure of efficiency, improved 30 basis points to 80.5%, showing that Cigna is taking in far more premiums than the medical expenses it is paying.

Following quarterly results, Cigna raised its guidance for 2023, with adjusted earnings-per-share totaling at least $24.75. This would represent a 6.4% increase from 2022. Revenue is projected to grow 6.7% to at least $192 billion.

Risks to Investment Thesis

While Cigna has done a remarkable job of growing both revenue, net income, and earnings-per-share, the company’s profit margin has not kept up. The last decade has seen a 90 basis point decline in the net profit margin to 3.7%, which is why top-line gains outpace bottom-line results.

If revenue growth continues to move at an upwardly pace, Cigna should enjoy high net income and earnings growth.

Assisting in this will be the addition of members to the company’s coverage plans. Total customer memberships did decrease 8% to 164.2 million in the most recent quarter. This was largely due to a non-renewal of a supplement behavioral care agreement with New York Life, but this was not a material impact to the business performance during the period. On the plus side, pharmacy customers increased 3.7% to 98.3 million while total medical customers grew 9.2% to 19.6 million.

Cigna continues to add customers in its most important areas of its business, pharmacy and medical. A slowdown in either space could materially impact results, especially since profit margin has shrunk.

That said, the need for healthcare plans remains high, driven by an aging population that will cause the need for services to rise. Today, the U.S. population is as old as it has ever been, something that is expected to continue as people live longer.

It is projected that the number of Americans age 65 and older will increase to 82 million by 2050. This will represent nearly a quarter of the total population. The need for services, especially in the areas of pharmacy and specialty care, will be higher as this age group becomes a larger portion of the total population. This should give Cigna, already one of the largest providers of insurance plans, an avenue to add new customers.

And after several years of uncertainty immediately following its passage, the Affordable Care Act is almost certainly here to stay, which should provide more customers for Cigna. For example, it was announced at the end of the year that more than 20 million people had signed up for plans in health insurance exchanges during the latest enrollment period, the most since the implementation of the law. Of these, 3.7 million people were new to the exchanges.

The company can also supplement its growth through the use of acquisitions. One good example of this was Cigna’s $54 billion purchase of Express Scripts in 2018, which added one of the largest pharmacy benefit and insurance plan managers in the U.S. to the company. More recently, Cigna had been rumored to merge with rival health insurance Humana Inc. ( HUM ), but the deal fell apart amid a disagreement on financial terms. Even so, this shows that Cigna is not shy about attempting to purchase other companies that can help bolster growth.

Shares are also trading at 12.5 times expected earnings-per-share, a very reasonable valuation considering the performance of Cigna’s business.

Dividend Analysis

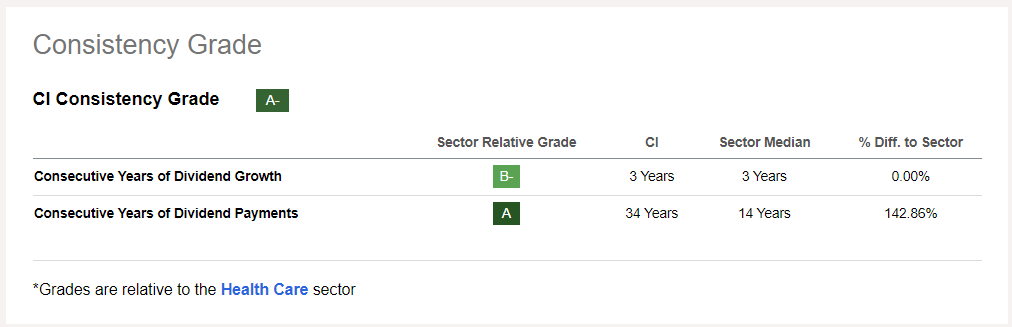

A business that should continue to grow can also deliver capital returns to its shareholders. Admittedly, paying dividends has been something of an afterthought for Cigna up until recently. While the company has distributed a dividend for more than three decades, Cigna did hold its annual dividend constant at $0.04 per share from 2008 through 2020.

That changed in 2021, when the company’s annualized dividend was raised to $4.00, 100 times what it had been for more than a decade.

Cigna followed that up with a 12% raise in 2022 and a 9.6% increase last year. The company has not yet announced the new increase, but will likely do so near the beginning of February as it has done the past few years.

{kind=link}

While Cigna’s growth streak is very much in its infancy, the company still receives high marks for its dividend.

{kind=link}

First off, the company has a very safe dividend. Even after a massive increase in the size of the dividend, the projected payout ratio for 2023 is just 20%. This is very much in-line with the company’s payout ratios for 2021 and 2022.

The dividend yield of 1.6% is roughly the same as the average yield for the S&P 500 Index, but the extremely low payout ratio probably means that future increases can be expected.

There are not yet enough data points to determine the size of the raise, but the company appears to have settled on a target payout ratio of 20% based on the past three years. This could mean that future increases are more or less tied to earnings growth.

Final Thoughts

Companies with multiple decades of dividend growth tend to get much of the publicity among dividend growth investors. This is appropriate as these companies have demonstrated that they are serious about raising their distributions over long periods of time regardless of the state of the economy. Their business models can support growth even in difficult operating environments.

Cigna is one name I feel investors should not overlook simply due to the length of its dividend growth streak. The company’s business model has proven to work, particularly over the medium-term as revenue, net income, and earnings-per-share have all shown double-digit growth rates that are near or above long-term trends.

The company also benefits from aging demographics and the growing demand for healthcare plans in the U.S.

While the growth streak is short and the yield is just average, the size of the raises over the past three years is impressive. The dividend should be safe as well given that the payout ratio remains very low.

A safe and growing dividend supported by excellent business results should be enough to put Cigna on the dividend growth investor’s watchlist.

For further details see:

Why Dividend Growth Investors Should Buy Cigna