ABNB - Why I'm Going To Trim My Position At Airbnb To Buy Booking Holdings

2023-11-28 23:28:55 ET

Summary

- Booking Holdings is a strong business with experienced management, high returns on capital, and a solid growth future.

- The company faces competition and potential threats from big players like Google, but the current stock price offers a favorable risk/reward ratio.

- BKNG's main mission is to create a comprehensive travel system, offering flight booking, accommodation reservations, car rentals, and restaurant reservations through its various platforms.

- Airbnb faces significant regulatory challenges ahead, while Booking offers a similar yet distinct service, without such risks.

- The current price is truly a bargain for long-term investors while considering the significant Google risk.

My Thesis

I believe that Booking Holdings ( BKNG ) is one of the best businesses in the world. It has everything I look for in a company: good and experienced management with great incentives, high returns on capital, excellent free cash flow generation, a solid growth future, high returns to shareholders in the form of buybacks, and a robust balance sheet. It is also the leader in its space.

However, it's not all rosy; otherwise, the stock would be way up, I suppose. It faces intense competition, and big players such as Google ( GOOGL ) could pose a threat to its business in the future.

Despite these risks, I think the current price, offering around a 6% free cash flow yield, tilts the risk/reward game in investors' favor. Additionally, I see risk at its main direct competitor, Airbnb ( ABNB ), and in my view, trimming my position at Airbnb and transferring to Booking is not a bad idea.

Booking's Business

So, Booking's main mission is to create an all-encompassing system for travel, starting from flight booking to hotel or villa search, and then transportation or car rental. Moreover, after that, you could reserve a table through its OpenTable platform. It achieves this through its main website and app, Booking.com, which is the world's leading brand for booking online accommodation reservations, based on room nights booked. It is also the number one app in the travel space. Additionally, it has five other platforms that operate in this space: Priceline, specializing in the cost-conscious customer; Agoda, the Asia specialist; Rentalcars, without further explanation; Kayak, which compares travel itineraries; and OpenTable, a restaurant reservations platform. Booking is working hard to integrate its platforms, as Glenn Fogel, the CEO, believes that to beat the competition, Booking has to deliver the best product, and yes, that also includes AI.

The advantage of operating multiple brands is that Booking can try different marketing strategies for each one and also reach different types of customers and geographies.

Booking profits from fees collected from travelers and travel service providers, but it can also benefit from the Google/Amazon ( AMZN ) model. In this model, Booking can leverage its huge user base. Businesses that want to feature their locations at the top of the search page will pay Booking to promote their locations for higher visibility in search results. In my view, Booking needs to focus on this segment, given the profitability we've seen from this ad model on other platforms like Amazon and Google.

Another aspect I appreciate about Booking's business is its global and diversified nature. As demonstrated by the recent quarter results and the Israel war, it only affected 1% of Booking's revenue. More importantly, the CEO mentioned that travel demand is always present. Despite the decline in the first week of the war, people are returning to travel. He also noted that this was the trend seen in Eastern Europe following the Ukrainian war. Booking's portfolio consists of:

2.7 million properties in over 220 countries and territories and in over 40 languages, consisting of over 400,000 hotels, motels, and resorts and 2.3 million homes, apartments, and other unique places to stay.

Another aspect that bothers me about Airbnb, which is essentially okay with Booking, is the regulatory pressure. People don't like their building to become a sort of motel, with luggage arriving at night and perhaps even parties. This puts pressure on cities to restrict short-term rentals. Another reason is that short-term rentals are taking apartments away from potential long-term residents, and the US already has a housing shortage . The third reason is that hotels pay more taxes compared to short-term rentals. We see this aspect unfolding in New York recently , and I worry that this trend will spread to cities worldwide. Because Booking's main business is hotels, it does not face this kind of regulatory risk and also provides different types of accommodations.

What I appreciate about the CEO's statements is that Booking is aware of the AI revolution and is taking steps to integrate chatbots and other aspects into its platforms. Essentially, in the future, you won't have to deal with the annoying task of booking hotels and flights. The ambition is for it to happen as automatically as possible. With Booking's whole ecosystem integration, they can potentially provide the entire travel experience in-house, automatically. In June , Booking introduced its AI planner:

Travelers can ask the AI Trip Planner general travel-related questions, as well as more specific queries to support any stage of their trip planning process, including scoping out potential destinations and accommodation options, providing travel inspiration based on the individual traveler's needs and requirements, as well as creating itineraries for a particular city, country or region.

And Glen Fogel is well aware of the possibilities of this revolution:

The recent developments with generative AI are accelerating the work we've been doing for years with machine learning to enhance and improve every aspect of the customer experience on our platform, whether it's optimizing the right order to display a hotel's photos to surfacing the most relevant reviews. Our new AI Trip Planner is simply the next step in our ongoing journey to explore how we can bring even more value, and hopefully enjoyment, to the entire trip planning process.

The Main Risk

The main risk I see, and probably every investor who has looked into Booking's business, is the threat from Google and Apple ( AAPL ). Booking is generating great profits from its operations and, therefore, is attracting tech superstars with a huge user base to compete in this arena. Booking provides an excellent service and has a massive user base, but players like Google have the ability to integrate those services into their already popular apps, like Maps. Google has Google Flights, and its Maps include transportation options and attractions; integrating hotels into it is an easy job. Look at how Booking describes it in their 10-K:

Google's online travel offerings have grown rapidly in this area by linking travel search services to its dominant search functionality through flight, hotel, and alternative accommodations meta-search products, and by integrating its hotel meta-search products and restaurant information and reservation products into its Google Maps app.

They acknowledge it as a threat, and their response is to become the best ecosystem for travel planning by providing the best and most innovative service, leveraging their already strong brand.

Booking isn't new, and Google's services aren't either. However, I believe there's room for multiple companies to operate in this space and profit well from it. People value brand loyalty, and they are connected to it, making them resistant to switching easily, especially if the service is superior.

If Booking can deliver a superior service and maintain its brand value, it will grow, even with alternatives from the mega-tech companies. For example, the transportation app Moovit thrives in Israel despite the significant alternative of Google Maps. People like and are accustomed to their service, and I wouldn't say there's a significant advantage over Maps. Even though Moovit is an Intel-acquired startup, it continues to thrive here despite the dominance of the Google giant. There are plenty of examples. Even within Google, the most popular navigation app here in Israel is Waze, which is owned by Google but still outperforms (by far) Maps in popularity.

Growth And Profits

Booking operates in the travel and tourism industry, which has solid organic growth. According to McKinsey , the forecast is optimistic:

Travel and tourism GDP is predicted to grow, on average, at 5.8 percent a year between 2022 and 2032, outpacing the growth of the overall economy at an expected 2.7 percent a year.

This can be derived from factors like population growth, age expansion, and the thriving global middle class, as well as the transition of some countries to newfound prosperity, like India.

Booking is expected to grow faster than the market, with analysts projecting around an 8% CAGR for the next five years, similar to the past five years' growth of 8% CAGR. However, you could anticipate a surprise in those numbers, as Booking has consistently beaten analysts' expectations in the last decade, though not by a large margin. This kind of growth indicates a market share capture as it expands its 34% (apps) market share by taking business from small travel agencies, with online travel booking gaining more share.

Besides this solid growth, what makes this stock undervalued, in my view, is the fact that the EPS growth projection is much higher. Analysts project a 15% CAGR, which seems reasonable with margin growth. In the last quarter , the FCF margin was at 31%, compared to the 26% average of the last 5 years, with much of the average being impacted by the COVID bump. Another crucial aspect of real growth is the average 4.7% annual share count reduction evident in the last 5 years. These buybacks suggest that even if there is no market share capture and Booking grows at market growth, we can still expect high single-digit growth in the FCF per share figures.

Booking presents high and stable margins. I appreciate high margins because they promise that even in an inflationary period, the company won't cut investment initiatives and/or buyback or dividend programs. Booking also has superior margins compared to its competitors:

These margins are a direct factor in what I consider the most important metric, alongside top-line growth: returns on capital. Recent research by Morgan Stanley indicates that a high and potentially growing spread between a company's weighted average cost of capital and its return on invested capital are contributing factors to potential winners. Booking is a master in this space, creating enormous shareholder value in contrast to its competitors. This is probably also why Google is interested in this space. Booking ratios are not only high but also stable, indicating long-term quality and value creation.

Solvency And Return To Shareholders

In my view, BKNG has a robust balance sheet ; it holds more cash than total debt, can cover its interest more than nine times, boasts a current ratio above 1, and an Altman Z-score above 5. While it may not be as debtless as Airbnb, for example, I perceive the risk as very low. About $5 billion of the total debt carries a relatively high interest rate of around 4%, while the rest is under 3%.

As I mentioned earlier, a significant part of the thesis revolves around stock buybacks, as they add growth to the EPS figures on top of solid organic growth. With a 23% reduction in stock count in the past 5 years, it matches the pace of other notable share cannibals, like those of AutoZone ( AZO ) and Lowe's ( LOW ), for example.

In addition to these buybacks, Booking is relatively not diluting its shareholders with SBC when compared to peers. BKNG is not paying any dividends, which is common for growth stocks.

{kind=link}

Great Management

I'm impressed with Booking CEO Glenn Fogel. He has been with the company for almost 24 years, knowing it and the industry from scratch. I recently listened to him speaking on a podcast, and I am quite impressed. I believe that his vast experience within the company and the company's success since he took on the role in 2017 are strong indicators of future outperformance.

Moreover, despite not having meaningful insider ownership like Brian Chesky (Airbnb CEO and founder), he is motivated by a great compensation plan. With only a 3% annual cash salary and 75% performance-based (mostly equity) on revenue, EBITDA, Total Stockholder Return, and non-financial goals. I would be pleased if they set goals based on returns on capital, similar to other companies I've analyzed, such as Lowe's and Zoetis ( ZTS ).

Director compensation at Booking is also mostly equity-based, and I appreciate that, as everyone making decisions is aligned with shareholder targets.

{kind=link}

Valuation

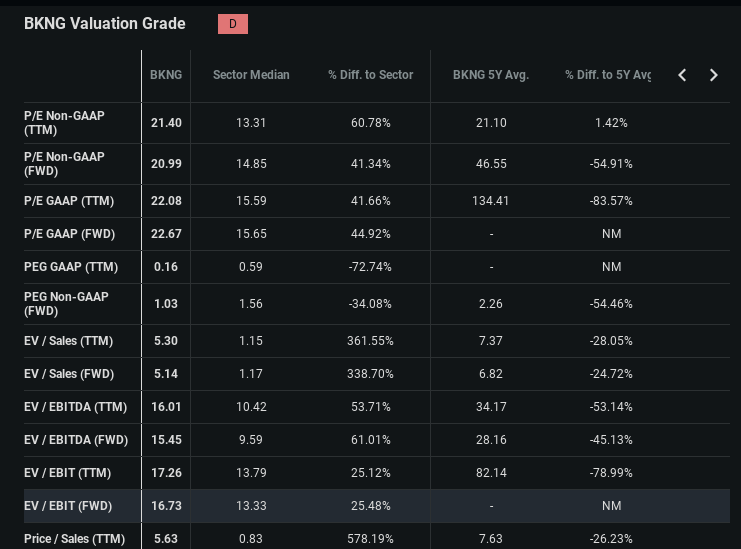

In my view, the main point is that you rarely find high-quality companies trading above a 5% free cash flow yield. Booking is currently trading at a 6.7% FCF yield. This might be due to the rise of Airbnb or the threat from Google, but for a company with such high returns on capital and solid growth, it is cheap in my opinion. Moreover, in most valuation multiples, it is trading below its 5-year average, providing room for multiple expansions, perhaps back to the average. However, those averages are heavily impacted by the ZIRP era, so I wouldn't solely rely on them to be the same.

{kind=link}

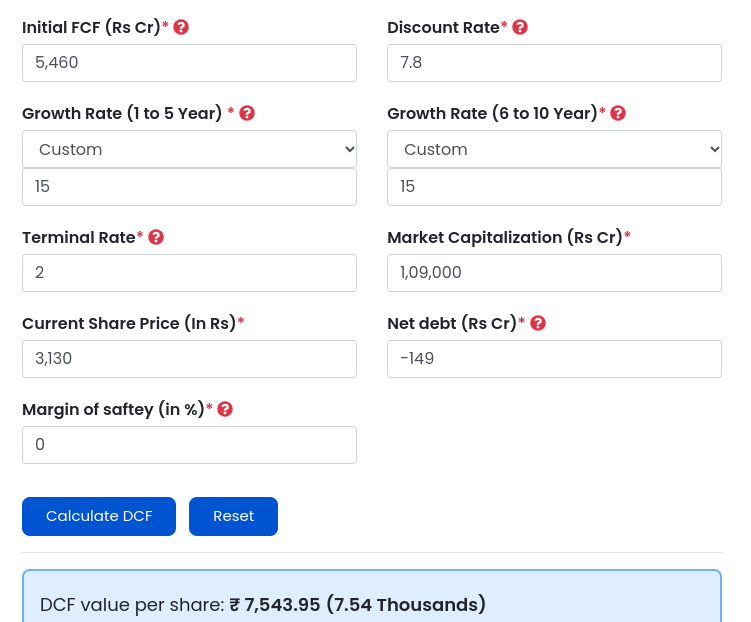

Moving on to the DCF, I'll consider the bear, bullish, and base case scenarios.

I'm using a 26% FCF margin as the average over the last five years, with the FY23 revenue forecast. The terminal rate is set at 2%, the WACC is 7.8%, and for the bullish case, I'll use the analysts' EPS forecast of 15% CAGR. The derived result is a stock with bargain quality, showing an undervaluation of 58% and an intrinsic value of up to $7.5K per share.

{kind=link}

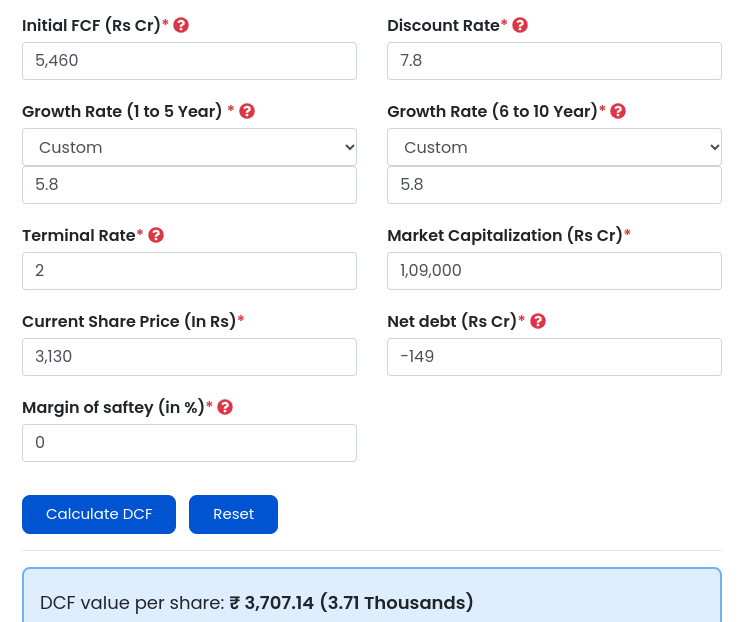

This is an optimistic case; let's consider a more bearish scenario. The inputs remain the same except for the growth rate, set at 5.8% to align with the market-anticipated growth. This assumes no buybacks, which could enhance growth but also no margin drop. Even with this bearish case, the stock still appears undervalued by 15%.

{kind=link}

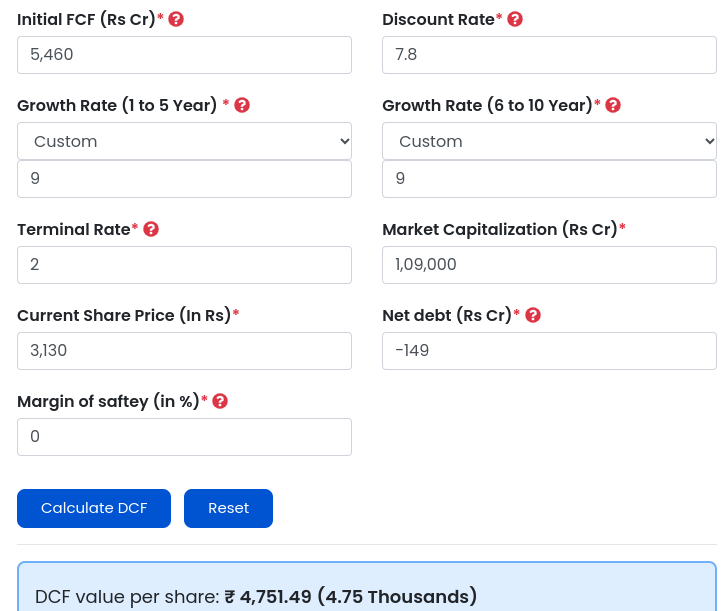

Now, let's consider the base case, assuming no market share growth but only market growth with an annual share reduction of about 4%. The growth rate will be at 9%. In this scenario, we get an undervalued stock by 34%.

{kind=link}

A 34% undervaluation for such a quality stock, in my view, makes me want to own it despite the significant Google risk.

Conclusions

Well, Booking is a great company. It has excellent management in my view, practices sound capital allocation, boasts a high Return on Capital, and exhibits solid organic growth. It is actively engaged in the AI race and is building its integrated travel ecosystem.

The main risk, posed by Google and Apple, shouldn't be underestimated. However, I do believe the current price compensates for such a scenario. If Google were to enter the scene, Booking might lose some market share, but it won't disappear.

Considering the risk-reward balance, in my view, Booking is a strong buy stock. In the near future, I'm planning to trim some of my Airbnb positions to make room for BKNG.

What are your thoughts on the stock?

For further details see:

Why I'm Going To Trim My Position At Airbnb To Buy Booking Holdings