ARE - Why I Believe 4%-Yielding Alexandria Real Estate Is The Best Office REIT On The Market

2023-12-03 22:02:38 ET

Summary

- Office real estate segment continues to face supply risks, rising rates, and weak demand since the pandemic.

- Alexandria Real Estate Equities stands out as a strong player in the office real estate sector, focusing on healthcare and biotech companies.

- Alexandria has consistent dividend growth, strong tenants, secular tailwinds, and a decent yield, making it a favorable long-term investment in office exposure.

Introduction

When it comes to investing in real estate, I really like a number of areas, including self-storage, residential, and industrial real estate. Offices, I don't like so much.

As we will discuss in this article, the office real estate segment continues to be a minefield of risks. Supply risks are an issue, rising rates are pressuring landlords, and demand has never really recovered since the pandemic.

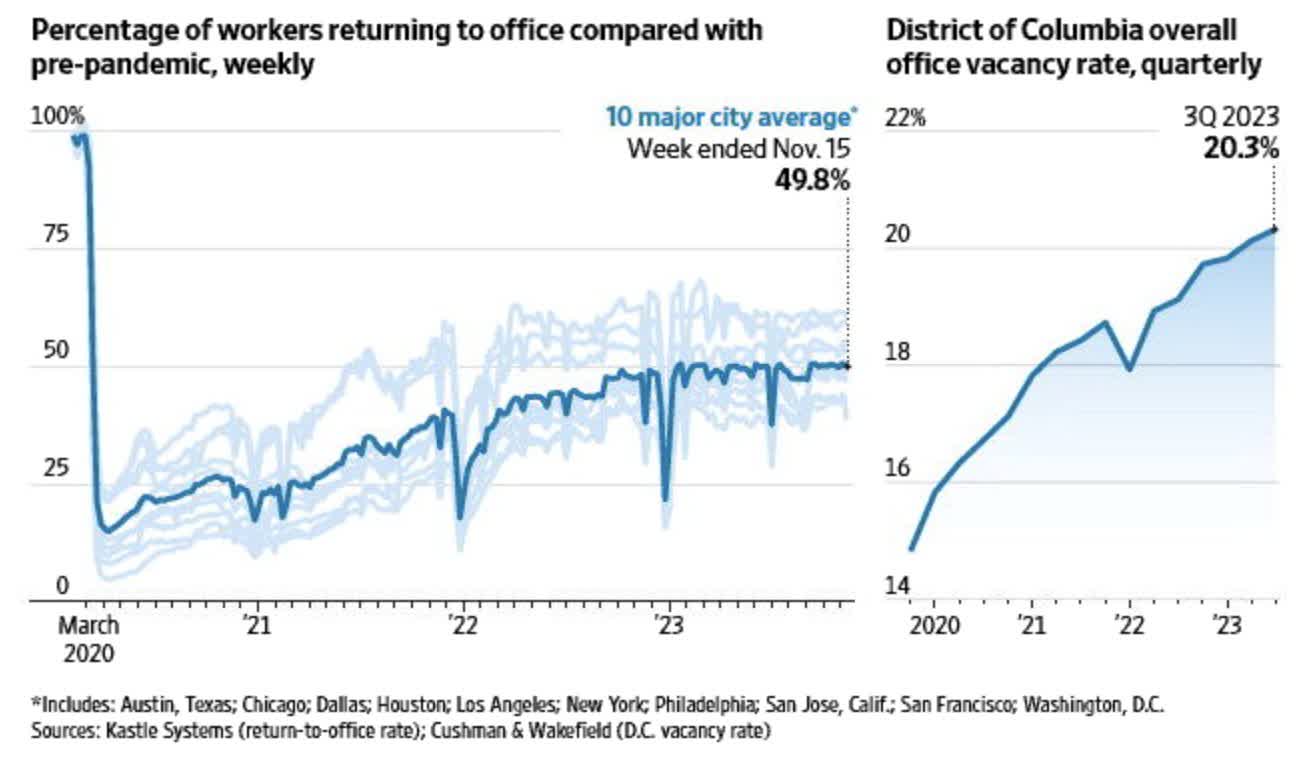

Looking at the chart below, we see that the ten major city average shows a return to the office recovery of just 50% without any meaningful upside momentum in 2023.

{kind=link}

Although I cannot make the case that anyone should have office exposure, I am dedicating this article to the one company that I really like in this space.

Alexandria Real Estate Equities ( ARE ) isn't just a random office REIT. No, the company behind the ARE ticker owns advanced offices that mainly cater to healthcare/biotech companies (no hospitals and low-margin assets).

The company has consistent dividend growth, strong tenants, secular tailwinds, and a decent yield.

If I were to buy long-term office exposure, it would be through ARE.

In this article, I'll tell you why, starting with a lecture on the macroeconomic environment.

So, let's get to it!

Offices Remain In A Bad Spot

Wells Fargo didn't protect anyone's feelings when it wrote a report titled The Office Market Remains Off-Kilter - Cyclical Headwinds Intensify As Structural Strains Persist .

As the chart above may have suggested, the bank finds that the office market is grappling with challenges as it struggles to find its footing amid the ongoing effects of hybrid work.

This has led to a significant increase in vacancy rates, reaching the highest levels since at least 2001.

In 3Q23, the national office vacancy rate soared to 13.3%, a nearly four-percentage-point increase from the 2019 average.

The availability rate, considering sublease space, reached 16.6%, marking a new high.

Wells Fargo

Major markets like San Francisco, Houston, Dallas, Denver, and Austin are experiencing availability rates exceeding 20%.

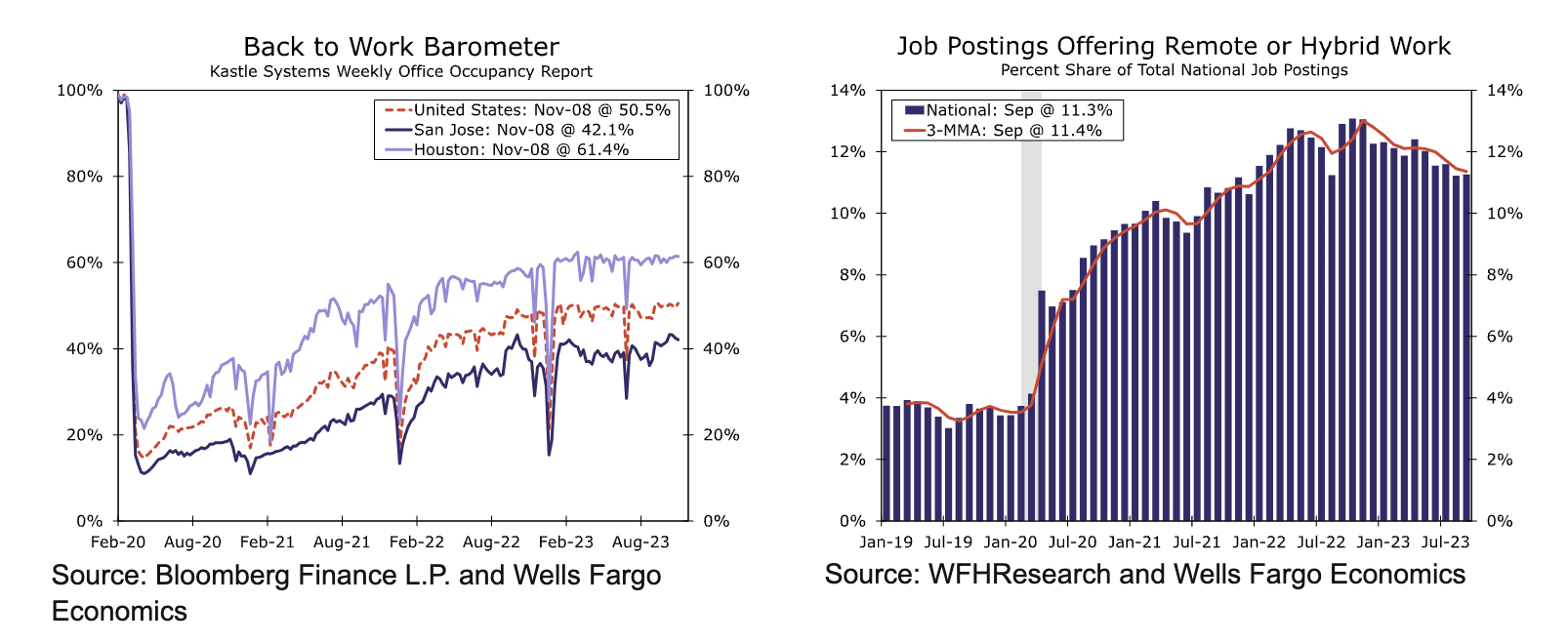

Furthermore, slower hiring in office-using industries, influenced by economic developments and technological advancements like artificial intelligence, poses an additional challenge to office demand. I think this is bad news in general, not just for office buildings.

{kind=link}

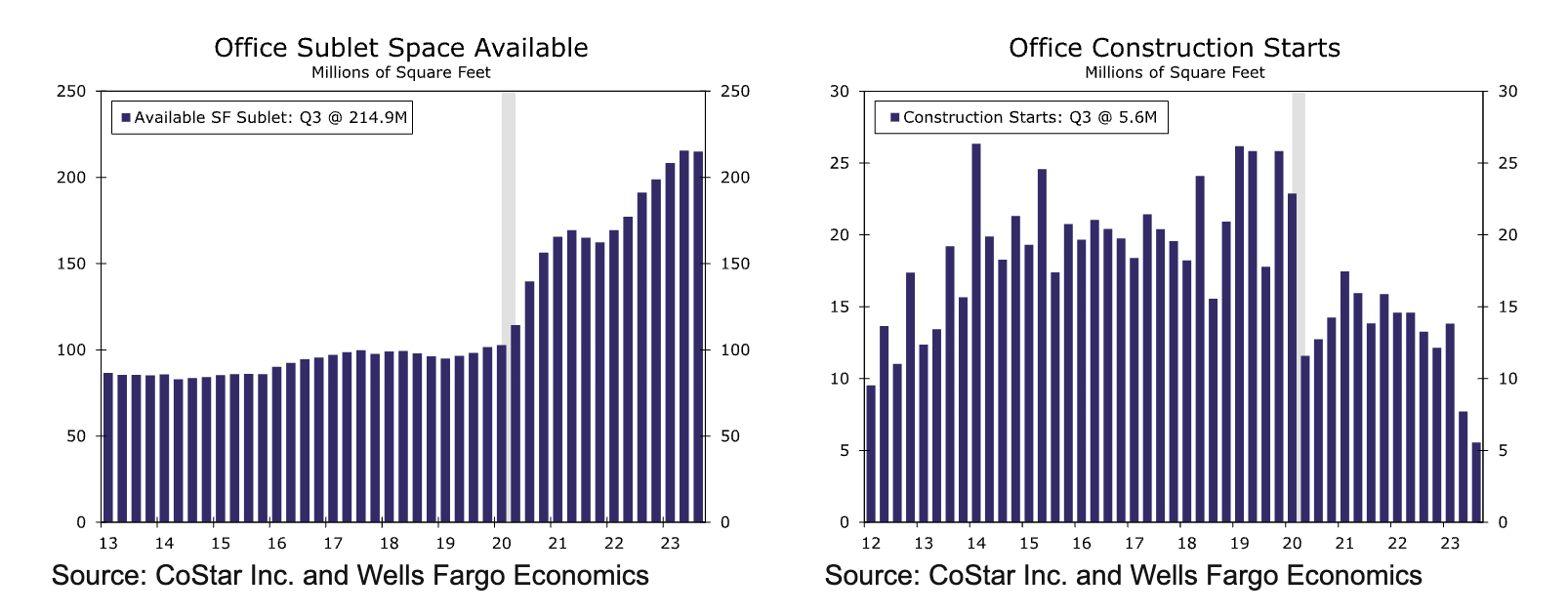

Even worse, the office market imbalance is exacerbated by a substantial increase in supply.

Sublease space continues to flood the market, and completed projects are adding inventory. Although new development has slowed significantly (as seen in the chart below), the supply overhang is likely to persist.

{kind=link}

To make things even worse, the addition of higher interest rates has led to a sharp drop in office property prices.

As of September 2023, prices were down almost 10% from the prior peak in June 2022. Rent growth has moderated, and landlords are offering concessions to retain tenants.

In other words, pricing pressure is high, demand is weak, and costs to service office CRE debt are rising.

That's a very toxic mix that tends to wipe out the weakest players.

Hence, as usual, I focus on the best of the best only.

This brings me to Alexandria.

What Makes Alexandria Such A Strong Play

I don't own physical real estate. I have almost every penny invested in dividend (growth) stocks. This includes REITs.

Although I own just two self-storage REITs, I cover almost all major areas.

When it comes to making long-term investments, I want real estate with secular tailwinds and strong demand. This includes industrial real estate, as we always need warehouses and places to build actual products.

I like residential real estate as we always need a place to live. I also like specific office real estate, as certain industries require a place to get work done.

This includes healthcare.

With a market cap of more than $20 billion, Alexandria Real Estate focuses on innovators in healthcare. This includes biotech companies.

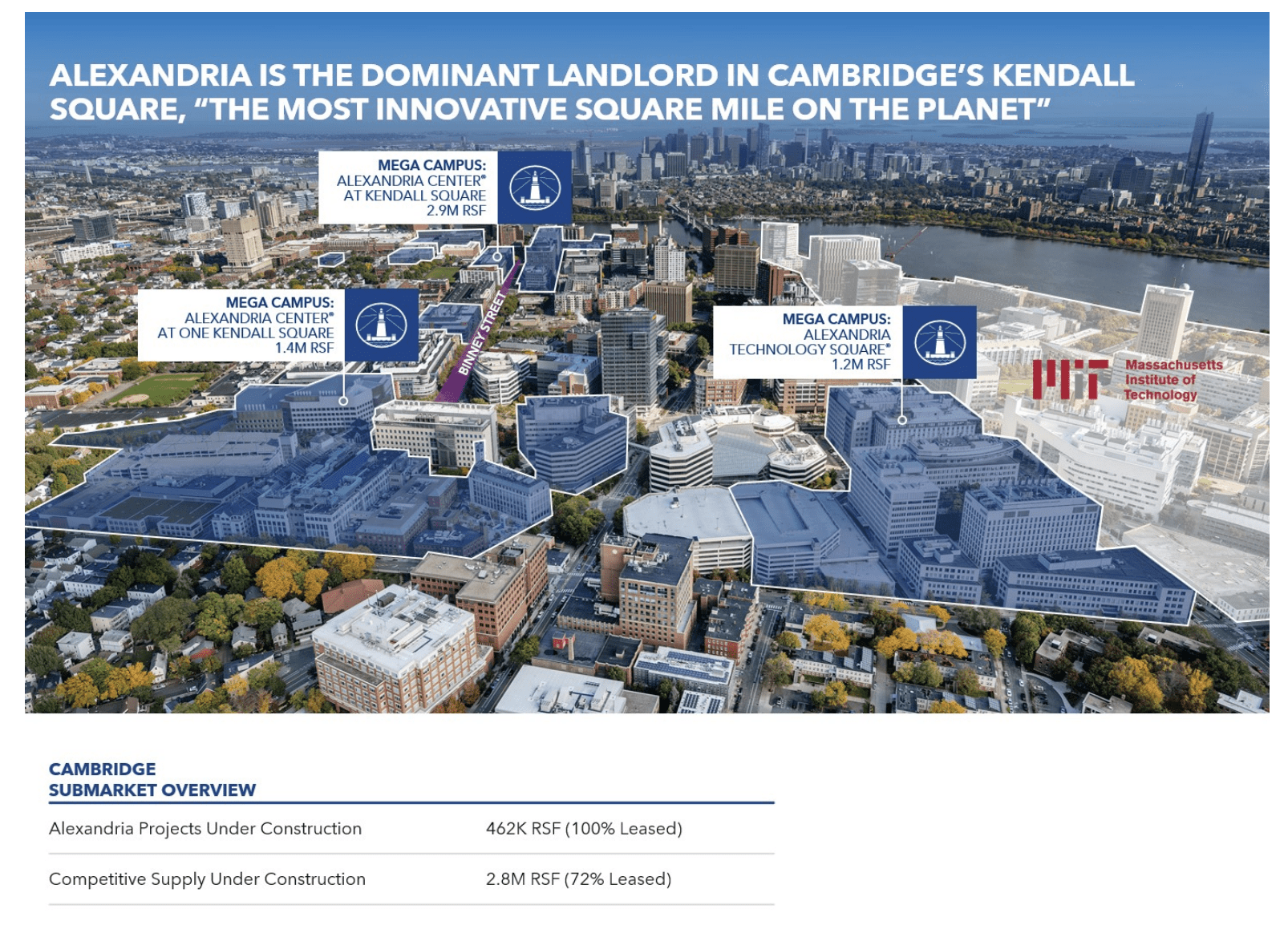

For example, the company is the biggest landlord in Cambridge's Kendall Square, which is considered to be "the most innovative square mile on the planet."

Alexandria Real Estate Equities

{kind=link}

In this market, the company has more than 460 thousand rentable square feet. 100% of it is leased.

Kendall Square in Cambridge, Massachusetts, has been called “the most innovative square mile on the planet.” It's a life science hub, hosting Biogen, Moderna, Pfizer, Takeda, and others. It's a major tech center, with Google, Microsoft, IBM, Amazon, Facebook, and Apple all occupying big chunks of pricey office space. - MIT Press Direct

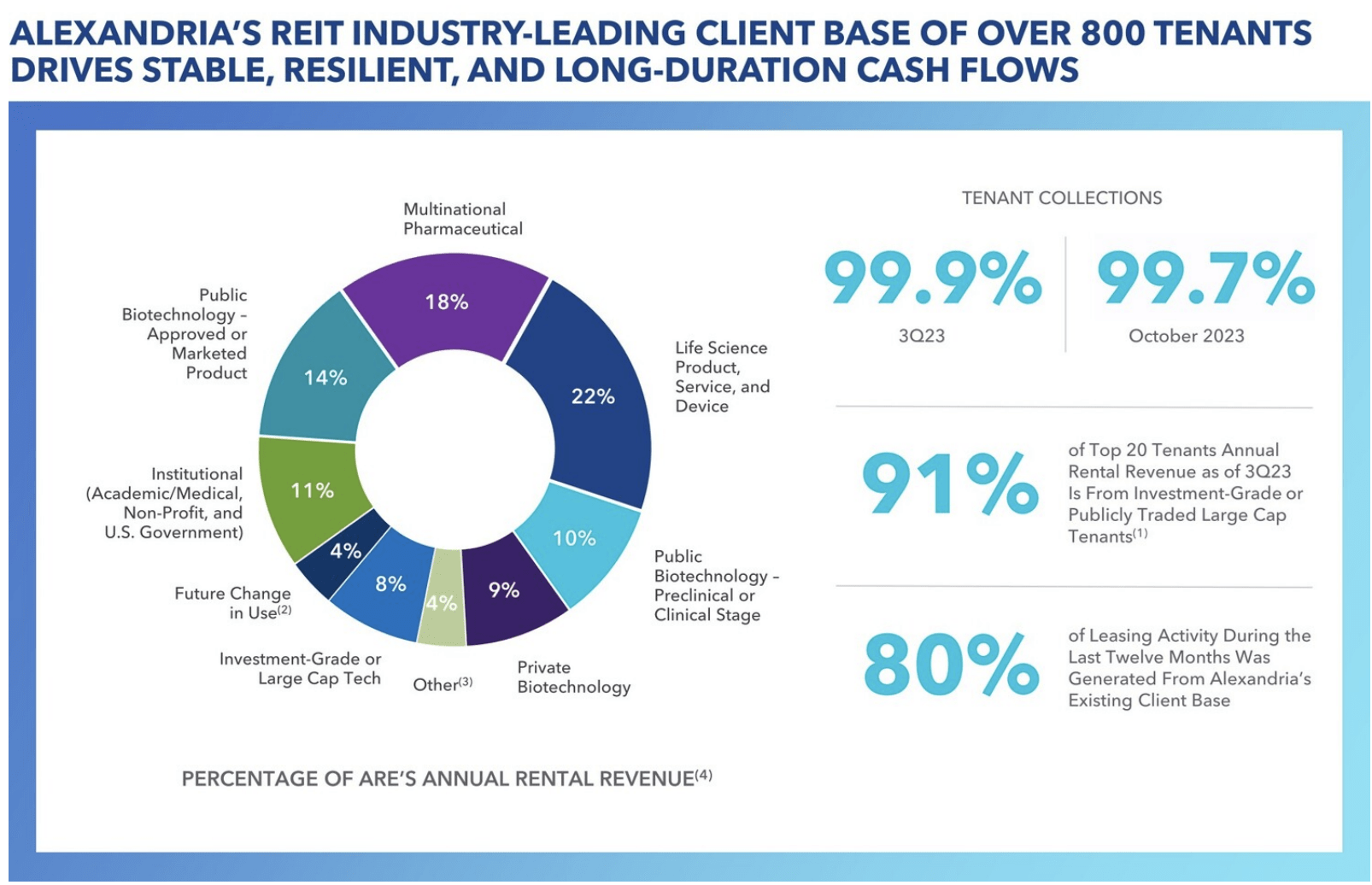

Looking at the chart below, we see that the company's tenant portfolio is dominated by biotechnology, life sciences, healthcare/research institutions, and multinational pharmaceutical companies. This results in high rent collection and subdued free cash flow volatility.

Alexandria Real Estate Equities

{kind=link}

Adding to that, this tenant base benefits from strong earnings growth, secular growth like an aging population, new healthcare threats, and AI-fueled innovation.

Even better, roughly half of its annualized rent comes from investment-grade tenants. That is extremely unique, as it is hard to get an investment-grade credit rating.

The company's mega-campus strategy is a strategy that makes it easier to target these tenants, as it allows for stronger "cluster" building, which supports innovation.

Furthermore, the average lease term going back to 2014 is 8.7 years. Year-to-date, the company has increased average new lease terms to 11.0 years, which reduces risks a bit more.

In the third quarter, internal growth remained steady, with a same-store cash NOI growth of 5.6% for the year. Occupancy is on course to reach about 95% by year-end.

Furthermore, new third-quarter leases came with an average lease term of 13 years. Leasing spreads were close to 20% on a cash basis, which is great news for longer-term internal growth.

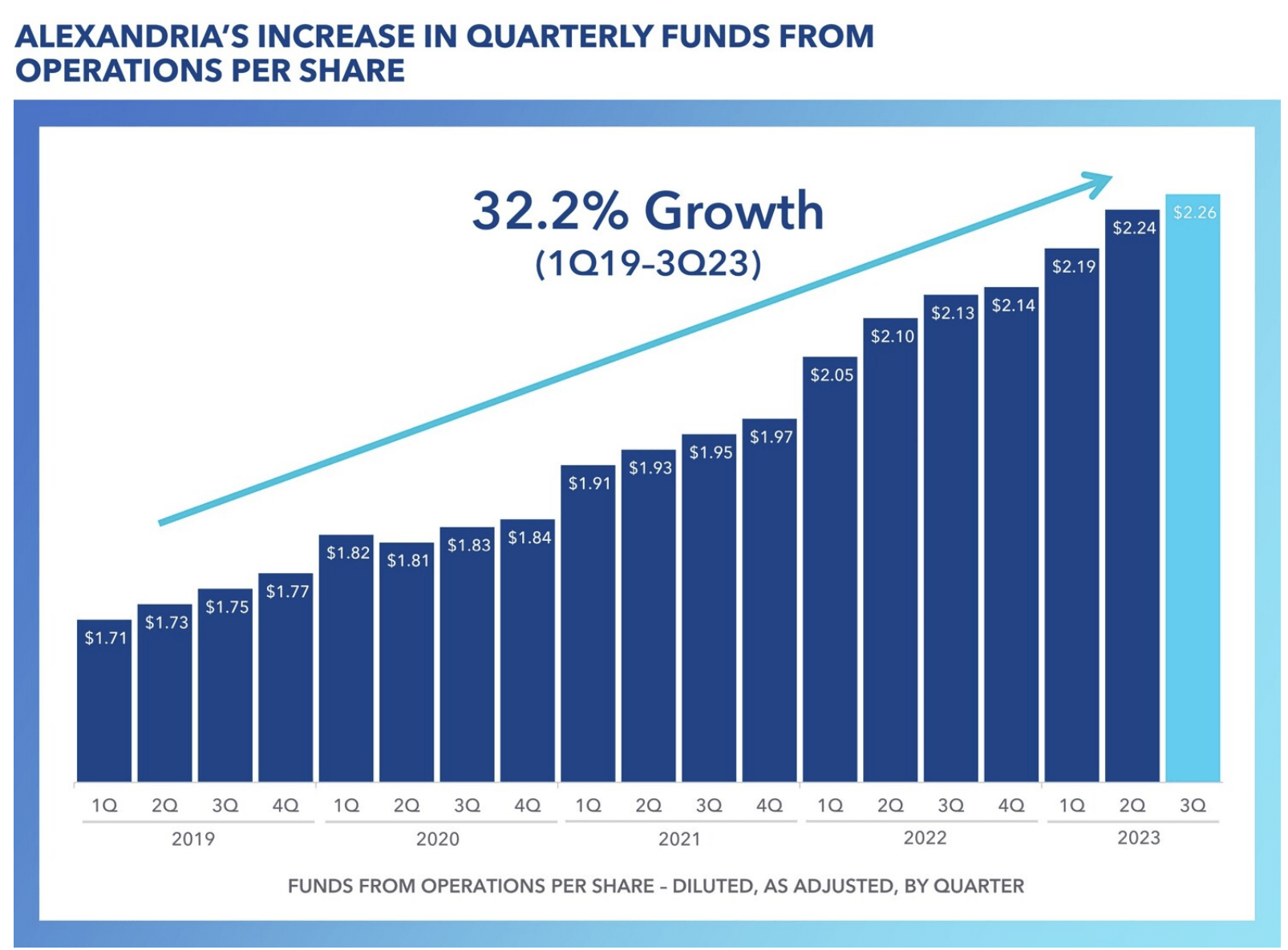

Speaking of growth and low volatility, the company has grown its funds from operations (per share) by 32% since 1Q19. During this period, it has seen just one single quarter of negative quarter-over-quarter growth. That quarter was 2Q20, the height of the pandemic. The decline back then was just 0.5%

Alexandria Real Estate Equities

{kind=link}

This also benefited its dividend.

Currently, ARE shares pay a $1.24 per share per quarter dividend. This translates to a 4.2% yield.

The five-year dividend CAGR is 6.0%, which is more than decent.

Since the Great Financial Crisis, the company has not cut its dividend.

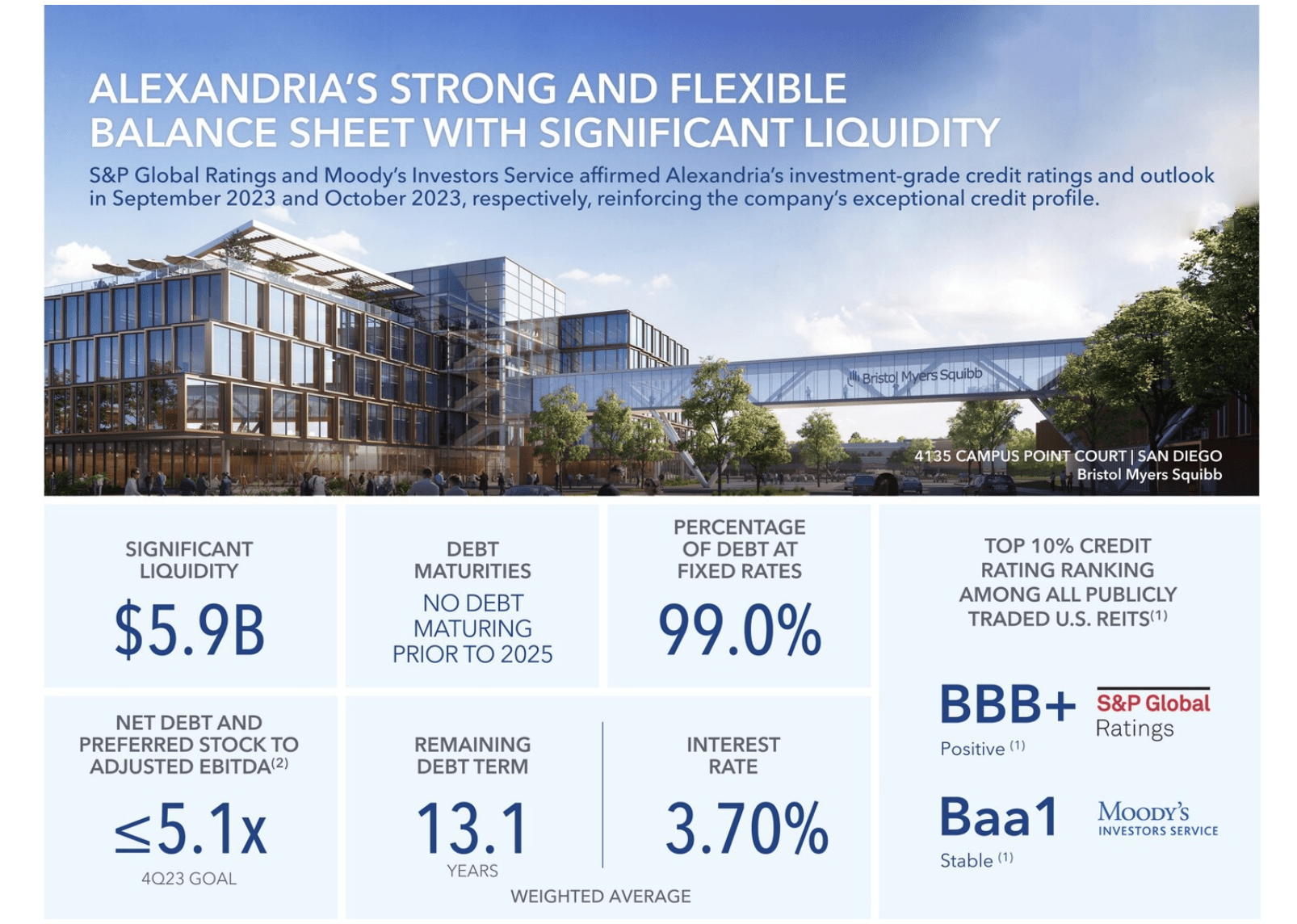

Currently, the dividend is protected by a 69% 2023E adjusted funds from operations ("AFFO") payout ratio and a healthy balance sheet.

- The company has close to $6 billion in liquidity.

- It has no maturities before 2025, which buys time in this unfavorable funding environment.

- The company aims to end this year with a net leverage ratio close to 5x (EBITDA).

- 99% of its debt has a fixed rate. This, too, protects its bottom line against elevated rates.

- The weighted average remaining debt term is 13.1 years.

- Its weighted average interest rate is 3.7%.

As a result, the company has a BBB+ credit rating, which is one step below the A-range.

Alexandria Real Estate Equities

{kind=link}

With that in mind, let's take a closer look at its valuation.

Valuation

Thanks to strong tenants, ARE is avoiding the major headwinds that its non-differentiated peers are facing.

In the third quarter, FFO per share reached $2.26, up by 6.1% compared to 3Q22.

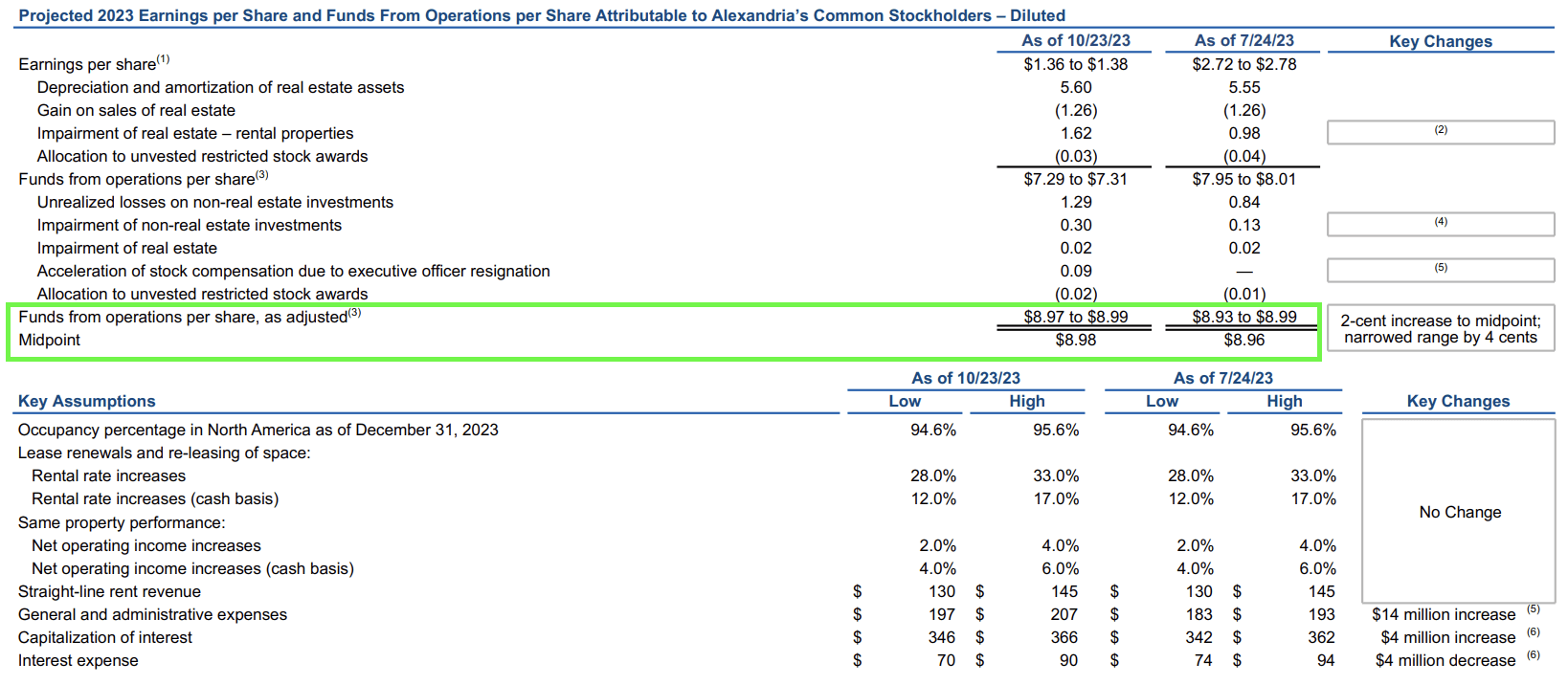

Thanks to this, the company is on track to achieve a solid year of growth in FFO per share, with a midpoint guidance of 6.7% for 2023.

FFO guidance was also hiked, as we can see in the overview below.

Alexandria Real Estate Equities

{kind=link}

Solid same-property net operating income growth was up 3.1% and 4.6% on a cash basis.

The outlook for 2023 same-property NOI growth remains solid at a midpoint of 3% to 5% on a cash basis.

Analysts believe that growth is set to last.

As we can see in the chart below:

- The company is expected to grow AFFO by 10% this year, followed by 6% and 3% growth in 2024 and 2025, respectively.

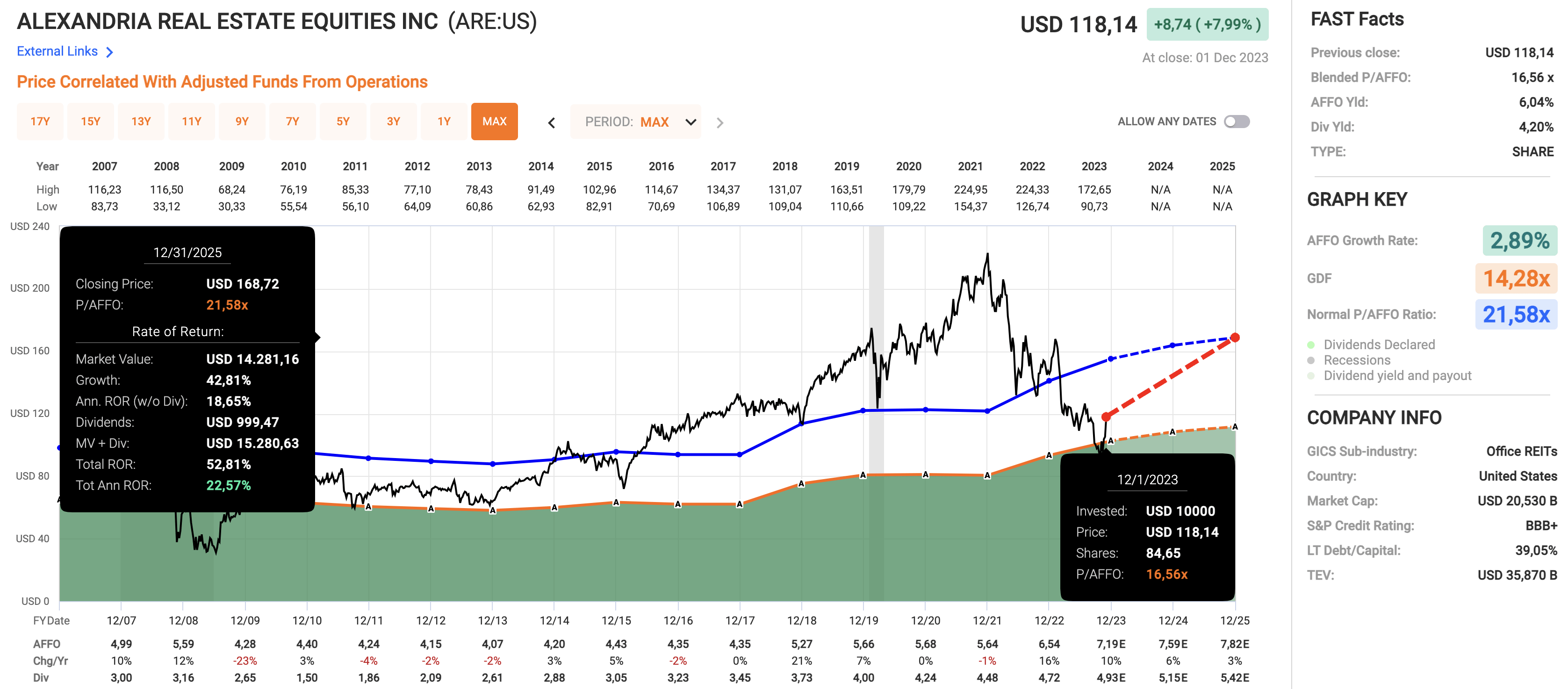

- AFFO currently trades roughly 47% below its all-time high.

- As a result of its stock price decline and steady AFFO growth, the stock trades at a blended P/AFFO multiple of 16.6x.

- The normalized valuation is 21.6x AFFO. In the first five years after the Great Financial Crisis, ARE has traded below that valuation. Between 2016 and the end of 2022, the stock has traded at a premium.

- If the company returns to its normal valuation, it could return more than 22% per year. This includes its dividend and expected AFFO growth rates.

{kind=link}

Needless to say, this is a theoretical return outlook. Elevated rates on a prolonged basis could keep the valuation subdued for a few more years.

Nonetheless, I believe these numbers not only show ARE's resilience in this market but also its longer-term potential.

Bear in mind, since the Great Financial Crisis, ARE shares have returned 11% per year.

Alexandria also outperformed the Vanguard Real Estate Index Fund ETF Shares ( VNQ ) by a wide margin over the past ten years.

If I were looking for long-term office exposure, I would go with ARE.

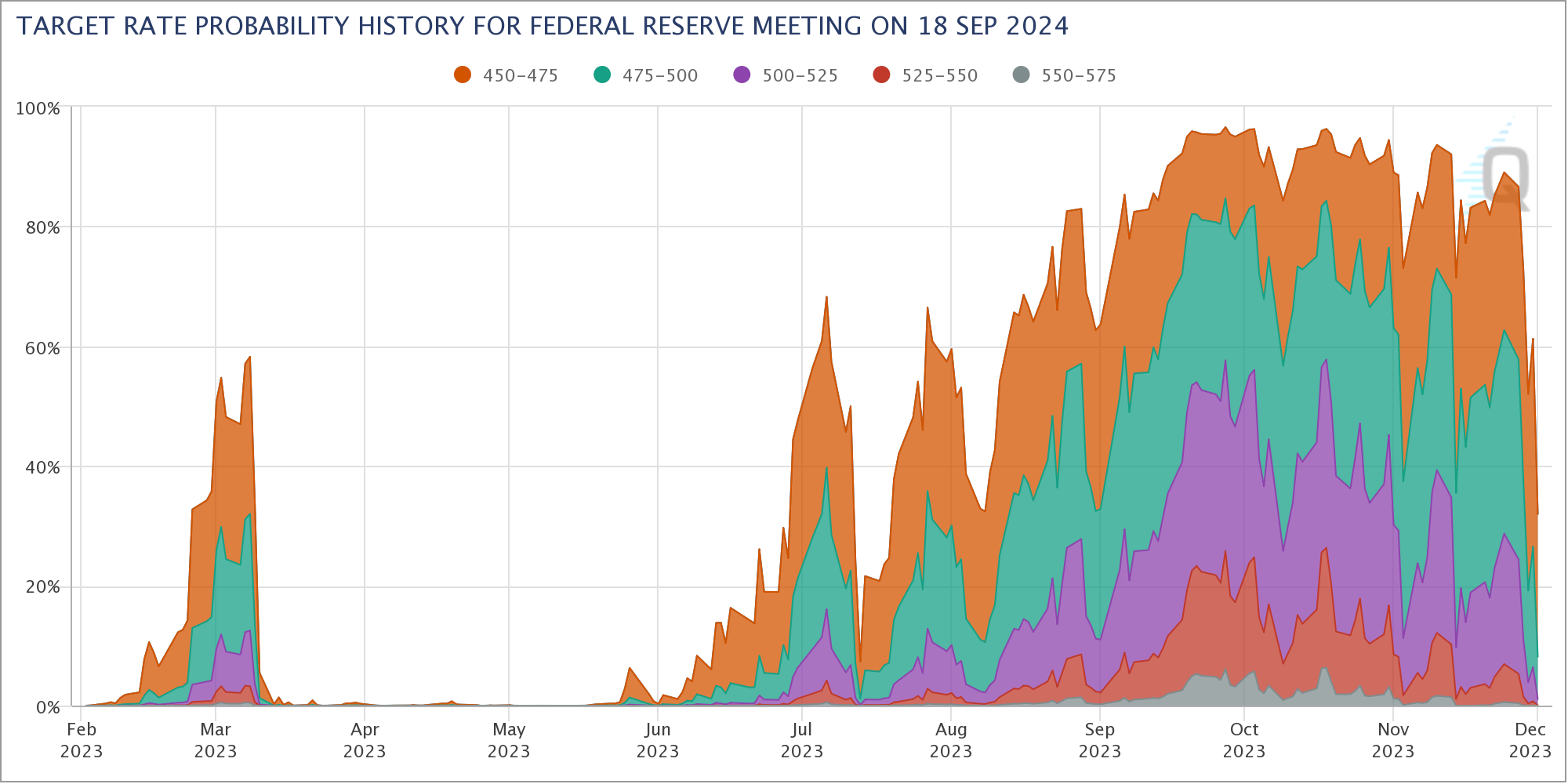

Nonetheless, although I give the stock a Buy rating, I do not rule out temporary stock price weakness.

ARE and its peers have had a very strong performance in recent months, mainly driven by the market pricing in a much more dovish Fed.

As we can see below, the implied probability of a >4.50% Federal funds rate on September 18, 2024, has dropped from almost 100% to roughly 35% within eight weeks!

{kind=link}

Due to this development and my belief that inflation will remain sticky on a prolonged basis, I have become more careful at these levels.

Having said that, the biggest takeaway is that I consider Alexandria to be an attractive company in a very risky real estate segment.

For further details see:

Why I Believe 4%-Yielding Alexandria Real Estate Is The Best Office REIT On The Market