FAF - Why First American Financial Is Worth A Nibble At Current Prices

2023-10-20 08:10:00 ET

Summary

- First American Financial has seen a material share price downturn over the past 2 months.

- While it faces near-term headwinds, the market appears to have priced in those risks.

- With a well-covered and growing dividend as well as potential for upside in the business next year, long-term investors may find value at the current price.

The housing market hasn't been an easy spot to be in over the past 12 months, considering headwinds and pressure from higher interest rates. Recent concerns around a 'higher for longer' interest rate environment has only added to that pressure.

This brings me to one of the leading title companies, First American Financial (FAF), which I last covered here back in January, noting its gaining of market share in the home purchase and commercial segments, while expanding its mortgage sub-servicing unit.

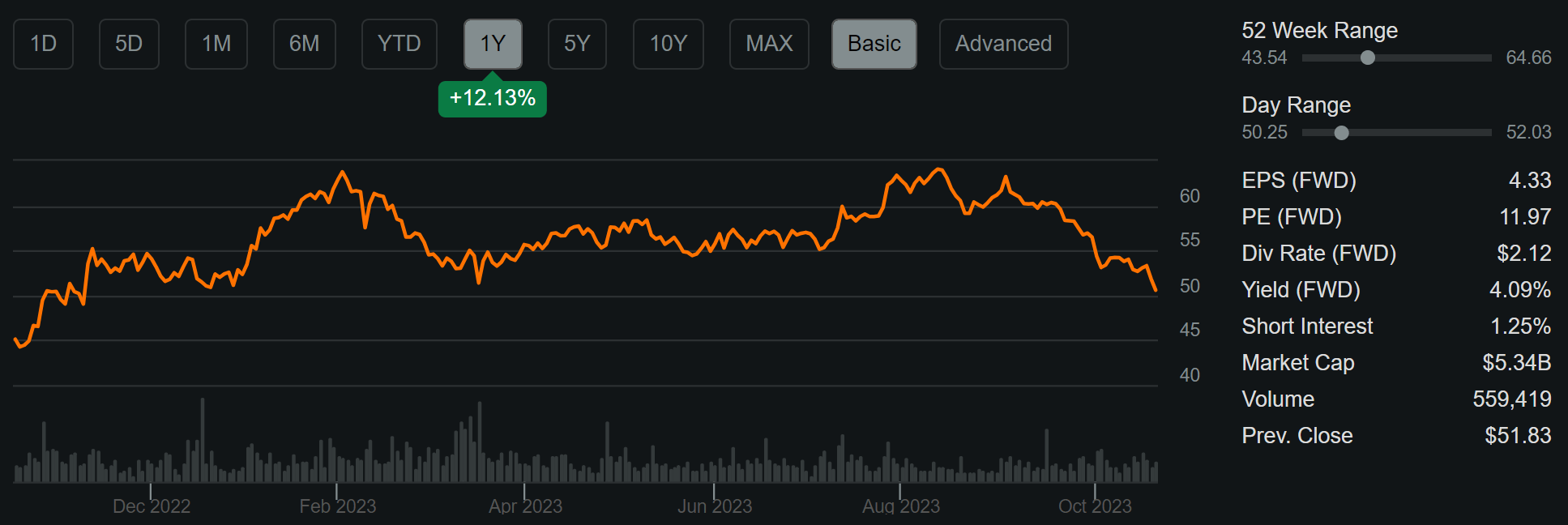

FAF's share price has declined since my last piece, as a higher for longer rate environment has spooked investors, with much of the decline happening over the past 2 months. However, its performance over the past 12 months has been rather resilient, as underlying business resiliency have overshadowed the initial shock of higher rates last year, as shown below.

In this piece, I discuss why FAF is worth nibbling on at current prices while the market has priced in plenty of risks, so let's get started!

{kind=link}

Why FAF?

First American Financial is one of the oldest companies in the U.S., having been in existence for 130 years. It is a premier provider of title, settlement and risk solutions for real estate transactions, which is often the biggest financial transaction in an individual's lifetime.

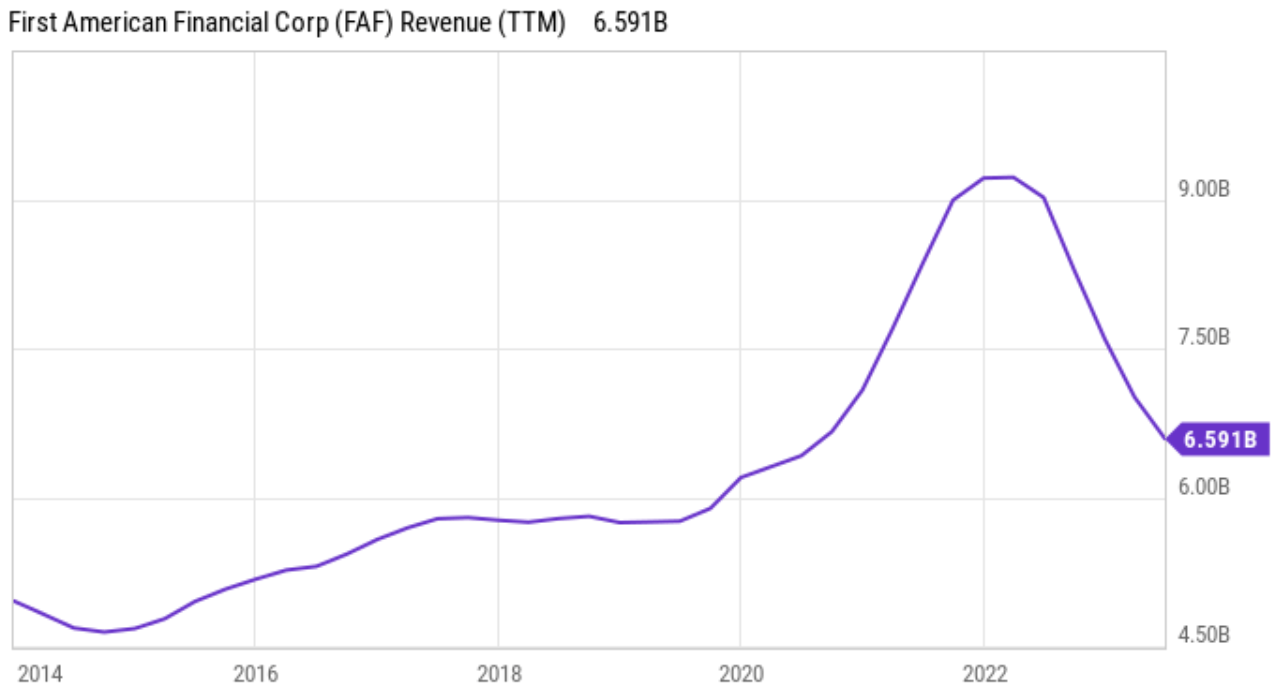

FAF also has a global presence, operating in 8 countries, and has a 25% market share in its bread and butter title business. While it may be easy to write-off FAF in the current higher interest rate environment. The fact of the matter remains that FAF's revenue over the trailing 12 reported months amidst higher interest rates is higher than where it was in 2020 and pre-pandemic times. As shown below, revenue has seen a normalization after seeing outsized gains in the 2021 to early 2022 timeframe due to pandemic-era low interest rates, stimulus payments, and pent-up savings from consumers pulling back on travel and entertainment spend during that time.

{kind=link}

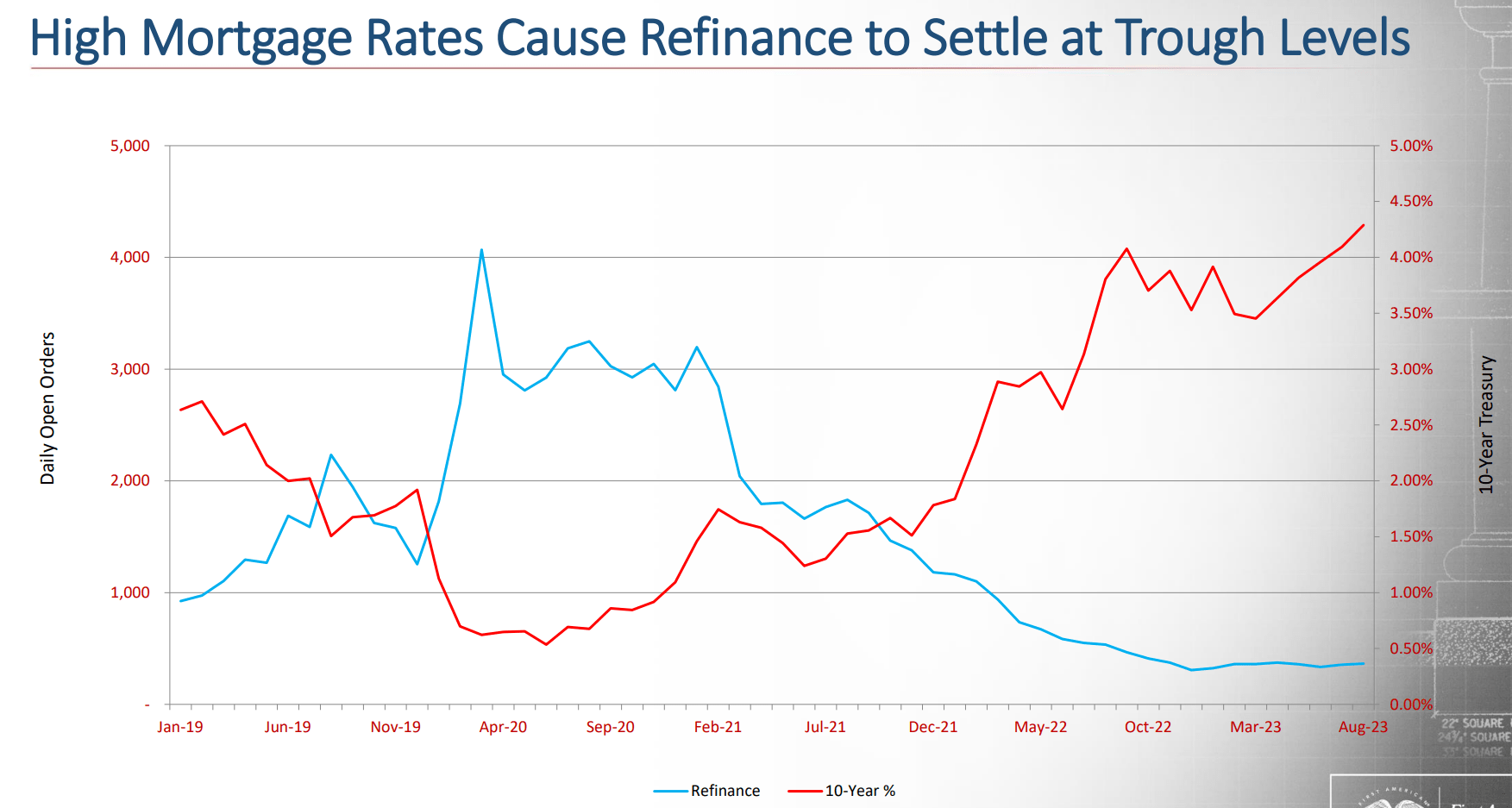

Another key underlying reason for FAF's strong uptick and subsequent downturn in revenue was historic refinancing activity that took place during the peak years (as shown above) due to historically low rates. As one can imagine, refinancing activity has an inverse relationship with interest rates, and the present refinancing activity (through August) remains muted since flatlining earlier this year.

{kind=link}

However, refinancing activity is just a part of the story, as FAF generates revenue from purchase transactions as well. As shown below, purchase originations across the industry in the U.S. is expected to land in between where it was in 2018 and 2019, and this is due in part to elevated home prices since then.

{kind=link}

Home prices matter for title insurers like FAF, since their fees are based on a percentage of the total transaction. In this respect, home prices are expected to remain elevated due to low housing inventory available for purchase. This makes sense as many would-be sellers are not listing their homes for sale due to them being 'locked in' to low interest rates, since selling their home would require buying a new home with a far higher mortgage rate.

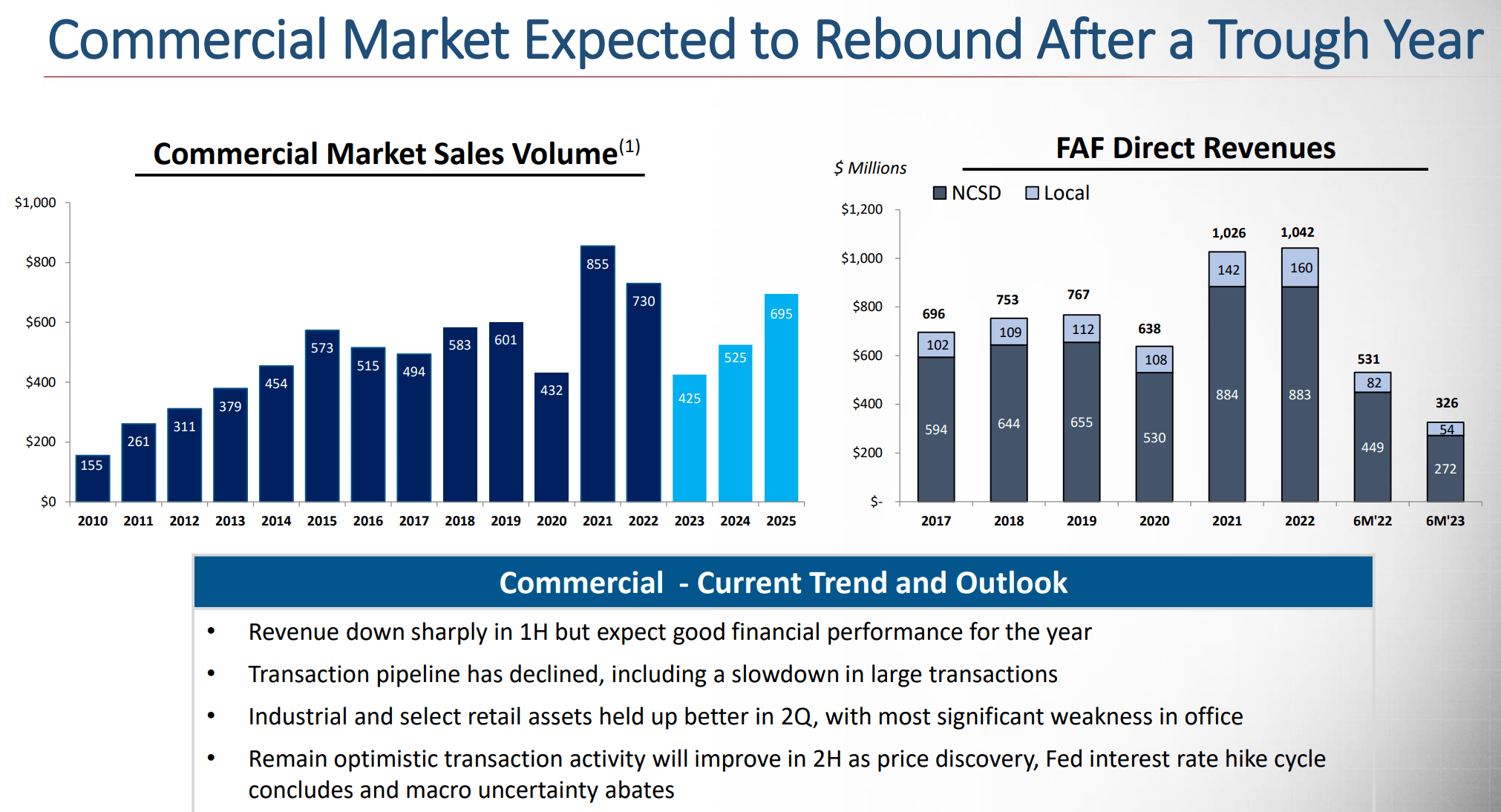

Near-term headwinds for FAF due to lower real estate transaction volumes are fairly well known at this point, with revenue falling by 20% YoY and net income per share falling from $2.04 in the prior year period to $1.35 during the second quarter. Plus, the commercial market remains fairly weak compared to the prior two years.

However, activity is expected to pick up in the next 2 years as the market digests the new reality of higher rates. This is according to the Urban and Land Institute, which shows estimated commercial market sales volume picking up in the 2024-2025 timeframe.

{kind=link}

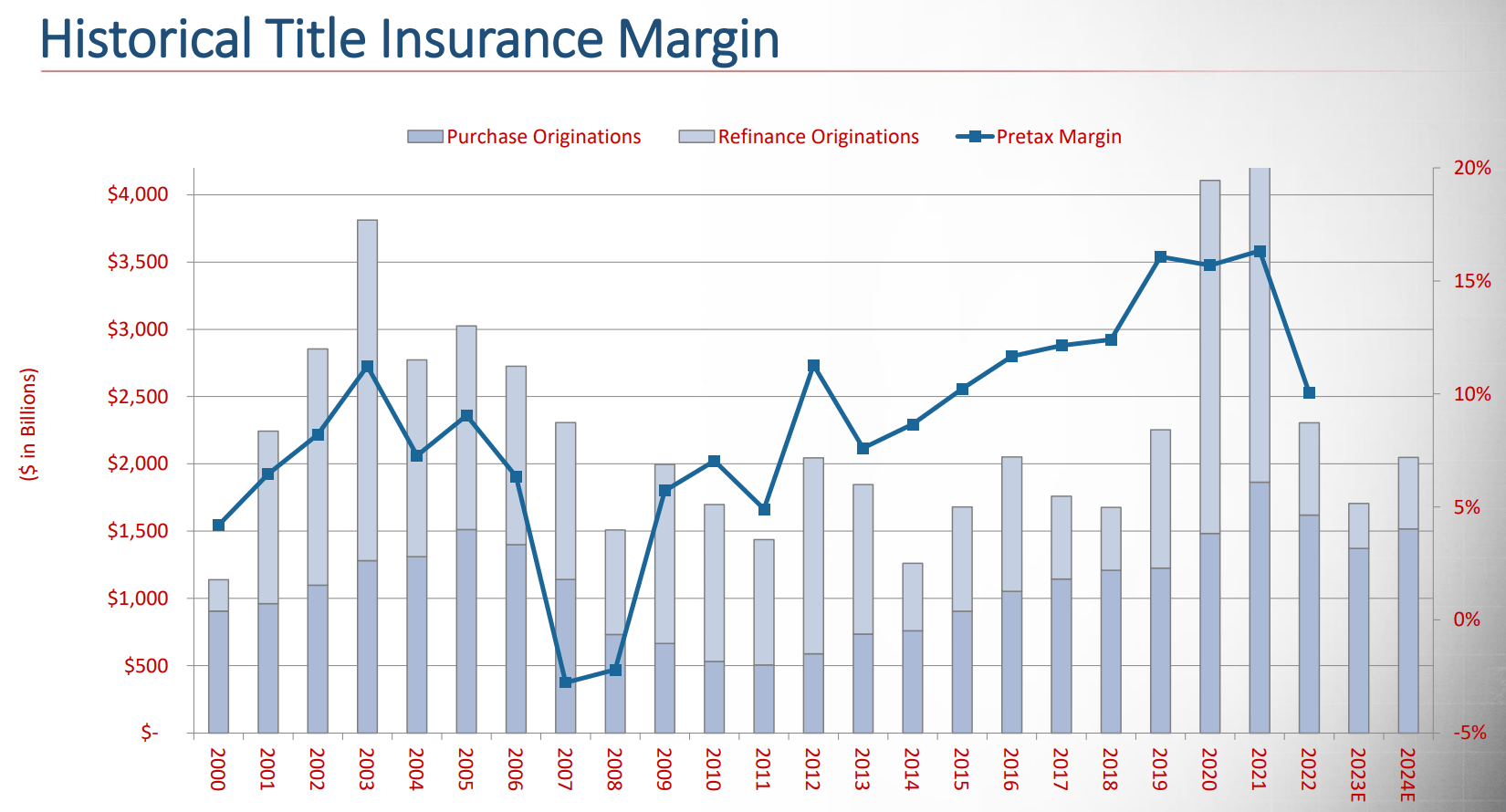

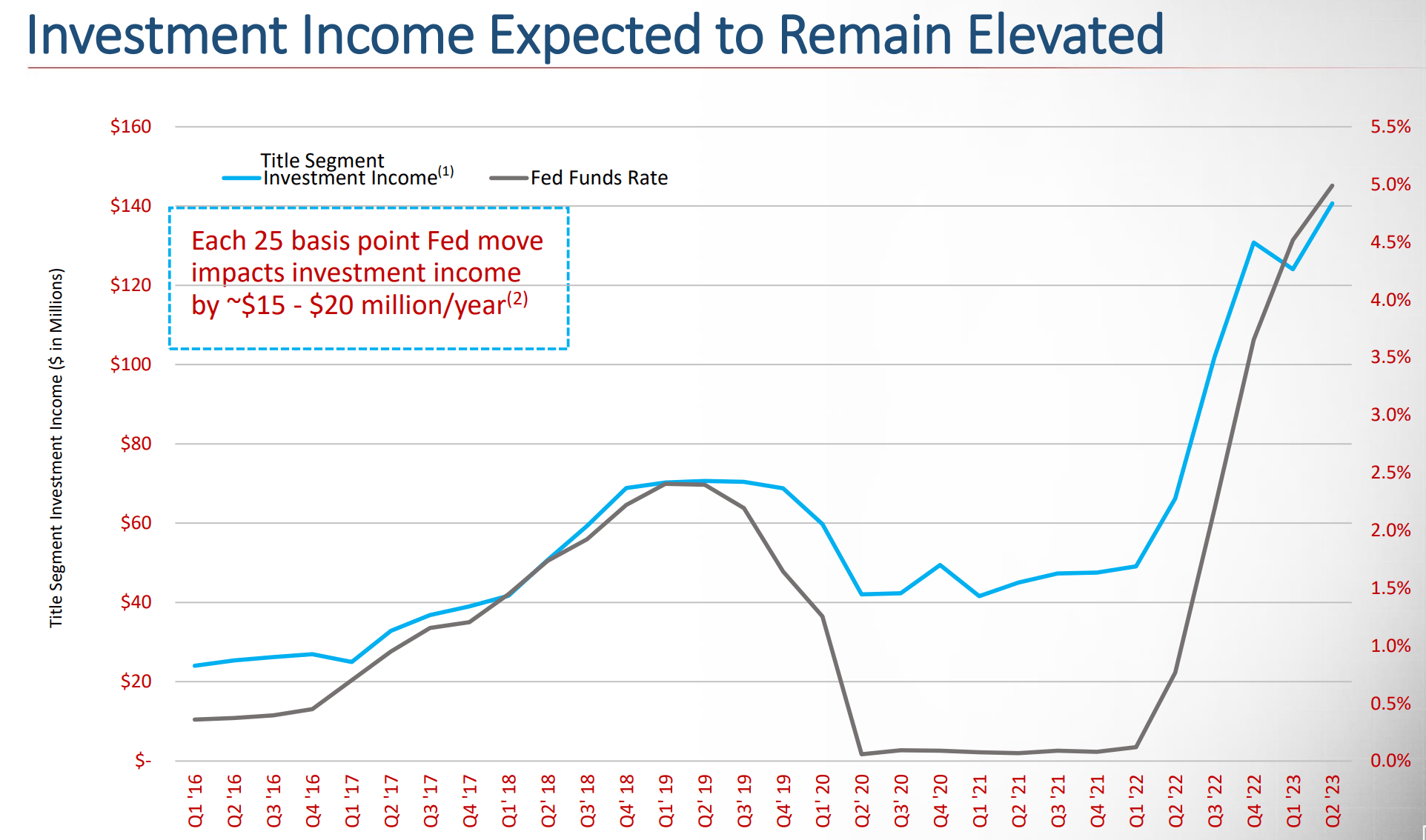

Looking ahead to Q3 results and beyond, I would expect FAF's business to continue to be challenged in the near term, considering the elevated rate environment. However, there is room for optimism as the market largely anticipates that the Fed won't raise rates again at least for the remainder of this year, and this could stabilize the housing market. In addition, like any insurance company, FAF invests its title premiums and benefits from higher rates in this segment of its business. As shown below, each 25 bps increase in rates pads FAF's investment income by $15 to $20 million per year.

{kind=link}

Meanwhile, FAF carries a BBB- investment grade rated balance sheet with a debt to capital ratio of 29%. Management is also returning excess cash to shareholders. As shown below, FAF has taken advantage of its share price downturn and has reduced its share count by 7% over the past 3 years. At the current price of $50.58 with a forward PE of 11.7, FAF is getting an 8.5% earnings yield on every dollar spent on share buybacks.

FAF Outstanding Shares (Seeking Alpha)

{kind=link}

At the same time, FAF continues to grow its dividend, and it's expected by land 2023 with a $2.10 per share annualized dividend rate (above the $2.06 per share paid out last year) at a safe 49% payout ratio. FAF's forward yield currently sits at a respectable 4.2%, which sits well above that of the S&P 500 ( SPY ) and a number of consumer staples companies, which are also not immune to higher interest rates.

Based on an NPV analysis, I arrive at a fair value of $69.28. This is based on a conservative long-term growth rate of 3%, which takes into account FAF's near-term headwinds, as well as a 3% discount rate, which sits above the Fed's long-term inflation target rate, taking into consideration the cyclicality of the business.

{kind=link}

Investor Takeaway

FAF hasn't been in an easy spot over the past 12+ months as higher interest rates and lower transaction volumes have weighed on the stock. However, it appears that the market has already priced in many of those risks, as a 'higher for longer' interest rate environment is fairly well known by now. Looking ahead, a stabilizing rate environment combined with share buybacks and higher investment earnings could be tailwinds for the business.

Risks to the thesis include more interest rate hikes and hard landing, which could materially impact the housing market and drive down business for FAF. With plenty of uncertainties in the economy, I would expect more share price volatility through the remainder of the year. As such, risk-adverse investors may want to wait for clearer skies before diving into the stock, while long-term investors who don't mind volatility may want to nibble at current prices.

For further details see:

Why First American Financial Is Worth A Nibble At Current Prices