VNO - Why I Am Buying Vornado Realty Trust Yielding 9.84%

2023-04-25 09:00:00 ET

Summary

- Shares of VNO look undervalued as they trade at -35.29% tangible book value.

- VNO looks to be in a strong liquidity position and has managed its debt well, which mitigates the impacts of rising interest rates on its portfolio.

- VNO looks to trade at a discount to its peer group and offers large yield that is almost 10%.

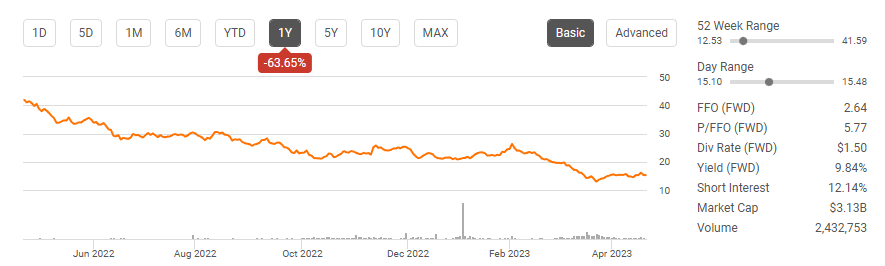

The short answer as to why I am buying shares of Vornado Realty Trust ( VNO ) is that the downward move in some REITs has been overdone. Shares of VNO have declined -63.65% over the previous year and have fallen -27.53% since the start of 2023. My opinion is that we have hit the mass fear stage in REITs, and there are some gems that have been impacted. I am looking at VNO as a long-term recovery play, and while I can't predict if the bottom is in, there looks to be a compelling value proposition based on what I am looking for. Today, shares of VNO pay a $1.50 dividend which works out to a 9.84% yield. I am quite comfortable establishing a position at these levels, collecting the large dividend, and if shares continue to fall without the value proposition changing, dollar cost averaging into the position. There are certainly risks in commercial real estate, but as more companies shift away from fully remote work, I believe now is the time to make long-term investments in strong REITs.

{kind=link}

Vornado has an NYC-focused portfolio and this is where I see value

VNO's NYC portfolio is very strong. VNO owns 62 Manhattan properties which consist of 19.9 million square feet of office space in 30 properties. VNO also has 2.6 million square feet of street retail space in 56 of its properties. VNO also has 6 residential properties with 1,664 units. Roughly 86% of VNO's business I stied to NY. VNO is developing 350 Park Ave and building an office building where Hotel Pennsylvania used to be. VNO has a 32% interest in Alexander's, Inc. (ALX), which owns 6 properties in the greater New York metropolitan area, including 731 Lexington Avenue, which is home to Bloomberg, L.P. headquarters, and The Alexander, a 312-unit apartment tower in Queens NY. VNO also owns Building Maintenance Services that provide cleaning and security services to its buildings and 3 rd parties. Outside of NY, VNO operates the theMART in Chicago, which is 3.7 million square feet, and has a 70% 70% controlling interest in 555 California Street, and other real estate investments.

{kind=link}

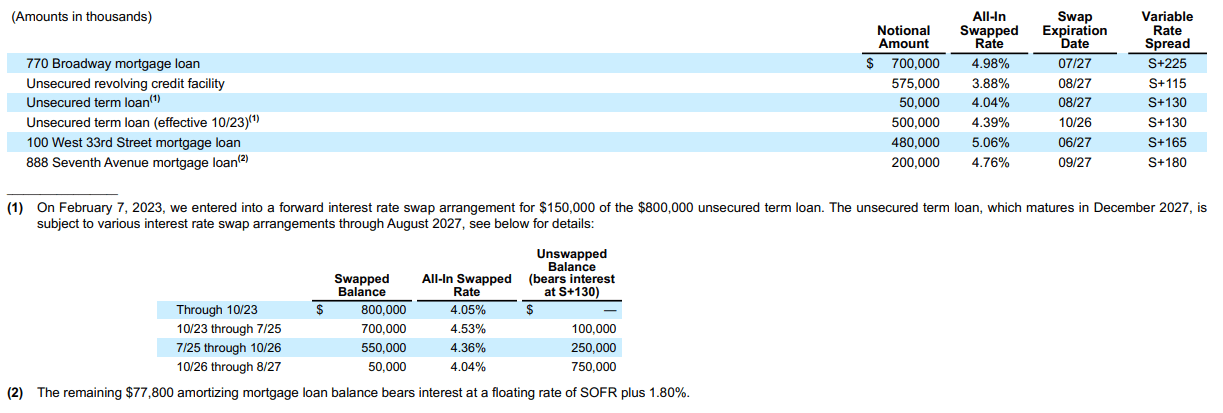

There are a number of reasons why I see value in shares of VNO, from liquidly to its business operations. As rates have continued to rise, it has made carrying costs more expensive to some degree. Any debt that isn't fixed could increase significantly, and the cost of borrowing is much more expensive. Management at VNO has been active in mitigating risk and entered into $2.0 billion of interest rate swap arrangements and extended a $500 million interest rate swap arrangement, reducing its variable rate debt as a percentage of its total debt at share from 47% to 27%. The exposure to VNO's exposure to LIBOR/SOFR index increases on its $2.8 billion of unswapped variable rate debt, but this is partially mitigated by $2.2 billion of interest rate caps and an increase in interest income on cash and cash equivalents over the next year.

{kind=link}

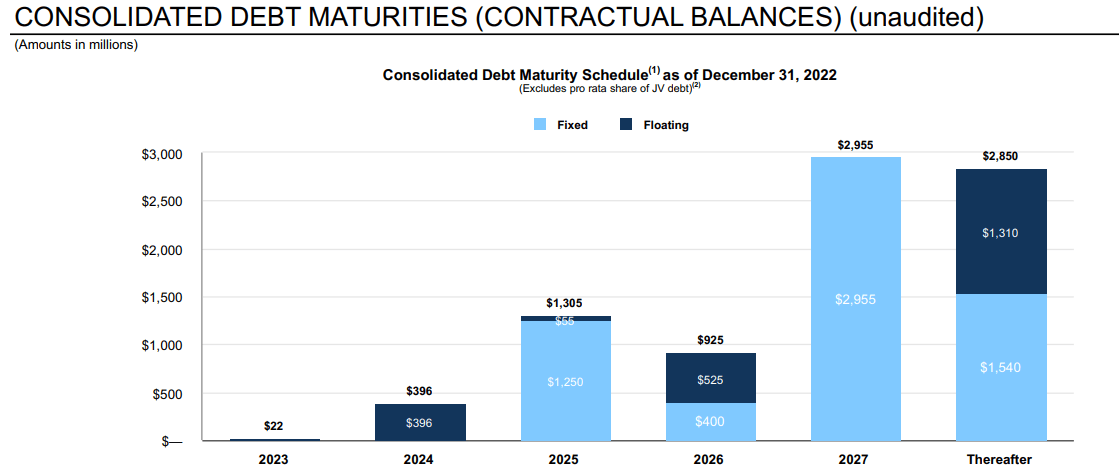

VNO finished 2022 in a strong liquidity position, with $1.49 billion in cash, cash equivalents, restricted cash, and investments in U.S Treasury bills. VNO also has the full $1.25 billion balance available on its revolving credit facility that matures in 2026 and $675 million available on its 2 nd revolving credit facility that matures in 2027 of $1.25 billion. VNO has $22 million of its long-term debt due in 2023, and $396 million due in 2024. The Fed is expected to pivot in 2024, and by the time 2025 rolls around, interest rates should be significantly lower, creating an opportunity to push out a portion of the maturities from 2025 – 2027 at favorable rates. VNO has enough cash on hand to repay all its maturing debt for 2023 and 2024 and still have more than $1 billion cash on hand going into 2025 without adding a single dollar to its balance sheet. I don't see VNO being a debt-ridden REIT, and it's in a strong liquidity position.

{kind=link}

Currently, VNO has a share price of $15.24 and a market cap of $2.92 billion. VNO has $6.51 billion in total equity on its balance sheet and a tangible book value of $23.55. Today, VNO's market cap trades at a -55.10% discount to its total equity, and shares would need to increase by 122.73% to trade at a 1:1 valuation. When I look at tangible book value compared to share price, VNO trades at a -35.29% discount to its tangible book value, and shares would need to increase by 54.53% to trade at a 1:1 valuation. VNO is also back to generating it's 2019 levels of EBITDA as its EBITDA fell from $891.9 million in 2019 to $624.5 million in 2020, then worked its way back up to exactly $891.9 million in 2022. After looking through the financials, I don't feel the debt is an issue, cash on hand is strong, a significant portion of the debt is hedged, and EBITDA is going in the right direction. I think the sell-off in shares of VNO has been overdone, and the current valuation looks like an opportunity.

How VNO compares to similar office REITs

I compared VNO to the following REITs to see how they traded compared to the peer group:

- Hudson Pacific Properties ( HPP )

- SL Green Realty ( SLG )

- Paramount Group ( PGRE )

- Douglas Emmett ( DEI )

- Kilroy Realty ( KRC )

- Boston Properties ( BXP )

- Cousins Properties ( CUZ )

- Corporate Office Properties Trust ( OFC )

- Easterly Government Properties ( DEA )

{kind=link}

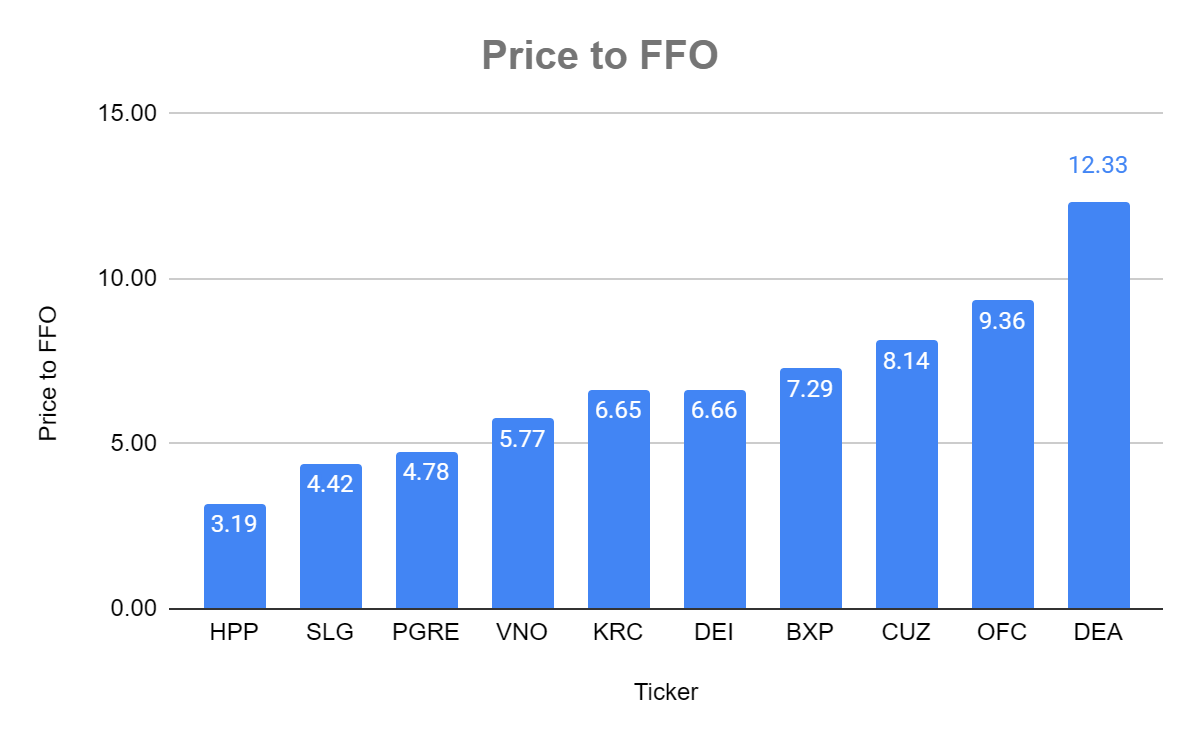

I have no problem saying that when it comes to making investments, I am cheap and want to pay the lowest I can for a REITs FFO. The peer group trades at an average price to FFO of 6.86x, and VNO trades under the peer group average at 5.77x.

{kind=link}

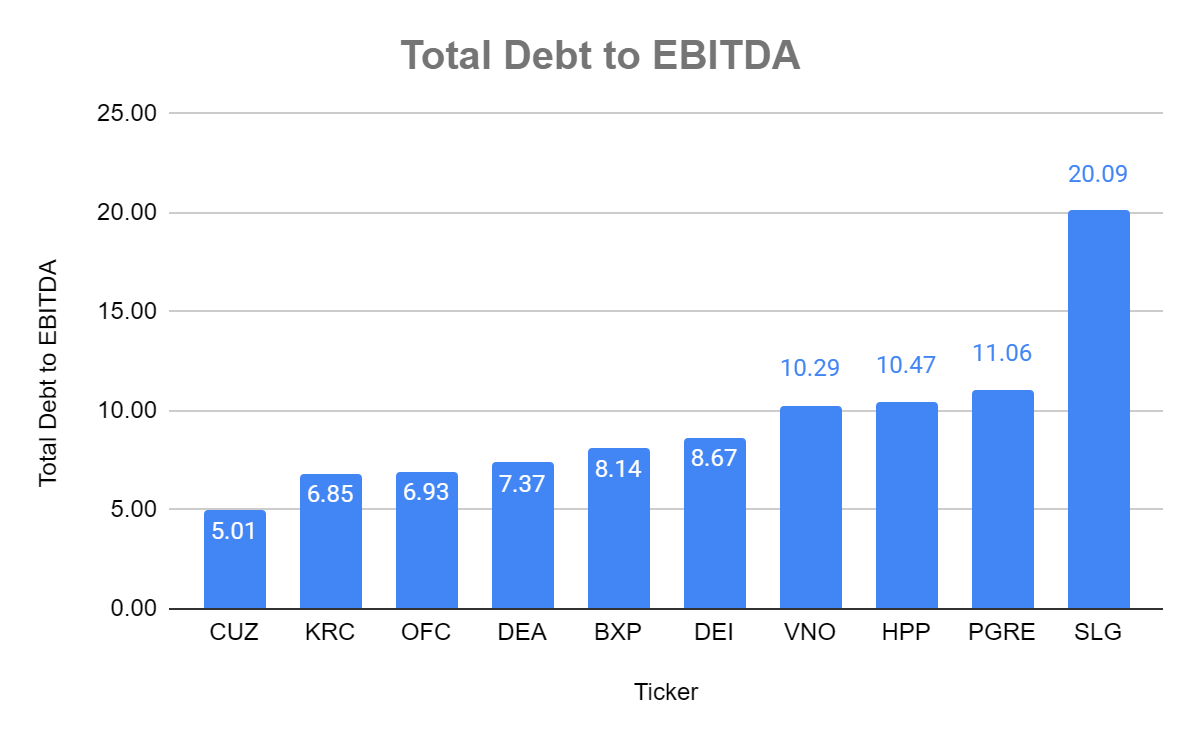

VNO trades at a 10.29x EBITDA to total debt while its peer group average is 9.49x. VNO trades slightly higher than the average of its peers, but after looking into its debt, I am comfortable with this ratio.

{kind=link}

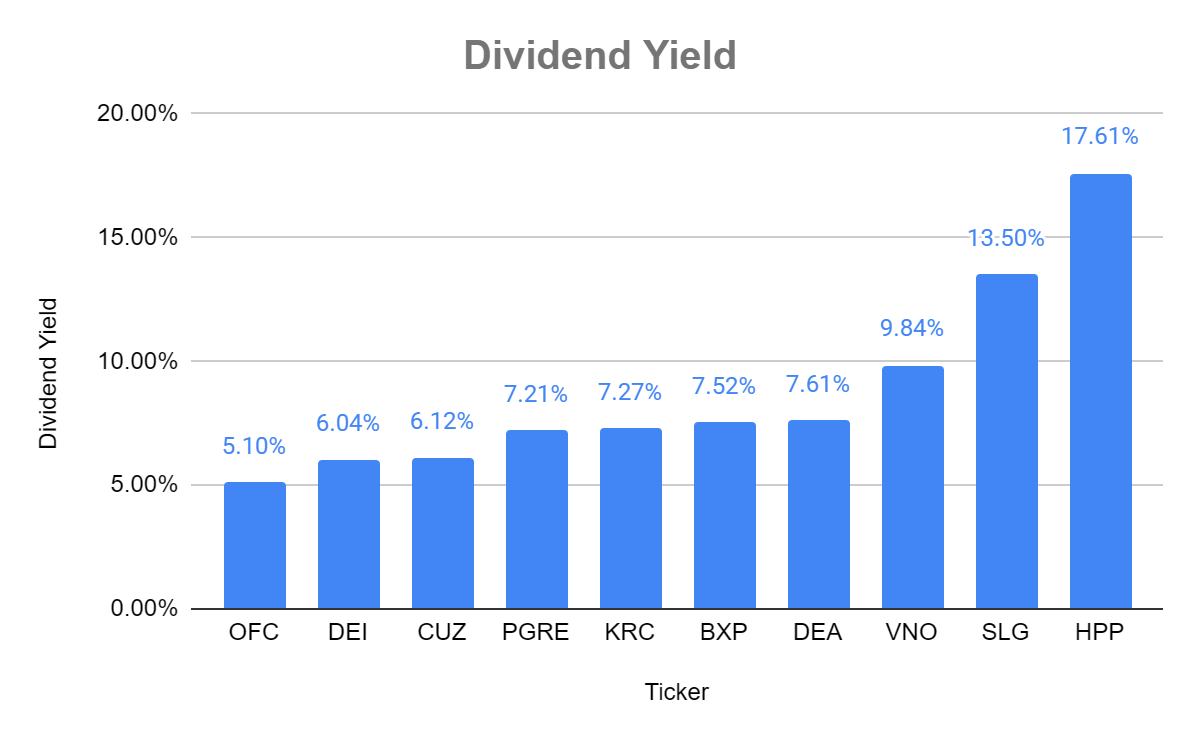

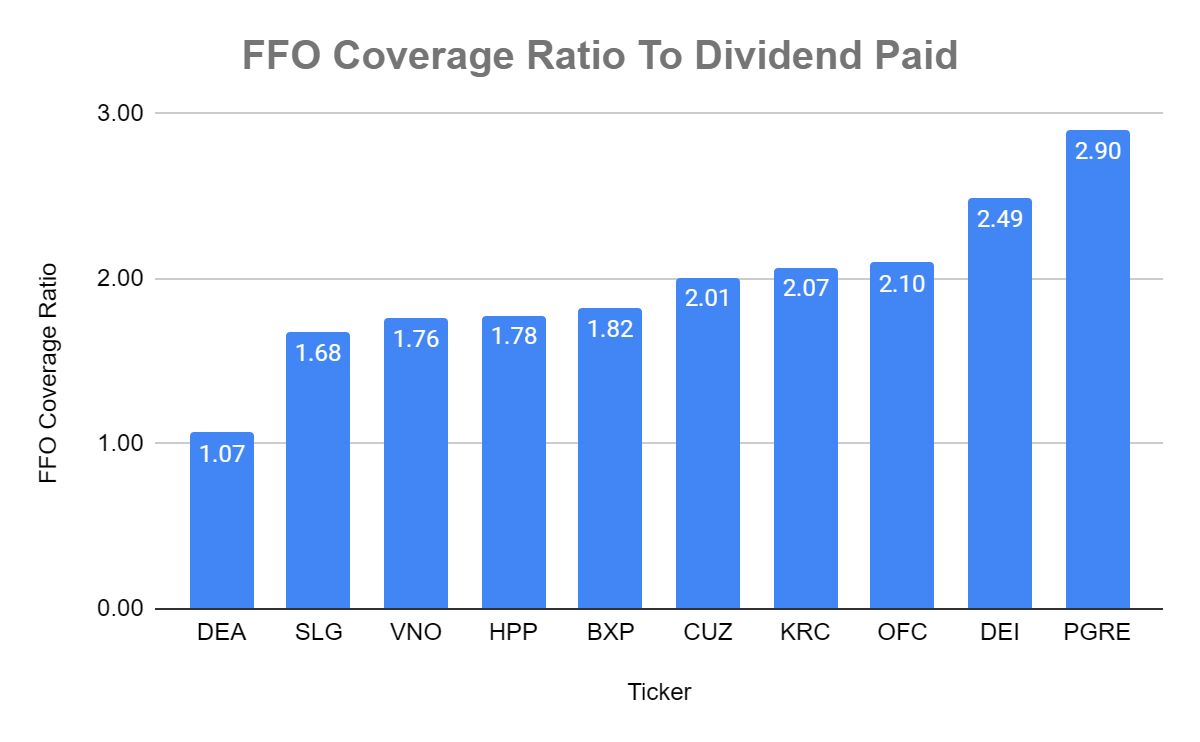

VNO has a dividend yield of 9.84% with a 1.76x FFO coverage ratio. Its peer group average is a dividend yield of 8.78% and an FFO coverage ratio of 1.97x. While VNO has a lower than average coverage ratio, it still has a 1.76x coverage ratio which is more than enough to make me feel the large 9.84% yield is safe.

{kind=link}

{kind=link}

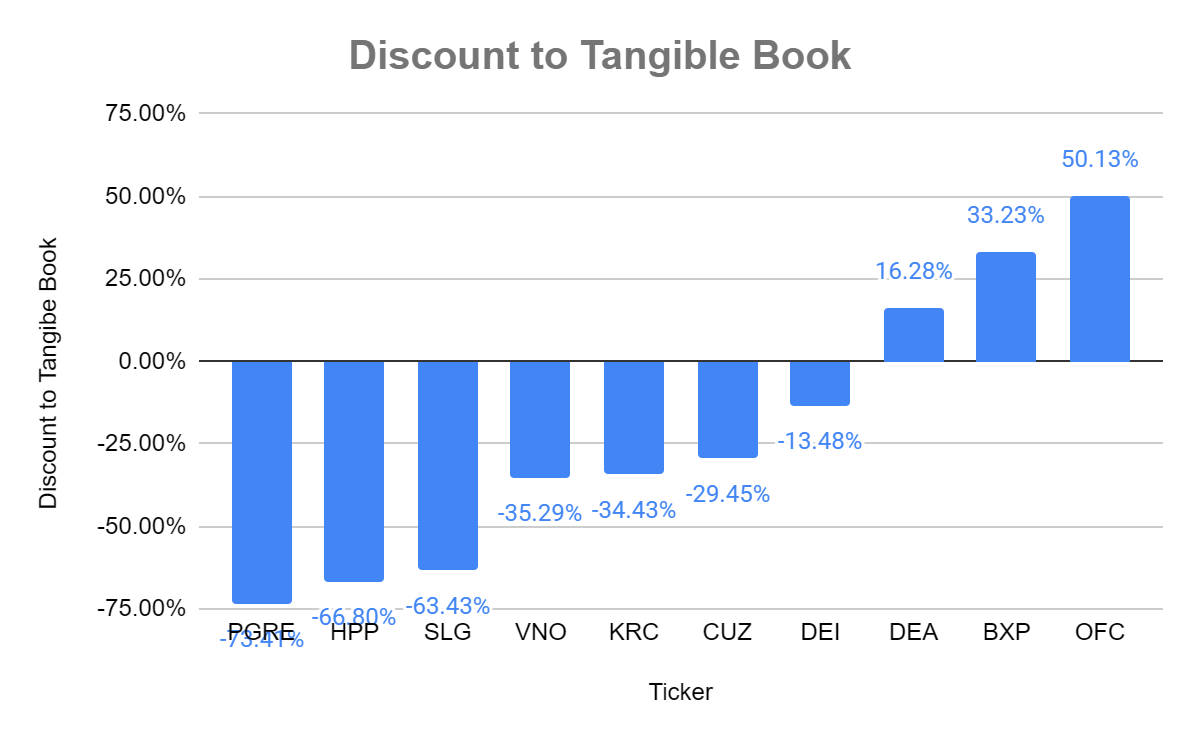

Office REITs are trading at discounted rates compared to tangible book value and the equity on their balance sheets. The peer group trades at an average discount to tangible book value of -21.66%, as only 3 of the 10 REITs trade at premiums. VNO trades at a -35.29% discount which is larger than the peer group average.

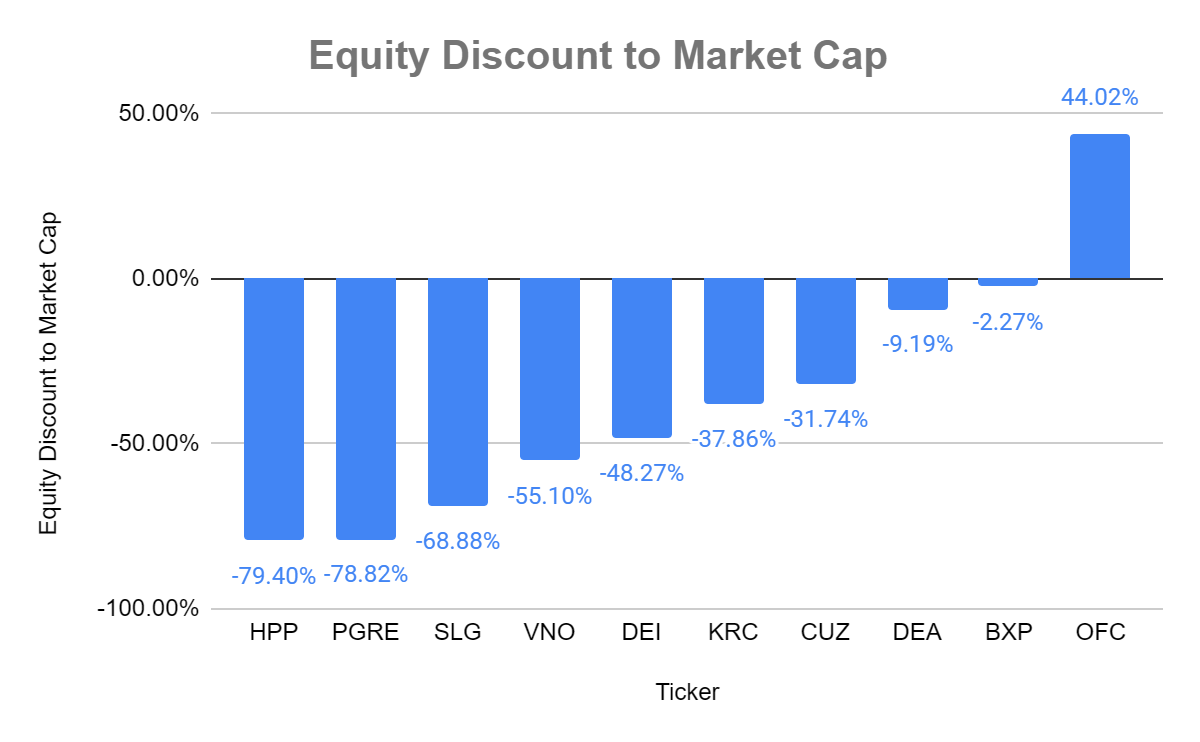

When looking at the discounted equity compared to market cap, only OFC trades at a premium. The peer group's equity is discounted at an average of -36.75%. VNO's equity is discounted by -55.10% compared to its market cap.

In both statistics, VNO looks undervalued, and the sell-off appears to be overdone compared to peer group averages. I think there is value in these shares.

{kind=link}

{kind=link}

Conclusion

I think the sell-off in several REITs has been overdone, and VNO looks like it fits into my thesis. This doesn't fit the narrative of a distressed REIT, as it has a strong liquidity position, and hedged interest rates on its debt obligations. VNO has minimal debt maturing over the next 2 years, and by the time a significant payment is required, rates should be low enough to offer favorable refinancing options. VNO trades at a steep discount to its tangible book value and equity while offering a large 9.84% yield. I am adding to my position in VNO stock as it fits my risk profile. Before investing in REITs, please do your own due diligence.

For further details see:

Why I Am Buying Vornado Realty Trust Yielding 9.84%