PAC - Why Grupo Aeroportuario Del Pacifico Is A Smart Investment For Manufacturing Nearshoring To Mexico

2023-03-13 09:12:17 ET

Summary

- Mexico offers a generational opportunity for investors who would like to capitalize on its emergence as the preferred destination for supply chain nearshoring.

- Wide-moated Grupo Aeroportuario del Pacífico (GAP) is poised to reap the benefits of manufacturing nearshoring to Mexico.

- In this article, I analyze the underlying economics of GAP to shed some light on its risk-reward profile.

The nearshoring of manufacturing from China to Mexico is a significant global trend that has just started to receive attention. Mexico has begun to be identified as a " lifetime opportunity " for investors. Several authors on Seeking Alpha have discussed how equity investors could benefit from the emergence of Mexico as a major manufacturing hub, including a recent article by myself.

Which stocks should risk-averse investors consider to take advantage of this emerging theme? In this article, I analyze Grupo Aeroportuario del Pacífico, S.A.B. de C.V. , also known as GAP ( PAC ), as an under-regulated infrastructure play, which I explained in an interview with Seeking Alpha .

Competitive position

Monopoly on 14 airports

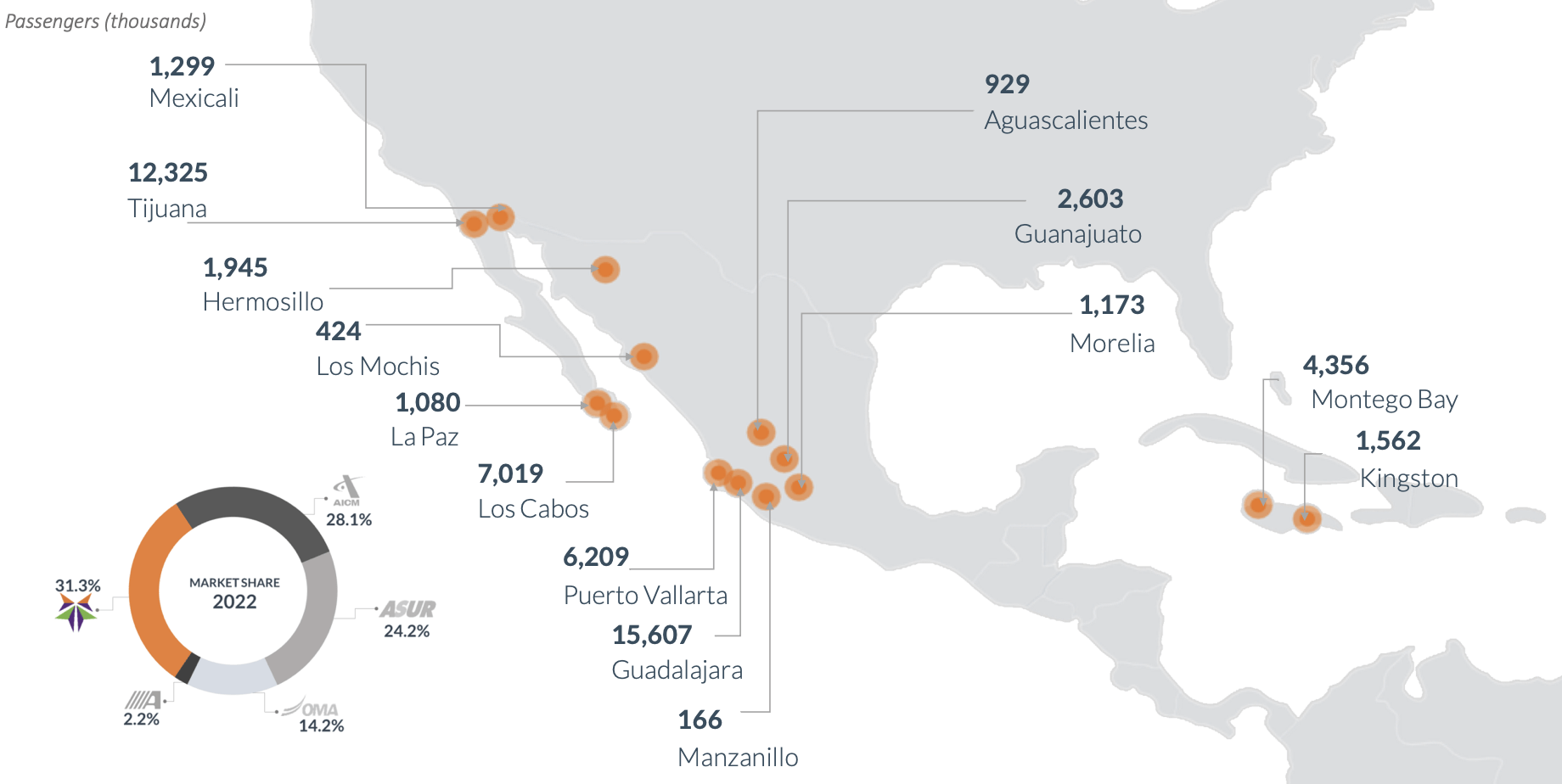

Grupo Aeroportuario del Pacífico was established in 1998, following the issuance of the Investment Guidelines for the Opening of Investment in the Mexican Airport System by the Mexican government. This initiative aimed to privatize 35 out of 58 main airports in the country. As part of this effort, a total of 12 airports on the Pacific coast were placed under GAP's management through a concession that runs until 2048. These airports include Guadalajara and Tijuana, as illustrated in Figure 1.

{kind=link}

Fig. 1. Airports of Grupo Aeroportuario del Pacífico, shown with its market share in Mexico (modified after Grupo Aeroportuario del Pacífico)

In 1999, the Mexican government sold a 15% equity stake in GAP to a joint venture consisting of equal partners AENA Desarrollo Internacional S.A. ( ANNSF ), Controladora Mexicana, and Desarollo de Concesiones Aeroportuarias S.A. for US$261 million. In 2006, the remaining 85% stake in GAP was disposed of by the Mexican government through an IPO.

In addition to its operations in Mexico, GAP also manages the Sangster International Airport in Montego Bay, Jamaica, under a 30-year concession since 2003. Furthermore, GAP has been operating the Norman Manley International Airport in Kingston, Jamaica, since 2019, under a 25-year concession.

Under the concessions granted by the governments, Grupo Aeroportuario del Pacífico enjoys a monopoly on air travel in the areas covered by its airports. This monopoly provides two key benefits:

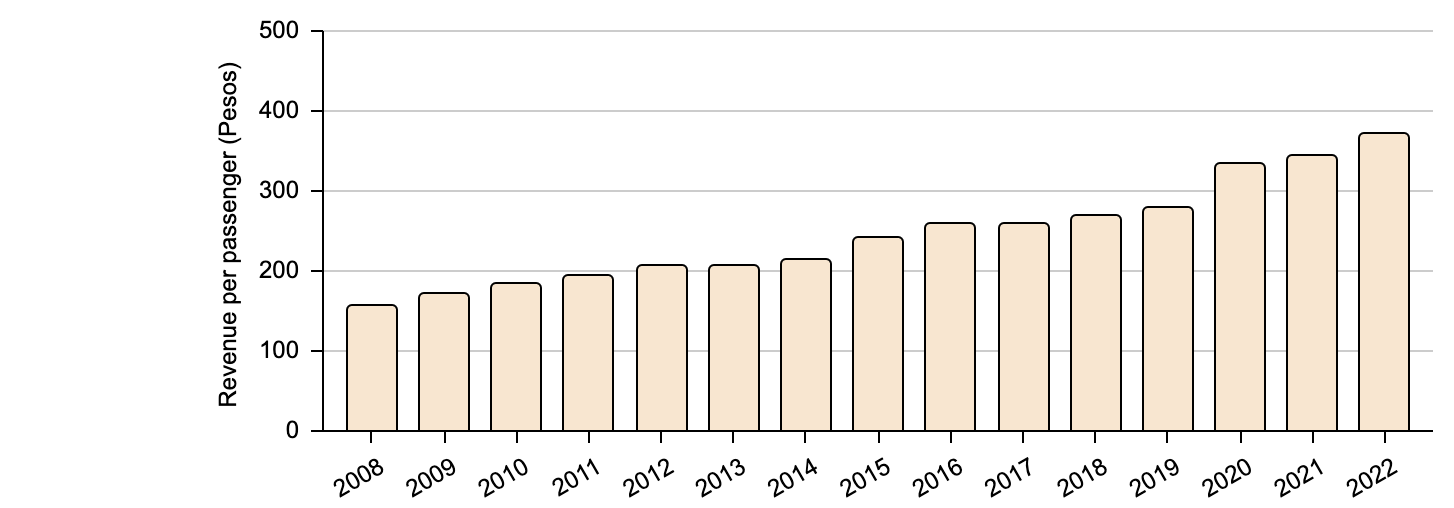

- Firstly, GAP is able to charge higher fees for each passenger passing through its airports, thanks to its pricing power over airlines and air travelers. From 2008 to 2022, revenue per passenger increased at a compound annual growth rate (or CAGR) of 6.34%, as portrayed in Figure 2.

- Secondly, the ability to raise prices enhances the resilience of its business even during adverse events. For example, when an H1N1 epidemic broke out in Mexico in May 2009, resulting in a 13.33% decline in traffic, it took two years for throughput at GAP-operated airports to recover. However, GAP managed to mitigate the impact of lost traffic by raising aeronautical revenue per passenger by 6.00% in 2009 and an additional 11.17% in 2010. In 2020, when the Covid-19 pandemic forced global air traffic to a halt, GAP was able to increase revenue per passenger by about 20.08%, which helped the company weather a disastrous year.

{kind=link}

Fig. 2. Revenue per passenger through the airports of Grupo Aeroportuario del Pacífico (Laurentian Research for The Natural Resources Hub based on data released by Grupo Aeroportuario del Pacífico and Seeking Alpha)

Profitability

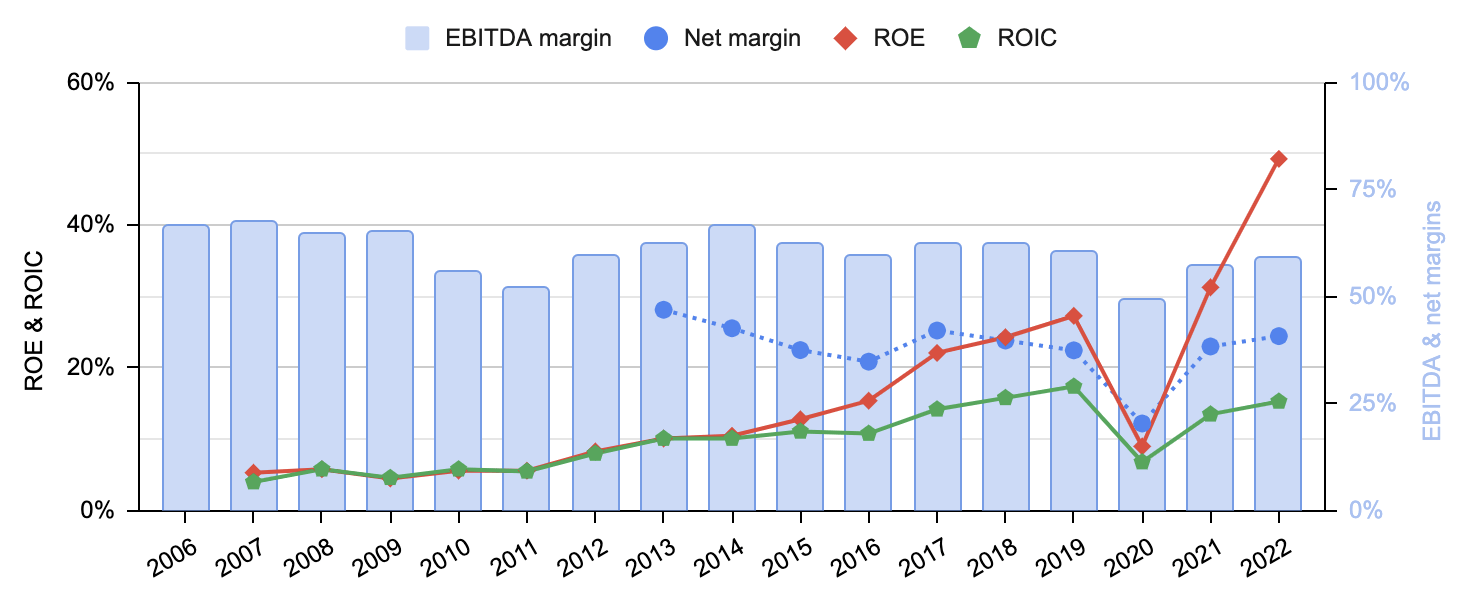

Grupo Aeroportuario del Pacífico benefits from an advantageous competitive position that enables it to earn high-margin profits and maintain excellent capital efficiency. GAP has an average EBITDA margin of 60.70%, even during years of and following adverse exogenous events, such as in 2009-2011 and 2020-2021, when it achieved an EBITDA margin of 49-57%. On average, it also maintains a net margin of 40%.

The depreciation of long-lived assets can inflate return on equity, as is the case with other under-regulated infrastructure plays, such as Union Pacific ( UNP ), which I discussed elsewhere . Except for the Covid-impacted years of 2020-2021, GAP has recorded a ROIC above 15.30% in recent years, as shown in Figure 3. WACC estimates for emerging market stocks tend to be affected to a large extent by the high country market risk premium, which may be unfair for high-quality businesses operating in those markets. For GAP, the country market risk premium assigned to Mexico is as high as 9.2%, even though Moody's assigned senior unsecured ratings of Baa1 on the global scale and Aaa.mx on the Mexican national scale to GAP, while S&P Global assigned mxAAA on the Mexican national scale. Despite this, management reiterates its commitment to reducing GAP's WACC below 9.0%, at which GAP earns sizable excess ROIC, indicating respectable capital efficiency. This conclusion has also been reached by a fellow Seeking Alpha author .

{kind=link}

Fig. 3. EBITDA margin, net margin, return on equity and return on invested capital of Grupo Aeroportuario del Pacífico (Laurentian Research for The Natural Resources Hub based on data released by Grupo Aeroportuario del Pacífico and Seeking Alpha)

Growth

Historical growth

Grupo Aeroportuario del Pacífico generates revenue from two sources:

- Aeronautical services, which mainly include fees and charges for departing passengers, landing fees based on aircraft weight and arrival time, parking fees, and fees for transporting passengers from an aircraft to a terminal building. These revenues are subject to regulation under maximum rates.

- Non-aeronautical services, which are not subject to maximum rates and chiefly comprise car parking charges and leasing of commercial space to tenants, advertisers, ground transportation providers, and other miscellaneous sources of revenue.

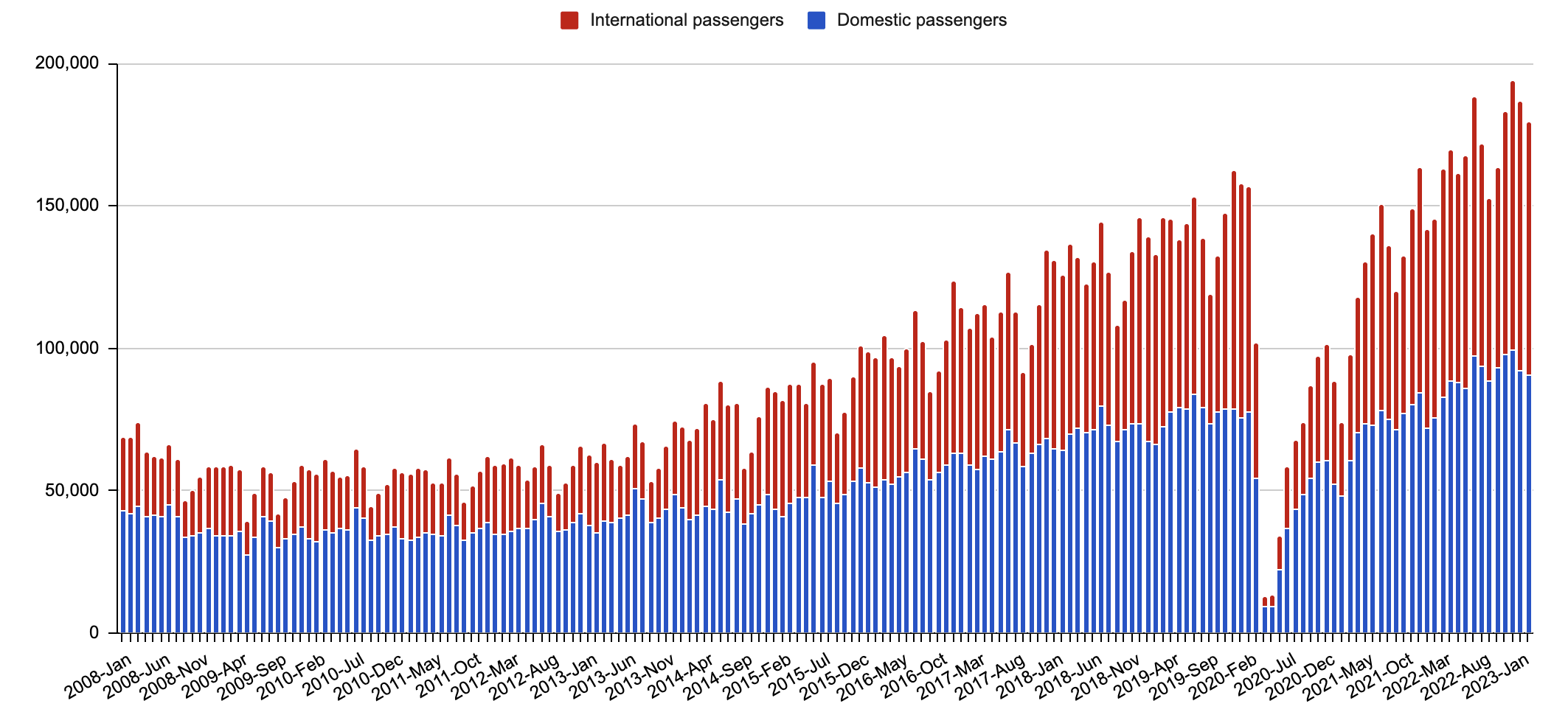

The main drivers of revenue are revenue per passenger, as discussed earlier, and passenger throughput. From the peak of the 2009 H1N1 epidemic to February 2023, domestic passengers grew at a compound annual growth rate of 7.48%, international passengers at a CAGR of 13.88%, and total passengers at a CAGR of 9.98%, as illustrated in Figure 4.

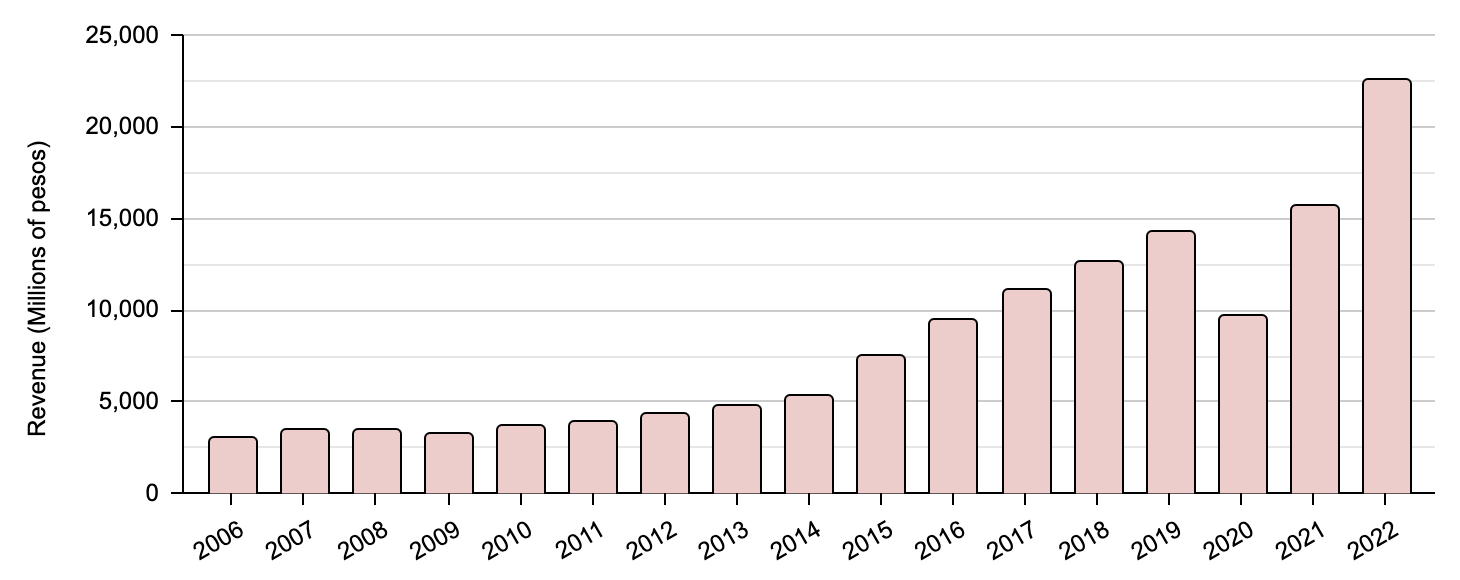

Thanks to the CAGR of 6.34% for revenue per passenger and 9.98% for passenger throughput, GAP achieved revenue growth of 16.02% CAGR during the same period, as shown in Figure 5.

{kind=link}

Fig. 4. Domestic and international passenger through the airports of Grupo Aeroportuario del Pacífico (Laurentian Research for The Natural Resources Hub based on data released by Grupo Aeroportuario del Pacífico and Seeking Alpha)

{kind=link}

Fig. 5. Total revenue of Grupo Aeroportuario del Pacífico (Laurentian Research for The Natural Resources Hub based on data released by Grupo Aeroportuario del Pacífico and Seeking Alpha)

Outlook

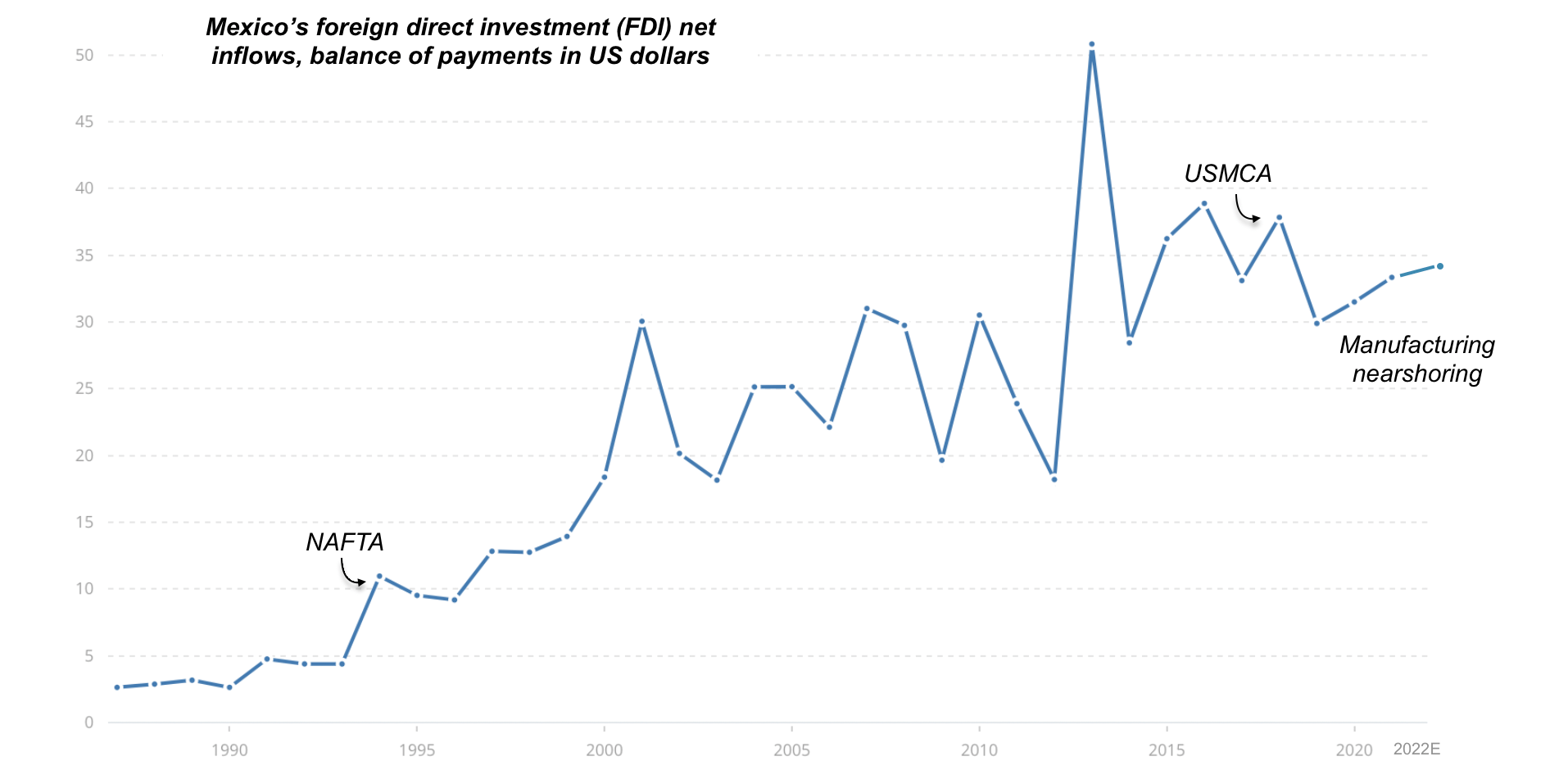

The Mexican economy has been experiencing rapid growth, which has driven the expansion of air travel in the country, including at GAP airports. The country's population is expected to continue growing at an annual rate of 1.06% for the next few decades. Since the implementation of the NAFTA trade agreement in 1994, foreign direct investment ((FDI)) has increased significantly, as shown in Figure 6. As previously mentioned , the projected increase in manufacturing nearshoring from China to Mexico is expected to further boost the Mexican economy in the future.

Mexico’s foreign direct investment net inflows, balance of payments in US dollars (modified from World Bank)

{kind=link}

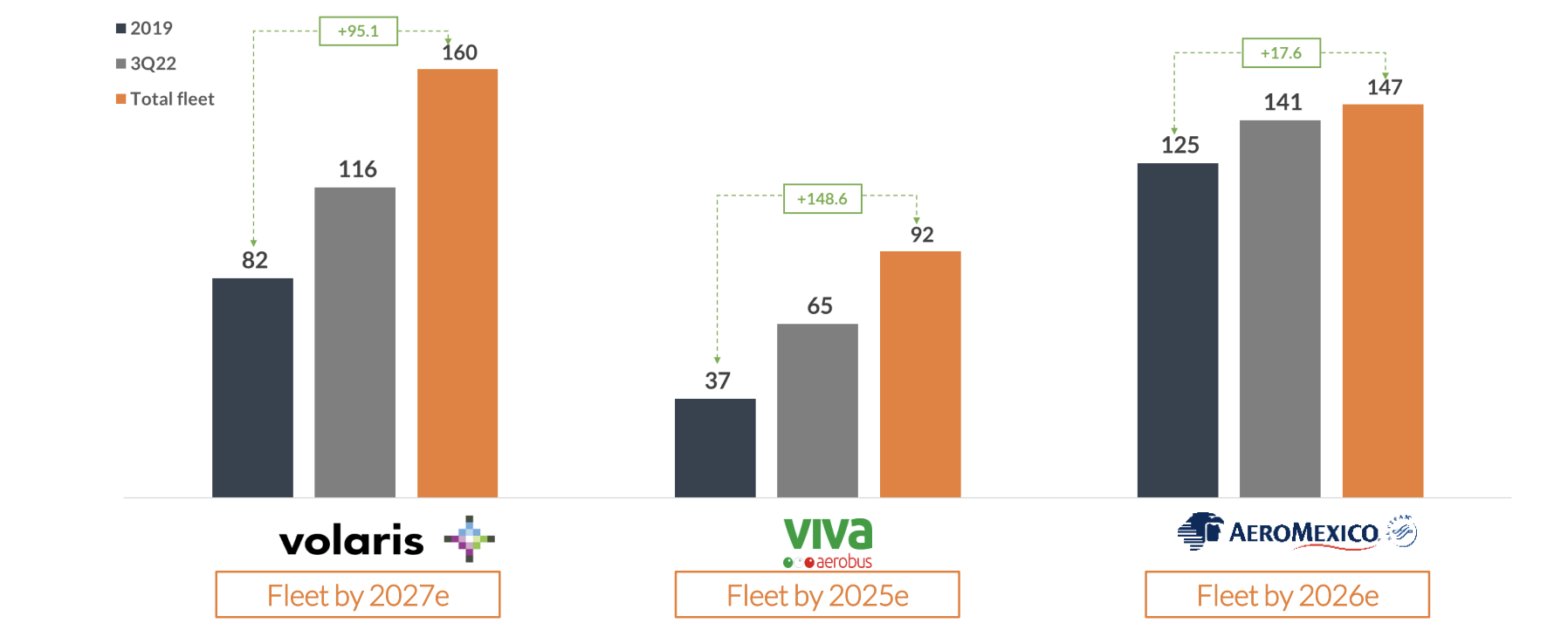

In response to the growing demand, airlines operating in the Mexican market are expanding their fleets and increasing their transportation capacity, as exemplified in Figure 7. As a result, the potential transportation capacity is projected to grow by 38% over the next five years.

{kind=link}

Fig. 7. The plans of Volaris, Viva and AeroMexico to expand their fleets (Grupo Aeroportuario del Pacífico)

Anticipating a strong increase in passenger traffic in the coming years, GAP is investing in expanding the capacity of its airports. The company has planned to construct a second runway at the Guadalajara airport, and build new terminals at the Tijuana, Guadalajara, and Puerto Vallarta airports, which will expand terminal space from 280,000 to 590,000 square meters by 2026. Additionally, GAP is developing commercial spaces, parking lots, hotels, corporate offices, and VIP lounges.

Valuation and risks

Let's assume that Grupo Aeroportuario del Pacífico can maintain domestic and international passenger throughput growth at 7.48% and 13.88%, respectively, increase revenue per passenger by 6.34% per year, and convert 40% of revenue into net income over the next 10 years. Afterward, its net income is expected to grow at 3.0% per year so that a terminal value can be calculated. A WACC of 9.0% is also assumed. Based on these assumptions, the intrinsic value of Grupo Aeroportuario del Pacífico is estimated to be US$292 per share, implying a 60% upside from the current share price of US$182.40 as of March 10, 2023.

For further details see:

Why Grupo Aeroportuario Del Pacifico Is A Smart Investment For Manufacturing Nearshoring To Mexico