REGN - Why I Expect Regeneron To Keep Delivering For Investors In 2024 (Upgrade)

2024-01-08 18:51:51 ET

Summary

- Regeneron Pharmaceuticals, Inc.'s shares have risen over 25% in recent months, reaching over $910 per share - a premium explained partly by share buybacks.

- The company's market cap is around $100 billion, despite generating substantially lower revenues compared to larger Pharmas such as, e.g., Gilead Sciences and Bristol Myers Squibb.

- Regeneron has consistently delivered profitable net income, however, and management may be prepared to start paying a dividend soon.

- Regeneron's success is built on the success of eye disease therapy Eylea, and immunology drug Dupixent, co-developed with Sanofi. These 2 drugs offer multi-billion dollar revenue streams that ought to last until the end of the decade.

- The company also has a burgeoning oncology pipeline also, and a proven ability to innovate and unlock lucrative market opportunities. That is why I am not necessarily put off by a ~$900 per share price tag and believe $1k is an achievable target.

Investment Overview

Shares in Regeneron Pharmaceuticals, Inc. ( REGN ), the Tarrytown, New York State-based Pharma company, have been rising sharply in recent months, from $725 in mid-August 2023, to >$910 at the time of writing - up >25%.

Regeneron's share float is only just over 100m, and its market cap valuation currently hovers around the $100bn mark. Arguably, that is a generous valuation for a company that has generated top line revenues of $6.6bn, $8.5bn, $16.1bn, and $12.2bn in the past 4 years to 2022, and is likely to report a figure in the region of ~$13bn for 2023, representing a price to sales ratio of ~8x. For context, the California-based Pharma giant Gilead Sciences, Inc. ( GILD ), market cap of $103bn, posted revenues of $27bn in 2022, its P/S ratio being ~4x.

At the same time, however, Regeneron is a profitable pharmaceutical company that has delivered net income of $2.1bn, $3.5bn, $8.1bn and $4.4bn over the same period (Gilead Sciences earned net income of $4.5bn in 2022). Based on management's 2023 guidance, which was updated when Q3 earnings were reported last November, net income is likely to come in at ~$4.8bn in 2023, which ought to translate to earnings per share ("EPS") of ~$46, and a price to earnings ratio of ~20x.

Regeneron is not yet a dividend-paying company, unlike its larger Pharma rivals, whose average payout is in the region of ~3%, although the company has repurchased ~11.7bn worth of shares since 2019, including $1.9bn across the first three quarters of 2023. In a recent fireside chat at the Piper Sandler Healthcare conference, the company's outgoing Chief Financial Officer ("CFO"), Bob Landry, who will retire next month, told the audience:

I personally think that it's probably in the foreseeable future in which Regeneron will become a dividend-paying stock.

Paying a dividend would certainly help to de-risk Regeneron shares in the eyes of potential investors, although since falling to a share price low of ~$275 in 2019, Regeneron stock has delivered a period of strong and steady growth. Shares are +130% over a 5-year period, and up 30% across the past 6 months.

When considering Regeneron stock, investors ought to take into account the fact that the stock price is trading at an all-time high, although if we analyze the Pharma's strengths, weaknesses, opportunities, and threats, as I will do in this post, we can certainly make the case that the company fully deserves this valuation.

Regeneron, like all Pharmas, faces some challenging issues in 2024, such as the looming patent expiry of its lead and most valuable asset, the eye disease therapy Eylea, increasing competition from rivals marketing similar drugs to Eylea in its key markets, its reliance on collaboration revenues from its 2 major Pharma partners, Sanofi (SNY) and Bayer Aktiengesellschaft (BAYZF), and successfully securing approvals for a range of new pipeline assets designed to offset any lost revenues due to, e.g., patent expiries, and grow the company's top line.

Despite these risks, in previous posts on Regeneron I have often pointed to management's unerring ability to find ways to overcome obstacles and keep outperforming, whether through innovative marketing, new product ideas, big Pharma partnerships, and, more recently, developing a wider range of late-stage pipeline assets - as a major characteristic and strength of the company.

As such, and as I will share in this article, although I would not make Regeneron shares a screaming buy at present, due to their premium, all-time high price, based on the chances of the company successfully diversifying itself as an oncology-first company over time, to ease the reliance on dupixent and eylea, I do think it can flourish in the longer term, and perhaps shares can rise above $1k this year.

In November 2022, when I last covered the company for Seeking Alpha , shares traded at $750, and I advised readers to look to buy any upcoming dips as opposed to paying such a high price. 15 months on, with shares up 22% since that note, I am tempted to give the same advice, as I expect there to be bumps in the road as Regeneron attempts to make the transition from a medium-sized Pharma, heavily reliant on 2 major drug products, to a more diversified, independent company, with revenues and net income as large as rivals such as Gilead Sciences, or fellow California based Pharma Amgen Inc. ( AMGN ).

Regeneron Overview - Phenomenal Sales Of Eylea Set To Continue For Foreseeable Future

Although Regeneron's pipeline is diverse and impressive, and we should also note the company boasted a cash position of >$15.5bn as of Q3 2023, versus long-term debt of just ~$2bn, meaning there are plenty of funds available for making M&A deals to bolster it, there is no question that Eylea and Dupixent are the company's crown jewel assets.

Eylea has been approved to treat the "wet" form of advanced macular degeneration ("wet amd") since 2011, and has also secured approvals in age-related macular degeneration ((AMD)), diabetic macular edema ((DME)), and macular edema following retinal vein occlusion ((RVO)). Regeneron markets and sells the vascular endothelial growth factor ((VEGF)) inhibitor in the U.S., with German Pharma partner Bayer marketing and selling it in Europe, splitting profits from sales equally with Regeneron. Regeneron also earns a 33.5% - 40% share of sales of Eylea in Japan, via Bayer's distribution partner in the region.

Revenues from Eylea in the U.S. were $5bn in 2020, $5.8bn in 2021, and $6.3bn in 2022, while Bayer collaboration revenues over the same period were $1.2bn, $1.4bn, and $1.44bn. In short, Eylea is big business for Regeneron and has underpinned the company's rise in revenues and valuation since its 2011 approval.

Eylea has generally been the "best in class" or "standard of care" drug in its indication throughout its life as a commercial product, resisting multiple challenges from the likes of Swiss Pharma's Roche Holding AG ( RHHBY ) and Novartis AG ( NVS ), but Roche's latest product, Vabysmo - a bispecific antibody that targets both vascular endothelial growth factor ((VEGF)) and angiopoietin-2 (Ang-2) - has been shown in studies to have a longer-lasting effect, and the drug has been taking market share away from Eylea in 2023.

9-month Eylea revenues in 2023 came to $4.4bn in the U.S., implying the full-year figure will be lower than last year, but Regeneron already has a solution to its Vabysmo problem, having secured approval last year for Eylea HD, an 8mg injection with 12- and 16-week dosing regimens, against standard Eylea's 8-week dosing regime. With this approval, Regeneron has quickly been able to re-take best-in-class status from Roche and Vabysmo - Regeneron's VP of Investor Relations had this to say during the recent Piper Sandler fireside chat:

our view is EYLEA HD addressed the primary unmet need in this space, which was duration, Bob mentioned the PULSAR study. And the second year, by the end of the second year, almost half, 47% of patients were eligible for every 20-week or every 24-week dosing, that's pretty good, when you are down to two or three injections per year. And I think doctors are going to want to see their patients at least a couple of times a year to ensure that vision is not being lost, that they are not seeing fluid re-accumulate. So, I think the unmet need has been met with EYLEA HD in large part.

In the first half of 2023, Vabysmo generated >$1bn in revenues, while in Q3, Regeneron reported $1.45bn of Eylea revenues, down from $1.63bn in the prior year period. Sales of Eylea HD - launched with 6 weeks of Q3 remaining - were $43m, but it seems likely the new drug's market share will grow rapidly, perhaps even exceeding the older version's ~45% market share in the future, providing Regeneron with many more years of >$5bn revenue contributions.

There are other threats to Eylea's market dominance, most notably the launch of biosimilar versions of Eylea, developed by the likes of Amgen, Alvotech ( ALVO ), Samsung Bioepis, Viatris Inc. ( VTRS ) and others. Once biosimilars are permitted to be sold - when Eylea's patents run out or are successfully challenged via the courts by a biosimilar drug developer - the average price of the product is likely to fall dramatically and Regeneron's market share will likely decrease amid all of the new competition.

Regeneron has been fighting numerous legal battles against several of the above companies, recently winning its case against Viatris, successfully arguing that Viatris' drug violates a patent not due to expire until 2027. Key patents will expire in 2024, however the presence of longer-lasting Eylea HD in the market may keep biosimilars at bay for a few more years yet.

Without doubt, Eylea HD revenues in 2024 will be one of the most closely watched figured by analysts, and may have a greater effect on Regeneron's share price performance than any other factor.

Dupixent Offers Major Long-Term Revenue Growth

Dupixent, which Regeneron developed in collaboration with French Pharma Sanofi, has been a major success story for Regeneron and is arguably as important to the company as Eylea. According to a statement in Regeneron's Q3 quarterly report / 10-Q submission :

We co-commercialize Dupixent in the United States and in certain countries outside the United States. We supply certain commercial bulk products to Sanofi. We and Sanofi equally share profits and losses from sales within the United States. We and Sanofi share profits outside the United States on a sliding scale based on sales starting at 65% (Sanofi)/35% (us) and ending at 55% (Sanofi)/45% (us), and share losses outside the United States at 55% (Sanofi)/45% (us).

Global net sales of Dupixent - which is approved for atopic dermatitis, asthma, and chronic rhinosinusitis, amongst other immunology indications - were $3.1bn in Q3 2023, up 33% year-on-year. According to Regeneron, there are now more than 750k patients using the therapy worldwide. Speaking on the Q3 earnings call , Regeneron's head of Commercial Marion McCourt commented:

In atopic dermatitis, Dupixent's largest indication, we continue to see more than 20% growth six years post-launch. Physicians have great confidence from the combination of efficacy, safety and ease of use across all age groups, including as young as six months.

In short, Dupixent has emerged as something of a wonder drug, approved in 5 indications, and has generated "positive pivotal results in seven Type 2 allergic diseases," according to Regeneron's Q3 earnings presentation .

Analysts have speculated the drug could break $20bn in peak revenues per annum, if approvals in new markets such as Chronic Obstructive Pulmonary Disease ("COPD"), and Regeneron's share of these revenues is expected to increase in the long term, as the company has been paying off a liability of ~$2.5bn that has been accumulated with Sanofi, with part of its profits from Dupixent - once this liability is cleared, CFO Landry suggested this could happen around 2026, the profit share will increase significantly.

Dupixent earned $8.4bn of revenues in 2023 to the end of Q3 - with that figure potentially doubling by 2030 - in Dupixent, Regeneron appears to have a strong source of de-risked revenue to sustain it well into next decade.

Late (& Early) Stage Drug Pipeline Provides Future-Proofing

Besides Eylea and Dupixent, Regeneron earns a revenue share of Sanofi's sales of Kevzara, a rheumatoid arthritis therapy, and on U.S. and ex-U.S. sales of Libtayo, a programmed death receptor-1 (PD-1) blocking antibody, indicated for non-small cell lung cancer ("NSCLC"), and earning revenues of $620m in 2023, to Q3.

Regeneron purchased the full rights to Libtayo - which has the same mechanism of action as Merck & Co., Inc.'s (MRK) <$20bn per annum selling Keytruda, or Bristol Myers Squibb Company's (BMY) >$7bn per annum selling opdivo - from Sanofi in 2022. Whether the company can secure further approvals for its immuno-oncology drug - or extract "blockbuster" (>$1bn per annum) revenues from this source - is hard to predict, but armed with a substantial R&D budget - the company says it invested $4.4bn into R&D in 2023 - you can certainly make the case that the drug's potential has not been fully tapped to date.

Regeneron earns a small amount - <$250m in the first three quarters of 2023 - from 2 cholesterol therapies, Evkeeza, and Praluent, while Inmazeb, to treat zaire ebolavirus, and Veopoz, recently approved to treat the ultra-rare condition CHAPLE disease, also make small revenue contributions.

Within Regeneron's late-stage pipeline, however, there are several intriguing, potential blockbuster revenue opportunities. The Phase 3 stage LAG-3 inhibitor Fianlimab could be approved after 2025, Regeneron management believes, in combo with Libtayo in melanoma. BMY has successfully combined Opdivo with a LAG-3 inhibitor to create Opdualog, a drug approved last year in melanoma, with management suggesting peak revenue expectations of $4bn may be achievable.

Itepekimab, a monoclonal antibody that targets interleukin (IL?33), is also being developed for approval in COPD - management will be hoping it can mirror the success of Dupixent. Veopoz is thought to have label expansion opportunities into C-5 mediated diseases, alongside cemdisiran, an investigational RNAi therapeutic being developed in partnership with the RNA-interference giant Alnylam Pharmaceuticals, Inc. ( ALNY ).

Its is hoped that Garetosmab, a monoclonal antibody targeting activin A, will gain approval to treat fibrodysplasia ossificans progressiva ("FOP"), which has a prevalence of 0.65m patients in North America, while there are 4 more major oncology candidates to consider.

REGN5678, an anti-PSMAxCD28 bispecific costimulatory antibody indicated for prostate cancer, has faced setbacks on safety, including patient deaths in a study alongside libtayo, but Odronextamab, a CD20xCD3 bispecific antibody, could win FDA approval in March in the indications of diffuse large C-cell lymphoma ("DLBCL") and follicular lymphoma, potentially opening up a $500m peak revenue opportunity.

Linvoseltimab, undergoing a Phase 3 confirmatory study in multiple myeloma, is a bispecific antibody, like Odronextamab, and pending approval, is designed to challenge cell therapies such as BMY's Abecma in this double-digit billion marketplace, while a third bispecific, Davutamig, is targeting NSCLC, and a fourth, Ubamatamab, ovarian cancer.

Concluding Thoughts - Optimistic Modelling Suggests Regeneron Trades At A Premium - But Upside In 2024 May Be Expected Nonetheless

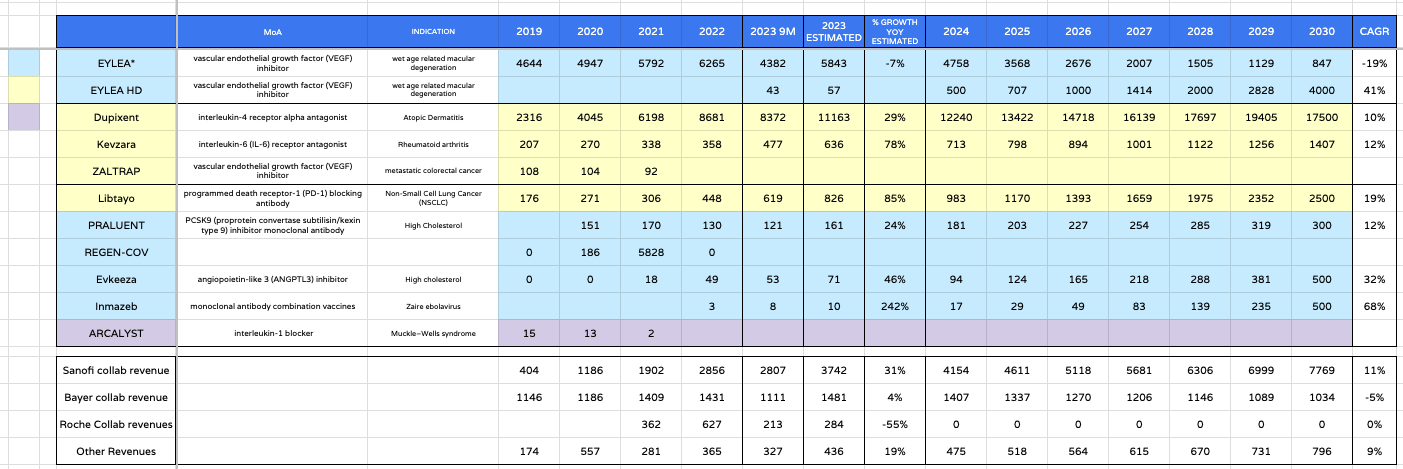

To try to determine what a "fair value" price to pay for Regeneron shares may be, I prepared some ballpark revenue estimates for the company's current product portfolio, plus collaboration revenues as follows (n.b. I disregard Arcalyst and ZALTRAP revenues after 2022, as Regeneron's own statements no longer include them).

Regeneron product and collaboration revenue forecasts (my table and figures)

{kind=link}

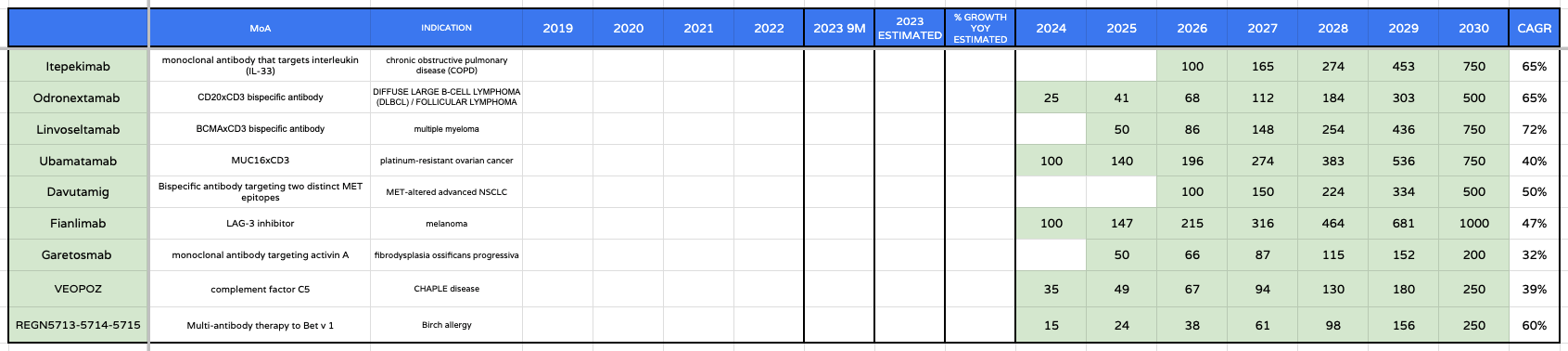

I also estimate the forward revenue prospects of a selection of Regeneron's late-stage pipeline assets, as below (using a highly optimistic scenario in which they all successfully gain approval), as follows:

Regeneron product pipeline forecast revenues (my table and assumtions)

{kind=link}

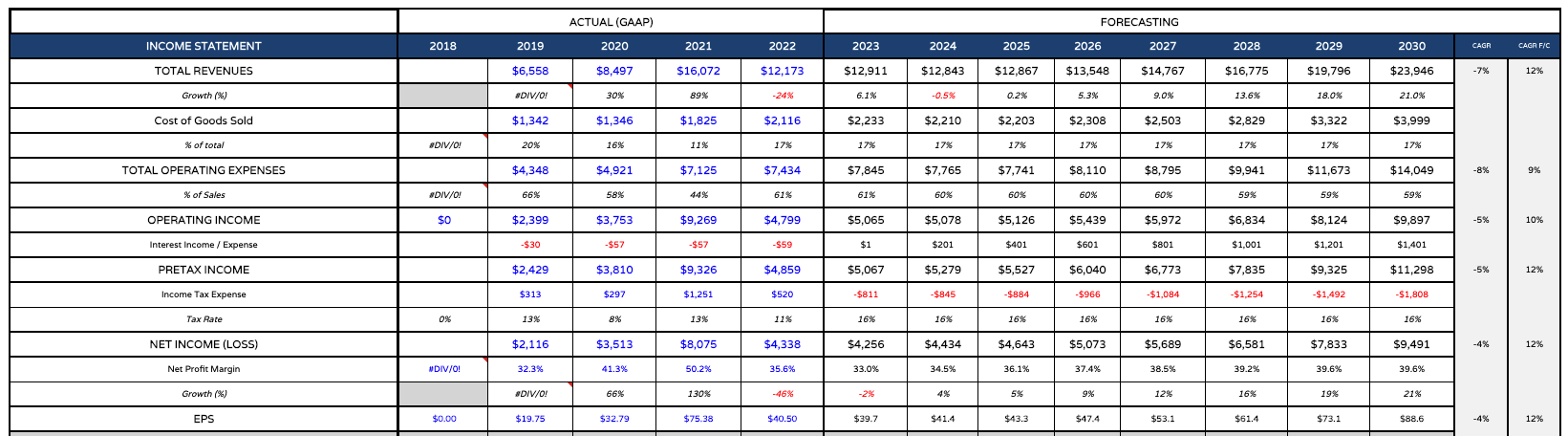

Adding these numbers together, I project a forward income statement for Regeneron as follows:

{kind=link}

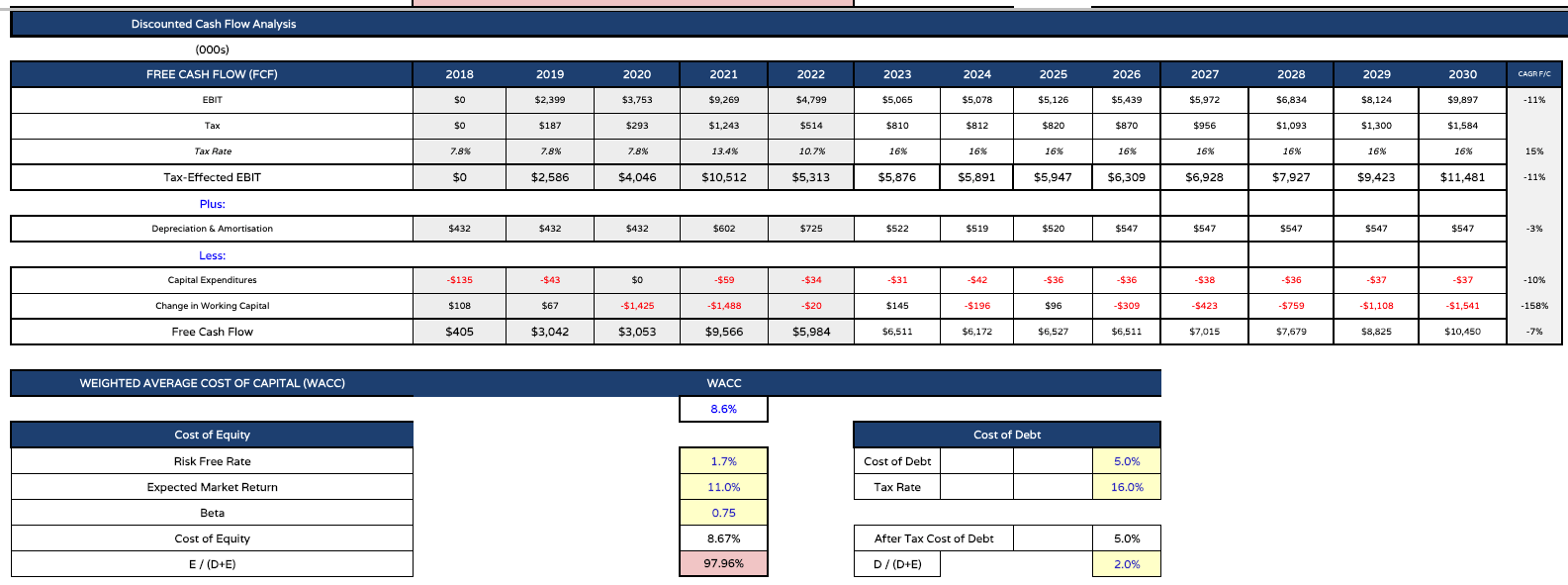

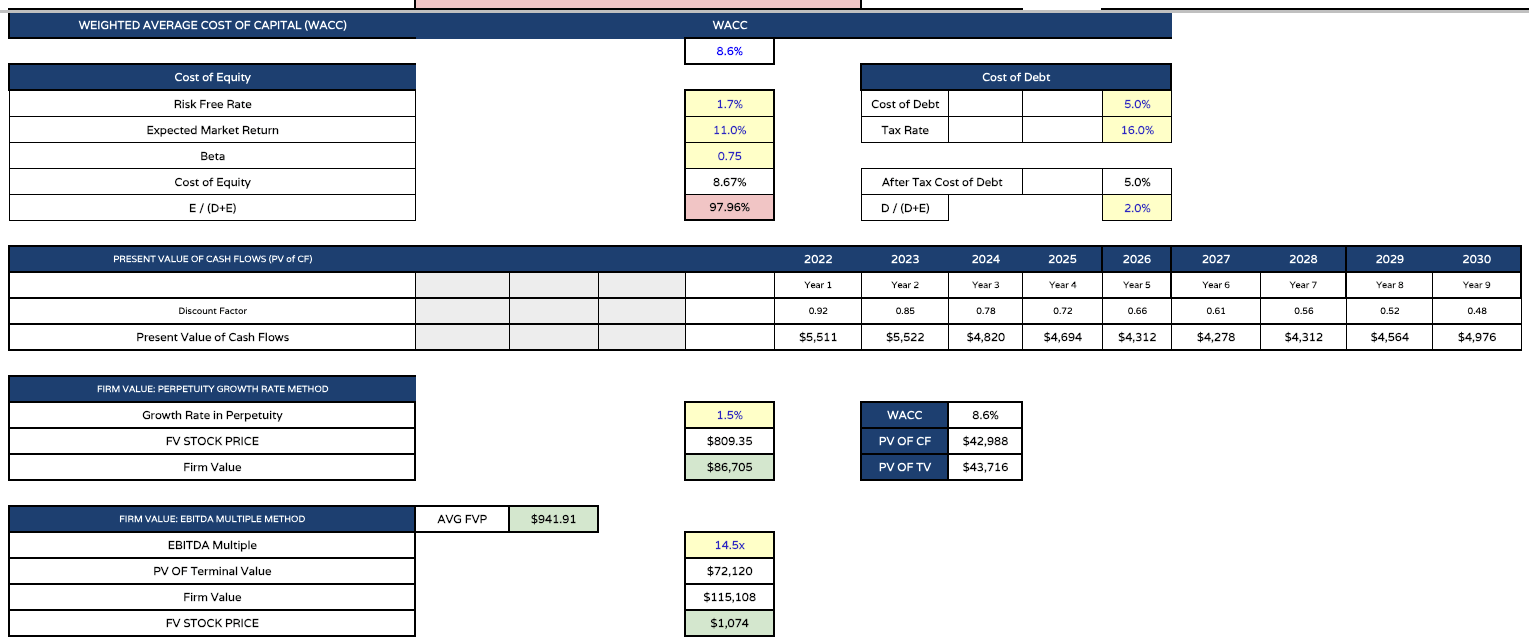

Next, I calculate cash flow and a suitable weighted average cost of capital to use:

Regeneron forward cash flow calculation (my table and forecasts)

{kind=link}

And finally, I can present a "ballpark" share price target for Regeneron stock, using discounted cash flow ("DCF") analysis:

share price target for regeneron using CF (my table and calculations)

{kind=link}

As we can, using the average of the EBITA multiple calculation method, and perpetuity growth rate method, my calculated share price target for Regeneron stock is $942 per share, or a 6% premium to current traded price.

This target is not intended to be set in stone as there are numerous unknown's in play, such as whether certain drugs will gain approval and meet my peak sales targets, and I have been more generous than usual by setting a low WACC percentage. On balance, however, given some drugs may not secure approval, while others may strongly outperform expectations, I believe it paints a reasonably realistic picture of what Regeneron the business will look like by the end of the decade. Still a significant reliance on Dupixent and Eylea, but offset by a thriving new oncology division.

As mentioned in my intro, Regeneron trades at a premium price based on several fundamental - price to sales, price to earnings etc. - measures, and it takes an optimistic model to calculate a share price target that implies Regeneron stock has further upside potential.

One of the qualities that is most important in the world of Pharma, however, is the ability to innovate and, although this may be a non-scientific statement - "be lucky." Regeneron will argue that it has made its ow luck through hard work, but either way, based on the company's and management's historic resilience and disproportionate number of successes, it would be my contention that Regeneron stock can break through the $1k per share barrier in 2024, and that that is not necessarily poor value to an investor, given the ongoing revenue potential of flagship assets dupixent and eylea, strong supporting cast of late-stage pipeline assets, and promise of a dividend in the coming years.

Nevertheless, a more cautious investor may want to wait for a dip created by a jittery market before making an investment. In Pharma, one is generally never far away, but Regeneron Pharmaceuticals, Inc. has every opportunity to bounce back quickly from a selloff in 2024, with multiple major data readouts and approval shots upcoming (see the Q3 earnings presentation for a full list), that would ordinarily give its share price a decent bump, if they prove successful, as seems likely.

For further details see:

Why I Expect Regeneron To Keep Delivering For Investors In 2024 (Upgrade)