KOS - Why I Bought Kosmos Energy

2023-07-06 06:30:00 ET

Summary

- I recently added a position in Kosmos Energy, which focuses on offshore oil production, due to its potential for significant gains.

- Michael Boyd's discounted cash flow models identify investment opportunities, recently showing an upside for Kosmos Energy of over 70%.

- Despite risks such as volatile oil prices and political issues, I believe Kosmos Energy is undervalued and recommend it to investors seeking substantial upside within a few years.

My actively invested portfolio has an Income Bucket and an Upside Bucket. Their names pretty much describe their purposes.

The Income Bucket is the focus of most of my writing. Not only is it four times the size of the Upside Bucket, it is also my main defense against a potential repeat of the 1970s.

Sometimes I hold a stock in both buckets, if I can’t find an alternative I like better. I did that with Tourmaline (TOU:CA) three months ago.

Recently, I closed that position, taking a 14% gain, and put the funds into Kosmos Energy ( KOS ). This article explains how and why I did that.

Kosmos Energy focuses on the development and production of offshore oil. They generally work in partnership with other firms, often large ones such as BP ( BP ).

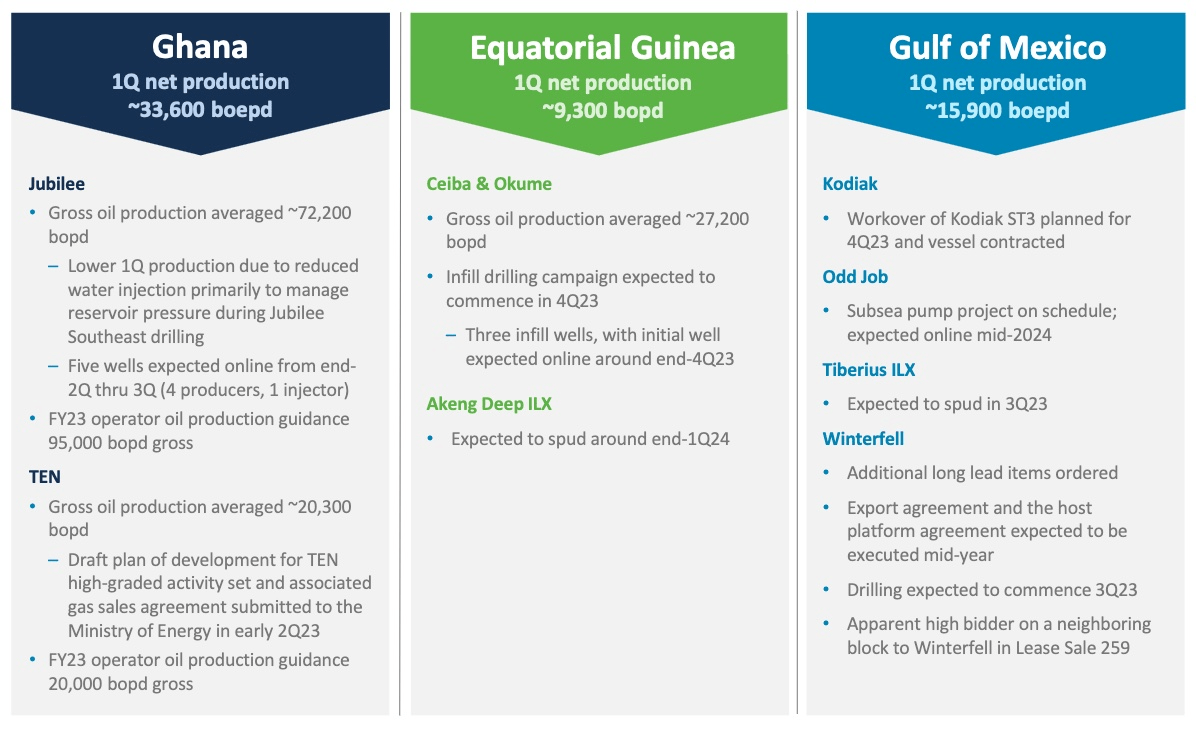

Today they have active production in Ghana, Equatorial Guinea, and the Gulf of Mexico. Net production in Q1 was 59,000 BOE/d. (BOE stands for barrel of energy, with other gases and fluids normalized to oil.)

{kind=link}

In addition, they are partners in the major “Tortue” gas field off of Mauritania and Senegal. They expect first LNG from that field in Q1 2024.

Another Valuation as a Trigger

I subscribe to Energy Investing Authority, an SA Investing Group run by Michael Boyd. Michael uses his knowledge of the industry to run discounted cash flow models (DCFs) for each firm in his coverage universe. At present he covers 29 upstream firms in the US and 19 in Canada. (He also covers 34 midstream firms.)

The DCF models for upstream energy firms are based on a 10% discount rate and the current futures strip pricing. What comes out is a set of target prices for the companies modeled. It reflects Michael’s estimate of future production volumes for each firm.

Taking these target prices as fair value, the various firms tend to move together in upside or downside. Recently the average upside for US upstream firms has been running around 20%.

Perhaps the entire sector will move up in due course. Or perhaps oil prices will drop and they all will go down. Time will tell.

The more interesting thing for me has been that, at times, some stock moves to a price that implies far more upside than the average. After such moves, those differences have tended to decrease over time, offering significant gains to those who invested.

Recently KOS showed an upside above 70% at a time when the average was 19%. I don’t chase 10% deviations, but when the upside for one stock from Michael’s models is well over three times the current average, my experience has been that there likely is something real there.

While seeing such a discrepancy is not a sufficient reason to invest, it is a sufficient reason to investigate. I never ever buy a stock I would not be willing to hold long-term, but I often buy in the hope of substantial gains within a year or two.

My View of the Kosmos Story

Michael has emphasized in recent articles that Kosmos is very near the end of a period of high capital intensity and is about to reap the benefits of substantial increases in production. He sees DACF, or Debt Adjusted Cash Flow, increasing by 30% from 2023 to 2024.

The forward increase in production and revenues also comes through clearly in the Kosmos investor presentation and in a recent article by FluidsDoc.

And quoting the from the press release that came with Q1 earnings:

Chief Executive Officer Andrew G. Inglis said: “Kosmos delivered solid performance in the first quarter and moved the company closer to the expected mid-year free cash flow inflection point. We have three development projects underway that aim to increase production by around 50% from current levels.

FluidsDoc, writing in April when the price was $8, had a price target well above Michael’s value of $9.50.

{kind=link}

But KOS has sagged since early May. Today the price is below $6. I see no good reason for this and believe that markets behave in irrational ways, as did Benjamin Graham and as does Howard Marks. This is no surprise if one considers the general poor quality of human thinking and also the many incentives that drive institutional investors away from a focus on fair value.

In particular, the market often fails to credit the value of developments like this until they are realized. Investors who believe that intrinsic value is accurate and only represented by current earnings are likely to miss opportunities that come from looking ahead.

My view is that pricing KOS anywhere in the range of $5 to $8 is not giving them credit for the coming increase in production. But the increase in production is likely to be realized within the next year, along with an inflection in free cash flow. In due course the market is very likely to give the stock credit for this.

So I bought KOS at $5.48. Notionally, I will sell after 50% upside.

The Risks

KOS is far from the lowest-cost producer, at near $50 per barrel today. A sag in oil prices would reduce or even eliminate their profits while it lasted, which in turn would likely impact the stock price.

But on a midcycle basis, and pro forma for their increases in production within the next year, KOS is very underpriced today. An additional boost will come because their new projects will lower their cost production.

Of course, there are also all the political risks associated with offshore oil. I like that Kosmos is dealing with several different countries, implicitly leveraging the potential to vary their emphasis depending on how they are treated.

Who Should Invest

Kosmos is small and the price is volatile. Don’t invest if that will be intolerable for you.

They do not pay a dividend and will not do so for some years. Net Debt/EBITDA is above 2x, which is not where E&Ps want to live. Paying that down will come before any shareholder returns. So do not invest any funds from which you need dividends any time soon.

Growth investors may want to consider KOS. But the burst of growth coming up will not continue unabated. They will have to find a next set of opportunities to grow more, and one cannot know how that will go.

That said, the assets they are developing now should be very long-lived and should sustain a valuation well above the present one. To my mind, investors seeking positions likely to have substantial upside within a small number of years are the best candidates to buy KOS. That’s why I did.

For further details see:

Why I Bought Kosmos Energy