SVC - Why I Sold Spirit Realty And Reinvested In Spirit Realty's Preferred Stock

2023-04-17 09:00:00 ET

Summary

- SRC has persistently traded with a higher cost of capital (especially cost of equity) than its peer group.

- Since his appointment as CEO in 2017, Jackson Hsieh has done yeoman's work to improve the portfolio and balance sheet and to earn a lower cost of capital.

- Alas, the market never cooperated, so Hsieh had to adapt to a higher cost of capital by taking calculated risks in higher-yielding properties.

- We look at some examples that could indicate SRC is taking more and more risk in its acquisitions in order to maintain a spread over its cost of capital.

- While the move may ultimately prove too skittish, I recently sold SRC in order to reinvest in the REIT's preferred stock.

Spirit Realty Capital ( SRC ) is a diversified net lease REIT with a spotty history.

For a few years, I was optimistic that SRC had turned a new leaf and refined itself into a company that could earn a valuation multiple somewhere in the same neighborhood as most of its net lease REIT peers. Today, I'm much less confident about that.

Though SRC now trades at a 7% dividend yield, I recently sold the stock at a yield of about 6.6% and reinvested the proceeds into Spirit's discounted 6% Series A Preferred Stock ( SRC.PA ) at a dividend yield of 7% in order to lock in a 7% yield that is much safer than the common dividend.

To fully explain why I ultimately chose to sell SRC and move into its preferreds, though, we need to travel back to the distant past of 20 years ago...

A Brief History of Spirit Realty Capital

Spirit Realty was founded in 2003 as "Spirit Realty Finance Corporation." Originally, it was a private company, then went public in the mid-2000s, then was taken private again, and finally went public once more in 2012 with its new name: "Spirit Realty Capital."

In the last 20 years, the REIT has had four different sets of top management teams, and the strategy has shifted slightly with each one.

The first set of managers from 2003 to 2010, led by Spirit co-founder and then-CEO and President Chris Volk (who would later go on to co-found and lead STORE Capital), grew Spirit to about $3 billion in assets, nearly a third of which (30% by total rent at the end of 2010) were Shopko stores.

Side note: Shopko was a once-popular chain of department stores that traded as a public company during the 1990s and early 2000s but was bought out by a private equity firm in 2005. High debt and weakening sales ultimately led to the retailer's bankruptcy in the late-2010s.

{kind=link}

The second set of managers from 2011 to 2015, led by then-CEO Tom Nolan as well as then-COO Pete Mavoides, grew the REIT to $8 billion by 2015 while materially lowering exposure to Shopko (14% at the end of 2014).

But there were differences between the respective investment strategies of Mavoides, at the time Spirit's President and COO at their headquarters in Scottsdale, Arizona, and Nolan, who acted as the remote CEO in Dallas. These differences led Mavoides to leave Spirit and found Essential Properties Realty Trust ( EPRT ) a year later in 2016, where he remains CEO today.

A year after Mavoides left in 2015, then-CEO Tom Nolan moved the headquarters of the company from Scottsdale, Arizona to Dallas, Texas. In the process, over 80% of Spirit's employees left the company. Many of those, including Spirit's former CIO Gregg Seibert, went on to work under Mavoides for EPRT. So, with the move to Dallas, Spirit's management team was almost completely revamped. Thus: management team #3.

While Nolan did continue to lower Shopko exposure (ending 2015 at 9.1% of the portfolio), Spirit under management team #3 did not have a particularly strong cost of capital to work with nor a consistent investment strategy when it came to acquisitions. A handful of Shopko stores were sold in 2015, but mostly the Shopko exposure fell because Spirit was filling its portfolio with a mix of solid investment grade retail properties like Lowe's ( LOW ), Tractor Supply ( TSCO ), and Best Buy ( BBY ) and non-investment grade retail properties like movie theaters, car dealerships, and restaurants like Applebee's.

In 2016, Spirit hired former investment banker Jackson Hsieh as President and Chief Operating Officer. Perhaps knowing the REIT's credit controls needed improvement, Hsieh's role would include "oversight responsibility for credit underwriting, new investments, and portfolio and asset management."

Spirit Realty Capital

At the end of 2016, Shopko remained Spirit's largest tenant at 8.2% of total rent. But at this point Shopko's issues were well-known, and there were no good options to deal with these big-box properties.

In May 2017, Nolan stepped down as Chairman and CEO. No explanation was given for his departure, but perhaps none was needed. The announcement of his departure was days after Q1 2017's earnings report, which revealed an earnings miss after "an unusually high number" of retail and restaurant tenants had not paid any rent year-to-date.

Hsieh was immediately installed as Spirit's new President & CEO (management team #4). He came in with a strong sense of what needed to be done to right the ship. He was quoted as saying:

Our plan moving forward will focus critically on credit and tenant concentration challenges in order to enhance the profitability of our platform. We remain committed to growing the company in a manner that enables us to strengthen our balance sheet, preserve liquidity and create long-term stockholder value.

A few months after Hsieh's ascension to the CEO desk, Spirit announced that they would spin off a significant portion of their weaker properties into "Spirit MTA REIT" in order to separate them from the core assets and ultimately dispose of them.

In Q2 2018, SRC completed the spinoff and subsequently cut its dividend to right-size it with the remaining portfolio.

In January 2019, after its private equity sponsor failed to find a buyer for the retail chain, Shopko filed for bankruptcy and began the process of liquidating and closing many of its stores, including many owned by Spirit MTA REIT. Later that year, in September, Spirit completed the sale of SMTA to the externally managed Hospitality Properties Trust, which changed its name to Service Properties Trust ( SVC ).

Finally emancipated from the albatross of Shopko and most of Spirit's other weaker properties, SRC enjoyed one of the best years in its history in 2019. On a price basis alone, the REIT outperformed its larger and more venerable net lease peers:

With Hsieh's newfound, well-defined focus on properties leased to large, publicly traded, higher credit tenants (perhaps not entirely investment grade, but just below it), a new life seemed to have been breathed into Spirit Realty.

An investment strategy had formed. Quality controls had been put in place. The plan to restore Spirit's image in the investor community and ultimately improve its cost of capital seemed promising. And leverage was coming down. Spirit ended 2019 with debt to EBITDA of 4.9x, down from 6.2x at the end of 2016 and 7.6x at the end of 2014.

SRC 2016 Annual Report

At the end of 2019, Spirit's portfolio derived about 44% of rents from investment grade or equivalent tenants, and ~49% of rents came from public companies.

...And then along came COVID-19. In the Q1 2020 earnings release , Spirit reported collecting 70% of contractual rent in April. The stock price halved from February to April.

Ultimately, though, Spirit delivered AFFO per share of $3.31 in 2020, down only slightly from 2019's $3.34.

Spirit's Cost of Capital Constraint

Unfortunately, SRC's trajectory of multiple expansion in 2019 seems to have been halted by COVID-19, then later by rising interest rates, and now, perhaps, by the looming threat of recession.

You can hear the disappointment in Hsieh's voice in conference call after conference call, despondence over the market's cold shoulder to SRC shares and perhaps some frustration that his efforts have not been recognized.

But in truth, even in 2019, SRC had a ways higher to go before its price-to-AFFO was in the same general range as its peers. When I first wrote about SRC in December 2019 (see Here ), I was bullish, because I thought management was making all the right moves to earn that higher AFFO multiple.

Another goal was to upgrade the strength of the balance sheet so as to earn a credit upgrade to BBB+. This, in turn, would have driven SRC's cost of equity lower and allowed the company to compete for the highest quality net lease properties.

Alas, though, that cost of equity discount has persisted for SRC, despite the numerous times I argued here on Seeking Alpha that the REIT is " Unfairly Maligned By The Market " and " Higher Quality Than The Market Thinks ." And the goal of a credit rating has not been achieved.

Let me illustrate this for you. We'll illustrate SRC's cost of capital disadvantage by looking at the simplest measurement of cost of equity: the AFFO yield.

The lower the AFFO yield, the lower the cost of capital and thus the lower the cap rate can be on acquisitions while maintaining an adequate (accretive) spread. Of course, all net lease REITs operate with debt leverage as well, which lowers their overall cost of capital. But the best net lease REITs operate with common equity at 60% or more of their capitalization, which in turn helps them to achieve a better credit rating and thus lower their cost of debt in a positive feedback loop.

So, having a lower AFFO yield is an important and unalloyed good for a net lease REIT.

In 2019, when things were looking up for Spirit, the REIT's AFFO yield averaged 7.6% but never got lower than 6.3%. Meanwhile, that year, the average investment grade retail net lease property traded at cap rates of 6% or under, while investment grade industrial properties traded at 5% or under.

Compare that, for example, to Agree Realty's ( ADC ) average 2019 AFFO yield of 4.4%. ADC's AFFO yield got as low as 3.8% and as high as 5.2% in 2019.

Likewise, Realty Income's ( O ) 2019 AFFO yield averaged 4.8%, going as low as 4.2% and as high as 5.5%.

National Retail Properties ( NNN ) averaged an AFFO yield of 5.1% in 2019, going as low as 4.7% and as high as 5.8%.

| 2019 Avg. AFFO Yield |

| 2019 Lowest AFFO Yield |

| Spirit Realty |

| 7.6% |

| 6.3% |

| Agree Realty |

| 4.4% |

| 3.8% |

| Realty Income |

| 4.8% |

| 4.2% |

| National Retail Properties |

| 5.1% |

| 4.7% |

Even in the best of times, SRC had a cost of capital disadvantage.

And then, in perhaps the ideal environment for net lease REITs in 2021, SRC's AFFO yield averaged 7.1% but again never got lower than 6.3%. And again, IG retail commanded cap rates of 6% or less, and IG industrial commanded cap rates of 5% or less.

| 2021 Avg. AFFO Yield |

| 2021 Lowest AFFO Yield |

| Spirit Realty |

| 7.1% |

| 6.3% |

| Agree Realty |

| 5.0% |

| 4.7% |

| Realty Income |

| 5.5% |

| 4.9% |

| National Retail Properties |

| 6.7% |

| 6.4% |

Again, SRC's AFFO yield couldn't break lower than 6.3%.

And since the beginning of 2022, SRC's stock price has been the worst performer among its peer group:

Does this mean that SRC has performed poorly in terms of fundamentals? No , absolutely not.

See, for example, some metrics from 2022:

| Gross RE Assets At 12/31/21 |

| 2022 Acquisitions |

| 2022 Acq. / 2021 Assets |

| 2022 AFFO/Sh Growth |

| SRC |

| $7.479 billion |

| $1.547 billion |

| 20.7% |

| 9.5% |

| ADC |

| $4.601 billion |

| $1.59 billion |

| 34.6% |

| 9.2% |

| O |

| $35.909 billion |

| $9.0 billion |

| 25.1% |

| 9.2% |

| EPRT |

| $3.151 billion |

| $0.937 billion |

| 29.7% |

| 14% |

| NNN |

| $7.444 billion |

| $0.848 billion |

| 11.4% |

| 4.9% |

| WPC |

| $15.918 billion |

| $1.4 billion |

| 8.8% |

| 5.2% |

SRC managed to grow its AFFO per share at a high single-digit clip last year in spite of its cost of capital disadvantage. Management was able to raise capital opportunistically and find higher cap rate deals that fit with their cost of capital constraints. The lowest quarterly average cash acquisition cap rate last year was 6.34%, while the highest was 7.27%.

Whether it's stocks, bonds, or real estate properties, high yield investing is tricky. Higher yields = higher perceived risk.

Slipping Underwriting Standards?

To be sure, SRC has a lot going for it.

For starters, incentives appear to be heavily aligned between shareholders and management. 100% of equity-based compensation for SRC executives is tied to performance-based metrics. Last year, those metrics weren't hit, so management's compensation took a significant hit.

And despite the stock selloff, Hsieh continues to show confidence in the portfolio. Here's an excerpt from the CEO Letter in the 2022 Annual Report :

We believe that our portfolio will perform at very low volatility from a cash flow perspective, similar to that of an investment grade tenanted real estate portfolio.

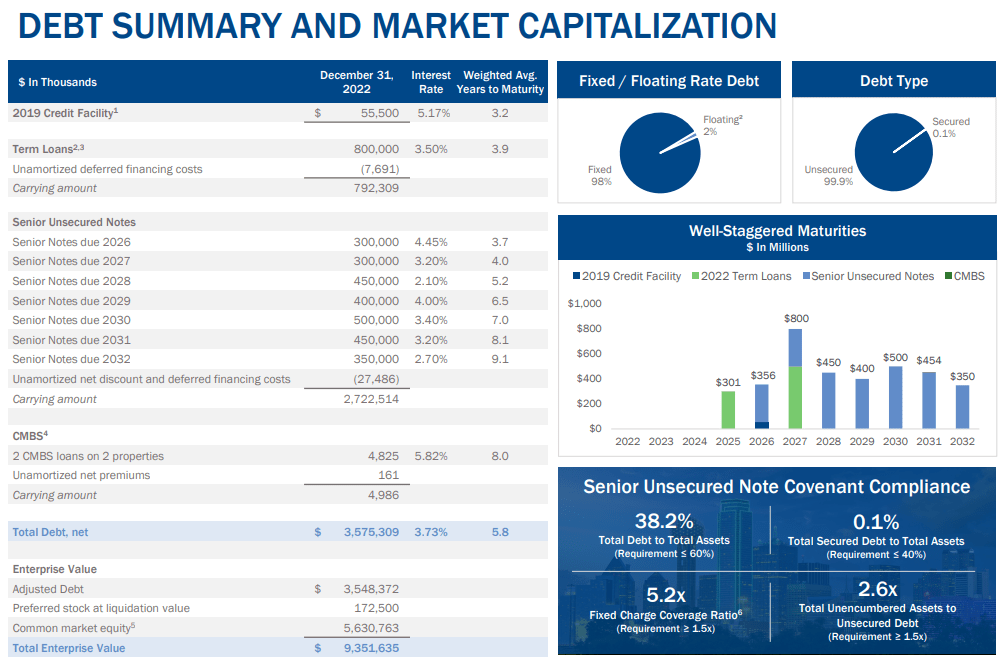

What's more, SRC's BBB rated balance sheet is in excellent shape, with virtually all debt fixed and unsecured. No debt matures until 2025.

{kind=link}

It doesn't get much better than this as far as the balance sheet is concerned.

That said, competition for net lease properties has been fierce in the last several years. There's no such thing as a free lunch, and there's no such thing as a higher cap rate without higher risk. Like the bond market, pricing in the net lease market is far more efficient than in the stock market. While a stock can be bought with one click, net lease investors spend months doing due diligence before closing on properties. So do their brokers, bankers, etc.

Thus, when a net lease property is priced at an above-average cap rate, it almost certainly isn't merely from overly pessimistic investor sentiment. It's from some real, tangible risks.

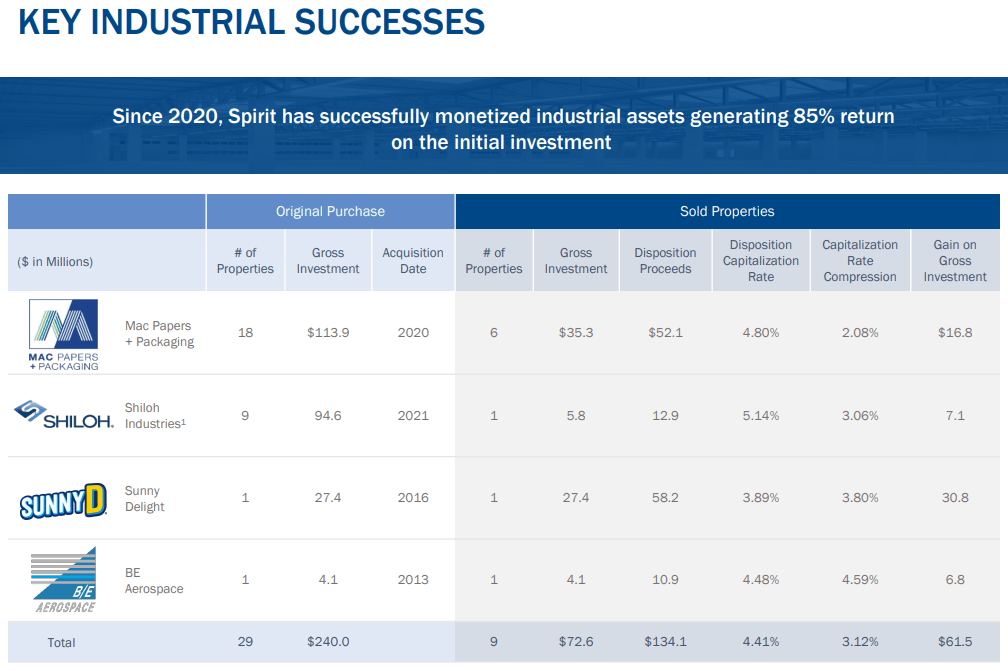

Admittedly, some of these calculated risks have paid off handsomely, as some industrial tenants have earned credit upgrades after SRC's initial purchase, and some of these higher cap rate properties were sold at huge gains on the original purchase prices.

{kind=link}

But notice that all of these success story properties were purchased in years when SRC had access to either a strong cost of equity (2013) or a strong cost of debt (2016, 2020, 2021) or both.

My worry is that, because of SRC's high cost of capital (specifically cost of equity), the REIT is now moving up the risk curve and acquiring higher-risk / lower-credit properties in order to secure higher yields.

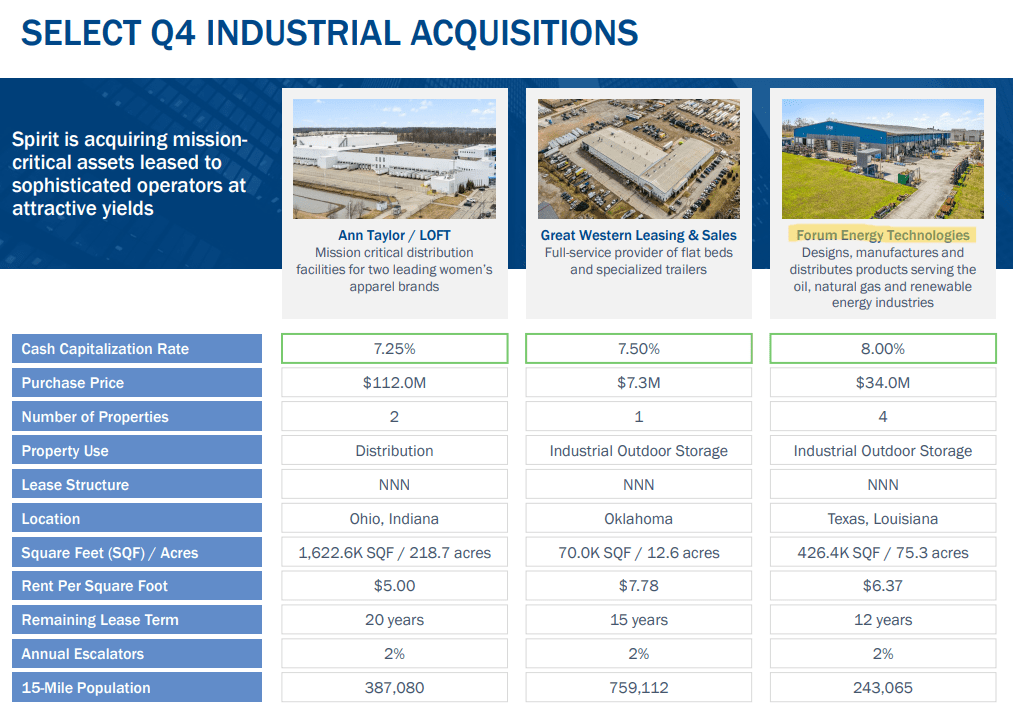

What gives me this impression? Well, consider the three industrial property acquisitions that management recently highlighted:

{kind=link}

All three of the highlighted industrial acquisition deals from Q4 2022 have tenants that are backed by private equity firms. That's not necessarily a bad thing on its own. There have been some PE-sponsored success stories, such as Academy Sports and Outdoors ( ASO ). But for every Academy, there are numerous other stories of companies that have languished after PE buyouts, burdened by high debt, neither growing nor dying - simply acting as dairy cows for the PE firms to milk.

90% of SRC's Q4 acquisitions were sale-leasebacks, which suggests that the majority of the quarter's investments were for PE-owned tenants. Why? Because during a time when interest rates have risen to the degree that they have, monetizing real estate through sale-leaseback deals becomes cheaper for highly leveraged PE-backed businesses than refinancing debt with more debt.

Ann Taylor / LOFT were once owned by Ascena Retail Group before the company went bankrupt during the pandemic, and several of its clothing brands (including these two) were sold to a private equity firm. Admittedly, though, these facilities are state-of-the-art with very low rents per square foot.

Case Study: Forum Energy

Forum Energy Technologies ( FET ), on the right side of the image above, is a public company, so their financials are publicly available. The company has a CCC+ credit rating, and over 99% of its substantial debt burden matures in a single year: 2025. The 2025 debt is in the form of 9% convertible secured notes. They are secured by "substantially all the company's assets."

FET has the option to pay down this debt with cash on hand before the August 2025 maturity date, but with what cash? Even in 2022, a great year for energy-related businesses like FET's, the company's gross profit only barely edged higher than its SG&A expenses (overhead).

In fact, since the oil price collapse in 2015, FET has consistently been unprofitable.

It would not be surprising to see FET go bankrupt sometime in the next few years, at which point it wouldn't be surprising to see many of its subsidiaries liquidated rather than bought out and operations continued.

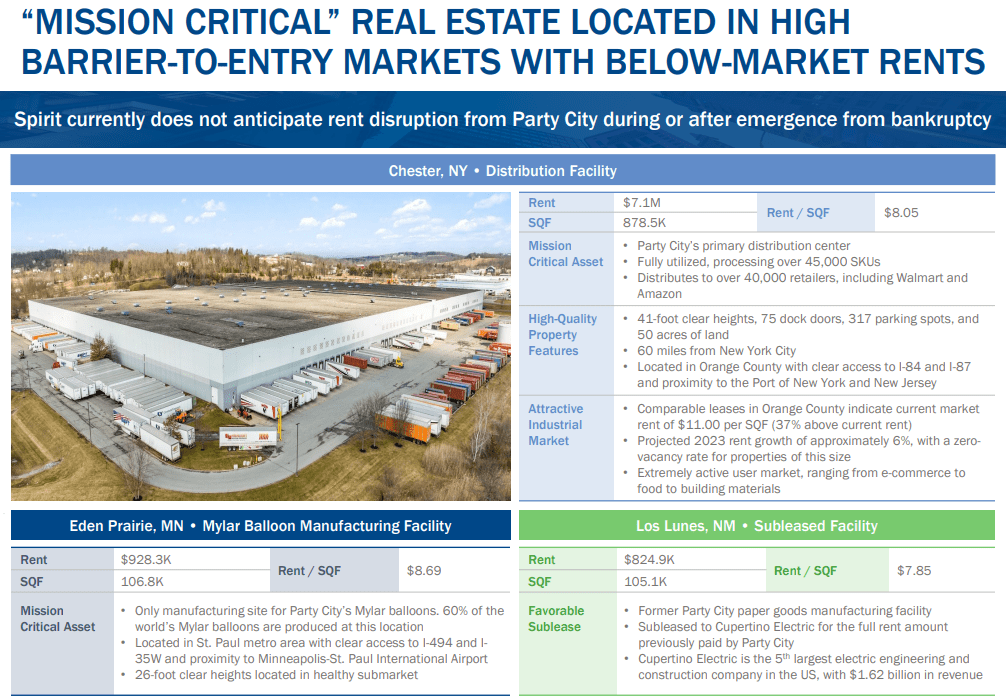

That's what makes FET different, in my estimation, than the case of the industrial properties leased to Party City that SRC purchased in 2019.

{kind=link}

Yes, the Party City properties share in common with the FET properties low rent per square foot. But they also share in common that, at the time that SRC purchased the properties, the companies were teetering on the verge of bankruptcy.

What they may not share in common is mission-criticality and irreplaceability. One of those Party City properties is responsible for producing 60% of the world's mylar balloons.

By contrast, FET's buildings appear to be mostly older and lacking in mission-criticality or specialization in themselves. Plus, the locations appear to bear a bit more risk. The Louisiana location, for instance, is in South Lafayette, about 30 miles from the Gulf Coast - a.k.a. hurricane alley.

To be fair, these properties are leased at such low rents per square foot that it would seem reasonable to assume that replacement rents could be obtained at similar or higher levels in a releasing scenario. Even so, the above-average risk from poor locations and/or older buildings that would require substantial capital investment to re-tenant shouldn't be ignored.

Shopko properties generally had pretty low rents per square foot, too. That didn't make them good investments.

Forum Energy is just one example. SRC invested a total of $312 million in Q4 2022, and Forum accounts for just $34 million of that.

But is Forum illustrative of a broader erosion in tenant credit quality? I fear it might be.

Consider these changes in portfolio-wide metrics:

| Q4 2019 |

| Q4 2022 |

| Unit-Level Reporting |

| 51.1% |

| 50.2% |

| Investment Grade Tenancy |

| 23.5% |

| 19.5% |

| Private Equity Owned Tenants |

| 27.7% (Q1 2020) |

| 29.4% |

These are subtle changes, to be sure, but they are not in the right direction. More PE-backed tenants, fewer investment grade ones, and slightly less unit/property-level financial reporting to SRC.

This strikes me as evidence that SRC is incrementally increasing the risk of acquisitions in order to secure yields high enough to maintain a spread over its relatively high cost of capital.

Although the properties SRC kept after the spinoff of SMTA REIT in Q2 2018 are mostly higher in quality, I fear that management has been forced to gradually mix in more and more lower-quality and higher-risk properties since then because of its cost of capital constraint.

Some of these investments have turned out quite well, such as the handful highlighted above. But I worry that during a recession, many of these tenants could "suddenly" default on rent in a manner similar to what occurred in Q1 2017, an event that ultimately led to a CEO change, a spinoff of weak properties, and a dividend cut.

This is the curse of a high cost of capital. It forces REITs to take higher risks. They are calculated risks, to be sure, but risks nonetheless. Those higher risks often result in losses. And even if those losses are not devastating, they are enough to keep the stock cheap and the cost of capital high, which reinforces the cycle.

SRC's cost of capital is not just marginally higher but significantly higher than its peers...

| Forward AFFO Yield (4/15/23) |

| Spirit Realty |

| 9.4% |

| Agree Realty |

| 6.0% |

| Realty Income |

| 6.5% |

| National Retail Properties |

| 7.6% |

...which leads me to believe that the REIT must be taking more-than-marginally higher risks in order to secure the level of cap rates and the attractiveness of lease terms that it's getting.

At the very least, surely not all of its non-investment grade property acquisitions from the last few years will turn out to be winners. And it doesn't take that many stinkers to ruin an otherwise good portfolio.

Lower-Risk Alternative: Spirit's Preferred Stock

In the wake of the Silicon Valley Bank collapse in early March, SRC.PA inexplicably sold off from around $24.15 to as low as $21.12. I found this baffling, because SRC has almost nothing to do with SVB. The market apparently came to its senses pretty quickly, because SRC.PA's price has almost climbed back to its pre-SVB-collapse level already.

Given my reservations about SRC's cost of capital and potential higher risk-taking, trading the (at the time) 6.6%-yielding common shares for the 7%-yielding preferred shares made sense to me. I bought SRC.PA at $21.45, giving me 16.6% upside to par in addition to the 7% yield.

The preferreds' call date already passed in October 2022, but given SRC's cost of capital issues, I doubt redeeming them is a high priority for management at this point.

SRC.PA's capitalization at par value is $172.5 million, which makes up about 1.9% of SRC's current enterprise value.

If the preferred stock sells off to the low $20 territory again, investors might consider buying it like I did.

Bottom Line

Why has SRC been the worst performer among the peers cited above since the beginning of 2022? I would argue that it is because the market perceives SRC to be taking above-average risks with its recent acquisitions.

SRC has guided for capital deployment of $700 to $900 million this year. Dispositions should be between $225 to $275 million, and free cash flow after dividends should be around $100 million (assuming SRC collects as much contractual rent as they think they will). The REIT has no forward equity available to draw, but they can draw down on a $500 million delayed-draw term loan with a floating interest rate that currently has an effective yield of 5.7%.

Put all of that together and you've got capital available for investments this year of $825 to $875 million.

Perhaps the greater concern than acquisitions, though, is how well SRC will be able to fare through a recession.

One of the biggest hopes of SRC bulls is that the REIT will be a buyout target for a larger peer like Realty Income or alternative asset management firm like Blackstone ( BX ). But Realty Income does not seem keen on more M&A after its recent Vereit acquisition, and Blackstone is not targeting net lease in its acquisitions.

Besides, if I am right that SRC is taking too much risk in its recent acquisitions, then potential buyers will discover that and be dissuaded.

If you are concerned about SRC's recession resilience as well as its cost of capital disadvantage, then you might consider joining me in switching to the preferred stock.

For further details see:

Why I Sold Spirit Realty And Reinvested In Spirit Realty's Preferred Stock