IITSF - Why I Own Intesa Sanpaolo

2023-04-30 21:46:00 ET

Summary

- Banks may be a risky investment, as we have seen in recent months.

- Intesa Sanpaolo is the leading bank in Italy, a country where I see positive trends for wealth management banks.

- Intesa is a big dividend payer, and its de-risking activity has made the dividend even safer.

Introduction

It is always looming over the horizon. It unsettles us. It concerns the world.

I am talking about banking crisis. No matter what happens, the shock of the Great Recession is still alive in our memories and at any news of a banking undergoing financial distress fear comes out once again.

Though I think it is reasonable to be a little wary of banks (Warren Buffett recently stated he believes some banks are set to go bust in the near term), I must say I do have a few positions in the industry and I feel rather comfortable as a shareholder.

The largest position I have is Intesa Sanpaolo S.p.A. ( OTCPK:ISNPY ), the largest Italian bank.

Summary of previous coverage

An Italian bank? Are you serious?

I bet these questions may arise. In my previous coverage, I have already outlined my view on the Italian banking system and the Italian economy overall.

To cut a long story short, I believe the European banking system, and the Italian one in particular, have been able to recover from the financial crisis and the sovereign debt crisis by implementing a massive de-risking action, while making sure to stay well-above a CET1 ratio of 10%.

Furthermore, Italian household wealth is around €11.4 trillion, €5.2 of which in financial assets. Italians deposit in the banking accounts something around €30-40 billion per month. Usually, this goes along with low household debt. However, with high inflation, Italian banking deposits are shrinking a bit. Nonetheless, the amount of cash parked in banking accounts is still huge and, if inflation lasts longer than expected, many Italians will need to convert part of their cash savings into other assets that offer a hedge against inflation.

Here Intesa comes into play. It is the largest bank in Italy, but it is also the largest wealth management player in the country. I am bullish on the wealth management industry. Secondly, it has become very efficiently run with a cost/income ration among the best ones in Europe. With a revenue generated mainly from fee-based businesses and interest rates rising, I picked Intesa as one of the best deals to play this trend.

Update

Currently, Intesa has been on the radar of SA Top Rated Stocks, always part of the first five picks together with another Italian Bank, UniCredit ( OTCPK:UNCRY ). It seems like it is still heavily undervalued, with a price/book ratio still below 1.

Currently, Intesa is the market leader in Italy in every different activity a bank can handle, as we can see below.

Intesa FY2022 Presentation

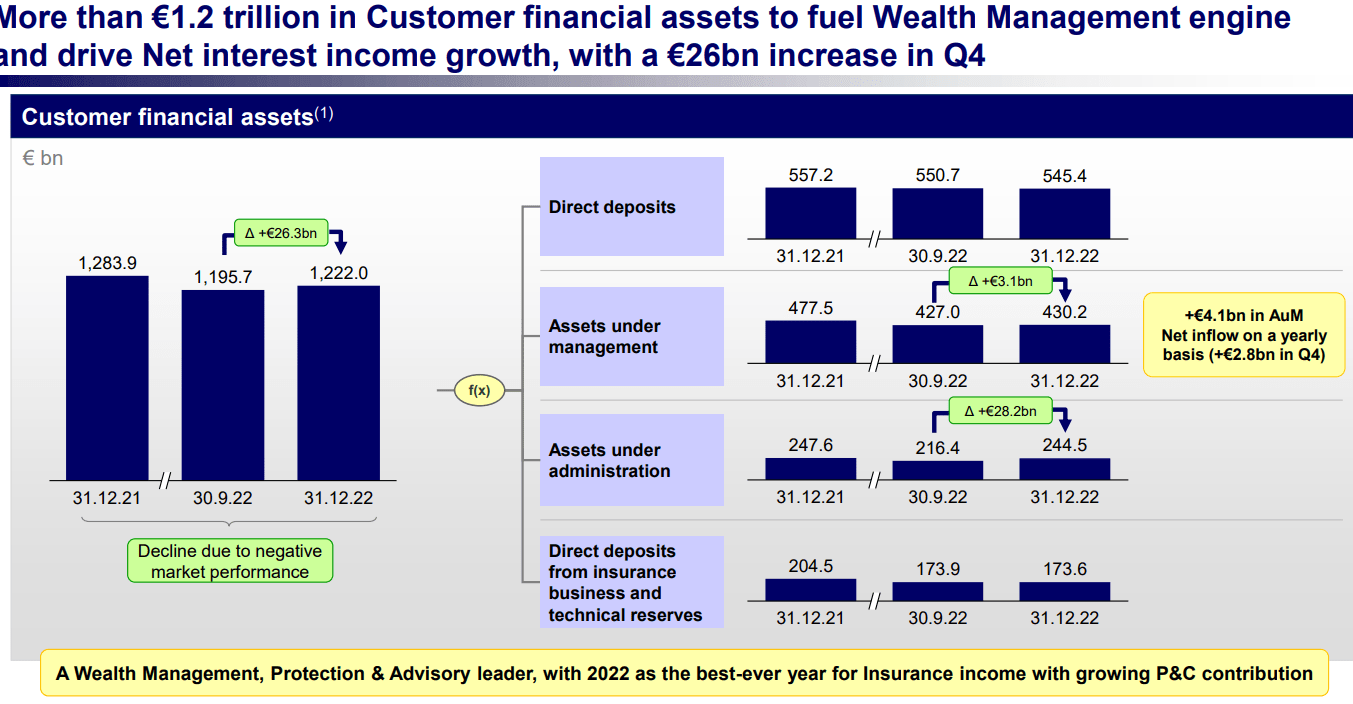

As I already mentioned, I am particularly interested in Wealth Management, where Intesa is the market leader. As we can see below, it has more than €1.2 trillion in customer financial assets. Customers deposit are over €500 billion and AuM is well above €400 billion, with a net inflow of €3 billion per year.

{kind=link}

But is this enough to make it a good investment in a time where investors are once again worried about banks?

I think Intesa seems to be able to weather different kinds of storms.

First of all, it was quick in exiting Russia, losing €1 billion of net income. However, the bank was still able to reach its best net income result since 2007, with €4.4 billion reported .

Sticking true to its dividend policy, the bank paid to its shareholders €3 billion in dividends, with a payout ratio of 70%. This was coupled with a €3.4 billion buyback program that has just recently been completed.

Secondly, at the end of 2022, the bank reduced by another €29 billion its risk-weighted assets to strengthen its capital position and achieve a CET1 ratio of 13.5%. Just to understand how much Intesa improved, we should know that in 2011, during the sovereign debt crisis, Intesa had only an 8.9% CET1 ratio.

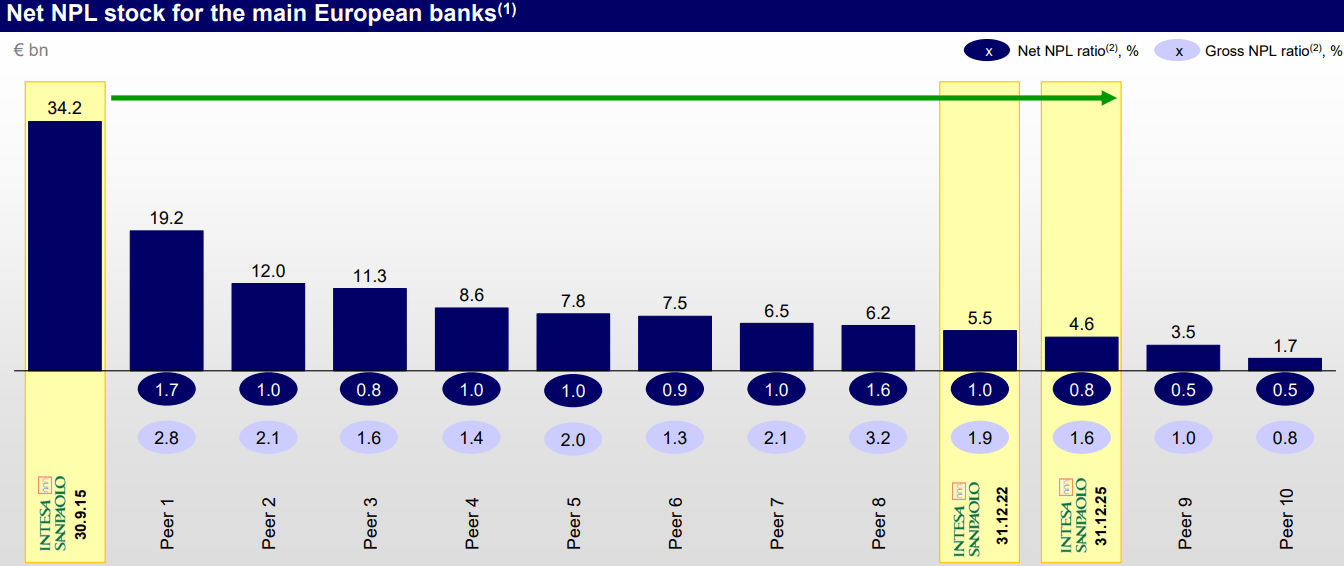

As we can see, Intesa is currently one of the best European banks in terms of NPL stock it carries.

{kind=link}

The Italian Central Bank has repeatedly shown how total NPLs held by Italian banks has been reduced from €240 billion in 2017 to just €30 billion in January 2023.

At the end of last year, the average capitalization of Italian banks was higher than the average of the largest European institutions and more than double the level recorded just before the global financial crisis. In addition, by the same date, the ratio of non-performing loans to total loans had fallen to a low level, in line with the European average.

Intesa is also strong because of its efficiency, with a cost/income ratio of 50.9% at the end of 2022 and a return on capital of 8.5%, which is quite good for a bank.

Rising interest rates are also providing a further tailwind for Intesa, that I expect to have a net interest margin above €12 billion at the end of 2023.

Intesa is also set to pay its semi-annual dividend on May 24th, with ex-date two days before on May 22nd. The recent drop in price may offer, thus, a buying opportunity before the dividend is paid.

Conclusion

In the past year, Intesa has outperformed the market by growing almost 30%. At the same time, its valuation metrics still show a very cheap stock compared to the industry. True, there might be some country risk baked in, but, as I have tried to show, it seems to me as if Europe and Italy are now in a stronger position compared to the past. Intesa has made it clear to aim at becoming leaner and more efficient by 2025, targeting a cost/income ratio below 50%. At the same time, it is developing more and more its higher margin businesses, such as wealth management. Last, but not least, Intesa's balance sheet has been significantly de-risked in these years. With net income increasing also thanks to higher interest rates, Intesa shows the strength to support its the almost 7% dividend while hinting that it might also approve another buyback program.

For further details see:

Why I Own Intesa Sanpaolo