BFFAF - Why I Sold BASF

2024-01-08 23:48:50 ET

Summary

- In the article, I discuss my reasons for selling BASF, and I look not only at the company but also at the industry and the "Big Picture".

- I explain why I not only think we are heading for a recession but are also at the end of several long-term cycles, making a depression more likely.

- And in such an environment, holding stocks from the technology, financial, and material sectors is not the best idea as these sectors usually underperform.

I sold BASF SE ( BASFY ). I sold the stock a few days ago (on the first trading day of the year) and I sold the stock almost for the same price as I bought it (it traded about 0.2% higher than at the time of purchase about 22 months ago). Of course, I collected dividends in the last two years and therefore had an annual return of around 7%, which is acceptable in my opinion. It was certainly not the best investment, but I also didn’t lose money.

In the following article, I will explain my reasoning why I sold BASF, and I will follow a top-down process and start by looking at the economy (or even society) as a whole, followed by looking at the different industries (especially the industry BASF is operating in) and finally I will look at the individual company – BASF.

But I will not only try to explain my reasons why I sold BASF. I also want to explain my “superior framework” and give some more hints and guidance on what to expect and what to do about stocks at this particular time because the reason for selling BASF has not only to do with the company itself but also with the industry it is operating in and especially with the “Big Picture”. However, let’s start by explaining my I bought BASF and what my bullish thesis was.

Bullish Thesis

In March 2022 I wrote an article explaining my reasoning why I bought BASF. And in the conclusion – despite seeing BASF as a solid investment, I was already a bit cautious:

BASF is not the perfect investment and not the type of company I usually search for: It is a rather cyclical business, and we can argue if the company has a wide economic moat around its business. However, BASF is one of the major (and oldest) businesses in Germany and one of the leading chemical companies in the world. And at current valuation multiples, the stock seems to be too cheap to ignore in my opinion. Eight times earnings are extremely cheap for a business, that was able to grow in the mid-to-high single digits over the long run. And additionally, dividend investors get a tempting 7% dividend yield right now.

And I concluded my article with the following prediction:

But I also don't know if I will be holding BASF for the long term. It could happen, that I will sell BASF again in the next few quarters or years.

Looking back and reading these sentences now, I think it is interesting that I already had a feeling that I might not hold on to BASF for too long. But I probably expected to sell the stock for a higher price as I wrote in the above-mentioned article that I assumed BASF could be worth as much as €100. That certainly did not happen.

And in December 2022 I wrote another article arguing why BASF is still a good long-term investment. I mentioned the high dividend yield again and pointed out the several long-term growth drivers leading to higher stock prices for BASF in the years (and maybe decades) to come. So, the question here is why I changed my mind now. Of course, it is 13 months later, and a lot can change in 13 months, but the major reason I am selling right now (or sold) is the big picture.

The Big Picture

I am often arguing that we should look at longer timeframes when trying to assess a business and not just look at the last few quarters. And usually, I am looking at one or a few decades – this time, however, I am trying to look at a century and longer. If you know my articles, you know that I am rather bearish for the coming years, and I have written from time to time why I think we are at the end of a long-term cycle.

The best summary and description of these long-term cycles stems from Ray Dalio, and I will focus on his book and writings here. The thesis here is that we are extremely close to the end of three long-term cycles that don’t always go hand-in-hand but can overlap and create turmoil, difficult times, or major crises (whatever you would like to call it). These three cycles are:

- The long-term debt and capital markets cycle

- The internal order and disorder cycle

- The external order and disorder cycle

External Disorder Rising

That the external order (the order between states) is “collapsing” can be seen by the rising number of conflicts (and wars) and the number of deaths due to these wars. This is not only the conflict between the established superpower United States and the rising superpower China (which thankfully seems further away from a hot war at this point), but also the Gaza conflict or the war in Sudan and Russia trying to establish itself as a global superpower by regaining power over countries that were once part of the Soviet Union.

{kind=link}

Internal Disorder Rising

Additionally, we see the internal order shifting to disorder in many countries around the world – including the United States, many European countries, Argentina, and probably several other countries I don’t know about. In most cases, we see radical forces gaining control (or at least winning elections) and we see the division of societies with populism rising on the left and right. This is including rising wealth gaps.

Long-term debt cycle

And finally, the long-term debt cycle and market cycle seem to be close to their end and at extreme levels. This is including extremely high debt levels all over the world and increased debt-to-GDP ratios (especially in the United States). And in such a scenario, necessary interventions from the FED are becoming more frequent, but due to extremely low interest rates (close to zero for more than a decade) and already using quantitative easing in an aggressive way are making it more difficult for the FED to respond. And this happens at a time when asset prices are extremely inflated (due to the FED’s policy in the last decade).

{kind=link}

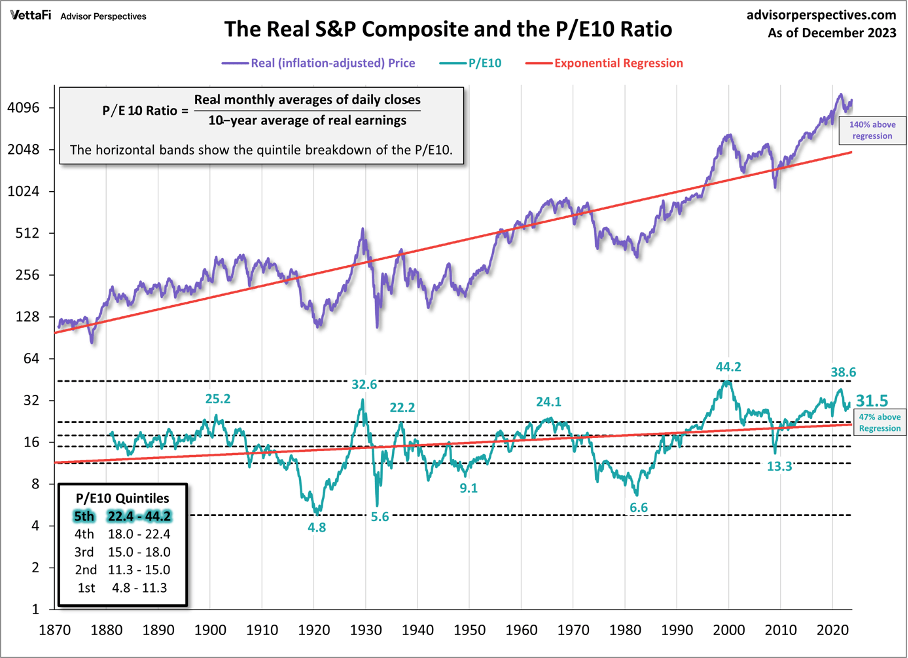

The S&P 500 trading for a CAPE ratio of 31.5 (after already trading for 38.6 a few quarters ago) is an example of inflated asset prices.

And all three are typical signs that we are at the end of a long-term cycle, and at the end of such cycles, we usually see a “lost decade” for the stock market, many conflicts within countries, cold and hot wars between countries, the destruction of wealth and the shift of power between different groups, organizations, and countries. And all in all, this is not the best time to hold stocks. And as the stock market (the S&P 500) reached its previous all-time high again (and we see the very real potential for a double-top) now is the time to trim my positions and restructure my portfolio (now is defined here as the next few weeks or months).

And to provide a different perspective on the bigger picture that is also looking at cycles, but from a slightly different angle, I would like to refer you to the articles of Avi Gilburt (see here for example). And although the perspective is different, the conclusion is the same – challenging times most likely lie ahead of us.

Sidenote: In the last few weeks, I started working on this topic and will certainly publish some extensive articles to explain my thinking and my view of the world in more detail.

Looking at Industries

When assuming a basic assumption that we are heading towards a recession (or worse) we can look at the different industries. And although not every recession is the same, we can see patterns and sectors that are often performing quite well during recessions and other sectors that usually perform horribly during recessions.

And it is not very surprising that sectors perform differently in the same market environment. Just when looking at the difference between goods and services, the difference between discretionary and non-discretionary spending, it becomes obvious that not every industry is performing the same.

Stansberry Research

Stansberry Research published a chart showing the performance of the different sectors in the last recessions. And when looking at the stock price performance usually financials, information technologies, and materials are among the sectors performing worst and it is never a good idea to hold these stocks during a recession.

When looking at the performance of the sectors in the last few decades we usually see a performance during recessions (and bear markets) that is not great. These sectors are not the best pick for a recession. Hence, we should think long and hard about what stocks in these sectors we should hold on to in a recession.

Looking at BASF

And finally, we are looking at BASF. Because not every business in a certain industry is performing the same way. And although stocks from the technology, materials, or financial sectors perform not great during recession does not mean every single stock has to perform that way. And even during recessions some individual technology or material stocks perform well.

One of the strongest arguments we can still make for BASF is that the stock is really cheap. Assuming a share price of €48 and taking the trailing twelve months EPS (adjusted numbers) of €3.05 we get a P/E ratio of 15.7. When using the fiscal 2022 adjusted EPS of €6.96 BASF is even trading for 6.9 times earnings. But we should not forget that these are adjusted numbers, and we should always be cautious about adjusted numbers. However, when taking the free cash flow of either the last four quarters (which was €3,084 million) or of fiscal 2022 (which was €3,333 million) we get a P/FCF ratio of 12.6 to 13.6.

And the stock is certainly cheap, but risks remain. The first is BASF being hit rather hard by a recession and to be honest, when looking at the results in the last few quarters, BASF is in trouble already.

In the third quarter of fiscal 2023, sales declined 28.3% year-over-year from €21,946 million in the same quarter last year to €15,735 million this quarter. EBIT before special items was €1,348 million in Q3/22 and declined to €575 million in Q3/23 – resulting in 57.3% year-over-year decline. And instead of €1.01 in earnings per share in Q3/22, BASF reported a loss per share of €0.28 in Q3/23. Of course, we can look at the adjusted earnings per share which were €0.32 in Q3/23 but compared to €1.77 in the same quarter last year this is a decline of 81.9% year-over-year. The only glimmer of hope here is free cash flow, which increased 13.1% year-over-year from €1,295 million in the same quarter last year to €1,465 million this quarter.

{kind=link}

To get a bigger picture we can also look at the results for the first three quarters, but the picture is quite similar to the third quarter. Sales for the first nine months declined from €68,003 million in the same timeframe last year to €53,051 million this year – resulting in 22.0% YoY decline. EBIT before special items declined 46.0% YoY from €6,505 million in the same timeframe last year to €3,514 million in the first nine months of 2023. Adjusted earnings per share declined from €4.67 to €2.03 – resulting in a decline of 56.5% YoY and adjusted earnings per share declined 56.8% YoY from €6.85 to €2.96. And while free cash flow was rather high in Q3/23, free cash flow in the first nine months was only €488 million – a 33.9% decline compared to €738 million in the same timeframe in 2022.

{kind=link}

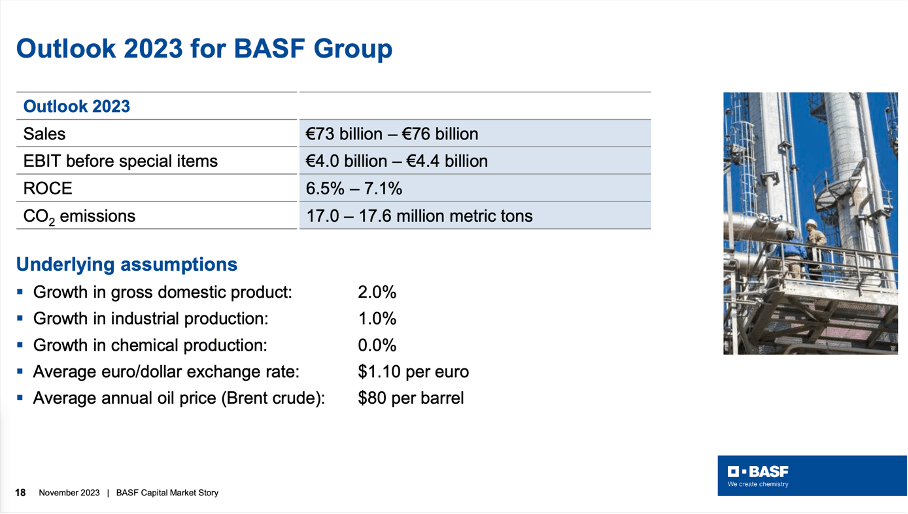

And honestly, I don’t know if the guidance for fiscal 2023 is still realistic. BASF is expecting €73 billion to €76 billion in sales which would mean between €20 billion and €23 billion in sales in the fourth quarter (much higher than in the previous two years).

Aside from fundamentals declining and leading to lower earnings per share – which should also be reason enough for a lower stock price – there is a second risk right now. Even if the fundamental performance of the business does not justify a sell-off, the risk of the stock declining anyway is still rather high. Sentiment is driving the stock price performance – at least in the short-to-medium-term and when I am correct with my prediction and the U.S. stock market declines 50%, 60%, or even 70% how likely is it that BASF – a business that is not so recession-resilient can withstand the negative sentiment. It seems very likely that BASF will sell off and trade for even lower valuation multiples.

We assume that BASF is already trading for a low stock price and as the stock is already trading for a low valuation multiple which might limit the downside risk. But just one thought-provoking impulse: Let’s just assume adjusted earnings per share on a trailing twelve-month basis decline another 50% to only €1.50 and investors assume that any valuation multiple above 10 is not justified – in such a scenario we are looking at a stock price of €15 for BASF. I am not saying this will happen, I am just saying we should think about what could happen.

Bottom Line

When looking not only at BASF and the materials (or chemicals) industry but also at the bigger picture, the bottom line for me can be summarized like this: I am trying to reduce my risk as I expect the next few years to become very, very rough and I must decide what stocks to hold and what stocks to sell.

There are still several stocks I haven’t made up my mind about – Novo Nordisk ( NVO ) and Starbucks ( SBUX ) for example - but I started to trim and sell positions. And as the materials and financial sector are not the best assets to hold during a recession, I sold BASF and I also sold Svenska Handelsbanken ( SVNLF ) – the only bank I was buying and holding in the last few years.

I certainly don’t know what will happen in the years to come and of course, I could be wrong. But thinking about how much risk one is willing to take at this point – after a 14-year bull market – might not be the worst idea in the world.

By the way: I will still rate the stock as "Hold" as I don't think you should short the stock and there are certainly reasons for holding the stock (the low valuation for example).

For further details see:

Why I Sold BASF