HDELY - Why HeidelbergCement Is One Of My 2023 Considerations

Summary

- I've beefed up my position in HeidelbergCement whenever the stock has been under €50/share for the native. My current cost basis is around €44/share.

- My position is now at its target. I have covered HeidelbergCement for you before, but I'm going to make a clarification here.

- One of the key reasons why HeidelbergCement is so interesting to me is the ongoing war between Ukraine and Russia.

Author's Note: A longer version with more explanations of this article was posted on iREIT on Alpha back in December of 2022.

Dear subscribers,

I've covered HeidelbergCement ( HDELY ) plenty. Many of you have read my exclusive and free articles, and I know many of my readers here have a position. Myself, I'm up to a 5% position now, and I have no plans to divest this, despite already seeing double-digit returns on my investment in the short term.

Why is that?

Well, I will explain here - along with some background.

Why HeidelbergCement?

HeidelbergCement is one of the largest building materials companies on earth - period. After completing the M&A of Italcementi, it became the largest aggregate producer of construction aggregates at the time and is now one of the world's largest producers of building materials.

While the company's asset base isn't as shiny as some of its competitors, because this M&A came with a lot of trouble-laden assets, the company still has a significant upside. In 2020, HDELY was ranked as the 678th largest company - in any sector - in the world - and this hasn't shifted much since.

It works in 60 countries with 50,000+ employees working at over 3,000 production sites, operating over 135 plants with an annual capacity of over 175 million tonnes. Additionally, the company has over 1,500 ready-mix sites and over 600 quarries where aggregate is sourced.

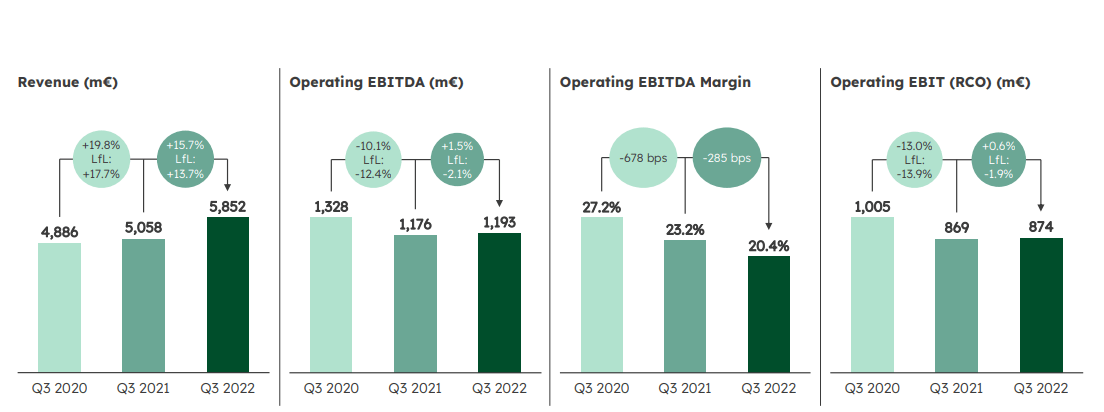

I've been through HeidelbergCement before - but I want to emphasize the recent results here. Take a look at the top-line and bottom-line results.

HeidelbergCement IR (HeidelbergCement IR)

{kind=link}

Yes, the bottom line is under pressure due to energy costs - no, it's not going to improve markedly in the near-term future for as long as the energy trend subsists. And no, it doesn't make the company unattractive in the least.

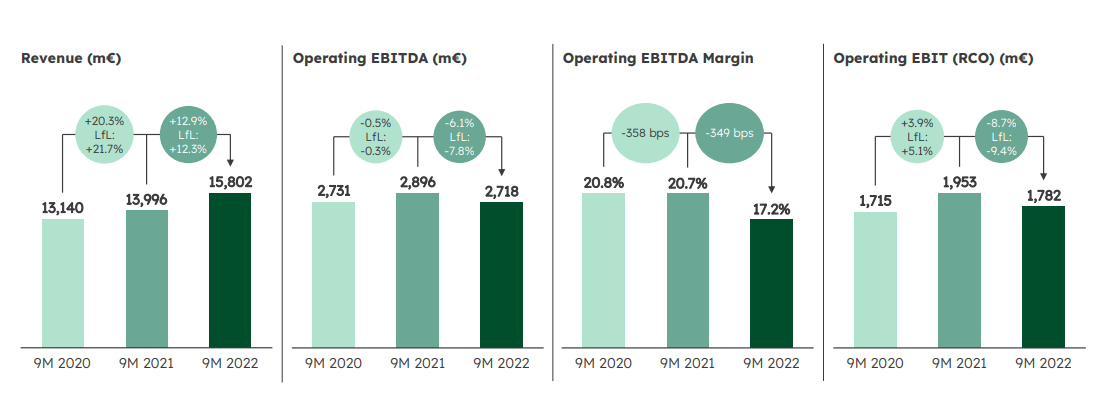

On a 9-month perspective, things look slightly better.

HeidelbergCement IR (HeidelbergCement IR)

{kind=link}

In a way, it's not all that odd that the company has been punished since Ukraine was invaded, because the company does operate 3 cement factories in Russia. What's more, HDELY lacks some of the efficiency seen in the company's competitors, such as Holcim ( OTCPK:HCMLY ), and Vicat ( OTCPK:VVCTY ).

If you recall my base article on the company, the results for 2021 were absolutely stellar. HeidelbergCement saw a near-double digit sales revenue increase, a 6% EBITDA increase, and above all, a successful across-the-board price hike increase and fixed cost management that preserved the company's operating margins and profit - despite the aforementioned, sub-par asset quality in context to competitors. These trends were further confirmed by the most recent set of quarterly results, which were also impressive - even if some of the weaknesses we can expect started to materialize.

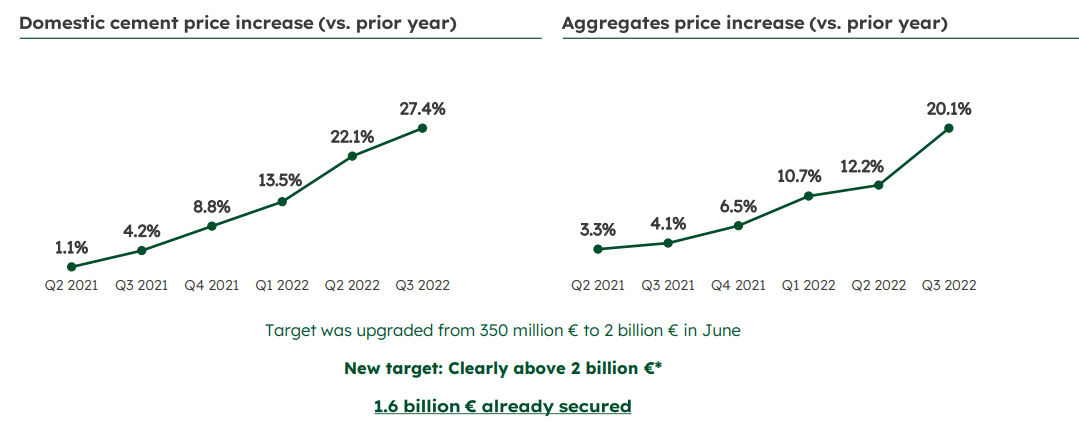

Current results are seeing pressures from net volumes (demands), pricing, and inputs (energy and the like) resulting in the EBITDA we see here. It's important to emphasize that HDELY has been able to push pricing, despite energy prices, and its commercial excellence is really paying off here.

The company has also implemented a good excellence program, and despite energy risks, the current forward/spot pricing gives HDELY confidence that price over-cost improvements are still possible for the company.

Take a look at some of these trends.

HeidelbergCement IR (HeidelbergCement IR)

{kind=link}

HDELY, despite all of the negatives, give us growth in free cash flow. We're at very low leverage despite these problems - net debt is down €700M for the year , with the second tranche of share buybacks planned ahead of schedule.

Guidance for 2022 calls for good revenue growth, an operating EBITDA of no less than €3.6B for the year, and leverage below 2x.

Yes, there are problems - no these problems do not make HeidelbergCement any sort of negative investment.

{kind=link}

The opposite, as I see it.

Please note that HeidelbergCement is changing its name - it will be known as Heidelberg Materials, and that is being implemented for year-beginning of 2023.

The company is extremely well positioned in both legacy and emerging markets, and it focuses on heavy building materials, with a 51% cement mix, 25% Aggregate, and 22% Ready-mix and asphalt.

The company is in a better position than ever before and is returning over €1B to shareholders through a mix of dividends and buybacks.

Concrete and cement prices rose in reaction to the war in Ukraine, due to the troubles in both Russia and the nation, with capacities actually being located there.

Me, I paid very close attention to what HeidelbergCement has done during the year. I have an entire folder full - so let me cut it down to the highlights and why I consider the company to be perfectly positioned for an end to the conflict - whenever it comes.

Remember, Concrete/Cement/Aggregate is not something you want to transport long distances. It's hugely expensive because you're essentially transporting gravel/powder. That means that you want to have capacities as close as possible to the area you're looking to supply - and that supply should preferably work by train or sea if possible.

Well, HeidelbergCement was already better positioned than Holcim and Vicat prior to the crisis because of its Italcementi M&A, and its asset base in Germany and eastern Europe.

More importantly, the company has been expanding its asset base in very strategic ways.

I wasn't surprised in the least when I learned in early May from IR that the company is acquiring no less than six plants and one sandpit using ?eskomoravský Beton, an HDELY subsidiary, from the competitor Kámen Zbraslav in Moravia, which is in the eastern part of the nation. At the same time, it's divesting assets in western Europe, such as Spain.

HDELY has been an active eastern-Europe player for more than 20 years. Other plants than the aforementioned ones in the former Czech republic could become plays for Ukraine as well. One of the largest and most modern European cement plants is located at Górazdze, in Poland, which by a combination of train/truck is within easy reach of Ukraine. This plant alone has an annual capacity of 4M tonnes per year.

The company is also heavy in RME in the Slovak Republic since 2011 as well as in Hungary. HDELY has also a presence in Romania, having expanded the Bicaz plant, in the north-east of the country, to an annual capacity of 2.3M tonnes, and modernized the Fieni plant, near the capital, Bucharest, including the installation of a new clinker silo and a mill with a capacity of 1M tonnes.

The business is also found in Georgia with terminals in the Black Sea which can handle hundreds of thousands of tonnes, all deliverable to the black sea coast.

I have personally been in contact with IR and management for both HDELY and for some of the subsidiaries to ask what questions I can, and I mean to book more "boots-on-the-ground" visits and reports where possible, as well as attending relevant conventions to see what the competitive landscape looks at not just from a high level, but on a more granular level.

Eastern Europe has never been unimportant to HDELY. It has been one of the company's major growth regions for some time - and it's my firm belief, that when the war ends and reconstruction is on the table, HeidelbergCement's resources and proximity will make it, if not the only choice, one of the first choices.

That is also what the company is betting on - and that is what I am mostly investing in.

HeidelbergCement's Valuation

It's my firm belief that once the war fades and the full strategy of the company becomes clear, HeidelbergCement's RoR from a €45/share price will make 100% RoR look conservative.

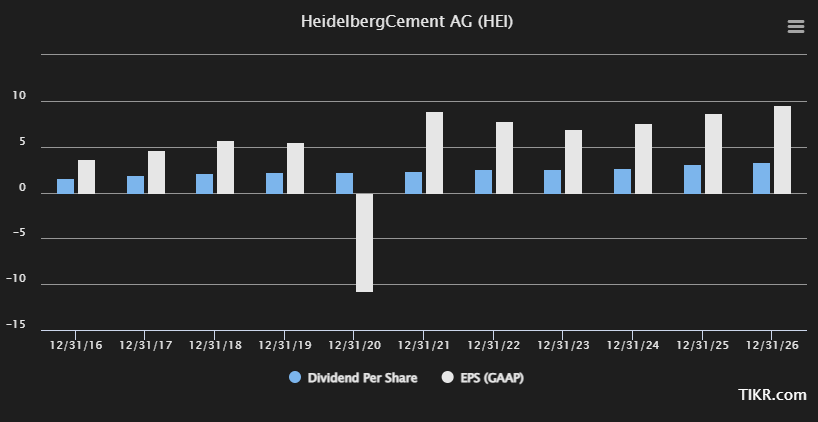

My YoC is over 5% - and I view the next few years of forecasts as more or less in the bag, even with energy pressure, because demand is likely to remain relatively high across the board. The dividend is expected to stay stable.

HeidelbergCement EPS/Dividends (TIKR.com )

{kind=link}

As before, I'm only slightly working over my current models. Unlike many other analysts, I don't shift my target due to the market having a hissy fit - which is what I see the market as mostly having here, and mostly having had for most of this year. The main impact I'm calculating and adjusting for my forward modeling is a margin impact due to lower margins from energy pricing and inflation.

I give the higher weight to DCF and NAV. For NAV, I'm remaining at a 0.8% sales growth, but I'm lowering my expected EBITDA growth rate to 0.1% per year to reflect pricing pressure, updated for December. However, these forecasts are nulled when the war ends - because that changes things.

Current DCF models imply an EV/Share of between €70-€75/share. For NAV, the changes are equally subtle, with a slight reduction in EBITDA multiples especially for Europe and APAC to reflect Macro, reducing the implied NAV/Share to €86/share.

NAV remains colored by the replacement value of the company's assets and will continue to be high regardless of impacts here. It's extremely expensive to replace the company's assets at current or future market costs. That makes the ownership of these assets, even if they're old, extremely attractive simply on the base assumption of demand. And that demand remains high.

I'm not shifting my price target. The last PT was €80/share. The current PT is €80/share - and that's conservative.

Expect the stock to go on a tear possibly the day that the war ends.

HeidelbergCement is one of the best-positioned Cement and Concrete businesses that will likely be integral to the rebuilding of large parts of the Ukrainian nation.

This is the Reader's Digest version of the research I have been doing for the past 7 months. This is something I will be following, and I will be visiting Ukraine, speaking to IR and management, visiting trade shows and conventions, and keeping my ear to the ground, not just for Concrete but for rebuilding, in general, to see where the wind shifts.

I would never take a strong position in a small, local company or put my money in local plays - which by the way I have been offered to do. My risk tolerance would never allow for the quadruple-digit total Rates of return that are on offer there, and what those plays entail - they're more or less outside of the market as well.

However, investing in HeidelbergCement - Or rather, Heidelberg Materials as it will be known , is one of the safest ways to play the Ukrainian upside. That is why I'm at maximum exposure, and why I won't touch that sell button until the company hits triple-digits or around there, if then. There's too much "other stuff" in the company's mix.

And there are other companies like it out there, in other fields.

However, this is the main one.

Questions?

Let me know.

For further details see:

Why HeidelbergCement Is One Of My 2023 Considerations