CUR - Why Gold Is A Bad Investment

2023-10-26 14:19:56 ET

Summary

- In this article, we explore popular arguments both in favour of and against gold as an investment. Crucially, we shall attempt to debunk some of the myths surrounding gold.

- The evidence of gold as an effective hedge against inflation in the short-to-medium term is mixed. While there are much better alternatives to gold for portfolio diversification.

- Given our view that neither inflation nor geopolitical risks present a serious threat to the global economy, for now, we see little reason to be bullish on gold.

- Instead, we believe that the rally in gold may be overdone and that we are more likely to see prices fall as the economic and geopolitical outlook gradually improves.

The age-old debate over whether gold is a worthy investment has continued to occupy the minds of investors even decades after the Gold Standard was abandoned in 1971. The debate is a rather extensive one, encompassing multiple aspects of gold as a medium of exchange, a store of value, a hedge against inflation, a safeguard against geopolitical risks, an asset class for portfolio diversification, as well as its relative attractiveness versus other asset classes.

As the investment environment enters a new age marked by monetary policy normalization and escalating geopolitical risks, it may be worthwhile to reassess gold's potential as an investment not just on its own but also within the context of a diversified portfolio.

In this article, we shall explore popular arguments both in favour of and against gold as an investment. Crucially, we shall attempt to debunk some of the myths surrounding gold, and argue why we think gold is likely to underperform other major asset classes over the next few years. Coincidentally, gold prices are approaching historic all-time highs and we view this as an opportunity to initiate our bearish view on gold.

Investing Versus Speculating In Gold

Before we begin, it is crucial that we first separate investing from speculation. While it is quite common to see investors actively managing their exposure to gold in response to changing macroeconomic fundamentals, some firmly believe that gold deserves a permanent allocation within their portfolios.

Generally, we identify an investor as someone who intends to maintain a strategic allocation to gold over the entire investment horizon. This means that gold is considered a permanent allocation within their portfolios over time, while active tactical positioning to moderately increase/reduce exposure to gold is acceptable for enhancing returns.

In contrast, we associate speculation with the intention to profit from short-term price action or momentum in gold prices. Another tell-tale sign of speculative behaviour is "all-or-nothing" trades, where a position in gold is bought and sold in its entirety, usually in an attempt to profit from a temporary view on prices. Below is a table summarising other key differences between the two approaches.

U.S. Global Investors, Forbes

Why People Think Gold Is A Good Investment

Let us first explore the reasons why gold may be a good investment. Arguments that are in favour of investing in gold typically focus on its ability to provide some form of risk mitigation rather than its ability to generate returns over time. These risks include the loss of purchasing power (inflation), fluctuations in the value of other asset classes (diversification), and the potential loss of accumulated wealth as a consequence of war (geopolitics).

A Hedge Against Inflation

One of the most popular arguments in favour of investing in gold is that the value of the precious metal has held up well over time relative to inflation.

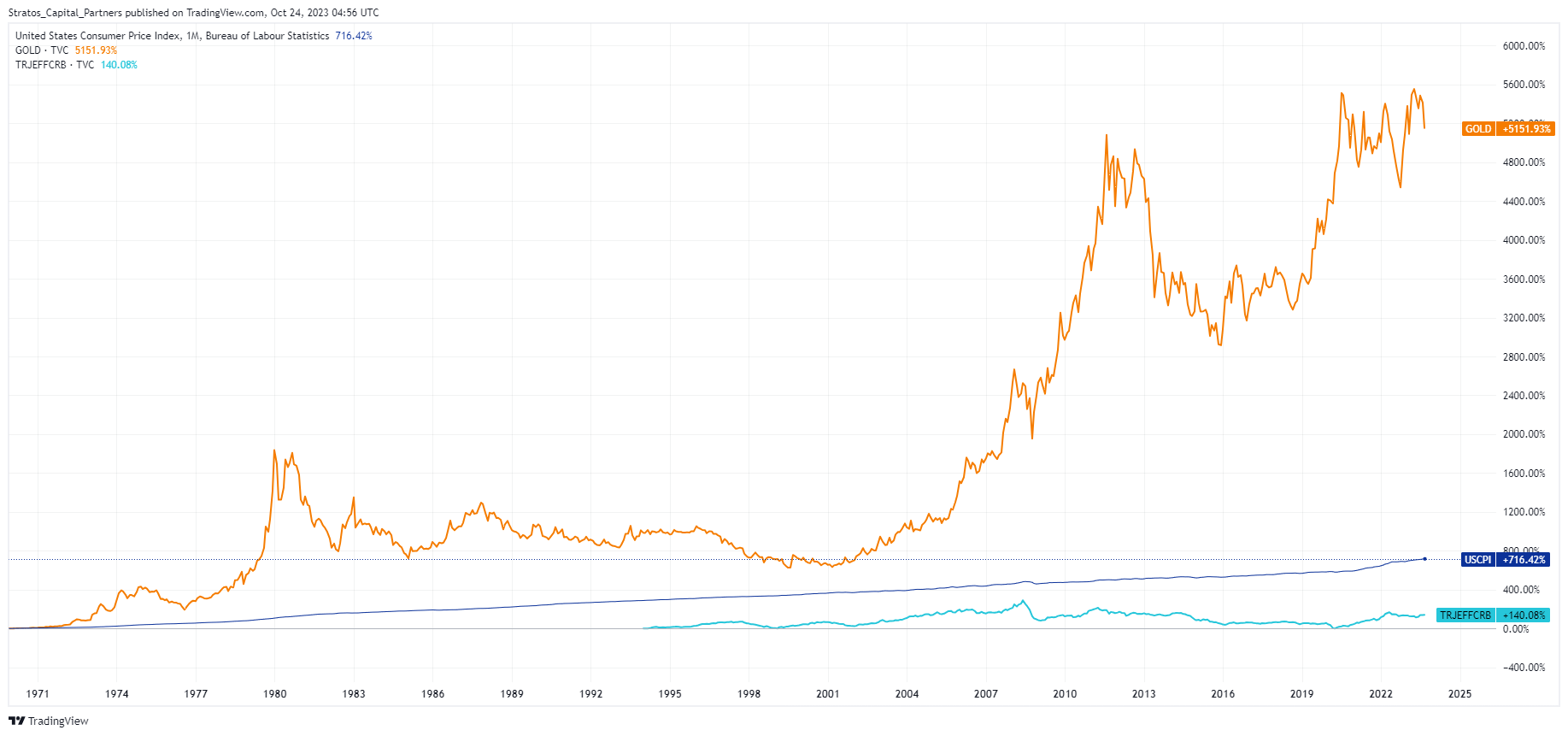

The chart below shows how gold in U.S. dollar terms has performed versus the US CPI Index since 1970. Gold has gained by a staggering 5,151% to date, while the US CPI Index has risen by only 716%. We have also added data on the Thomson Reuters/CoreCommodity CRB Inde x since 1994, which shows that broader commodities prices have risen by a modest 140% to date.

{kind=link}

Clearly, gold has demonstrated its value in outperforming inflation over long periods of time.

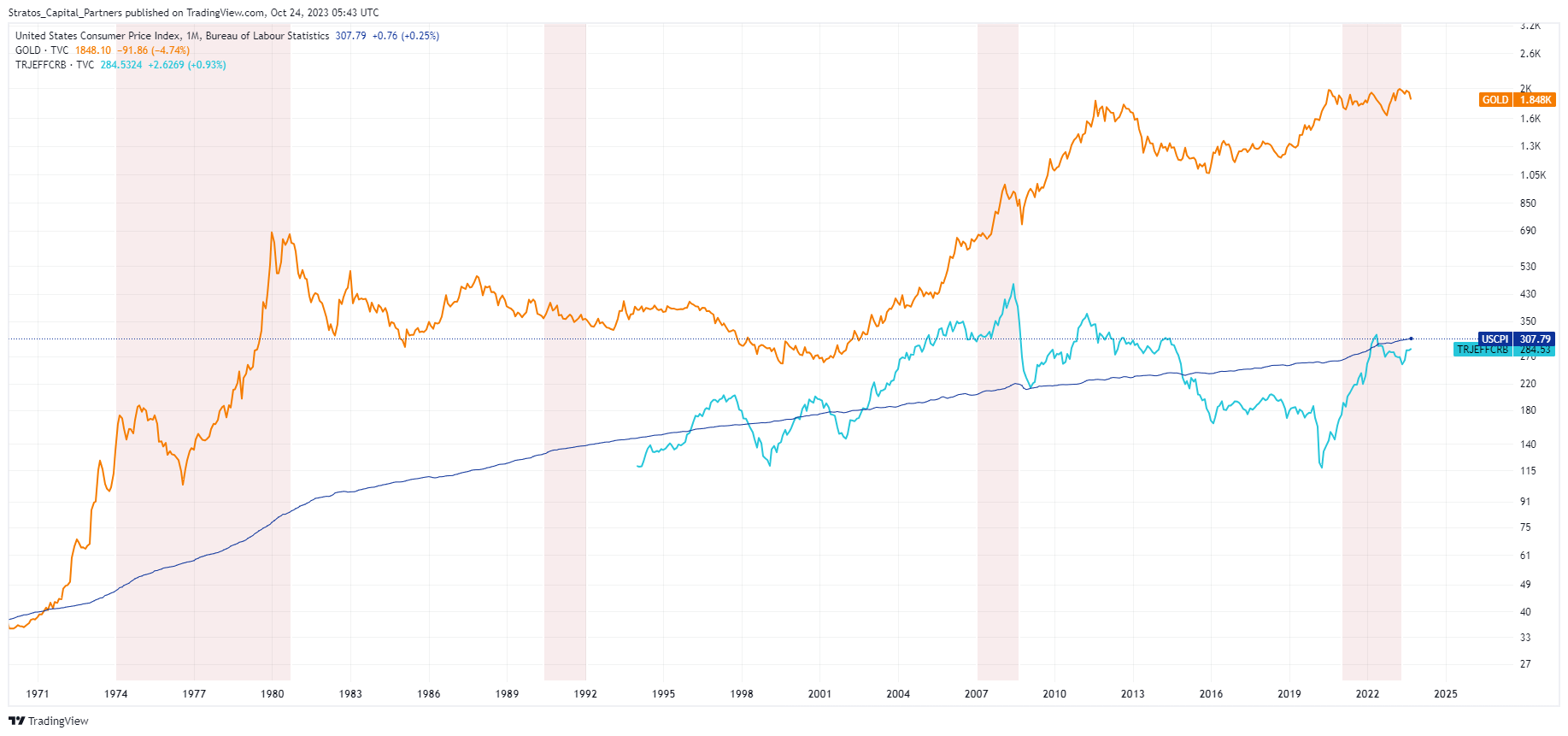

In the next chart below we have highlighted periods in which the US economy experienced high inflation (specifically when US CPI is above 5%). We plotted the same set of data on a logarithmic scale to better visualise the magnitude of changes during those periods. These include the stagflationary era of the 1970-1980 which saw inflation peak at 14% in 1980, and the most recent episode when inflation peaked at 9.1% in 2022.

{kind=link}

Here, the evidence of gold as an effective hedge against inflation in the short-to-medium term is mixed. As we can see, gold prices actually declined during the period between 1990 to 1992 when inflation averaged around 6%, and gold has seen only modest gains from 2021 to date.

Overall, it seems to us that gold's widely touted quality of being an effective hedge against inflation is nothing more than a myth. We can certainly make the argument that gold prices have simply risen over time, and therefore gold has historically outperformed inflation by a wide margin. But this says nothing about gold being endowed with certain qualities that would make it especially effective as a hedge against inflation. The evidence we have presented also supports our long-held suspicions that tactical advice encouraging investors to invest in gold as a way to manage inflation risk is nothing more than speculation.

For Portfolio Diversification

Even if gold isn't a reliable hedge against inflation, many analysts argue that investing in gold will nonetheless provide some form of portfolio diversification. This is theoretically true as long as returns on gold are not highly correlated to other asset classes. In practice, however, investors are subjected to various trade-offs and will need to balance between other factors that impact the overall performance of a portfolio besides diversification.

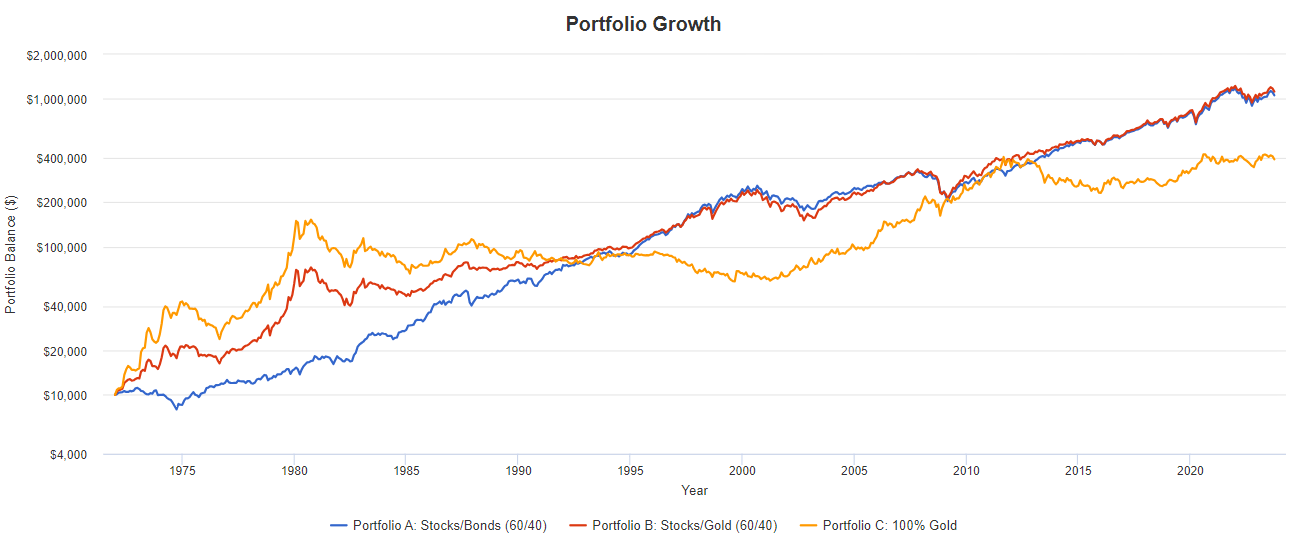

To better visualise these trade-offs, we shall perform a backtest (portfoliovisualizer.com) and compare the historical performance of three different portfolios:

- Portfolio A – Stocks/Bonds (60/40)

- Portfolio B – Stocks/Gold (60/40)

- Portfolio C – 100% Gold

Below is a chart demonstrating the performance of the three portfolios beginning with $10,000 in 1972, with no rebalancing.

{kind=link}

In the above example, Portfolio B with a 60% allocation to equities and 40% to gold performed almost identically to that of the standard 60/40 Equity/Bond allocation for Portfolio A. Portfolio C, which represents a 100% investment in gold underperformed both A and B. At first glance, allocating to gold does not seem to provide any real benefit to investors.

{kind=link}

Comparing the performance statistics of the portfolios provided in the table above, we acknowledge that Portfolio B did indeed improve returns by delivering a slightly higher annualized return ((CAGR)) of 9.55% versus 9.43% for Portfolio A. However, this additional boost in performance by allocating to gold came at the cost of much higher volatility in returns (higher standard deviation). Overall, this resulted in a lower Sharpe Ratio of 0.39, a popular measure for risk-adjusted returns.

We also note that gold did not perform consistently over the backtest period. Gold performed extremely well during the hyperinflationary decade of 1970 to 1980, but suffered a prolonged bear market that lasted for almost two decades from 1981 to 2000. Gold then suffered yet another prolonged bear market in 2012 and only bottomed out by 2015.

Prolonged periods of drawdown for gold present serious challenges for investors as performance could be volatile and unpredictable. The fact that gold also does not produce any income in the form of dividends or interests during the investment period, only makes the asset even more risky for retirees, or middle-aged investors planning for their retirement needs.

An Asset That Survives Wars

Ultimately, what truly holds up as a valid argument in favour of investing in gold is the asset's ability to preserve wealth during periods of economic turmoil particularly hyperinflation, or catastrophic events such as war.

Gold's true advantage lies in its long tradition and historical role as money and its impeccable track record of having survived multiple wars and economic crises. Without diving into the seemingly endless history detailing gold's widespread adoption and influence through the ages, it is suffice to say that gold is truly a time-tested asset for the preservation of wealth having survived countless conflicts, revolutions, and wars to date.

Gold has preserved wealth over countless wars because it has always been readily accepted and exchangeable for any other currency in the world. In contrast fiat money, which includes any government-issued currencies that are not backed by a commodity, depends entirely on the faith of its users. Thus, there have been many occasions in history when fiat money was devalued during war, political upheaval, and economic turmoil. Even ownership of land and property are subjected to the risk of being expropriated and destroyed in the event of war or political upheavals.

In terms of wealth preservation, it is quite clear that there are few assets, if any, that can match gold's enduring status through the ages.

Now, let us explore reasons why we think gold may be a bad investment. The arguments against gold are usually much more direct and grounded in economic reality, rather than driven by beliefs and traditions. As we have already highlighted the mixed evidence of gold being an effective hedge against inflation, as well as its subpar risk-reward profile, we will look at other qualitative factors that make gold a bad investment.

A Non-Productive Asset

Gold is commonly used in the manufacturing of electronics, aerospace equipment, and medical devices, due to its properties of being a good conductor of electricity and the least reactive metal. However, due to its scarcity and high price relative to other metals, gold is used in limited quantities and mostly reserved for applications where there is simply no better alternative to gold.

Thus, gold is primarily considered as an asset that is a "buy-to-hold" investment rather than productive assets like equities, debt, or real estate. Because gold does not produce any income in the form of dividends, interests, or rent during the investment period, investors only generate returns if they are able to sell it at a much higher price. This, however, makes gold an unsuitable investment for retirees who require periodic income. Gold may also be unsuitable for investors with a short investment horizon since we have demonstrated that drawdowns in gold prices can be extremely long.

In contrast, bond investors earn interest in the form of coupons while waiting for those bonds to mature. Equity investors may also earn dividends indefinitely as long as they remain shareholders of a corporation. Even if a stock does not pay dividends, shareholders ultimately own a share of the corporation and will gain from any growth in the intrinsic value of the corporation over time.

Being a non-productive asset, it is not possible to use gold to create and grow value on its own. Unlike corporations that can reinvest profits to grow revenues, or real estate that can be redeveloped and enhanced to grow rental income.

Better Alternatives

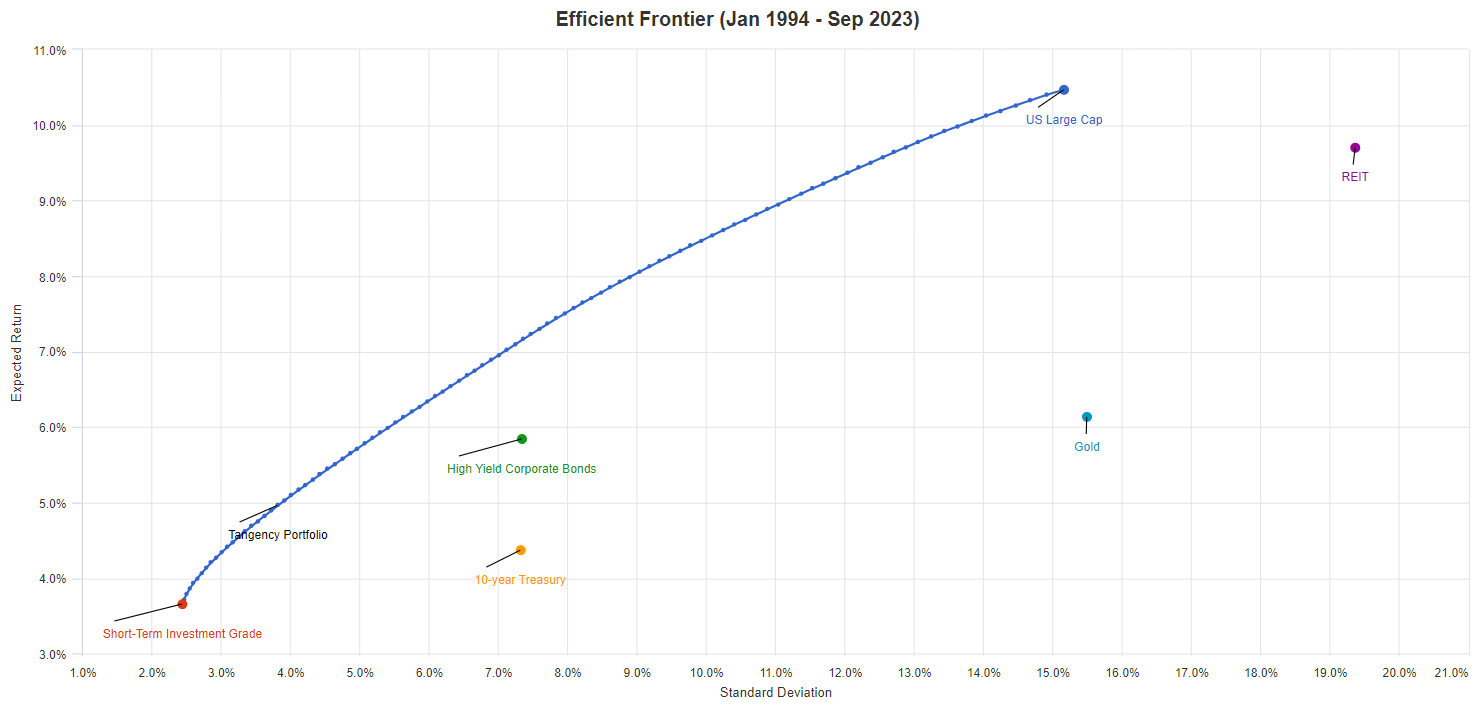

Gold's potential as an investment should not be determined as a standalone asset class, but within the context of a diversified portfolio. Doing so provides a more holistic view of the inherent risk-reward trade-offs associated with constructing a portfolio of assets. To keep the analysis simple and only at the asset class level, below is the efficient frontier for major asset classes since 1994 generated using portfoliovisualizer.com.

{kind=link}

The efficient frontier graph essentially allows investors to compare the historical performance of all assets in question with standard deviation representing volatility on the X-axis and expected returns on the Y-axis. The efficient frontier then represents the most efficient risk-return profiles that an investor can achieve by combining these assets with varying weights when constructing a portfolio. Such analysis can be done not just for asset classes but also at a much more granular level by comparing individual assets. For our purposes, we will only look at major asset classes and consider gold as a unique asset class on its own.

To compare the assets in the graph, start by thinking in terms of risk-return trade-off: for each unit of additional risk that an investor takes on, how much in additional returns can the investor expect?

As the efficient frontier graph shows, gold has generated returns averaging 6.14% over the test period, with a standard deviation of 15.5%. Meanwhile, the asset with the closest level of risk is U.S large-cap stocks (S&P 500 Index), which generated returns averaging 10.5% and a standard deviation of 15.2%. So clearly, by taking on almost the same amount of risk investing in gold, the investor is much better off investing in the S&P 500 Index. Returns from REITs are quite close to the S&P 500 Index but would require investors to take on excessive risk. On the other extreme, short-term investment grade bonds are the least risky but also provide the lowest returns.

The efficient frontier also considers the benefits of diversification by combining different assets based on the correlation between those assets to achieve an efficient portfolio. Based on our simulation, despite the diversification benefits of adding gold, none of the efficient portfolios on our efficient frontier hold greater than 17% weight in gold. In fact, by adding more asset classes with superior risk-return profiles compared to gold, we can further reduce or even do entirely without gold when building an efficient portfolio.

We were unable to include other major asset classes including hedge funds and private equity due to limitations in data availability. However, various research studies have shown that adding alternative assets can help further improve the efficient frontier.

Look Beyond Inflation & Geopolitical Risks

Our discussion thus far has largely focused on the long-term considerations of investing in gold as an asset class. However, even in the short-to-medium term, we expect gold to underperform other major asset classes.

We note that gold prices are near all-time highs as a result of two key forces that have been driving capital flows towards safe-haven assets including gold.

First is inflation, which drove investors and even central banks to buy gold in 2022 partly due to fears that inflation would remain stubborn and that the world economy would descend into a hyperinflationary environment. Of course, those fears did not materialize and inflation has since cooled to within reach of the Federal Reserve's target of 2%. However, gold prices did not follow the downward path of inflation. We suspect that this could potentially be increased speculative buying that is simply chasing returns on gold and propping up prices.

Secondly, geopolitical risks around the world have clearly escalated recently in addition to a drawn-out war in Ukraine. So it is understandable that some investors may be thinking of hedging geopolitical risks by buying gold. Although we acknowledge that geopolitical risks have escalated meaningfully, there is little reason to believe that the world is inching towards large-scale war. Instead, we are seeing consistent dialogue among major world leaders for restraint and de-escalation. More often than not, geopolitical risks have a limited and fleeting impact on risky assets, and we think this time is no different.

Given our view that neither inflation nor geopolitical risks present a serious threat to the global economy, for now, we see little reason to be bullish on gold. Instead, we believe that the rally in gold may be overdone and that we are more likely to see prices fall as the economic and geopolitical outlooks gradually improve.

In Conclusion

We hope we have provided a comprehensive overview of the major arguments in favour of and against gold as an investment. Overall, we conclude that there is little merit in holding gold in one's portfolio unless one is reasonably confident that the U.S. is headed for some kind of catastrophic crisis in the next few years. The subpar historical performance of gold versus other asset classes should, at the very least, encourage investors to seriously reconsider the purported benefits of investing in gold.

For further details see:

Why Gold Is A Bad Investment