PSA - Why I'm Aggressively Buying Public Storage This Year

Summary

- Public Storage has a terrible dividend scorecard, thanks to no dividend growth since 2016 and a subdued yield. PSA has also underperformed its peers over the past ten years.

- However, the company is everything except a pet rock. Aggressive investments in growth, high margins, and a healthy balance sheet provide the way for new dividend growth.

- While the self-storage industry remains healthy, I expect that macroeconomic headwinds provide us with juicy buying opportunities in 2023.

Introduction

The stock market is truly in a challenging situation. Global economic growth is consistently declining, indicating a high recession likelihood. On top of that, inflation is persistently high, supply chain and structural labor issues are still present, and the Federal Reserve is eager to hike until it complies with its 2% inflation mandate again. Public Storage ( PSA ) has been one of the first dividend holdings of my portfolio, which I started in 2020. The company hasn't hiked its dividend once since 2016, and its stock price is 20% lower compared to 12 months ago. Yet, I'm not giving up on the stock. On the contrary, I decided to stick with it, making it the core of what will be much more real estate exposure in the years ahead. The company continues to maintain an incredible portfolio of top-tier assets. Moreover, it has high margins, a fantastic all-weather balance sheet, and persistent industry tailwinds, despite the aforementioned economic troubles. I also believe that aggressive dividend growth will return sooner than later. This could fix the stock price underperformance versus its peers.

FINVIZ

With all of this said, let me guide you through my thoughts!

On a side note, I also own its peer Extra Space Storage ( EXR ).

What's PSA?

For the purpose of this article, I'm quickly listing some facts, so investors who are new to PSA have a better understanding of what we're dealing with here (especially for the macroeconomic parts of this article).

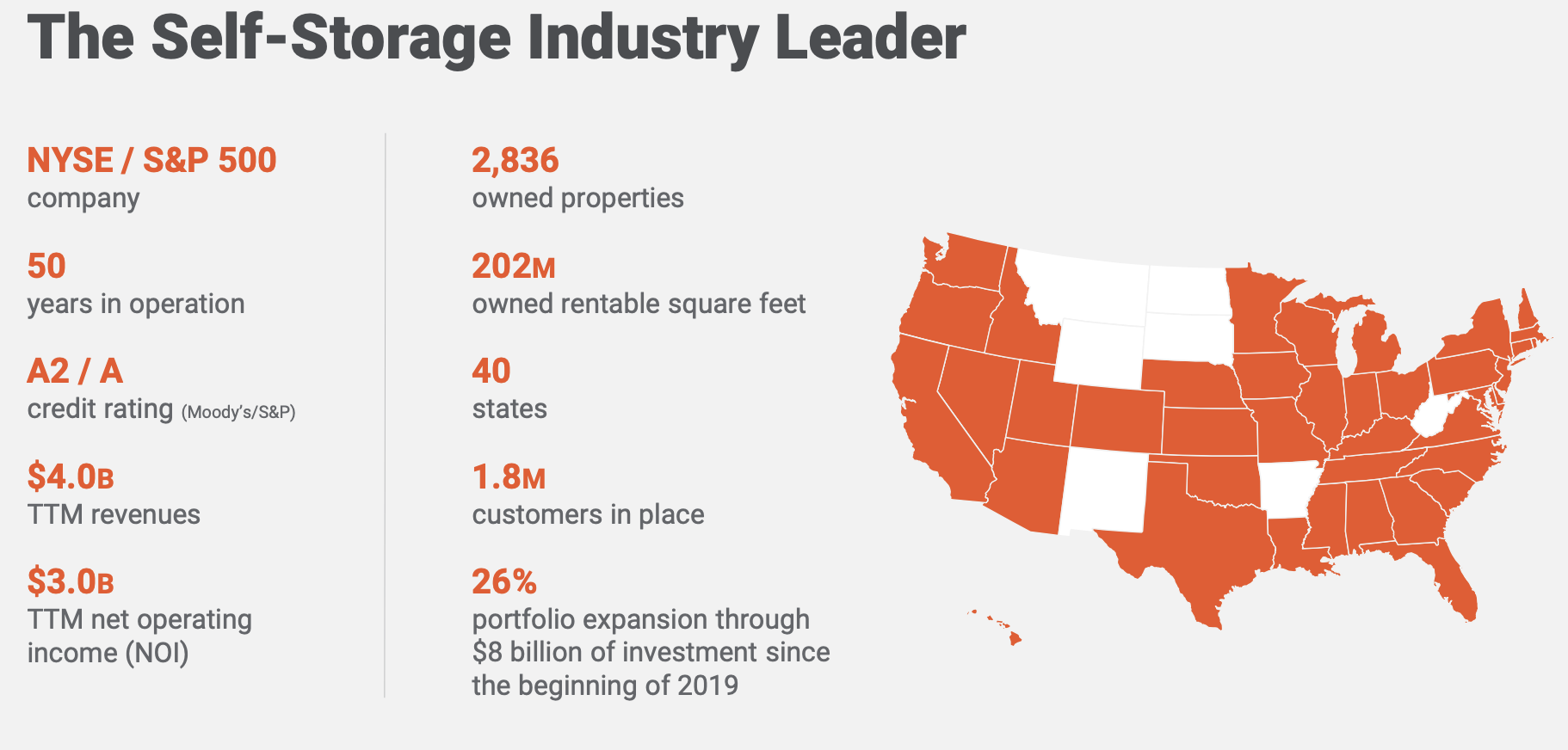

With a market cap of $48.7 billion, Public Storage is the nation's largest self-storage real estate investment trust. This makes the company a part of the industrial REIT industry.

Founded roughly 50 years ago, PSA has become a real estate operator covering more than 2,800 properties in 40 states, servicing 1.8 million customers.

{kind=link}

As we'll discuss in much greater detail, the Glendale, California, based company is one of the few major REITs with an A-rated balance sheet. Since 2019, the company has expanded its portfolio by 26%, which explains the dividend growth numbers I'm about to show you.

The company's largest market is the greater Los Angeles area, where it generates 17% of its same-store net operating income.

While the company is not the fastest-growing operator in its industry, it does have high margins thanks to a very efficient business model.

{kind=link}

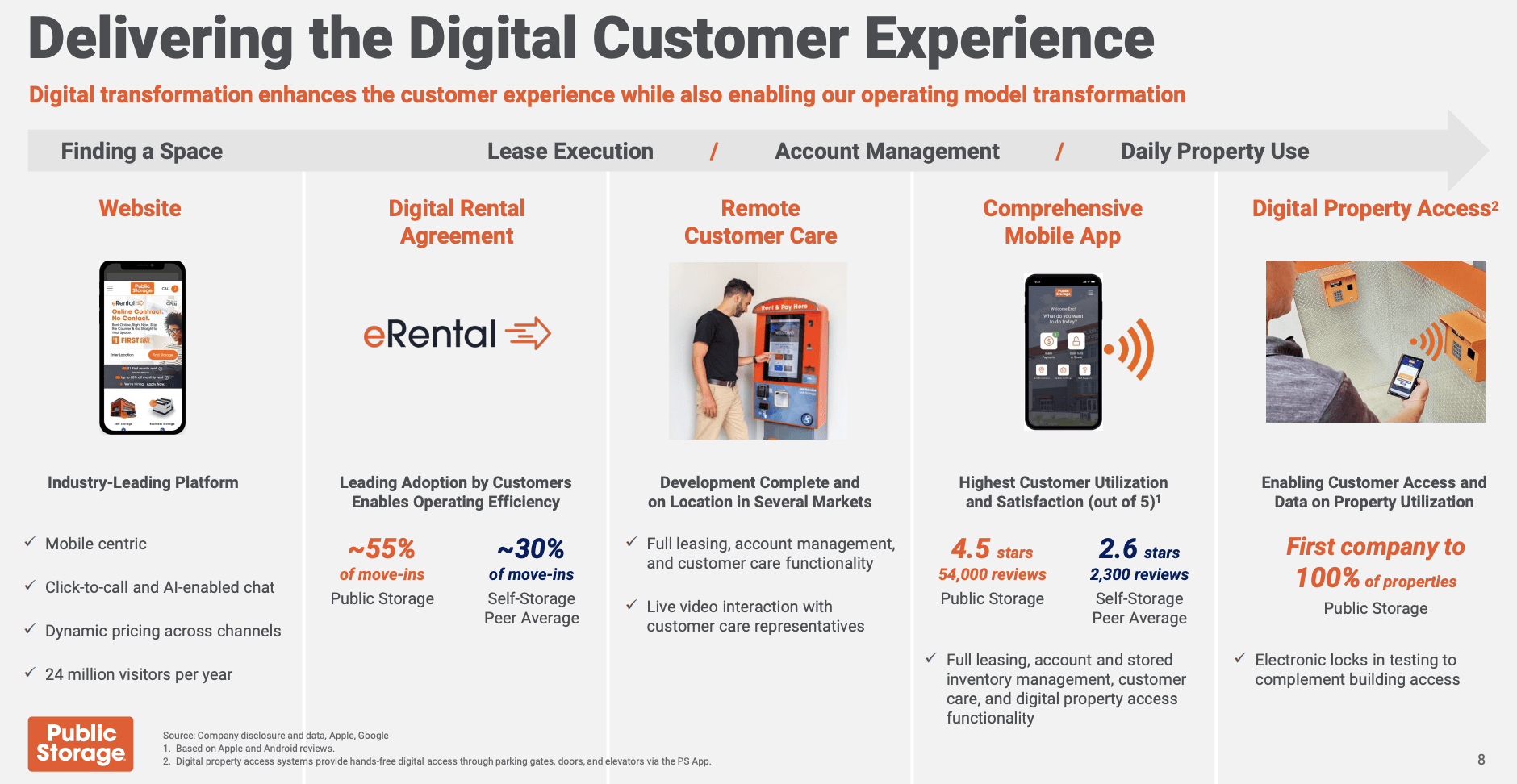

The company is increasingly transforming its business, incorporating technologies that make it harder for non-"professional" operators to compete. After all, the entry barriers in this industry are very low. Operators who figure out how to gain an edge can exploit that.

{kind=link}

Since 2004, the company has grown its net operating income by 5.2% per year. This beats the real estate sector average by 240 basis points per year, resulting in 146% cumulative growth, beating the industry sector by 84 percentage points.

Unfortunately, the company was unable to beat its industry peers over the past ten years, while crushing its sector peers.

One of the reasons why PSA wasn't able to keep up with its peers is the total lack of dividend growth, which we will discuss now.

PSA Looks Terrible At First Sight. Let's Look Closer!

Let's say you go to a car dealership where the first car you see has too many miles, a history of mechanical failures, and a price that just isn't competitive. You'll probably ignore that car.

While I would never compare my beloved Public Storage to a terrible car, the company is suffering from the same thing: bad news at first sight. Investors assess these basic facts and decide to skip the stock.

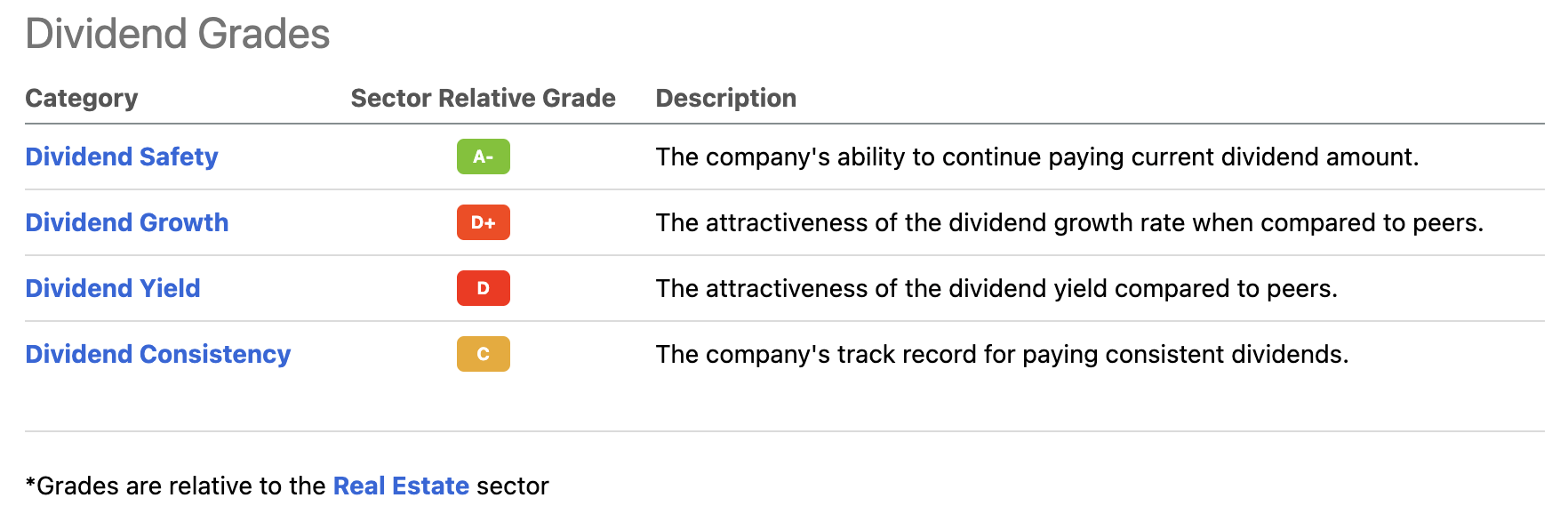

Looking at the Seeking Alpha dividend scorecard below, we see that Public Storage scores very low on dividend growth, very low on its dividend yield, and poorly on dividend consistency. Ugh...

{kind=link}

These are relative scores versus the real estate sector, which we'll discuss in greater detail.

Dividend Safety

Dividend safety is the company's biggest strength, according to the dividend scorecard. That is no surprise as the company has a strong business and a subdued payout ratio due to a lack of dividend growth.

Using the numbers behind the score, we see that the company has an AFFO (adjusted funds from operations) payout ratio of 61%. The sector median is 73%. Moreover, the company's net leverage ratio is 2.0x EBITDA, which is well below the sector median of 6.0x.

With that said, when incorporating preferred equity, the leverage ratio increases to 3.3x, which is still extremely healthy. The company's long-term target is 4.0x-5.0x, meaning there is debt capacity to fund additional growth along with annual retained cash flow.

{kind=link}

Roughly $2.2 billion worth of debt is due before 2027. Moreover, thanks to its healthy debt ratio and efficient business, the company's A-rated credit rating provides great rates. Its largest outstanding debt position, $700 million worth of notes due in 2024, is yielding just 47 basis points above the SOFR rate.

Moreover, the company complies with all of its financial covenants , which also shows tremendous financial flexibility.

Included in these covenants are ("A") a maximum Debt to Total Assets of 65% (approximately 14% at September 30, 2022) and ("B") a minimum ratio of Adjusted EBITDA to Interest Expense of 1.5x (approximately 25x for the twelve months ended September 30, 2022) as well as covenants limiting the amount we can encumber our properties with mortgage debt.

Dividend Yield/Growth/Consistency

As all of these things are connected, I'm going to throw them into the same basket.

Essentially, we're dealing with a stock with an average compounding dividend growth rate of 0.00% over the past five years.

Unfortunately, the long-term dividend chart has been messed up by a special dividend paid on August 4, when the company paid a $13.15 special dividend. This was the result of a $2.3 billion tax gain from the sale of PS Business Parks to Blackstone ( BX ). The company was legally obligated to distribute these funds.

Looking at the base dividend only, the company has not hiked its dividend since October 2016 when management announced an 11.1% increase to $2.00 per share. Since then, investors have not enjoyed another hike.

The company currently yields 2.9%, which is now close to the longer-term median of 3%. I'm looking to buy more aggressively with a yield above 3%.

Before 2016, the company consistently hiked by double-digits, letting shareholders benefit from high growth in net operating income.

At this point, it is important to mention that the company isn't neglecting shareholders. While I understand that people do not want stocks with inconsistent dividend growth, I like to look at the bigger picture, incorporating somewhat of an ownership mentality when assessing my investments.

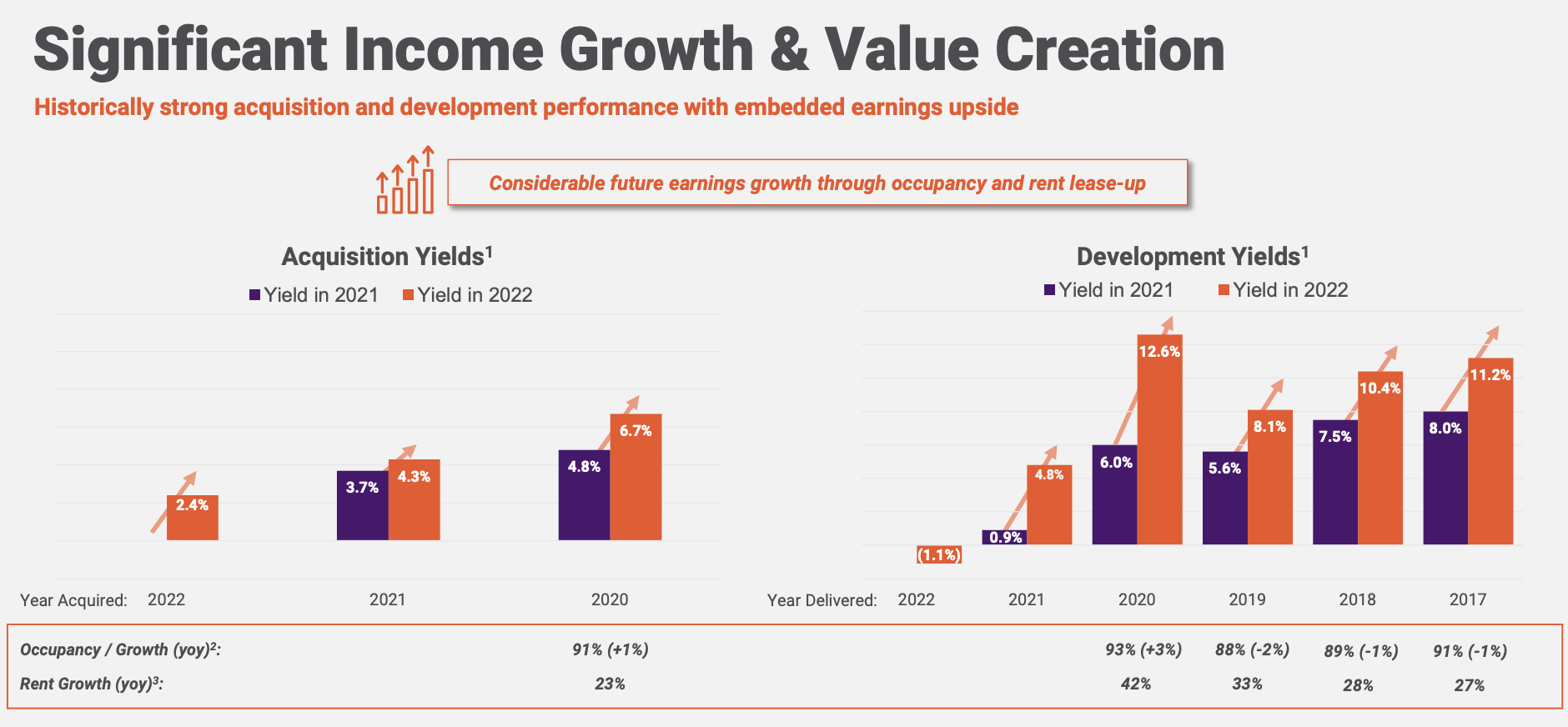

Since early 2019, PSA has invested $8 billion in external growth, meaning acquisitions, development, and redevelopment of properties. This has increased the portfolio size by 26% (more than 40 million square feet), making it one of the biggest expansions in the company's history.

The yields on these acquisitions and developments are high. Yields on 2020 acquisitions are currently at 6.7%, up from less than 5.0% in 2021. Development yields are in double-digit ranges with occupancy rates close to 90%, which is decent.

{kind=link}

With that in mind, investors have one question on their minds: when is dividend growth coming back? The bad news is that the word "dividend" was mentioned zero times in the most recent earnings call .

However, in its 2Q22 earnings call , the company's comments suggested that a hike in 2023 is on the table.

[...] it's been some time and growth has been strong. It's that as well as taxable income increasing that is likely to increase our dividend over time here as we move forward. And that's something that we highlighted at Investor Day as well as taxable income increases. We'll be poised to increase the current return to our shareholders. And that is, as we move forward into 2023, something that will begin to be more of a topic.

Not only are investments paying off, but the company also continues to enjoy a favorable business environment, which is key - especially in light of high rates and falling consumer sentiment.

A Favorable Business Environment - Given The Circumstances

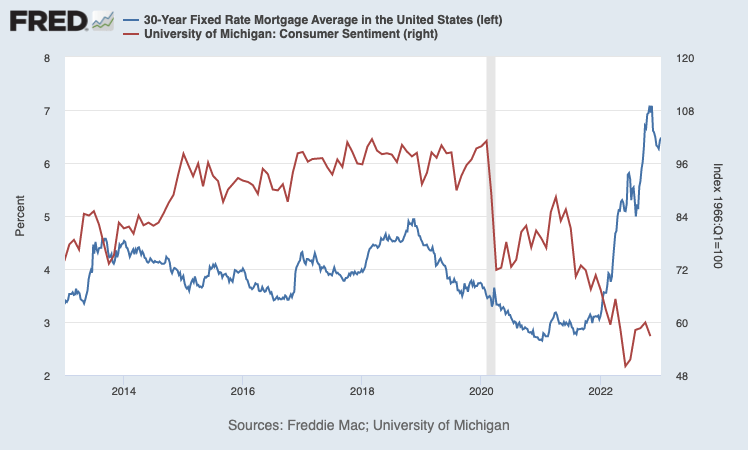

First of all, we're dealing with a semi-favorable business environment. A situation where mortgage rates are at multi-decade highs and consumer sentiment is imploding is far from favorable.

Federal Reserve Bank of St. Louis

{kind=link}

This situation is also the reason why REITs are selling off. REITs started to gain downside momentum when yields accelerated. As a yield proxy, I'm using the 20+ year government bond ETF ( TLT ) in the chart below.

I believe the surge in rates is an opportunity. After all, we get to buy great REITs at better prices.

What matters is that the industry is not suffering from higher rates. We are not seeing structural damage that could hurt the financial health of PSA and its peers.

This is what PSA commented on the macroeconomic situation in November:

As demand has remained very good, existing customers, too, are staying longer, giving us the ability to optimize rate increases and occupancy. On a macro basis, new supply of competitive product has been flat to down from peak deliveries in 2019. Nationally, markets have been able to absorb the more subdued pace of new development. Our view is that new development will also be static for the near term as risk levels tied to development have increased, particularly due to city approval time frames, higher component costs and the dramatic increases in the cost of construction lending.

With this said, it has become harder to predict the economic environment we are heading into with record inflation and consensus that the recession is imminent. We are, however, highly confident we have excellent tools to maneuver changing macro conditions.

The December Yardi Matrix National Self Storage Report confirmed this.

This report looks at key numbers like pricing and new supply, which are very important in an industry with low entry barriers.

Yardi Matrix finds a mix of weakening pricing and demand, yet at elevated levels. New supply is very subdued due to headlines like higher rates and construction costs.

Street rates continued to decelerate in November, largely due to typical seasonal patterns. Despite the drop from peak levels, the bigger picture shows street rates are healthy, as they are still more than 10% higher than they were prior to the pandemic.

[...] occupancy remains high and operators are focusing on increasing rates for existing customers. Meanwhile, the development pipeline is anticipated to gradually slow, as banks have become reluctant to write construction loans, which means that new starts will decline once projects under construction are delivered.

[...] Though storage is well positioned relative to other property sectors, the economy is a potential headwind.

Again, this does not mean that there's no more downside. It means that we don't need to worry too much about the health of self-storage companies in our portfolios.

I believe that real estate, in general, is due to experience some more weakness as the Fed will have to tighten more aggressively than expected to contain labor inflation - among other inflation components. It also needs to do it quickly to avoid an increase of close to $600 billion in potential debt servicing costs for the US Treasury in the years ahead.

It also helps that PSA remains in a good spot, which I will cover in the next part of this article.

Valuation

PSA is expecting to generate between $15.35 and $15.75 in core FFO per share on a full-year basis. This is based on at least 13.5% same-store revenue growth, between 6.0% and 8.0% growth in expenses, and at least 15.4% growth in net operating income growth.

Occupancy rates remain healthy as well. As of December 31, 2022, the average occupancy rate was 92.4%. That is down from 94.8% when the pandemic resulted in very high occupancy rates.

The average contract rent per square foot was $23.02 as of December 31. That's 15.3% higher compared to the prior-year period. This also means that rates continued to climb after a strong third quarter with 17.7% rent growth.

If we ignore future expected growth, the company is trading at 17.6-18.0x 2022E core FFO. The industry median is 18.0x, which makes PSA relatively more attractive, given higher returns than its industry, and its ability to benefit from this.

Takeaway & Game Plan

Real estate stocks aren't doing so well recently. High rates, weakening consumer sentiment, and the outlook that rates might have to remain high for at least four more quarters are hurting investors' willingness to buy REITs - or physical real estate, for that matter.

While I do not expect the Fed to suddenly become dovish, I do like the opportunity these sell-offs provide. I decided to make REITs a much larger part of my portfolio. That is based on the fact that some stocks offer a tremendous mix of growth and value and the fact that I expect even better buying opportunities in the months ahead.

My current real estate exposure is just 6.1%.

While Public Storage has a terrible dividend scorecard and underperformance, I continue to believe in its ability to turn into an outperformer again. The company has bought a lot of high-quality assets in the past few years, it has a great, high-margin business model, a very healthy balance sheet, and the ability/willingness to boost its dividend again.

I am closely watching PSA, and looking to aggressively add to my position this year.

(Dis)agree? Let me know in the comments!

For further details see:

Why I'm Aggressively Buying Public Storage This Year